June 25, 2026

Stranded Assets, Stranded Capital: Why Brownfield Conversion Is Rewriting the Lithium Playbook

The economics of building new mining infrastructure from the ground up have never been more punishing. In an era defined by compressed commodity margins, rising construction costs, and cautious equity markets, the capital required to develop a remote greenfield lithium processing facility can easily exceed C$1 billion before a single tonne of concentrate reaches a buyer. That brutal arithmetic is forcing a strategic rethink across the critical minerals sector, and nowhere is that rethink more visible than in Canada's James Bay region, where the Li-FT Renard diamond mine lithium processing hub concept is beginning to reshape how the industry thinks about stranded infrastructure.

Against that backdrop, Li-FT Power Ltd. (TSXV: LIFT) has made a move that crystallises the emerging brownfield conversion thesis: securing an exclusive option over the Renard diamond mine in Québec, with the explicit intention of evaluating whether its substantial existing processing plant can be reoriented toward spodumene concentrate production for the North American battery supply chain.

When big ASX news breaks, our subscribers know first

The Asset at the Centre of the Li-FT Renard Diamond Mine Lithium Processing Hub Strategy

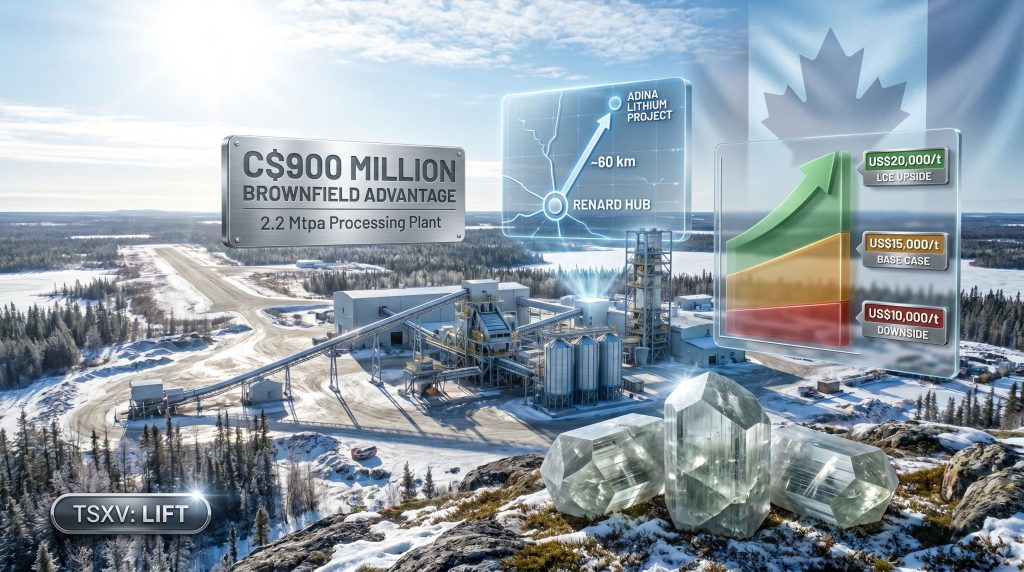

The Renard diamond mine operated as one of Québec's most significant hard-rock mining projects before financial and market pressures forced it into dormancy. What it left behind is arguably more valuable to the lithium sector than it ever was to the diamond industry: a 2.2 million tonne per annum processing plant, a self-contained power station, a functional airport, camp accommodation, tailings management infrastructure, and a suite of mineral processing permits accumulated over years of operational history.

Li-FT Power has secured an exclusive two-year option over this asset, expiring in June 2028, with a possible one-year extension. The option carries a fee of C$12 million (approximately US$8 million), plus care and maintenance obligations throughout the option period. Court approval under Canada's Companies' Creditors Arrangement Act (CCAA) creditor protection proceedings was scheduled for July 2, 2026.

The CCAA framework is a well-established mechanism in Canadian mining for managing distressed asset transitions. It provides a court-supervised process that offers legal certainty to acquirers and creditors alike, making brownfield acquisitions through this pathway structurally more transparent than private bilateral deals on similarly encumbered assets.

