July 8, 2026

Commodity Markets Rarely Lie: What the Lithium Forward Curve Is Actually Telling You

In commodity markets, prices tell one story. Forward curves tell another. And when the two diverge sharply from popular narrative, the forward curve almost always wins. The prevailing assumption among many retail investors is that removing a meaningful chunk of global supply will automatically tighten prices. However, the lithium price recovery and CATL Jianxiawo mine restart is one of the clearest demonstrations of why that assumption deserves serious scrutiny.

Understanding what is actually happening requires stepping back from the headline and reading the structural signals that professional market participants use to express their collective view on where prices are going. Furthermore, the global lithium market context adds an additional layer of complexity that retail investors frequently overlook.

When big ASX news breaks, our subscribers know first

How the LME Forward Curve Functions as a Market Intelligence Tool

The London Metal Exchange lithium hydroxide forward curve is not simply a pricing schedule. It functions as a real-time aggregation of the expectations held by every serious participant in the market, including producers, battery manufacturers, trading desks, and institutional hedgers. Unlike spot prices, which reflect the pressure of immediate transactions, forward contracts encode multi-month consensus about where supply and demand are heading.

The shape of that curve carries enormous informational value:

- A steeply upward-sloping curve, known as contango, signals that buyers expect supply to tighten and are willing to pay a premium to lock in future material

- A downward-sloping curve, known as backwardation, typically appears when near-term supply is genuinely scarce relative to demand

- A flat curve across an extended range of contracts signals something arguably more important: the market sees no meaningful catalyst to move prices in either direction

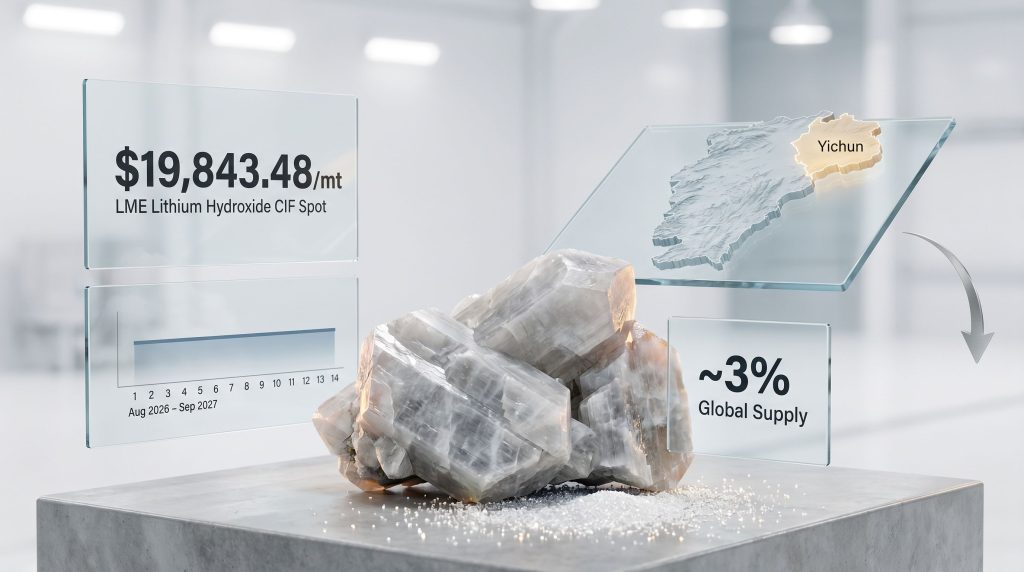

As of early July 2026, LME Lithium Hydroxide CIF closed at $19,843.48 per metric tonne, up 0.61% on the day. Every single forward contract from August 2026 through September 2027 settled at a uniform $19,820.00/mt. That produces a spot-to-forward spread of just $23.48/mt across a 14-month horizon.

| Metric | Value | Market Interpretation |

|---|---|---|

| LME Lithium Hydroxide CIF Spot | $19,843.48/mt | Marginal intraday buying |

| LME Forward Contracts (Aug 2026 to Sep 2027) | $19,820.00/mt | Uniform across all tenors |

| Spot-to-Forward Spread | $23.48/mt | Near-zero term premium |

| Forward Curve Shape | Flat | No supply disruption priced |

| Implied Price Outlook (14 months) | Unchanged | Market expects no recovery |

A flat forward curve spanning 14 consecutive monthly contracts is statistically rare in markets experiencing genuine supply disruptions. Professional participants who are genuinely worried about future scarcity bid up forward contracts to secure supply. The complete absence of that behaviour across every tenor out to September 2027 is not noise. It is a deliberate, collective signal.

