June 19, 2026

When the Investment Thesis Breaks: Anatomy of a Commodity Surplus

Commodity markets have a long history of punishing consensus thinking. When an investment narrative becomes universally accepted, capital floods in, capacity expands beyond what demand can absorb, and the very conditions that made the thesis compelling eventually destroy it. Few recent examples illustrate this cycle more vividly than the lithium hydroxide market surplus that took shape between 2023 and 2026, collapsing prices by more than 90% from their peak and triggering some of the largest write-downs in the history of ex-China battery materials processing.

Understanding how this happened, and what it means for the market's next phase, requires looking beyond the headline price collapse to the structural forces that are still reshaping how lithium hydroxide is produced, traded, and priced.

When big ASX news breaks, our subscribers know first

From Shortage to Surplus: The Investment Cycle That Went Wrong

The early 2020s represented an era of near-universal conviction about the trajectory of battery chemistry. High-nickel cathode formulations, specifically NMC 811 and NCA variants, were expected to dominate the next generation of electric vehicles by delivering the energy density needed to extend driving range. Lithium hydroxide, the essential precursor for these cathode chemistries, was positioned as one of the battery sector's most strategically critical materials.

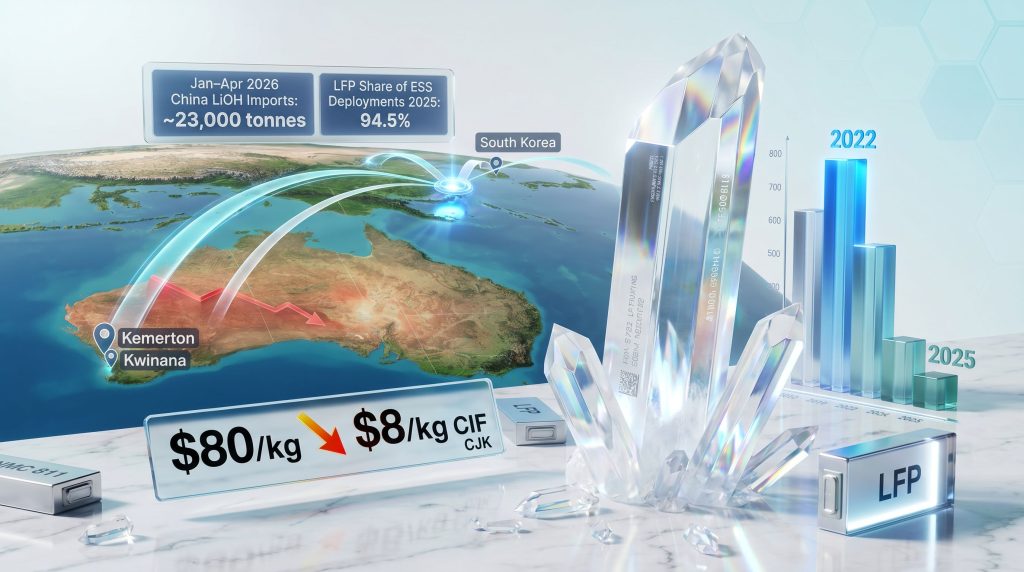

Price signals reinforced this conviction with extraordinary force. Battery-grade lithium hydroxide spot prices surpassed $80 per kg on a CIF China, Japan and Korea (CJK) basis in late 2022, according to Fastmarkets benchmark data. At those levels, refinery construction projects that might have appeared marginal at $20/kg suddenly looked highly attractive.

Three structural forces then converged to invert the supply-demand balance in ways that most participants did not anticipate:

- Western EV adoption grew more slowly than the projections that underpinned investment decisions

- Lithium iron phosphate (LFP) battery chemistry captured a substantially larger share of the battery market than consensus forecasts suggested

- New refining capacity continued moving towards commissioning even as the demand environment was softening

By 2025, battery-grade lithium hydroxide spot prices had collapsed to approximately $8 per kg CIF CJK, their lowest levels since meaningful price reporting began in 2017. The scale of this correction, more than 90% from peak, reflects not just a supply overhang but a fundamental realignment of the market's structural assumptions. This trajectory is consistent with broader patterns observed across the lithium market downturn that has reshaped the sector since 2023.