Critically, the Renard site sits approximately 60 kilometres south of Li-FT's Adina Lithium Project, a hard-rock spodumene asset in the Eeyou Istchee James Bay region. That geographic relationship is not incidental — it is the load-bearing pillar of the entire strategic proposition.

Why the Existing Infrastructure Creates an Asymmetric Capital Advantage

To understand why the Li-FT Renard diamond mine lithium processing hub concept has attracted serious attention, it helps to examine what a development team would need to build from scratch to replicate the Renard site's capabilities in a remote subarctic environment.

| Infrastructure Asset | Estimated Greenfield Significance |

|---|---|

| 2.2 Mtpa processing plant | Core processing capability worth hundreds of millions to replicate |

| Dense media separation (DMS) circuits | Directly applicable to hard-rock spodumene beneficiation |

| High-pressure grinding rolls (HPGR) | Proven for pegmatite comminution; expensive to procure and install |

| Ore sorting technology | Pre-concentration capability that reduces downstream processing costs |

| On-site power station | Eliminates grid connection costs in a region without reliable power access |

| Camp and accommodation | Reduces operational mobilisation costs by years of construction time |

| Airport access | Logistics lifeline in a remote region with no road access year-round |

| Tailings management facility | Pre-permitted and operational; avoids multi-year regulatory build |

Building equivalent infrastructure from greenfield would cost multiples of the C$12 million option fee, and would consume years of permitting, construction, and community engagement time before a single ore tonne could be processed. The brownfield premium embedded in the Renard site is therefore not reflected in the option price — it is reflected in the risk and timeline compression it provides relative to any competing development pathway.

Dense Media Separation and Spodumene: A Technically Compatible Circuit

One of the less widely understood aspects of this strategy is how naturally the Renard plant's existing circuit design maps onto the requirements of spodumene pegmatite processing. Furthermore, understanding the lithium mining process more broadly reveals why this compatibility matters so significantly. This is not an obvious conversion, and it is worth examining the technical logic carefully.

Spodumene, the primary lithium-bearing mineral in hard-rock pegmatite deposits, has a specific gravity of approximately 3.1 to 3.2 g/cm³, which places it comfortably within the density separation range that dense media separation circuits are designed to exploit. Diamond processing historically used DMS to separate the relatively dense kimberlite-hosted diamonds from lighter waste material. The same physical principle — exploiting density contrasts between target mineral and gangue — applies directly to separating spodumene from quartz, feldspar, and mica in a pegmatite ore.

High-pressure grinding rolls, which feature prominently in the Renard plant, are particularly well-suited to pegmatite comminution. Pegmatite ore tends to be coarse-grained and competent, and HPGR technology reduces energy consumption per tonne compared to conventional ball milling while generating a product size distribution that feeds efficiently into downstream DMS and flotation circuits. Ore sorting technology adds a further layer of pre-concentration upstream of the primary circuit, reducing the mass of material that needs to be fully processed and lowering reagent and energy costs per unit of concentrate produced.

That said, Li-FT will need to resolve several technical unknowns during the option period:

- Whether reagent chemistry adjustments are needed for lithium flotation versus diamond concentration

- The degree of circuit modification required to handle pegmatite ore hardness and fragmentation behaviour relative to kimberlite

- Tailings chemistry differences between diamond processing residues and spodumene flotation tailings, and any associated permitting implications

- Actual throughput efficiency when processing Adina ore through a circuit designed for a different ore type

In addition, advances in spodumene extraction techniques may offer further guidance on how circuit adaptations should be prioritised during the feasibility phase.

The Winsome Resources Precedent: What a Terminated Option Actually Signals

Before Li-FT, the Renard asset attracted interest from Winsome Resources, an Australian-listed lithium explorer that secured a similar option in 2024. That option was terminated in July 2025, with market conditions in the lithium sector widely cited as a contributing factor. Lithium carbonate equivalent prices fell from a peak of over US$80,000 per tonne in late 2022 to below US$10,000 per tonne by mid-2024, creating a capital allocation environment in which even compelling strategic assets were being released rather than exercised.

