June 15, 2026

The London Gold Auction's Asian Time Zone Problem Is Older Than Most Traders Realise

For over a century, the architecture of global gold pricing has been built around the rhythms of London's financial district. The conventions that govern when gold prices are officially set were not designed with a global marketplace in mind — they emerged from a specific moment in financial history, when the institutions that mattered most to bullion trading all happened to occupy the same time zone. That logic made sense in 1919. It made reasonable sense in 1968. In 2026, with Asian institutions now among the most consequential buyers of physical gold on earth, it is increasingly difficult to defend.

The discussion around moving the London gold auction to an earlier time for Asian traders has moved from background industry chatter to formal public commentary from the London Bullion Market Association (LBMA) itself — a signal that what was once considered an operational inconvenience is now being treated as a structural deficiency worth addressing.

When big ASX news breaks, our subscribers know first

Understanding the LBMA Gold Price Benchmark

The LBMA Gold Price is the most widely referenced gold benchmark in the world. It is set twice each day through an electronic auction platform, with the morning (AM) auction running at 10:30 a.m. London time and the afternoon (PM) auction at 3:00 p.m. London time. Both prices are denominated in US dollars per troy ounce.

The benchmark is not merely a reference number for financial traders. It underpins an enormous range of real-world transactions:

- Central bank reserve valuations use it to mark gold holdings to market

- Mining company offtake agreements and physical gold sales are often priced directly against it

- Refinery purchase contracts settle against the AM or PM fix depending on the transaction type

- Gold-backed ETF net asset values are calculated using LBMA reference prices

- Over-the-counter (OTC) derivatives referencing gold commonly use it as the settlement benchmark

The LBMA Gold Price is set twice daily at 10:30 a.m. (AM) and 3:00 p.m. (PM) London time, denominated in US dollars via an electronic auction platform. This benchmark underpins pricing for gold contracts, central bank reserves, refinery transactions, and ETF valuations globally.

The electronic auction replaced the old telephone-based London Gold Fix in March 2015, following regulatory scrutiny and manipulation concerns that had emerged around similar benchmark-setting mechanisms in other markets. The transition brought greater transparency and an auditable price formation process, but the underlying timing architecture remained unchanged. The LBMA and COMEX markets continue to serve as the twin pillars of global gold price discovery, even as debate grows around their structural accessibility.

A Benchmark With a 107-Year History of Structural Adaptation

Understanding why the AM auction runs at 10:30 a.m. requires a brief detour through financial history. The first daily London gold pricing auction was established in 1919, convened at N M Rothschild and Sons in St Swithin's Lane. Five major bullion dealers would agree on a price at which supply and demand balanced — a process that took place once a day, timed to coincide with London's working hours.

The system remained a single daily fixing for nearly five decades. Then, in 1968, a second afternoon auction was introduced. The rationale was straightforward: American financial markets had grown significantly in their importance to global gold trading, and a single morning price left US participants operating without a benchmark that reflected active New York market conditions. The 3:00 p.m. London fix corresponded to morning trading hours on the US East Coast, providing a relevant reference point for American institutions.

This historical precedent is significant. The LBMA's own institutional structure has already demonstrated a willingness to adapt benchmark timing to accommodate the world's dominant physical gold demand centres. In 1968, that meant accommodating the United States. The parallel being drawn by market participants today is that Asia now occupies a structurally equivalent position — and that the absence of an Asian-hours benchmark reflects an institutional lag rather than a deliberate design choice.

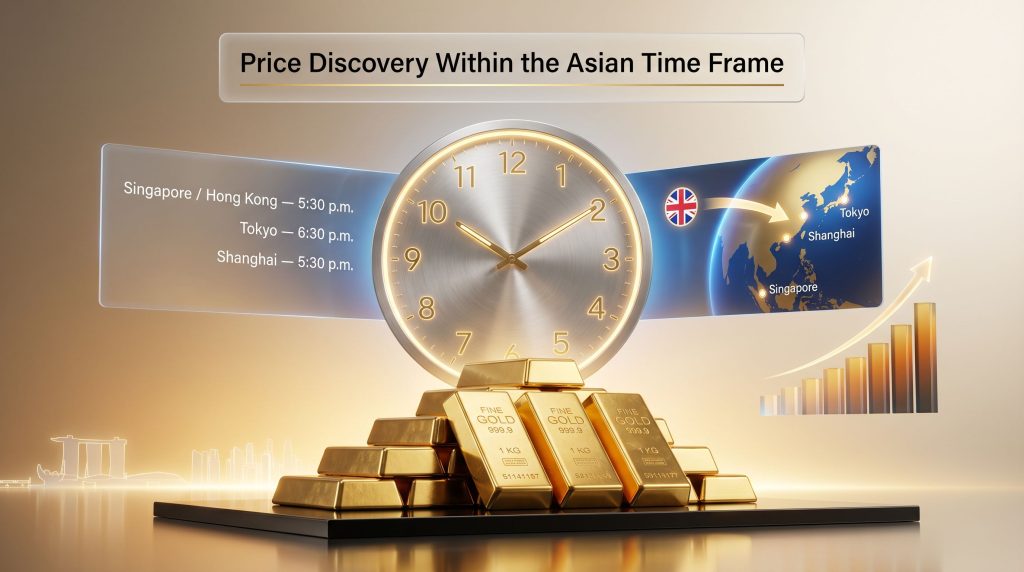

The Time Zone Arithmetic That Disadvantages Asian Institutions

When the AM auction runs at 10:30 a.m. in London, the clock in Asia tells a very different story. For the major financial centres that have become central to physical gold flows, the benchmark is set after their primary trading sessions have already closed or are winding down.