The LFP Revolution: A Chemistry Shift That Redrew the Demand Map

Perhaps the most consequential and least anticipated force driving the lithium hydroxide market surplus has been the accelerating dominance of LFP battery chemistry. LFP batteries use lithium carbonate, not lithium hydroxide, as their primary lithium precursor. Every percentage point of market share that LFP gains over nickel-rich chemistries in EVs and stationary storage represents a structural reduction in the total addressable market for hydroxide refiners.

The advantages driving LFP adoption are well-documented but worth examining in context:

- Thermal safety: LFP cells are significantly more stable at elevated temperatures, reducing fire risk in both vehicles and grid-scale storage applications

- Cycle life: LFP chemistry typically delivers more charge-discharge cycles than NMC equivalents, a critical attribute for stationary storage that undergoes daily cycling

- Cost per kWh: LFP eliminates nickel and cobalt from the cathode entirely, reducing material costs substantially

- Energy density disadvantage: LFP's lower energy density relative to NMC 811 is less commercially relevant in applications where physical space and weight are secondary to cost and longevity

In the energy storage system (ESS) market, these tradeoffs have produced an almost complete dominance of LFP chemistry. According to Fastmarkets research, LFP batteries accounted for approximately 94.5% of ESS deployments in 2025, with that share forecast to rise further to 95.1% in 2026.

The ESS Market as an Accelerant

The rapid scaling of battery energy storage systems has itself become one of the most significant structural forces in the battery materials sector, and it is almost entirely a lithium carbonate story rather than a hydroxide story. Furthermore, the lithium carbonate supply dynamics at play here have increasingly diverged from hydroxide market conditions in ways that matter for investors.

One underappreciated driver of ESS growth is the explosive demand for power-dense infrastructure associated with artificial intelligence computing. Data centres operating large-scale AI workloads require continuous, high-quality power supply, and battery storage systems have become an increasingly important component of that infrastructure. This dynamic added a demand vector to the ESS market that was not widely incorporated into hydroxide demand forecasts prepared during the 2020 to 2022 investment cycle.

Fastmarkets research estimated lithium demand from the ESS sector at 339,080 tonnes of lithium carbonate equivalent (LCE) in 2025, with projections pointing to nearly 30% growth to 440,046 tonnes LCE in 2026. This growth accrues almost entirely to lithium carbonate, creating a divergence in demand trajectories between the two primary lithium salts. The ongoing battery storage expansion therefore benefits carbonate far more than hydroxide, a distinction that many earlier market models failed to adequately capture.

"The lithium hydroxide market surplus was not caused by a collapse in battery demand. Global EV and ESS volumes continued growing. What changed was the chemistry composition of that growth, shifting demand toward carbonate and away from hydroxide at a pace most market participants did not model."

Automakers Pivoting Into Storage Markets

As EV demand growth slowed in key Western markets, several major automotive manufacturers began repositioning towards the ESS sector. Ford's strategic expansion into energy infrastructure is a notable example of this pivot, as the company responded to a widening gap between earlier EV assumptions and market reality. This shift by automotive OEMs further reinforces LFP chemistry dominance, adding institutional weight to a trend that was already structurally entrenched in the battery supply chain.

Western EV Demand: Policy Uncertainty and the Cascade Effect

The demand-side story for lithium hydroxide cannot be separated from the policy environment that shaped Western EV purchasing behaviour. The expiration of US Inflation Reduction Act EV tax credits on September 30, 2025 materially weakened near-term purchasing incentives in the United States market, creating a demand air pocket at precisely the moment when ex-China refining capacity was scaling up.