The termination carries two distinct readings, and investors in Li-FT should hold both simultaneously.

The first reading is cautionary: a well-resourced company with direct strategic motivation evaluated the Renard asset during a lithium downturn and concluded that the risk-return profile did not justify proceeding. That judgment was made by a team with full access to technical data rooms, and it should not be dismissed.

The second reading is constructive: the fact that a second company has pursued the same asset within twelve months of the first option's termination suggests the underlying brownfield value proposition is resilient enough to attract repeat institutional interest, even before lithium prices have materially recovered. Strategic assets do not stay orphaned indefinitely. The question is whether the timing and the holder are the right combination.

"The Winsome termination did not invalidate the Renard thesis. It stress-tested it under the worst commodity conditions in a decade, and the asset remained attractive enough for a follow-on bid. That is a form of validation."

Adina as the Feedstock Foundation: The Hub-and-Spoke Logic

The Adina Lithium Project represents the primary feedstock rationale for the Renard processing hub. Located approximately 60 kilometres north of Renard, Adina's proximity enables a logistics model that would be cost-prohibitive if the processing facility were located in a different region entirely.

The James Bay lithium corridor in Québec has emerged as one of the most resource-dense hard-rock lithium regions in North America. Multiple pegmatite systems have been identified across the corridor, which raises the possibility that the Renard hub, if commissioned, could eventually process third-party ores from neighbouring projects under tolling agreements. This hub-and-spoke model has been successfully deployed in other mining jurisdictions and represents significant potential upside not fully captured in a single-project analysis.

The regional infrastructure advantages extend beyond proximity. The James Bay area benefits from:

- Access to Québec's hydroelectric grid in parts of the corridor, offering some of the lowest-carbon and lowest-cost power available to any mining operation in North America

- Established Cree Nation community relationships built through decades of resource development in the region

- Provincial regulatory frameworks with meaningful experience processing mining permits in subarctic environments

- A growing network of road and air infrastructure developed partly through prior resource projects including Renard itself

Scenario Analysis: Four Pathways for the Option Period

The two-year option structure creates a defined decision window. Li-FT must complete a technical, economic, environmental, and social feasibility study within that window, or negotiate an extension, before determining whether to exercise the option and commit the full acquisition capital.

| Scenario | Key Assumption | Likely Outcome |

|---|---|---|

| Base Case | LCE prices recover to US$15,000/t by mid-2027 | Feasibility confirms positive NPV; option exercised; DFS commenced |

| Upside Case | LCE prices exceed US$20,000/t; Adina resource upgraded | Accelerated timeline; strategic partnership or offtake discussions initiated pre-exercise |

| Downside Case | LCE prices remain below US$10,000/t through 2027 | Option allowed to lapse; C$12M fee expensed as exploration expenditure |

| Extension Case | Feasibility requires additional technical or permitting work | One-year extension exercised; final decision deferred to mid-2029 |

Disclaimer: The above scenario table is illustrative and speculative in nature. Lithium price forecasts are subject to significant uncertainty, and outcomes will depend on a wide range of factors including global EV adoption rates, supply additions, and macroeconomic conditions. This does not constitute financial advice.

The Social and Environmental Dimensions That Will Define Execution

No feasibility outcome, however technically compelling, will translate into a viable project without meaningful engagement with Cree Nation communities in the Eeyou Istchee region. Free, prior, and informed consent (FPIC) is both a legal requirement under Canadian federal and Québec provincial frameworks and a practical prerequisite for maintaining social licence during construction and operations.

The Renard mine has an existing relationship history with local Cree communities from its diamond mining era, which provides a starting point for engagement but does not guarantee a straightforward pathway. Transitioning from diamond processing to lithium processing introduces new questions around tailings chemistry, water management, and long-term land use that will require transparent community consultation processes.

