July 23, 2026

The Strategic Investment Framework: Understanding Battery Metal Market Dynamics Through 2026

Investment cycles in critical materials rarely follow predictable patterns, yet certain structural forces create identifiable inflection points that sophisticated investors learn to recognise. The battery metals sector, particularly lithium, presents a compelling case study in how supply-demand fundamentals, technological transitions, and geopolitical dynamics converge to create strategic opportunities. Understanding these convergent forces requires analysing multiple frameworks simultaneously: macroeconomic trends, technological adoption curves, and resource scarcity dynamics.

Market participants who successfully navigate commodity cycles typically focus on structural rather than cyclical factors. The lithium market 2026 represents such a structural shift, where demand diversification beyond traditional applications creates new investment paradigms. This transformation demands sophisticated analytical frameworks that consider not just production capacity and demand growth, but also the complex interplay between energy storage deployment, battery chemistry evolution, and regional policy dynamics.

When big ASX news breaks, our subscribers know first

Supply-Demand Rebalancing Fundamentals Creating Market Inflection

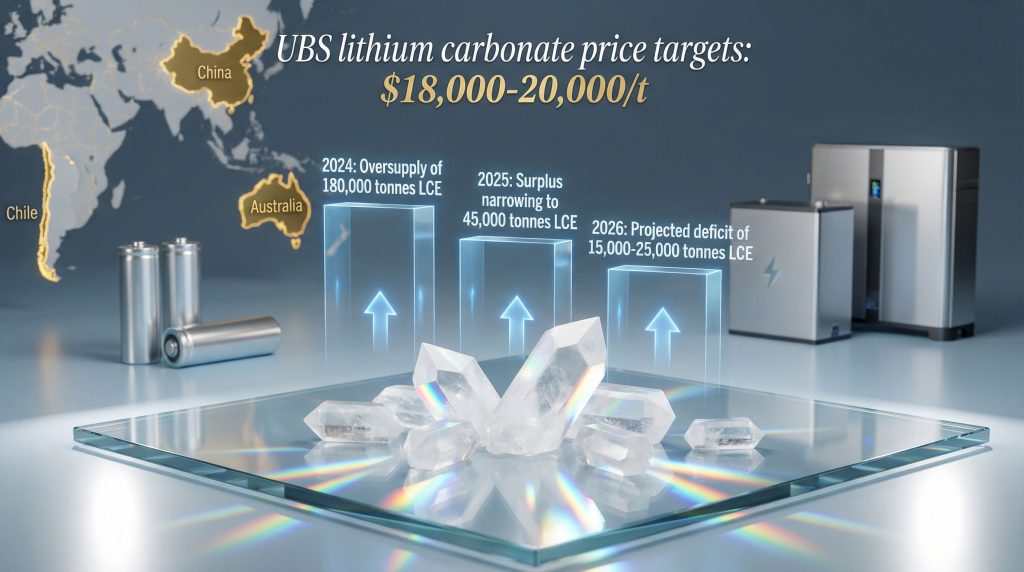

The lithium market 2026 outlook reflects a fundamental shift from oversupply conditions toward potential deficit scenarios. Current market analysis indicates the sector is transitioning from surplus conditions, with major investment banks revising their price forecasts significantly upward. UBS projects spodumene concentrate prices reaching $1,800 per tonne, while JP Morgan anticipates $2,000 per tonne by late 2026, representing increases exceeding 50% from 2025 levels.

These projections contrast sharply with current realised prices, exemplified by operations like those achieving approximately $700 per tonne in recent quarters. The gap between current pricing and institutional forecasts suggests substantial upside potential for producers that can maintain operations through the transition period.

Global Lithium Market Balance Evolution

| Year | Market Condition | Volume (kt LCE) |

|---|---|---|

| 2024 | Oversupply | 180 |

| 2025 | Narrowing Surplus | 45 |

| 2026 | Emerging Deficit | 15-25 |

| 2027-2030 | Widening Supply Gap | Expanding |

Production economics during market transitions reveal critical insights about marginal cost structures. Operations that were mothballed due to unprofitability during price troughs often possess restart capabilities when market conditions improve. The economic viability threshold appears aligned with institutional price forecasts, suggesting that current mothballed capacity could return to production as prices recover.

