July 28, 2026

The Supply Chain Stress Test Lithium Markets Were Never Prepared For

Every commodity market carries within it the seeds of its own next crisis. During periods of abundance, capital flows toward volume and efficiency, systematically dismantling the redundancy that would otherwise buffer against shocks. The result is a supply chain that functions flawlessly in calm conditions and fractures precisely when resilience matters most. Lithium in 2026 is the clearest current example of this dynamic playing out in real time.

The lithium deficit from China and Zimbabwe supply cuts did not emerge from nowhere. It was constructed through years of rational economic decisions that concentrated production, processing, and investment into an increasingly narrow geographic and political footprint. Understanding why this matters requires looking past the price charts and into the structural architecture of how lithium actually moves from ground to battery.

When big ASX news breaks, our subscribers know first

How Concentration Risk Was Engineered Into the Global Lithium System

The economics of lithium supply favoured consolidation for decades. Australia's hard-rock spodumene deposits offered scale and consistency. Chile's Atacama brine operations offered low extraction costs. China offered unmatched downstream processing infrastructure. Capital followed these advantages, and the result was a global supply chain where three jurisdictions collectively dominated both upstream mining and the critical conversion stage that transforms raw concentrate into battery-grade material.

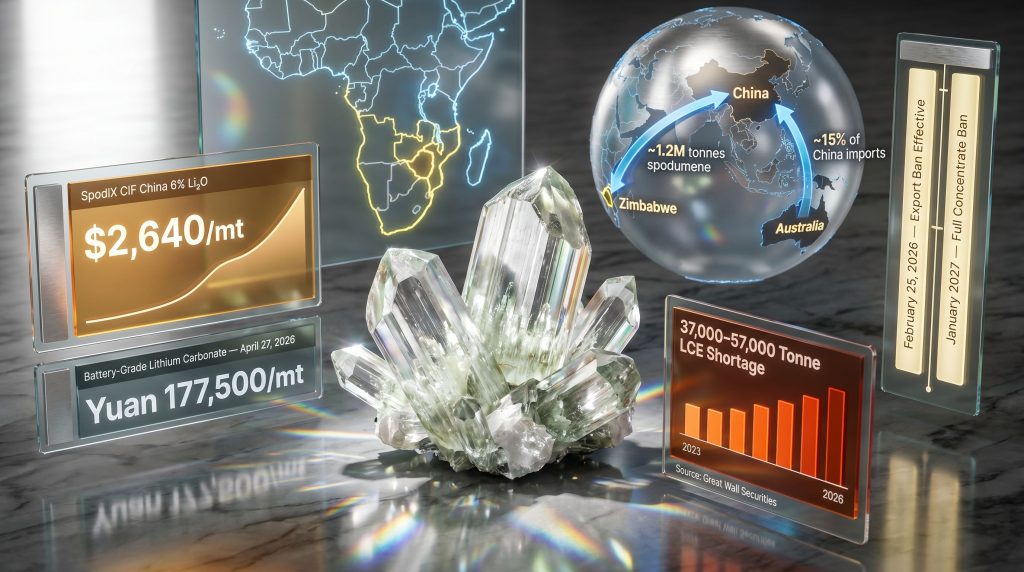

Zimbabwe's emergence as a fourth significant supplier initially appeared to offer meaningful diversification. By 2025, the country had grown into Africa's leading lithium producer, ranked fourth globally, accounting for approximately 10% of world mine output and exporting roughly 1.128 million metric tonnes of spodumene concentrate to China across that year alone. That volume represented around 15% of China's total spodumene imports, making Zimbabwe a genuinely material link in the global supply chain.

The diversification narrative, however, concealed a more nuanced risk. The overwhelming majority of Zimbabwe's lithium sector was owned and operated by Chinese capital. Zhejiang Huayou Cobalt controlled the Arcadia project. Sinomine Resource Group operated the Bikita mine. Chengxin Lithium Group, Sichuan Yahua Industrial Group, and Tsingshan Holding Group collectively held additional project positions across the country.

What appeared geographically as a fourth major supply jurisdiction was, in structural terms, an extension of the same Chinese-dominated processing ecosystem that already controlled the downstream end of the chain. Furthermore, this structural reality meant that spodumene extraction from Zimbabwe was, in practice, feeding a system with limited true independence from Chinese oversight.

"The critical insight here is that geographic diversification of mining locations does not produce supply chain resilience when those mines feed a single, concentrated processing system. True diversification requires redundancy at the conversion and refining stage, not just at the pit face."

