July 8, 2026

Why Lithium Pricing Has Never Worked the Way It Should

For decades, the world's most consequential commodity markets have operated through a common architecture: transparent, exchange-traded price discovery that allows every participant, from producers to consumers to financial intermediaries, to access the same real-time signal. Oil trades on NYMEX and ICE. Copper anchors itself to the London Metal Exchange. Gold has two centuries of benchmark history behind it.

Lithium, despite becoming one of the defining materials of the clean energy economy, has spent most of its commercial life without any of this infrastructure. Prices were set through opaque assessments by private price reporting agencies, bilateral contracts negotiated behind closed doors, and spot transactions that reflected regional dynamics rather than global fundamentals. For a mineral now sitting at the centre of a multi-trillion-dollar battery economy, that structural gap has imposed real costs on every participant in the value chain.

That architecture is now changing, and the change is coming from an unexpected direction for many Western market observers: Guangzhou, China.

When big ASX news breaks, our subscribers know first

The China Lithium Futures Market Expansion: What It Actually Means

GFEX Opens Its Doors to the World

The Guangzhou Futures Exchange launched its domestic lithium carbonate futures contract in July 2023, giving Chinese industry participants their first regulated mechanism for hedging lithium price exposure. For nearly three years, that contract remained inaccessible to overseas traders. That changed on July 3, 2026, when GFEX formally opened both futures and options on lithium carbonate to qualified international participants.

The contract structure is deliberately designed to reduce friction for non-Chinese institutions. While the instruments are denominated in Chinese yuan, overseas participants are permitted to post US dollars as margin collateral, subject to a 5% haircut. Delivery eligibility for futures contracts dated from July 2026 onward extends to qualified foreign traders. This architecture does not require international participants to hold yuan, significantly lowering the operational barrier to entry.

The China lithium futures market expansion is not occurring in isolation. It follows the April 2026 opening of China's nickel futures to overseas traders on the same exchange, suggesting a deliberate and sequenced strategy to internationalise Chinese commodity pricing infrastructure across the critical minerals complex. Furthermore, understanding the broader global lithium market context is essential to appreciating why this shift carries such weight.

Volume Tells the Real Story

The most striking aspect of GFEX's market position is not its regulatory architecture but its sheer transactional dominance. The following comparison illustrates just how asymmetric the competitive landscape has become:

| Exchange | Monthly Lithium Futures Volume (May 2026) |

|---|---|

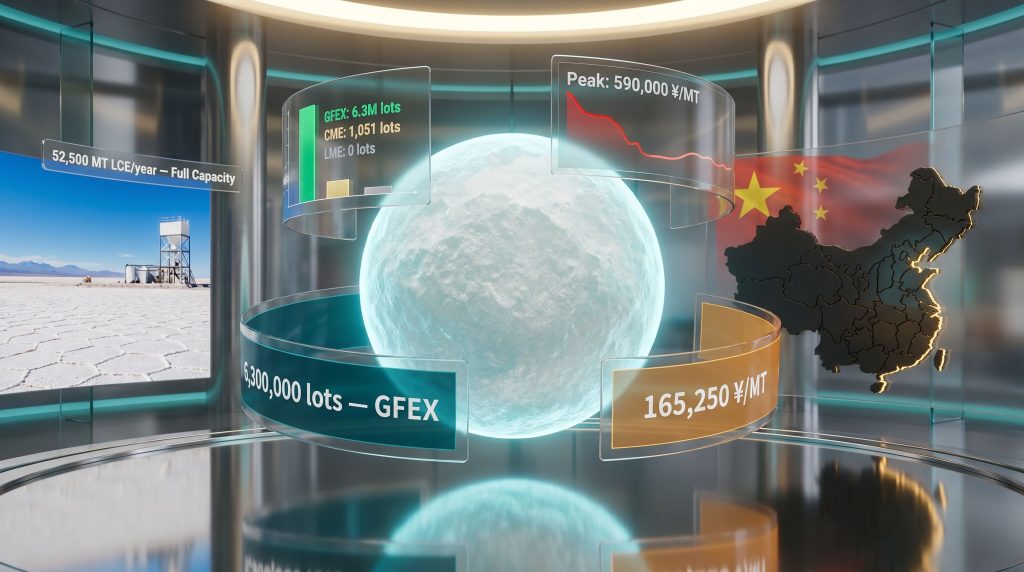

| Guangzhou Futures Exchange (GFEX) | 6.3 million lots |

| CME Group (Chicago) | 1,051 lots |

| London Metal Exchange (LME) | 0 lots |

The LME launched its own lithium contract with considerable fanfare, but it has failed to generate meaningful trading activity. The CME's contract remains a rounding error by comparison. GFEX's dominance is not the result of regulatory protection alone; it reflects the exchange's proximity to where lithium actually flows through the global economy. China processes approximately 70% of the world's lithium and manufactures around 80% of all lithium-ion battery cells, according to the International Energy Agency. When the overwhelming majority of physical lithium changes hands within China's industrial ecosystem, it is logical that the most liquid price signal would also originate there.

The practical implication for global producers and battery manufacturers is significant: the price they reference for contract negotiations, hedging decisions, and financial reporting is increasingly the price set in Guangzhou, not London or Chicago.

China's Supply Chain Position: Why Refining Matters More Than Mining

The Midstream Advantage That Most Investors Overlook

A persistent misconception in lithium market analysis is that pricing power flows from where lithium is mined. In reality, pricing influence is concentrated at the midstream processing level, where raw spodumene concentrate and lithium brine are converted into the battery-grade lithium carbonate or lithium hydroxide that manufacturers actually purchase.

| Metric | China's Estimated Share |

|---|---|

| Global lithium refining capacity | ~70% (IEA) |

| Global lithium-ion battery cell production | ~80% (IEA) |

| Global EV production by volume | Largest single national market |

Australia mines more lithium spodumene than almost any other country, but a substantial portion of that material is shipped to China for processing before it re-enters the global supply chain as battery-grade product. Chile's lithium reserves in the Atacama brine deposits are the world's largest, but again, a significant portion of refined output is processed through Chinese industrial infrastructure. This midstream concentration is what gives China's futures market its gravitational pull: the exchange is not pricing an abstract derivative but a physical commodity that overwhelmingly moves through Chinese hands.

Emerging Supply Pressures Adding Market Complexity

Several upstream dynamics are amplifying the commercial value of futures-based hedging for both producers and consumers:

- Africa's rising feedstock role: Mali has emerged as a growing source of spodumene concentrate, adding a new geographic dimension to the upstream supply picture.

- Zimbabwe export restriction risks: Political and regulatory uncertainty around Zimbabwe's lithium export policies creates upstream supply volatility that producers need instruments to hedge against.

- Jiangxi province curtailment risk: China's Jiangxi region is a significant domestic lithium processing hub, and any production disruptions there create immediate downstream market effects.

- Fastmarkets' 2026 deficit projection: Forecasters at Fastmarkets have projected a lithium market deficit for 2026, driven by demand growth outpacing the rate of new supply additions.

These pressures collectively increase the strategic value of exchange-traded hedging instruments. A futures market that allows a battery manufacturer to lock in input costs, or a miner to floor its revenue, becomes more operationally valuable precisely when physical markets are most uncertain.

Lithium Prices: A 70% Collapse and What Followed

Understanding the Price Cycle in Structural Terms

Lithium's price history over the past five years offers a compressed version of the commodity super-cycle dynamics that typically play out over decades in markets like iron ore or copper. The speed of the collapse is as instructive as its magnitude.

Battery-grade lithium carbonate in China peaked at above 590,000 yuan per metric ton in November 2022, driven by a near-perfect storm of surging EV demand, production constraints, and speculative inventory accumulation. By mid-2026, the same material was trading at approximately 165,250 yuan per metric ton, representing a decline of more than 70% from peak levels. A temporary recovery in April 2026 briefly pushed prices toward 177,500 to 180,560 yuan per metric ton, the highest reading in approximately two years, before softening again.