Investment Bank Consensus Evolution

The shift in institutional sentiment reflects deeper analytical work around structural demand drivers. Goldman Sachs has accelerated its structural deficit timeline, whilst Morgan Stanley has upgraded its rationale for battery metal exposure. This consensus shift represents more than cyclical optimism; it reflects recognition of fundamental changes in demand composition and supply constraints.

Contemporary analysis suggests that total lithium carbonate demand may reach 1.5 million tonnes LCE by 2025, with historical projections from consulting firms indicating potential growth to 3 million tonnes by 2030. Even conservative growth scenarios would more than double 2021 consumption levels, creating structural supply challenges given current production capacity and development timelines. Furthermore, the Australia lithium industry continues to benefit from favourable policy support and operational advantages.

Energy Storage Systems Driving Demand Diversification

Traditional analysis focused primarily on electric vehicle applications underestimates the growing significance of stationary energy storage systems. Industry analysis suggests that energy storage applications, including grid-scale installations and data centre backup systems, could account for approximately one-third of total lithium consumption by 2026.

Energy Storage System Deployment Projections

- Global ESS installations: 359 GWh projected for 2026

- 2025 baseline: 273 GWh

- China leadership: 180+ GWh annual additions

- Combined US/Europe: 85+ GWh new capacity

Grid-Scale Battery Infrastructure Expansion

Grid modernisation initiatives worldwide are driving unprecedented demand for large-scale battery installations. These systems serve multiple functions: renewable energy integration, transmission system flexibility, and distributed energy resource management. The scale of these installations creates significant lithium demand that operates independently of automotive industry cycles.

Data centre infrastructure represents another emerging demand driver. Hyperscale facilities require massive backup power capabilities, increasingly supplied by battery systems rather than traditional diesel generators. The integration of these systems with renewable energy sources creates additional complexity and scale requirements that further drive lithium consumption.

Behind-the-meter commercial applications include industrial energy arbitrage systems, peak demand management installations, and distributed energy resource networks. These applications offer economic returns through energy cost optimisation, creating self-reinforcing adoption cycles as technology costs decline and grid electricity prices increase. In addition, developments in lithium extraction technology are improving operational efficiency across various applications.

Battery Chemistry Evolution Impacting Lithium Demand Patterns

The lithium market 2026 outlook must consider evolving battery chemistry preferences and their differential impact on lithium consumption patterns. Lithium iron phosphate (LFP) technology has gained significant market share in both electric vehicles and energy storage applications, driven primarily by cost advantages over nickel cobalt manganese (NCM) and nickel cobalt aluminum (NCA) chemistries.

LFP Technology Market Penetration

LFP batteries offer several advantages that drive adoption: lower raw material costs, improved safety characteristics, longer cycle life, and reduced dependence on scarce materials like cobalt and nickel. Manufacturing scale economies in China have accelerated LFP cost reductions, making the technology increasingly competitive despite lower energy density compared to NCM chemistries.

The choice between lithium carbonate and lithium hydroxide depends significantly on battery chemistry selection. LFP batteries typically utilise lithium carbonate, whilst high-nickel chemistries require lithium hydroxide. Market trends toward LFP adoption could shift demand patterns between these lithium products, affecting pricing dynamics and producer positioning.

Next-Generation Battery Technology Development

Solid-state battery technology represents a potential paradigm shift with implications for lithium demand intensity. These batteries promise higher energy density, improved safety, and longer cycle life, but commercialisation timelines remain uncertain. Major automotive manufacturers and battery technology companies continue investing heavily in solid-state development, though large-scale production may not emerge until the latter part of the decade.

Lithium metal anode technology development could significantly increase lithium content per unit of energy storage capacity. Silicon nanowire integration and other advanced anode materials also present opportunities for performance improvements, though their impact on overall lithium demand depends on adoption rates and manufacturing scalability. However, battery recycling breakthrough technologies are emerging as sustainable solutions for meeting growing demand.

Regional Market Dynamics Shaping Investment Opportunities

Chinese Market Policy Influence and Supply Constraints

China's regulatory environment for lithium mining has shown recent tightening, as evidenced by the revocation of 27 expired mining permits in Jiangxi province during December 2025. Whilst these permits were not associated with operating mines, the action signals potential regulatory scrutiny that could affect future supply development.