South Korean battery manufacturers, which had made substantial capacity commitments based on anticipated US demand under IRA incentive assumptions, experienced significant financial deterioration in 2025, including operating losses and revenue declines tied to inventory corrections.

The project cancellation cascade that followed illustrates how interconnected the downstream demand chain had become:

- Ford cancelled a $6.5 billion EV battery supply agreement with LG Energy Solution in December 2025, citing a combination of policy uncertainty and demand softness

- Three planned Ford EV models were cancelled as part of the same restructuring

- F-150 Lightning production was discontinued, removing a high-profile demand anchor from the premium EV segment

- Battery producers in South Korea reduced plant utilisation rates and began releasing both fresh and aged lithium hydroxide inventories into the spot market

This destocking behaviour created a secondary supply wave on top of the primary surplus from new refining capacity, compressing prices further and faster than supply-demand models alone would have suggested.

The Ex-China Capacity Build: Scale, Ambition, and the Limits of Timing

One of the most striking features of the lithium hydroxide market surplus is the sheer scale of refining capacity that was constructed outside China during the investment cycle. According to Fastmarkets research, ex-China lithium hydroxide output rose from approximately 23,000 tonnes in 2021 to 105,600 tonnes in 2025, representing a nearly fivefold increase over four years.

This capacity expansion was designed to reduce Western battery supply chain dependence on Chinese processing, a strategically rational objective given geopolitical risk considerations. However, building competitive lithium hydroxide processing outside China proved far more difficult than many project developers anticipated. Ex-China lithium hydroxide production has faced persistent delays and specification challenges that compounded the sector's difficulties.

Why Ex-China Refining Underperformed

Several compounding factors undermined the commercial performance of new ex-China hydroxide capacity:

- Ramp-up difficulties: Lithium hydroxide processing requires precise chemical control to consistently meet battery-grade specifications. Many newly commissioned facilities struggled to achieve stable, on-spec output during their commissioning phases, releasing lower-quality material into the spot market at discounted prices

- Operating cost differentials: Chinese processors benefit from scale, established supply chains, and significant accumulated process expertise, creating a structural cost advantage that proved difficult to close

- Demand timing mismatch: The investment decisions that drove this capacity expansion were made in 2021 to 2022, based on demand forecasts that did not adequately account for LFP's accelerating market share gains or the moderation in Western EV adoption

The financial consequences have been severe. Albemarle completed the full shutdown of its Kemerton lithium hydroxide processing plant in Western Australia in February 2026, citing the need to improve financial flexibility. IGO fully impaired its stake in the Kwinana lithium hydroxide refinery joint venture with Tianqi Lithium Energy Australia in July 2025, explicitly citing low confidence in any meaningful recovery in asset performance.

China's Structural Reversal: From Exporter to Clearing Market

Perhaps the most underappreciated dimension of the current lithium hydroxide market surplus is the complete structural reversal of China's role in global trade flows. For most of the early 2020s, China was a net exporter of lithium hydroxide, supplying seaborne markets with processed material. That dynamic has now reversed in a historically significant way.

China has re-emerged as the primary import destination for surplus seaborne hydroxide material, functioning as the global clearing market in a way that no other single market is capable of doing. This is possible because China's processing infrastructure offers multiple absorption pathways:

- Higher-quality imported material that meets specification can be used directly in cathode active material manufacturing

- Material that does not meet direct-use specifications can be converted into battery-grade lithium carbonate for LFP applications

- Other cargoes can be re-refined into higher-specification battery-grade hydroxide for downstream deployment

The trade data that reflects this shift is striking. According to customs data cited by Fastmarkets, China's lithium hydroxide imports surged to over 23,000 tonnes in January to April 2026, compared with approximately 5,600 tonnes in the same period a year earlier. Simultaneously, China's export volumes declined sharply from over 41,876 tonnes in January to April 2024 to approximately 13,171 tonnes in the same window of 2026. The China battery recycling outlook further complicates this picture, as domestic recycled material increasingly competes with imported hydroxide for cathode manufacturing slots.