What Drove the Collapse?

The price correction was not a demand story. Global lithium demand grew from roughly 75,000 metric tons in 2020 to an estimated 240,000 metric tons in 2024, according to IEA data, representing more than a tripling in four years. The lithium market downturn was a supply story, driven by:

- Aggressive capacity expansion in Australia, Chile, Argentina, China, and emerging African producers, all simultaneously responding to the price incentives created by the 2022 peak

- Inventory overhang accumulating across the midstream processing sector as new material arrived faster than downstream consumption could absorb it

- Project development timelines compressing as capital flooded the sector during the price spike, pulling forward supply that might otherwise have arrived years later

- Speculative destocking by battery manufacturers who had built precautionary inventory during the shortage period

The Demand Foundation That Remains Intact

Despite the price correction, the structural demand case for lithium has not deteriorated. Global electric vehicle sales exceeded 20 million units in 2025, representing approximately one in every four new vehicles sold worldwide, according to IEA tracking data. In addition, battery storage expansion is scaling rapidly alongside accelerating solar and wind deployment, adding a second major demand vector that was less prominent during the 2022 price spike.

The USGS estimates global lithium reserves at approximately 30 million metric tons, concentrated in Chile, Australia, Argentina, and China. At current and projected consumption rates, reserves are not the binding constraint on long-term supply. The constraint is the speed at which processing capacity and downstream battery manufacturing can be scaled to meet demand growth.

Sodium-Ion Batteries: Competitive Pressure, Not Structural Replacement

What Sodium-Ion Technology Actually Changes

Sodium-ion batteries replace lithium with sodium as the charge-carrying ion. Sodium is the sixth most abundant element in the Earth's crust, compared to lithium's 25th, making the raw material cost differential between the two chemistries significant at scale. China's regulatory approval for broader commercial deployment of sodium-ion batteries in 2026 has accelerated domestic production scaling, with several manufacturers now bringing sodium-ion cells into volume production.

The technology offers genuine performance advantages in specific operating conditions, particularly cold-weather performance, where lithium-ion cells experience capacity degradation that sodium-ion chemistry handles more effectively. Sodium-ion cells also avoid cobalt and reduce dependence on lithium itself, addressing two of the most contested raw material dependencies in the battery supply chain.

Mapping Where Sodium-Ion Competes and Where It Cannot

| Application | Preferred Chemistry | Primary Reason |

|---|---|---|

| Long-range passenger EVs | Lithium-ion | Superior gravimetric energy density |

| Urban and short-range EVs | Sodium-ion viable | Cost efficiency prioritised over range |

| Stationary grid storage | Sodium-ion viable | Energy density less operationally critical |

| Consumer electronics | Lithium-ion | Size and weight constraints are binding |

| Cold-climate applications | Sodium-ion competitive | Better low-temperature performance |

The IEA's assessment is that lithium-ion technology will retain its dominance in high-performance applications through at least 2035. Sodium-ion adoption is more accurately described as a demand moderator than a demand destroyer: it may slow the rate of lithium consumption growth in cost-sensitive segments while leaving the structural growth trajectory largely intact.

An important distinction that many market commentators overlook: sodium-ion batteries do not currently match lithium-ion's energy density at the cell level. Until that gap closes substantially, the addressable market for sodium-ion remains structurally capped in the applications that consume the most lithium.

Eni's $225 Million Commitment: Reading Institutional Signals During a Downturn

The Black Giant Project and What It Represents

The decision by Italian energy major Eni to commit $225 million to EnergyX's Black Giant Lithium Project in Chile's Atacama region, announced in July 2026, deserves careful contextual analysis. This is not a junior mining company making a speculative bet. Eni is a fully integrated energy major with a sophisticated understanding of commodity cycles and long-lead capital allocation. Its participation in a lithium brine project during a period of historically suppressed prices sends a clear institutional signal about long-term demand conviction.