The CATL Jianxiawo Mine Restart: Scale, Context, and Strategic Weight

The Jianxiawo hard-rock lithium mine, situated in Yichun, Jiangxi Province, is not a marginal operation. Jiangxi has become one of the central hubs of China's domestic lithium supply chain, predominantly producing lithium from lepidolite, a mica-group mineral that differs meaningfully from spodumene lithium supply operations in Western Australia.

Lepidolite vs. Spodumene: A Distinction Worth Understanding

Most Western investors are familiar with spodumene as the dominant hard-rock lithium mineral globally, given its prevalence across Australian operations like Greenbushes and Pilgangoora. Lepidolite, by contrast, carries a lower lithium grade and requires more energy-intensive processing to extract battery-grade material. This cost structure makes Chinese lepidolite producers structurally more vulnerable to low lithium prices, as their breakeven thresholds are generally higher than those of premium spodumene operations.

Jianxiawo's operational parameters place it among the most significant single-asset events in the 2026 lithium supply calendar:

- Nameplate capacity: approximately 100,000 tonnes of lithium carbonate per year

- LCE annual contribution: roughly 46,000 metric tonnes

- Share of 2025 global lithium supply: approximately 3%

- Share of Chinese domestic lithium output: 8 to 10%

- Suspension period: August 10, 2025 through June 29, 2026 (approximately 11 months)

- New safety permit validity: June 29, 2026 through February 27, 2028

The regulatory mechanism behind the shutdown is worth understanding clearly. In China, mining operations are legally required to hold a valid safety production license (安全生产许可证). When Jianxiawo's previous permit expired on August 10, 2025, operations were required to cease. This was not an accident, environmental enforcement action, or financial suspension. It was a scheduled regulatory event that required successful reapplication before production could resume. The new permit, issued on June 29, 2026, authorises continued operations through February 2028, at which point another renewal process will be required.

The Regulatory Timeline in Full

| Event | Date | Market Impact |

|---|---|---|

| Previous safety permit expiry | August 10, 2025 | Mine suspended; lithium equities briefly rallied |

| Shutdown duration begins | August 2025 | Supply disruption narrative emerges in markets |

| Safety permit application process | Late 2025 to mid 2026 | Regulatory uncertainty persists across 11 months |

| New safety permit issued | June 29, 2026 | Restart approved; disruption narrative collapses |

| Permit validity expires | February 27, 2028 | Next scheduled regulatory review window |

According to reporting from CNEVPost, the restart marks a pivotal moment for Chinese domestic supply, with broader implications for spot pricing across the region.

Why an 11-Month Supply Disruption Did Not Tighten the Market

This is perhaps the most counterintuitive finding embedded in the current market data. If the removal of roughly 3% of global lithium supply over nearly a full year had created any meaningful tightening in market conditions, the LME forward curve would show it. Forward buyers would have bid up future contracts. A visible upward slope would have appeared. Instead, the curve remained perfectly flat.

Two structural explanations account for this outcome, and both are likely operating simultaneously:

-

Inventory buffers absorbed the production gap. Battery manufacturers, cathode material producers, and chemical processors across the Chinese supply chain had accumulated sufficient stockpiles during the 2021 to 2022 lithium price supercycle. Those inventories proved adequate to cover Jianxiawo's absence without requiring participants to return aggressively to spot markets.

-

Alternative supply sources compensated. Australian spodumene operations continued producing, South American brine producers maintained output, and other Chinese lepidolite operations picked up incremental volume. The global lithium supply system absorbed the loss without visible strain.

The market absorbed 11 months of disruption from a mine representing 3% of global output without any measurable tightening in forward pricing. This is a structural statement about the current depth of surplus conditions in the lithium market, not a temporary anomaly.

The broader implication is significant. The lithium market is currently carrying an inventory overhang substantial enough that a disruption of this scale registers as noise rather than signal in the forward curve. That is a very different market condition from what many equity investors have been assuming. In addition, the lithium oversupply challenges already present before the shutdown compounded this dynamic considerably.

CME Futures Volume: What Near-Zero Activity Actually Reveals

CME Group's lithium hydroxide CIF CJK futures contract is cash-settled against the monthly average of Fastmarkets' lithium hydroxide price assessments, making it the primary financial instrument for institutional participants seeking to hedge lithium price exposure. The contract structure is designed precisely for producers protecting downside and consumers hedging against cost increases.