The Overlooked Vulnerability in Lithium's Conversion Bottleneck

A detail frequently missed by generalist observers is that lithium's strategic chokepoint is not the mine itself but the chemical conversion facility. Spodumene concentrate typically assays at around 6% Li₂O when exported and must undergo roasting and leaching processes to produce lithium carbonate or lithium hydroxide suitable for battery manufacturing. China controls approximately 70% of global lithium chemical conversion capacity, according to assessments from the International Energy Agency and U.S. Geological Survey data on downstream processing infrastructure.

This means that even if a lithium mine is located in Australia, Zimbabwe, or Canada, its output typically passes through Chinese processing before reaching a battery cell manufacturer. When feedstock flowing into that processing system is disrupted, the effect does not stay contained at the national level. It propagates across every battery supply chain that depends on Chinese-converted lithium intermediates, regardless of where the raw material originated. Understanding how lithium mining works helps clarify why this conversion bottleneck is so consequential.

Zimbabwe's Export Restriction: The Policy Decision That Changed the Market

On February 25, 2026, Zimbabwe's government implemented an immediate ban on exports of unprocessed lithium concentrate and other raw minerals. The official justification centred on eliminating revenue leakages and accelerating domestic value addition, consistent with a broader resource nationalism trend that had been building across African mineral producers for several years. The timing was notable because it accelerated a transition originally anticipated for 2027, compressing the adjustment window for Chinese processors and global buyers who had been operating on the assumption of continued concentrate availability.

The policy framework that followed, reported by Reuters, introduced several structural conditions that will govern Zimbabwe's lithium exports going forward:

- Individual export quotas assigned to specific producers, replacing the previous open export model

- A maintained 10% export tax on lithium concentrates, creating a cost differential that incentivises domestic processing over raw export

- A mandatory local processing investment commitment required from all mining operators before January 2027

- A full concentrate export ban expected to take effect in January 2027, eliminating the transitional window currently in place

The January 2027 deadline deserves particular attention. Processing facility construction typically requires between 18 and 36 months from groundbreaking to commissioning, depending on complexity, equipment procurement lead times, and local permitting. A mandate issued in early 2026 with a January 2027 deadline creates an operationally impossible timeline for companies that have not already broken ground.

China's Simultaneous Domestic Tightening

Compounding the Zimbabwe disruption, China's internal lithium production environment tightened through stricter permitting reviews and elevated environmental compliance requirements, particularly affecting smaller and higher-cost domestic operations. Industry intelligence from S&P Global Commodity Insights and Fastmarkets documented this tightening through early 2026.

Critically, China did not impose export controls on lithium. The supply disruption originated entirely from Zimbabwe's sovereign policy decision. The significance of China's domestic tightening is that it eliminated the buffer capacity that might otherwise have absorbed a portion of the import shortfall. With domestic operations facing regulatory friction and imports from Zimbabwe curtailed, the feedstock availability for Chinese conversion facilities tightened from both directions simultaneously.

Quantifying the Market Impact: Prices, Deficits, and Supply Gaps

The pricing response to these concurrent disruptions was rapid and substantial. The following table summarises the key market movements recorded through late April 2026:

| Market Metric | Pre-Disruption Level | Late April 2026 | Change |

|---|---|---|---|

| Spodumene SpodIX CIF China (6% Li₂O) | ~$2,350/mt | $2,640/mt | +$290/mt |

| Battery-grade lithium carbonate (DDP China) | Prior period range | Yuan 177,500/mt | Two-year high |

| Lithium price trough (June 2025) | $8,259/t | $25,269/t (April 27, 2026) | +206% recovery |

The $290 per metric tonne increase in spodumene prices since the ban announcement encodes more than lost volume. It reflects the premium that market participants now assign to supply certainty itself, a qualitatively different signal from a simple volume-adjustment repricing. Battery-grade lithium carbonate reaching Yuan 177,500 per tonne DDP China by April 27, 2026 represented the highest price point in over two years, and a recovery of more than 206% from the June 2025 trough of approximately $8,259 per tonne.

Supply-demand modelling from Great Wall Securities estimated the resulting global lithium carbonate equivalent shortage at between 37,000 and 57,000 tonnes for 2026, against a market that had been broadly balanced to slight surplus entering the year. Zimbabwe's forecast 2026 production of approximately 124,000 tonnes LCE represented roughly 7% of projected global supply, meaning the effective removal of even a portion of that volume was sufficient to flip the market's directional balance.