China Lithium Market Drivers

| Category | 2026 Targets |

|---|---|

| EV Production | 12+ million units |

| Grid Storage Mandates | Renewable project requirements |

| Export Controls | Processed lithium products |

| Mining Permits | Domestic consolidation |

Chinese domestic demand continues growing through multiple channels: automotive electrification targets, grid storage mandates for renewable energy projects, and industrial electrification initiatives. Export restrictions on processed lithium products could affect global supply chain dynamics, potentially benefiting production capacity outside China.

North American Supply Chain Localisation

The Inflation Reduction Act creates specific domestic content requirements for battery materials, driving investment in North American lithium processing capacity. Canadian critical minerals strategy implementation includes significant government support for domestic lithium development projects, whilst Mexico's lithium nationalisation policies create uncertainty about North American supply chain integration.

These policy frameworks aim to reduce dependence on Chinese processing capacity and create regional supply chain resilience. The effectiveness of these initiatives depends on private sector investment responses and the development timeline for domestic processing capabilities. For instance, the development of a battery-grade lithium refinery demonstrates the global shift towards localised processing solutions.

European Energy Security and Strategic Autonomy

REPowerEU initiatives include ambitious battery manufacturing capacity targets as part of broader energy security objectives. The European Green Deal industrial policy coordination seeks to develop domestic critical materials processing capabilities whilst maintaining environmental standards.

European approaches emphasise strategic autonomy in critical materials whilst maintaining commitment to sustainability objectives. This creates opportunities for lithium projects that meet both supply security and environmental criteria, particularly those incorporating renewable energy in processing operations. Furthermore, insights from Argentina lithium insights provide valuable context for understanding regional market dynamics.

Investment Positioning Strategies for Market Recovery

Tier-1 Producer Valuation Framework

Major lithium producers historically trade at 0.8-1.2x price-to-net-asset-value multiples during market troughs, expanding to 2.5-4.0x during supply-constrained periods.

This valuation framework provides context for current market positioning. Established producers with operational assets, strong balance sheets, and proven management teams typically offer lower risk profiles during market transitions. Their ability to generate cash flow during price recovery phases makes them attractive for value-oriented investment strategies.

Development-Stage Asset Evaluation

Project Development Risk Assessment Matrix

| Risk Factor | High | Medium | Low |

|---|---|---|---|

| Financing Completion | >50% probability | 25-50% probability | <25% probability |

| Permitting Timeline | >36 months | 18-36 months | <18 months |

| Offtake Security | Unsecured | Partial coverage | Full coverage |

| Technical Execution | Unproven technology | Established process | Proven track record |

Development-stage projects offer higher potential returns but require careful risk assessment. Key considerations include financing completion probability, permitting timeline certainties, offtake agreement security, and management technical execution track records. Projects that score well across multiple risk dimensions present more attractive risk-adjusted return profiles.

Downstream Integration Investment Thesis

Vertical integration strategies focusing on battery manufacturing, cathode material production, and recycling technology commercialisation offer exposure to growing battery supply chains whilst potentially capturing additional value beyond raw material extraction. These approaches require different analytical frameworks but can provide diversified exposure to battery market growth.

The next major ASX story will hit our subscribers first

Supply-Side Constraints Supporting Price Recovery

High-Cost Mine Curtailment Economics

Operating cost curves by production method reveal significant variation in economic viability thresholds. Marginal producers faced shutdown decisions during price troughs, with restart timelines and capital requirements varying significantly by asset type and geographic location.

Hard-rock spodumene operations typically require higher prices for economic viability compared to brine-based production, though restart timelines can be shorter given existing infrastructure. Brine operations often have lower operating costs but longer development timelines for capacity additions.

Development Project Delivery Challenges

Critical Development Bottlenecks

- Environmental permitting: 18-36 month typical timelines

- Indigenous consultation: Community engagement requirements

- Water access: Processing infrastructure needs

- Skilled workforce: Technical expertise availability

New project development faces multiple constraints that extend delivery timelines and increase capital requirements. Environmental permitting processes have become more rigorous, requiring comprehensive environmental impact assessments and community consultation processes. Water access represents a particular challenge for lithium processing operations, which require significant water resources for concentrate processing.

Skilled workforce availability constraints affect both construction and operational phases of new projects. The specialised technical expertise required for lithium processing operations is limited globally, creating potential bottlenecks as multiple projects advance simultaneously.