Observed activity in early July 2026 told a stark story:

- Total contracts traded: 3

- Options activity: Zero

- Implied hedging demand: Minimal

- Market interpretation: No significant directional price move is anticipated by institutional participants

In markets where a genuine price recovery is anticipated, futures volume expands across three distinct participant categories. Producers lock in forward prices to capture margins before they erode. Consumers hedge to protect against rising input costs. Speculators take directional positions betting on price movement. The near-complete absence of all three categories, across both the LME forward strip and CME futures, creates a multi-market convergence signal that is far more powerful than any single data point.

When physical market pricing, forward curve structure, and financial derivatives activity all point to the same conclusion simultaneously, the probability that the consensus is wrong diminishes sharply.

The Divergence Between Equity Narratives and Forward Pricing

One of the more instructive patterns in the lithium market over the past 12 months has been the persistent gap between how lithium mining equities responded to the Jianxiawo shutdown and what the forward curve was actually communicating throughout the same period.

When CATL's safety permit expired in August 2025 and operations ceased, lithium mining stocks rallied on the supply disruption narrative. The investment thesis was straightforward: less supply means higher prices, which means better margins for producers. However, the LME forward curve, even during those 11 months of shutdown, never reflected a supply shortage. It remained flat. The physical market did not tighten. Forward buyers did not bid up future contracts.

This divergence between equity market sentiment and futures market pricing is a recurring feature of commodity markets and represents a material analytical risk for investors relying on headline events rather than structural market data. Consequently, the Jianxiawo case study is a textbook example of why commodity equities frequently overreact to supply disruption headlines that the underlying physical market has already absorbed. Furthermore, analysis from Benchmark Minerals had previously flagged that any tightening effect from the shutdown may have been overstated.

The next major ASX story will hit our subscribers first

What a Real Lithium Price Recovery Actually Requires

The flat LME forward structure through September 2027 effectively defines, by exclusion, the conditions that would need to materialise before a sustained lithium price recovery becomes credible. Market participants are collectively signalling that none of these conditions are currently present.

1. Demand Acceleration Beyond Current Trajectory

- EV adoption rates would need to outpace existing forecasts meaningfully

- Grid-scale battery storage deployment would need to scale faster than infrastructure investment currently supports

- Emerging demand segments, including stationary industrial storage and grid frequency regulation applications, would need to absorb surplus inventory at a velocity not yet observed

2. Chinese Policy Intervention

- Coordinated production curtailment mandates targeting domestic lithium output

- Direct stimulus-driven demand acceleration through EV subsidies or large-scale grid storage procurement

- Capacity reduction agreements among major Chinese lepidolite and spodumene producers

3. Supply Disruptions Elsewhere in the Global Chain

- Unplanned shutdowns at major Australian spodumene operations such as Greenbushes or Pilgangoora

- Permitting failures or geopolitical disruption affecting South American lithium brine production in the Lithium Triangle

- Regulatory tightening across other Chinese mining jurisdictions, applying pressure similar to what drove the Jianxiawo suspension

Medium-Term Price Recovery Projections

| Timeframe | Price Outlook | Key Driver |

|---|---|---|

| Near-term (H2 2026) | Soft; range-bound approximately 150,000 to 200,000 yuan/tonne | Jianxiawo restart adds supply; inventories remain elevated |

| 2027 to 2028 | Gradual improvement possible | Demand growth from battery storage; potential supply discipline |

| 2029 to 2030 | Structural recovery potential | Projected market deficit as demand outpaces new mine development |

| Post-2030 | Recovery above $20,000/mt | Battery storage and next-generation EV demand wave |

Some market forecasters, including analysts at Fastmarkets, have projected that the lithium market could transition toward a structural deficit position during 2026 as incremental demand growth begins to outpace new mine supply additions. If realised, this scenario could provide a gradual upward price correction over a multi-year horizon. However, the Jianxiawo restart represents a direct near-term headwind against this thesis by returning 46,000 metric tonnes of LCE capacity to an already-oversupplied market. The lithium carbonate dynamics at play here further complicate any near-term bullish outlook.

Upstream, Midstream, and Downstream: Asymmetric Effects Across the Value Chain

The return of Jianxiawo's production capacity does not affect all participants in the lithium value chain equally. Its effects are asymmetric depending on where a company sits in the supply stack.