The Black Giant project is among the largest undeveloped lithium brine resources globally. Its development timeline follows a phased structure:

| Phase | Annual Capacity Target | Expected Start |

|---|---|---|

| Phase 1, Train 1 | 7,500 metric tons LCE/year | 2028 |

| Phase 2, Additional Trains | +45,000 metric tons LCE/year | 2030 |

| Full Operational Capacity | 52,500 metric tons LCE/year | Post-2030 |

LCE = Lithium Carbonate Equivalent

Direct Lithium Extraction: The Technology at the Core of the Investment

Traditional lithium brine extraction relies on evaporation ponds that can take 12 to 24 months to concentrate brine before processing begins. This method requires enormous land areas, consumes significant freshwater resources, and recovers only a fraction of the available lithium content, often between 40% and 60% depending on site conditions.

Direct lithium extraction bypasses evaporation entirely by using selective adsorption, ion exchange, or membrane technologies to extract lithium directly from brine. The theoretical advantages are substantial:

- Recovery rates potentially exceeding 80% to 90% of available lithium content

- Dramatically reduced land footprint, making projects viable in environmentally sensitive regions

- Significantly lower freshwater consumption, critical in arid environments like the Atacama

- Faster processing cycles, reducing the time between brine extraction and saleable product

The Black Giant project represents one of the most ambitious real-world DLE deployments planned to date. The technology is not yet proven at the scale EnergyX is targeting, which introduces execution risk that investors should weigh carefully. However, the involvement of a capital-disciplined energy major like Eni suggests the due diligence process has reached a level of technical confidence sufficient to justify nine-figure commitment.

The next major ASX story will hit our subscribers first

Three Scenarios for Lithium Market Rebalancing Through 2030

Scenario 1: Orderly Rebalancing (Base Case)

New supply from Chile, Australia, and North America enters the market progressively rather than in a simultaneous surge. EV adoption scales in line with IEA central projections. Lithium prices stabilise in a mid-cycle range that supports project economics without triggering another investment boom. GFEX gradually becomes the accepted global benchmark, and the transition from price reporting agency assessments to exchange-traded price discovery improves transparency for all participants.

Scenario 2: Prolonged Oversupply and Producer Attrition (Bear Case)

Lower-cost producers continue expanding output despite compressed margins, sustained by state support or balance sheet resilience. High-cost projects in North America and Africa are abandoned, concentrating supply further among the lowest-cost producing regions. Sodium-ion adoption accelerates faster than base case projections, compressing lithium demand growth in the near term. Futures market liquidity increases as more participants use GFEX, but prices remain structurally depressed for longer than most current forecasts anticipate.

Scenario 3: Supply Deficit and Price Recovery (Bull Case)

Fastmarkets' 2026 deficit forecast materialises and extends into 2027 and 2028 as project deferrals during the low-price period create a supply gap. EV and battery energy storage demand accelerates beyond base case projections, tightening the market from the demand side simultaneously. DLE technology delays push projects like Black Giant past their initial operating timelines. Consequently, the China lithium futures market expansion sees GFEX futures prices recover sharply, attracting significant speculative and hedging interest from international participants newly admitted to the market.

The Geopolitical Dimension: Who Controls the Benchmark Controls the Market

The Strategic Implications of a China-Anchored Global Price

A subtle but consequential shift occurs when an exchange-traded futures market achieves benchmark status: the country hosting that exchange gains structural influence over the commercial terms of a commodity's global trade, regardless of where the physical commodity is produced.

Iron ore provides the most relevant precedent. The transition from annual bilateral contracts between Australian miners and Japanese steel mills to index-linked pricing, and ultimately to futures-based price discovery, fundamentally altered the commercial relationships governing that market. A similar transition is underway in lithium, with the critical difference that the dominant exchange is located in the world's largest processing and consuming nation rather than in a neutral financial centre.