| City | Local Time When AM Auction Runs | Trading Session Status |

|---|---|---|

| Singapore / Hong Kong | 5:30 p.m. | Late afternoon / post-session |

| Tokyo | 6:30 p.m. | After market close |

| Shanghai | 5:30 p.m. | Late afternoon |

| Sydney | 7:30 p.m. | Evening / after hours |

| Mumbai | 3:00 p.m. | Mid-afternoon |

The practical consequences of this misalignment are more significant than they might initially appear. An Asian central bank or refinery seeking to execute a physical gold purchase against the LBMA benchmark must do so in the context of a price that will only be determined hours after their active trading day has ended. This creates several compounding inefficiencies:

- Overnight pricing risk accumulates between the close of Asian trading and the London AM fix, leaving hedges imprecise and exposures unmanaged

- Arbitrage opportunities open between Asian spot prices and the eventual London benchmark, creating costs that are ultimately passed on in transaction spreads

- Hedging accuracy for Asian gold producers and refiners is structurally compromised when the reference price is generated outside their operational time window

- Institutional participation in the auction itself is constrained when bidding occurs at times that fall outside normal working hours for Asian treasury teams

This is not merely an inconvenience for traders in Asia. It represents a systematic disadvantage embedded into the world's most important gold pricing mechanism — one that disproportionately affects the regions now responsible for the largest share of physical gold consumption globally.

What the LBMA Is Actually Considering

At the Asia-Pacific Precious Metals Conference held in Singapore, LBMA Chief Executive Officer Ruth Crowell addressed the timing question directly. She confirmed that the association is considering moving its morning gold auction to an earlier slot, framing the potential change as a response to a long-standing request from the market. Furthermore, she noted that the current geopolitical and structural environment makes the conversation particularly timely. As reported by the Financial Times, this represents one of the most significant potential structural changes to the benchmark in decades.

Critically, Crowell did not specify any candidate time or provide an implementation timeline. This means the discussion remains at an exploratory stage, and no formal consultation process has been publicly announced. Market participants should treat this as a signal of institutional intent rather than a confirmed operational change.

If the AM auction were to shift earlier, a window of approximately 7:00 to 8:00 a.m. London time would represent the most likely range for achieving meaningful Asian market overlap:

| Scenario | London Time | Singapore / HK | Tokyo | Shanghai |

|---|---|---|---|---|

| Current AM Auction | 10:30 a.m. | 5:30 p.m. | 6:30 p.m. | 5:30 p.m. |

| Earlier Window (Illustrative) | 7:00–8:00 a.m. | 2:00–3:00 p.m. | 3:00–4:00 p.m. | 2:00–3:00 p.m. |

A benchmark in this window would allow Singapore, Hong Kong, Shanghai, and Tokyo participants to actively engage during normal business hours, improving both price discovery quality and institutional participation volumes.

Why Asian Demand Now Carries Structural Weight

The case for moving the London gold auction earlier for Asian traders is ultimately grounded in where physical gold actually goes. China and India together account for roughly 50% of global consumer gold demand in a typical year, according to World Gold Council data. Furthermore, central bank gold demand across Asia has surged dramatically over the past decade, with monetary authorities accumulating gold at historically elevated rates.

Several converging forces are amplifying Asia's gravitational pull on gold markets:

- Central bank de-dollarisation strategies have led Asian monetary authorities to accumulate gold at historically elevated rates as a reserve diversifier

- Retail and institutional demand in China has expanded dramatically, with the Shanghai Gold Exchange now operating as a significant physical delivery platform in its own right

- Geopolitical risk premiums driven by US-China trade tensions and broader multipolar financial system uncertainty have reinforced gold's appeal as a neutral reserve asset among Asian institutions

- Singapore's emergence as a bullion clearing hub, including a recently announced gold clearing initiative involving major international banks, signals infrastructure investment consistent with a growing regional centre

The addition of the afternoon auction in 1968 was a direct institutional response to growing US market influence over global gold pricing. Analysts note that Asia's current share of physical gold demand presents a structurally equivalent case for accommodation — an earlier AM auction that aligns with the active trading hours of the world's largest physical gold consumers.

China's gold market dominance has, in particular, accelerated the urgency of this discussion, as Chinese institutions now represent some of the most significant participants in physical bullion flows globally.

The next major ASX story will hit our subscribers first

The Arguments On Both Sides

The case for an earlier London gold auction is compelling when viewed through the lens of market access and price discovery quality. However, the transition is not without legitimate operational concerns.