Additional Regional Pressures Narrowing the Supply Buffer

Beyond Zimbabwe and China, several concurrent developments further reduced available supply flexibility. Indeed, as lithium supply tightens and low prices stall new projects, these regional pressures compound an already strained global picture:

- Conflict-related disruptions in Mali are constraining West African lithium output from projects in early development phases

- Jiangxi province lepidolite operations in China face ongoing regulatory and environmental scrutiny that is limiting expansion

- Australian hard-rock producers implemented output reductions in response to the 2024–2025 lithium market downturn, reducing the spot market buffer available to Chinese processors

- Seasonal EV battery production peaks are simultaneously increasing demand, compressing market balance from the consumption side

Resource Nationalism and the African Minerals Policy Shift

Zimbabwe's export restriction sits within a much larger continental and global pattern. Resource-rich nations across Africa, Latin America, and Southeast Asia have progressively shifted their mineral policies toward domestic value capture rather than raw material export. Indonesia's implementation of nickel ore export bans beginning in 2020 demonstrated that this approach, while disruptive in the short term, can successfully catalyse domestic processing investment. Zimbabwe appears to be applying a comparable template to lithium.

The structural incompatibility between this trend and the existing global supply chain model is significant. Supply chains built on the assumption of freely traded, low-cost raw material flows are now encountering sovereign policy barriers at multiple points simultaneously. This is not a temporary friction but a durable realignment of the terms on which mineral-rich nations engage with global commodity markets.

"The shift from raw material exporter to processed material supplier fundamentally changes a country's position in the value chain. Lithium concentrate that previously generated perhaps $2,350 per tonne can, after chemical conversion to battery-grade carbonate, command many multiples of that value. Producing nations have recognised this differential and are acting on it."

What Jurisdictional Stability Is Now Worth: The U.S. Strategic Response

The combined effect of the lithium deficit from China and Zimbabwe supply cuts has materially repriced the strategic value of lithium assets in stable, rule-of-law jurisdictions. This repricing is most visible in the United States, where Nevada has emerged as the primary domestic lithium development corridor. In addition, the US lithium supply project at Thacker Pass exemplifies how domestic development is being accelerated in direct response to these geopolitical pressures.

General Motors' $625 million commitment to Nevada lithium clay development signals that major industrial consumers are moving beyond policy advocacy and deploying direct capital into domestic supply security. This is a qualitatively different form of market signal from corporate sustainability pledges or lobbying positions. It represents a binding capital allocation decision by one of the world's largest vehicle manufacturers, placing a specific dollar value on supply chain independence.

Nevada's structural advantages for lithium development are well documented:

- Established hard-rock and clay mining infrastructure from legacy operations

- Proximity to U.S. battery manufacturing facilities concentrated in the region

- A mature, transparent permitting environment with established regulatory processes

- Workforce availability and technical services ecosystem built around mining operations

Understanding Lithium Clay Deposits: A Technically Distinct Resource Type

One aspect of Nevada's lithium opportunity that is frequently underappreciated by non-specialist observers is the geological distinction between lithium clay deposits and the spodumene hard-rock or brine operations that dominate global supply. Lithium clay mineralisation, typically hosted in sedimentary basin formations, presents different extraction and processing characteristics that have direct economic implications.

Near-surface clay deposits with consistent mineralisation across broad lateral extents are amenable to conventional open-pit mining methods, which carry lower capital intensity per tonne than underground hard-rock extraction. Furthermore, advances in direct lithium extraction methodologies have progressively improved recovery rates and cost structures, making clay-hosted deposits increasingly competitive on a global basis.

Grade is a critical variable in assessing clay lithium projects. Average grades above 2,500 ppm lithium are generally considered the threshold for economic viability under reasonable processing cost assumptions. Projects achieving average grades of 3,000 ppm or higher, with localised zones exceeding 4,000 ppm, occupy a meaningfully stronger economic position because higher feed grades reduce the volume of material that must be processed per tonne of product, directly lowering operating costs per unit of output.