For Western governments and industry participants, this creates a tension that policy frameworks have not yet resolved. Diversifying physical supply chains through investment in North American, European, and Australian production does not eliminate pricing dependency if the dominant financial market for lithium remains in China. A Canadian miner producing battery-grade lithium carbonate for US battery manufacturers may find that the commercial terms of its contracts are ultimately anchored to a lithium price signal generated in Guangzhou.

The LME and CME's collective failure to develop liquid lithium futures contracts has effectively ceded this benchmark authority to GFEX by default rather than by design. Reversing that situation would require years of sustained liquidity development and the willingness of major industry participants to shift hedging activity away from a deeper, more operationally relevant market.

Frequently Asked Questions

What is the GFEX lithium carbonate futures contract?

The GFEX lithium carbonate futures contract is a yuan-denominated exchange-traded instrument that allows producers, manufacturers, and investors to manage lithium carbonate price risk through regulated futures and options markets. It was launched domestically in July 2023 and opened to qualified overseas traders on July 3, 2026.

Can foreign investors use US dollars as margin on GFEX?

Yes. International participants are permitted to post US dollars as margin collateral subject to a 5% haircut, even though the contracts themselves settle in Chinese yuan. This arrangement substantially reduces the currency barrier for non-yuan-holding institutions.

What is the current lithium carbonate price in China?

Battery-grade lithium carbonate was trading at approximately 165,250 yuan per metric ton in mid-2026, down from a peak above 590,000 yuan in November 2022. A temporary recovery to near 180,000 yuan was recorded in April 2026 before prices softened again.

Will sodium-ion batteries replace lithium-ion technology?

The IEA does not project sodium-ion chemistry replacing lithium-ion as the dominant battery technology within the current decade. Sodium-ion is expected to gain share in cost-sensitive, lower-energy-density applications while lithium-ion retains dominance in long-range EVs and high-performance storage systems.

What is Direct Lithium Extraction and why does it matter?

DLE is a processing technology that selectively separates lithium from brine without multi-year evaporation pond operations. It offers higher lithium recovery rates, a smaller land footprint, and lower freshwater consumption, potentially unlocking brine resources previously considered uneconomical or environmentally problematic to develop at scale.

Key Takeaways for Market Participants

- China's GFEX has become the world's dominant lithium futures market by volume, with overseas access from July 2026 formalising its role as the de facto global benchmark

- Lithium prices remain more than 70% below their 2022 peak, but demand fundamentals driven by EVs and grid storage continue to strengthen across both volume and geographic breadth

- The China lithium futures market expansion carries geopolitical weight that extends beyond market efficiency, creating pricing dependency for non-Chinese producers and consumers even as physical supply diversification proceeds

- Sodium-ion batteries introduce competitive pressure in specific segments but are not projected to displace lithium's dominance in high-energy applications through 2035

- Eni's $225 million commitment to DLE-based extraction in Chile during a period of suppressed prices represents a strong institutional signal that long-term supply security is being prioritised over short-term price optimisation

- A supply deficit is forecast for 2026, potentially creating upward price pressure even as the broader market remains in a post-peak correction phase

- DLE technology represents both an opportunity and an execution risk, with recovery rate improvements and reduced environmental footprint offering genuine advantages that remain to be proven at commercial scale

Readers seeking ongoing lithium price tracking and commodity market analysis can also explore the rise of lithium futures as documented by Fastmarkets, which provides detailed coverage of how exchange-traded lithium instruments are reshaping price discovery globally.

Disclaimer: This article is provided for informational purposes only and does not constitute financial, investment, or commodity trading advice. Forecasts, price projections, and scenario analyses represent analytical assessments based on publicly available data and are subject to material uncertainty. Readers should conduct their own due diligence before making any investment decisions.

Want to Spot the Next Major ASX Mineral Discovery Before the Broader Market Does?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries across lithium and more than 30 other commodities, converting complex geological and market data into clear, actionable insights for both short-term traders and long-term investors. Explore historic discoveries and the returns they generated to understand what early positioning in transformative mineral finds can mean for a portfolio, then begin your 14-day free trial to gain a market-leading edge.