Geopolitical Supply Chain Vulnerabilities

Argentina's export policy frameworks create uncertainty for international investors, particularly regarding foreign exchange regulations and export licensing requirements. Chile's constitutional reform processes include provisions affecting mining sector regulations, though specific impacts on lithium operations remain under development.

Australia-China trade relationship stability affects market access for Australian producers, though lithium's critical material status provides some protection from trade disputes. Diversification of market access across multiple jurisdictions reduces exposure to bilateral trade policy changes.

Long-Term Structural Demand Drivers Beyond 2026

Electric Vehicle Market Maturation Trajectories

Global EV Adoption Forecasting Framework

| Year | Unit Sales (millions) | Battery Capacity Trends |

|---|---|---|

| 2026 | 28-32 | Increasing per-vehicle content |

| 2030 | 55-65 | Second-life applications emerging |

Electric vehicle market maturation involves multiple dimensions beyond simple unit sales growth. Battery capacity per vehicle continues increasing as manufacturers prioritise range and performance. Second-life battery applications create additional value streams whilst potentially affecting primary battery demand timing.

Heavy-duty transport electrification represents a significant emerging market segment with substantially higher battery capacity requirements per vehicle. Marine and aviation battery development remains in early stages but could create substantial demand growth in the 2030s.

Industrial Electrification Acceleration

Mining equipment electrification programmes represent substantial opportunities given the large battery capacity requirements for heavy machinery. These applications often operate in remote locations where energy storage systems can provide operational advantages beyond emission reductions.

Industrial facility electrification extends beyond transportation to include stationary equipment and process heat applications. The scale of industrial energy consumption suggests that even partial electrification could create significant battery demand growth. Additionally, energy storage demand projections indicate continued expansion across industrial sectors.

Risk Management and Volatility Navigation Strategies

Market Cycle Recognition Framework

Historical lithium price volatility patterns demonstrate cyclical behaviour with periods of extreme price movements followed by extended consolidation phases. Inventory cycles significantly impact spot pricing, particularly in markets with limited financial hedging instruments.

Futures market development for lithium remains limited compared to other industrial metals, creating challenges for price discovery and risk management. Contango and backwardation patterns in available forward markets provide signals about market participant expectations regarding future supply-demand balances.

Portfolio Construction and Diversification

Strategic Diversification Framework

- Geographic exposure: Balancing jurisdictional risks

- Production stage distribution: Development vs. operating assets

- Currency considerations: Natural hedging strategies

- Correlation analysis: Battery metals interaction patterns

Effective portfolio construction requires balancing multiple risk dimensions whilst maintaining exposure to structural growth themes. Geographic diversification reduces exposure to single-jurisdiction policy changes whilst production stage distribution manages development risk versus operational risk trade-offs.

Currency hedging considerations become important given the global nature of lithium markets and the prevalence of US dollar pricing despite production occurring in multiple currency jurisdictions. Natural hedging through asset location selection can reduce currency risk without financial hedging instruments.

Exit Strategy Planning and Timing

Valuation multiple expansion targets provide frameworks for exit timing decisions, though market conditions can create extended periods where multiples remain compressed despite fundamental improvements. Merger and acquisition activity probability increases during market recovery phases as strategic buyers seek to secure supply chain access.

Regulatory change impact scenarios require ongoing monitoring given the strategic importance of lithium to national energy security objectives. Policy support for domestic production capacity could create acquisition premiums for appropriately positioned assets.

The lithium market 2026 investment framework requires sophisticated analysis across multiple dimensions: supply-demand fundamentals, technological evolution, regional policy dynamics, and market structure considerations. Successful navigation of this complex landscape demands both analytical rigour and strategic patience, as structural changes in battery markets create long-term investment opportunities for appropriately positioned participants.

This analysis is for educational purposes and does not constitute investment advice. Battery metal markets involve significant volatility and regulatory risks that require careful consideration. Prospective investors should conduct independent research and consult qualified financial advisors before making investment decisions.

Looking to Position Yourself for the Battery Metals Market Recovery?

Discovery Alert's proprietary Discovery IQ model delivers real-time notifications on significant ASX mineral discoveries, including critical battery metal announcements that could benefit from the emerging lithium supply deficit. Explore how major mineral discoveries historically generate substantial market returns and begin your 30-day free trial today to secure your competitive advantage in the evolving battery metals sector.