| Period | China LiOH Imports | China LiOH Exports |

|---|---|---|

| Jan–Apr 2024 | Low (baseline) | ~41,876 tonnes |

| Jan–Apr 2025 | ~5,600 tonnes | ~16,026 tonnes |

| Jan–Apr 2026 | ~23,000 tonnes | ~13,171 tonnes |

This shift has had direct consequences for price discovery. Spot market activity has increasingly migrated towards a CIF China basis, while CIF Japan and Korea activity has declined materially, consistent with reduced seaborne procurement by Northeast Asian battery manufacturers adjusting their inventory positions downward.

The next major ASX story will hit our subscribers first

Quality Differentiation: How the Surplus Is Changing Price Formation

One structural consequence of the lithium hydroxide market surplus that carries significant implications for how the commodity is valued is the emergence of meaningful price differentiation based on material quality and qualification status.

In a tight market, buyers accept a wider range of material because supply is scarce. In a surplus environment, however, buyers become selective, and quality premiums and discounts become larger and more persistent. The following factors have become increasingly important determinants of transactional value in the current market:

- Qualification status: Whether the material has received formal qualification approval from major battery cell manufacturers in the destination country

- Shelf life and age: Lithium hydroxide is hygroscopic and can degrade over time if not stored correctly, making aged inventory less commercially attractive

- Physical characteristics: Particle size distribution, moisture content, and impurity profiles all affect suitability for direct cathode manufacturing use

- End-use destination: Material destined for direct battery use commands a premium over material heading to conversion or non-battery applications

- Volume and payment terms: Increasing trader participation in the spot market has introduced commercial considerations around volume discounts and credit terms

This quality-based price bifurcation represents a maturing of the lithium hydroxide spot market, moving it closer in structure to more established commodity markets where specification differentials drive systematic price differentials.

Benchmark Methodology Evolution

In response to these structural changes, benchmark specifications for battery-grade CIF CJK lithium hydroxide assessments are being revised effective September 1, 2026, following consultation with more than 50 companies across the supply chain. The revision aims to ensure the benchmark reflects widely qualified, merchantable battery-grade material suitable for use in EV and ESS applications in the destination market, excluding unqualified material, aged inventory, and conversion-grade cargoes from the benchmark price formation process.

This evolution mirrors the historical development of the assessment framework itself. Daily price assessment frequency was introduced in December 2021 in response to heightened volatility. Derivative contracts were launched with CME and LME in 2021, followed by SGX in 2022 and ICE in 2025. A one-time differential publication is scheduled for August 28, 2026 to facilitate the adjustment of existing derivative contracts settling against the revised benchmark.

Supply-Demand Balance Outlook and Scenario Analysis

The broader lithium market recorded an estimated surplus of approximately 175,000 tonnes LCE in 2023, followed by roughly 154,000 tonnes LCE in 2024. Projections suggest this oversupply narrowed sharply to approximately 10,000 tonnes in 2025, with the market potentially moving into a modest deficit of around 1,500 tonnes in 2026. Innovations such as direct lithium extraction may, furthermore, alter future supply economics in ways that reshape these projections over the medium term.

Battery-grade lithium hydroxide is assessed as having a tighter supply-demand profile than lithium carbonate, which continues to face surplus pressure from LFP and ESS demand growth that does not translate into hydroxide consumption.

| Lithium Salt | 2025–2026 Balance Outlook |

|---|---|

| Battery-grade lithium hydroxide | Minor deficit potentially emerging in 2026 |

| Battery-grade lithium carbonate | Minor surplus persisting through 2026–2027 |

| Broader lithium market (LCE) | Rapidly narrowing; near-balance by 2026 |

Three plausible scenarios frame the recovery trajectory through 2027:

Scenario A: Accelerated Recovery

High-nickel EV penetration recovers in the US and Europe, ex-China capacity rationalisation continues at pace, and Chinese import demand remains elevated. A hydroxide deficit emerges by mid-2026, with prices recovering towards the $12–15/kg CIF CJK range.