Upstream (Mining and Extraction)

- Eases supply pressure on lithium chemical converters sourcing from Jiangxi's lepidolite deposits

- Reduces spot procurement urgency for battery-grade lithium carbonate feedstock

- Increases competitive pressure on higher-cost producers, particularly those operating near breakeven at current price levels below $20,000/mt

Midstream (Chemical Processing and Conversion)

- Stabilises feedstock availability for lithium carbonate and lithium hydroxide refiners

- Reduces the incentive for processors to draw down their own inventory buffers

- May compress processing margins further if spot prices soften on the additional supply

Downstream (Battery Manufacturing and EV Supply Chain)

- Reinforces input cost stability for cathode material producers

- Reduces urgency for battery manufacturers to accelerate long-term offtake agreements

- Supports continued downward pressure on battery pack costs, a structural positive for EV affordability and adoption rate acceleration

The downstream benefit is real and meaningful for the broader energy transition. Lower lithium prices compress battery costs, making EVs more commercially competitive without subsidy dependence. However, this benefit to the downstream creates direct margin pressure on every producer sitting upstream. Technologies such as direct lithium extraction may, in time, alter these dynamics by improving recovery efficiency and reducing unit costs across the supply chain.

Frequently Asked Questions: CATL Jianxiawo Mine Restart and Lithium Prices

What is the CATL Jianxiawo mine and why does it matter for lithium prices?

Jianxiawo is a large-scale hard-rock lithium operation in Yichun, Jiangxi Province, owned and operated by CATL, the world's largest lithium-ion battery manufacturer. With an annual nameplate capacity of approximately 100,000 tonnes of lithium carbonate and an LCE contribution of roughly 46,000 metric tonnes, the mine represents around 3% of 2025 global lithium supply and between 8 and 10% of China's total domestic output. Its operational status has direct implications for Chinese lithium carbonate spot pricing and broader global supply balances.

Why did the mine shut down and what triggered the restart?

The shutdown was a regulatory event, not a financial or operational failure. China's mining regulatory framework requires all active mines to hold a valid safety production license. Jianxiawo's previous license expired on August 10, 2025, triggering a mandatory suspension. Following approximately 11 months of the reapplication process, CATL received a new safety permit on June 29, 2026, valid through February 27, 2028.

Is the Jianxiawo restart bullish or bearish for lithium prices?

The restart is broadly bearish for near-term prices. Returning approximately 46,000 mt LCE of annual production capacity to an already-oversupplied market adds further pressure on spot pricing. The LME forward curve, which remained flat even throughout the 11-month shutdown, confirms that professional participants were not pricing the disruption as a meaningful supply tightening event to begin with.

When might a genuine lithium price recovery materialise?

Based on current analyst projections and forward curve pricing, a sustained lithium price recovery above $20,000/mt is not widely anticipated before 2029 or 2030. Near-term prices are expected to remain range-bound, with any medium-term improvement contingent on accelerating EV and battery storage demand, supply discipline among producers, or unplanned disruptions elsewhere in the global supply chain.

Reading the Market's Convergent Signals on Lithium

Three independent data streams — a perfectly flat LME forward curve across 14 monthly contracts, near-zero CME futures volume with no options activity, and the market's muted response to the return of 3% of global supply — are all pointing to the same conclusion from different analytical directions.

The lithium market in mid-2026 is structurally oversupplied, carrying an elevated inventory overhang, and is currently without any near-term catalyst sufficient to shift the pricing equilibrium in either direction. The CATL Jianxiawo mine restart does not alter this fundamental picture. It reinforces it by removing the last remaining supply disruption narrative that had supported lithium mining equity valuations since August 2025.

For investors and industry participants navigating the current environment, the analytical lesson is clear: forward curve structure is a more reliable leading indicator of commodity price direction than headline supply events. When equity markets rally on a supply disruption that the forward curve refuses to price, the forward curve has historically proven more accurate.

Disclaimer: This article is for informational purposes only and does not constitute financial advice. Lithium price forecasts and market projections involve significant uncertainty and may not be realised. Past market behaviour is not a reliable guide to future outcomes. Investors should conduct their own due diligence before making any investment decisions.

Want to Stay Ahead of the Next Major ASX Mineral Discovery?

While lithium's forward curve signals a prolonged oversupply, opportunities in other commodities continue to emerge — and Discovery Alert's proprietary Discovery IQ model delivers real-time alerts the moment significant ASX mineral discoveries are announced, turning complex data into actionable insights for traders and investors alike. Explore historic discoveries and their extraordinary returns, then start your 14-day free trial at Discovery Alert to position yourself ahead of the broader market.