Arguments supporting an earlier auction time:

- Real-time benchmark access during Asian business hours would reduce overnight hedging risk for miners, refiners, and central banks across the region

- Broadening the geographic participation base of the auction would likely improve price discovery by incorporating more diverse order flow

- Aligning the world's most credible gold benchmark with the world's largest physical demand base strengthens the LBMA's long-term institutional relevance

- Historical precedent exists: the 1968 PM auction was created for precisely this reason, demonstrating the mechanism's adaptability

Arguments for caution or phased implementation:

- Liquidity in London's bullion market is thinner during early morning hours, which could widen bid-ask spreads and reduce auction stability during the transition period

- European and US participants who have built compliance, settlement, and reporting workflows around the existing 10:30 a.m. benchmark would require operational adjustments

- Electronic auction platform participants distributed across multiple time zones would need to confirm readiness to submit orders at earlier London times

- No confirmed timeline, consultation structure, or shortlisted time slots have been announced, suggesting the feasibility work is still in early stages

Singapore's Expanding Role and the Limits of Regional Alternatives

Any discussion of Asian gold market infrastructure must account for Singapore's rapidly evolving role. The city-state has attracted significant investment in gold vaulting, refining, and now clearing infrastructure. The recently announced gold clearing initiative involving major international banks based in Singapore represents a meaningful step toward reducing Asia's settlement dependence on London.

However, regional gold benchmarks that have emerged in Asia over the years have consistently struggled to displace the LBMA price in contract specifications and institutional frameworks. The Shanghai Gold Exchange's yuan-denominated benchmark, while significant domestically, has not achieved the cross-border adoption that would challenge LBMA primacy.

This dynamic actually strengthens the case for an LBMA timing adjustment rather than a wholesale migration to competing benchmarks. A recognised LBMA auction that runs within Asian trading hours carries far more institutional credibility than a parallel pricing mechanism, and preserves the network effects that make the London benchmark valuable in the first place. Consequently, the gold market surge driven by Asian institutional buying has only reinforced the urgency of making the benchmark more accessible to the region's participants.

Frequently Asked Questions

What is the LBMA Gold Price and why is it considered the global standard?

The LBMA Gold Price is a twice-daily benchmark set through an electronic auction administered by ICE Benchmark Administration. It is considered the global standard because the vast majority of physical gold contracts, central bank valuations, ETF NAV calculations, and OTC derivatives globally reference it for settlement and pricing purposes.

What time is the London gold auction currently held?

The AM auction runs at 10:30 a.m. London time and the PM auction at 3:00 p.m. London time, both denominated in US dollars per troy ounce.

Why does the auction time matter for traders in Asia?

When the AM auction runs at 10:30 a.m. in London, it is already late afternoon or early evening across most major Asian financial centres. This means Asian institutions cannot effectively use the benchmark for intraday hedging or real-time price discovery during their normal working hours.

Is the LBMA planning to add a third auction or just move the existing one?

Based on available public commentary, the LBMA is considering moving the existing AM auction to an earlier time rather than adding a third daily auction. No official announcement has confirmed either option.

How would an earlier auction affect European and US traders?

European participants would need to adjust workflows to an earlier benchmark time, while US-based institutions would potentially lose the overlap between the AM fix and early New York market activity. These are non-trivial operational considerations.

When was the London Gold Fix replaced and why?

The telephone-based London Gold Fix was discontinued in March 2015 following regulatory scrutiny over potential manipulation risks in opaque benchmark-setting processes. It was replaced by a transparent electronic auction platform administered by ICE Benchmark Administration.

What the Timing Debate Reveals About Gold's Shifting Centre of Gravity

The conversation about a London gold auction earlier time for Asian traders is not, at its core, a technical discussion about scheduling. It is a reflection of a deeper structural reality: the institutions and economies that now drive physical gold demand are no longer primarily located in the time zones that the benchmark's architecture was designed to serve.

Every major timing change in the history of London gold pricing has followed a shift in where market power actually resides. The 1919 single-fix era reflected London's unchallenged dominance in global bullion markets. The 1968 PM auction reflected the United States' rise as a major force in gold trading. The question being asked today is whether the current moment represents a comparable inflection point for Asia.

The growth of central bank gold reserves across Asian economies has added further momentum to this debate, as sovereign wealth managers increasingly seek benchmark pricing that aligns with their operational hours. Moreover, analysts tracking the broader shift in gold market dynamics have noted that the LBMA's willingness to publicly engage with this question at a Singapore conference is itself a significant data point. What remains to be seen is whether the operational, liquidity, and stakeholder challenges can be resolved in a way that maintains the benchmark's integrity while extending its practical utility to the institutions that increasingly determine where gold actually flows.

Disclaimer: This article is for informational purposes only and does not constitute financial or investment advice. References to price scenarios and structural changes reflect publicly available information and analytical commentary. The LBMA has not confirmed any specific new auction time or implementation timeline.

Want to Stay Ahead of Major ASX Mineral Discoveries Before the Broader Market?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, turning complex data across 30-plus commodities into clear, actionable insights for both traders and long-term investors — explore historic discovery returns on Discovery Alert's dedicated discoveries page and begin your 14-day free trial today to secure a genuine market-leading edge.