Scenario B: Gradual Rebalancing

LFP continues gaining share but NCM maintains its position in premium EV segments, and ex-China capacity is partially curtailed. The market reaches near-balance by late 2026, with prices stabilising in the $9–12/kg range.

Scenario C: Prolonged Surplus

LFP dominance extends further than current forecasts suggest, idled ex-China capacity restarts prematurely on any early price signal, and Western EV policy remains uncertain. The surplus persists through 2027, and prices remain suppressed below $10/kg. The global lithium supply outlook suggests that structural oversupply risks of this kind could take several years to fully resolve.

Key Variables Investors and Market Participants Should Monitor

| Factor | Bullish for Hydroxide Recovery | Bearish or Surplus-Extending |

|---|---|---|

| NCM battery share | High-nickel EV growth accelerates | LFP continues gaining in EVs and ESS |

| Ex-China refining | Further curtailments and write-downs | Idled capacity restarts prematurely |

| Western EV policy | New subsidy frameworks restore demand | Policy uncertainty persists or deepens |

| China import absorption | Continued high volumes clear seaborne surplus | Domestic oversupply limits import appetite |

| ESS chemistry | NCM adoption in grid storage grows | LFP retains 95%+ ESS chemistry share |

Disclaimer: The scenario projections and price range estimates included in this article are based on publicly available market data and analytical frameworks. They do not constitute financial advice. Commodity markets are subject to significant uncertainty, and actual outcomes may differ materially from any forward-looking projections presented here.

Frequently Asked Questions: Lithium Hydroxide Market Surplus

What is battery-grade lithium hydroxide and why does chemistry matter?

Battery-grade lithium hydroxide monohydrate (LiOH.H2O, typically at 56.5% LiOH minimum purity) is the primary precursor for high-nickel cathode active materials including NMC 811 and NCA chemistries. These cathodes deliver higher energy density than LFP alternatives, making hydroxide the preferred input for premium EV batteries where maximising driving range is commercially critical. Because LFP cathodes use lithium carbonate instead, the market split between these two chemistries directly determines the relative demand for the two lithium salts.

How much have lithium hydroxide prices fallen?

Battery-grade lithium hydroxide spot prices fell from above $80/kg CIF CJK in late 2022 to approximately $8/kg by 2025, a decline of more than 90% from peak levels. This is one of the most severe price corrections recorded in the battery materials sector over a comparable timeframe.

Why is ex-China refining capacity being shut down?

The combination of lower-than-anticipated demand, significant operating cost disadvantages relative to Chinese processors, ramp-up difficulties, and sustained low spot prices has made a substantial portion of ex-China lithium hydroxide refining capacity commercially unviable at current price levels. Asset write-downs at Kemerton and Kwinana in Western Australia represent the most visible manifestations of this structural challenge.

When could the lithium hydroxide surplus end?

Forecasts suggest the broader lithium market is approaching near-balance by 2026, with battery-grade hydroxide potentially moving into a minor deficit position. However, the recovery timeline is highly sensitive to the pace of ex-China capacity rationalisation, the trajectory of high-nickel battery adoption versus LFP, and the stability of policy frameworks governing EV demand in Western markets. Investors should treat any specific timeline projections with appropriate caution given the structural uncertainties involved.

Want to Position Yourself Before the Next Major Battery Materials Discovery?

Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time, delivering instant alerts on significant mineral discoveries — including lithium and battery materials — so subscribers can identify actionable opportunities ahead of the broader market. Explore historic examples of exceptional discovery returns and begin your 14-day free trial today to gain a market-leading edge.