Environmental permitting will also require careful attention to the differences between diamond and lithium processing chemistry. Spodumene flotation typically involves reagent systems distinct from those used in kimberlite processing, and regulators will need to evaluate whether existing environmental approvals extend to the modified process or require amendment. This is a solvable problem, but it is not a trivial one, and it will consume a meaningful portion of the option period's timeline.

The next major ASX story will hit our subscribers first

ASX Listing Timing and the Capital Markets Dimension

The timing of this announcement within Li-FT's first month of trading on the Australian Securities Exchange is strategically significant. The ASX has historically provided Canadian and other international critical minerals companies with access to a retail and institutional investor base that has demonstrated strong appetite for battery metals narratives, particularly in the lithium and rare earths space.

By structuring a major strategic announcement to coincide with early ASX trading visibility, Li-FT is simultaneously establishing its investment thesis for a new investor audience and signalling that its management team is prepared to move decisively when opportunities arise. The C$12 million option fee, while material for a company of Li-FT's size, is positioned as a defined-cost, time-limited evaluation rather than an open-ended capital commitment.

This structuring approach should resonate with sophisticated critical minerals investors familiar with option-based project acquisition strategies. Evolving lithium extraction technologies are also shifting investor expectations around what constitutes a credible processing pathway, adding further context to why the Renard facility's existing circuit compatibility is viewed so favourably.

Australian investors have funded several Canadian lithium projects in recent years, and the ASX listing provides Li-FT with a capital channel that complements its existing TSXV investor base. This could prove important if the feasibility study generates results that support moving toward a development financing round.

Is Brownfield Conversion the Structural Future of Canadian Lithium Processing?

The Renard opportunity is unlikely to be unique. Canada's mining history has produced a substantial inventory of dormant or distressed processing facilities across remote and semi-remote jurisdictions, many of which were built to handle hard-rock ores with physical characteristics broadly comparable to lithium pegmatites. As greenfield capital costs continue to escalate and permitting timelines lengthen, the economic logic of repurposing stranded infrastructure is becoming increasingly difficult to ignore.

Several structural factors are reinforcing this trend:

- Capital scarcity in the junior mining sector is driving companies toward lower-capex entry points, of which brownfield options are the most accessible. Consequently, the junior mining investment landscape is increasingly rewarding creative asset structuring over conventional greenfield development.

- Processing capacity is increasingly recognised as a strategic bottleneck in the North American battery supply chain, separate from and arguably more valuable than raw resource extraction.

- Existing permits at brownfield sites compress the regulatory timeline in ways that are genuinely difficult to replicate through greenfield development, regardless of how well-funded a new project might be.

- Community relationships established through prior operations provide a social licence foundation that new entrants must build from zero.

- Infrastructure legacy in remote regions — including power, roads, ports, and accommodation — represents sunk capital that the market is currently pricing at distressed levels relative to its replacement value.

However, it is worth noting that the broader shift toward underground lithium mining in other jurisdictions illustrates how the industry continues to find innovative pathways to reduce surface impact and improve project economics simultaneously.

The Li-FT Renard diamond mine lithium processing hub, if it proceeds through feasibility to construction, would represent one of the first completed examples of this conversion model in the Canadian lithium sector. According to a detailed industry analysis, the strategic rationale behind repurposing dormant hard-rock facilities is gaining traction precisely because the cost and timeline advantages are so difficult to replicate through conventional development. Whether it succeeds or not, the strategic logic it embodies is likely to influence how the next generation of lithium processing capacity in Canada gets built — and who builds it.

This article contains forward-looking analysis and scenario projections that are inherently speculative. Readers should conduct their own due diligence before making investment decisions. Nothing in this article constitutes financial advice.

Want to Spot the Next Major Mineral Discovery Before the Market Does?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries — turning complex mineral data into actionable opportunities the moment they are announced. Explore Discovery Alert's dedicated discoveries page to understand how historic finds have generated substantial returns, and begin your 14-day free trial today to position yourself ahead of the market.