Key Economic Benchmarks for Competitive Domestic Projects

| Economic Parameter | Competitive Threshold | Strategic Significance |

|---|---|---|

| Operating cost per tonne LCE | Below $6,000/t | Positions project as low-cost vs. global average |

| After-tax NPV | Greater than $5 billion | Scale sufficient to attract institutional capital |

| Mine life | Greater than 30 years | Long-duration supply certainty for offtake partners |

| Average annual LCE production | Greater than 50,000 t/year | Material contribution to domestic supply |

| Lithium grade (clay) | Greater than 2,500 ppm | Above threshold for economic processing viability |

Projects that clear these benchmarks are positioned to attract both private capital and structured financing through mechanisms such as the Department of Energy's loan guarantee facilities under the Advanced Technology Vehicle Manufacturing program. The combination of strong project economics and domestic supply chain alignment creates a compelling investment thesis that operates independently of government support, while remaining eligible for it.

The next major ASX story will hit our subscribers first

Scenario Pathways: How This Resolves Over 2026 to 2028

The duration and severity of the current supply tightening depends on three primary variables: the consistency of Zimbabwe's policy enforcement, the speed at which Chinese processors establish qualifying in-country processing capacity, and whether additional supply disruptions materialise in other regions.

Three plausible trajectories are worth examining:

Scenario 1: Rapid Normalisation (Lower Probability)

Zimbabwe's enforcement proves inconsistent. Chinese processors secure alternative spodumene feedstock from Australian and South American spot markets within two to three quarters. Prices stabilise below Yuan 200,000/mt. This scenario requires rapid spot market reallocation and sustained output growth from producers that have already implemented cuts.

Scenario 2: Prolonged Tightness, Moderate Deficit (Base Case)

Zimbabwe's January 2027 full ban takes effect as scheduled. Companies with established in-country processing capacity gain competitive advantage over those relying on concentrate export. The global LCE shortage persists in the 37,000 to 57,000 tonne range through 2026 to 2027. New project investment accelerates in stable jurisdictions, with first meaningful supply additions reaching market by 2028 to 2029.

Scenario 3: Cascading Supply Shock (Elevated Risk)

Mali disruptions intensify. Jiangxi regulatory crackdowns expand. Australian production cuts deepen rather than reverse. The global supply gap widens beyond 57,000 tonnes LCE. Battery-grade lithium carbonate prices breach Yuan 250,000/mt. Supply chain security becomes a first-tier government priority across the US, EU, Japan, and South Korea.

"The base case scenario is consistent with current market signals, but the probability weighting assigned to Scenario 3 has increased materially since early 2026. Investors and supply chain managers should be stress-testing their positions against the cascading scenario, not just the base case."

Disclaimer: The scenario projections above represent analytical frameworks for evaluating market risk and do not constitute investment advice or predictions of future commodity prices. Actual market outcomes will depend on factors that cannot be reliably forecast, and all investment decisions involving lithium equities or commodity positions should be made following independent professional advice and thorough due diligence.

Five Strategic Implications for the Post-2026 Lithium Market

The lithium deficit from China and Zimbabwe supply cuts has accelerated a structural transition in how lithium assets are valued, sourced, and secured. Consequently, the following strategic implications are likely to persist well beyond the immediate supply disruption. China's lithium prices reaching their highest levels in two years on tight supply and demand growth reinforces why these structural shifts are unlikely to be transient:

- Diversification is no longer optional: Supply chains relying on single-region feedstock or single-pathway processing carry policy and geopolitical risk that has now been quantified in real-world price terms.

- Processing capacity is as strategically important as mining rights: Controlling or having guaranteed access to chemical conversion infrastructure determines whether a mining position translates into actual battery-grade material availability.

- Jurisdictional risk must be explicitly priced: The discount applied to projects in politically dynamic jurisdictions should now reflect not just disruption probability but the full cost of supply replacement at short notice.

- Long-duration assets carry a structural premium: Projects with 30 to 40-plus year mine lives provide supply certainty that shorter-lived operations cannot match, regardless of near-term cost advantages.

- Domestic sourcing premiums will persist: Policy frameworks across the US, EU, and allied nations are structurally oriented toward supporting domestic and allied-nation supply chains. This creates durable demand premiums for qualifying projects that operate independently of any specific government program outcome.

The transition from viewing lithium primarily through a cost-per-tonne lens toward a multi-factor framework incorporating jurisdictional stability, processing pathway certainty, and supply chain integration is not a temporary sentiment shift. It reflects a durable repricing of what supply security is actually worth when it can no longer be assumed.

Want to Catch the Next Major Lithium Discovery Before the Market Does?

As lithium supply chains fracture under geopolitical pressure and prices surge to two-year highs, Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries — instantly transforming complex geological data into actionable investment insights. Explore how major mineral discoveries have generated extraordinary returns and begin your 14-day free trial today to position yourself ahead of the next market-moving announcement.