July 21, 2026

The Rarest Commodity in Modern Mining Is Not Copper or Silver. It Is Certainty.

Across the global mining landscape, certainty is vanishing. Projects face water crises in the Atacama Desert, social licence failures in Peru, power deficits in sub-Saharan Africa, and processing infrastructure that must be built from zero at costs running into billions before a single tonne of ore is processed. Against this backdrop, the attributes that define a genuinely world-class critical metals project have become increasingly obvious and increasingly scarce: massive scale, reliable grades, established infrastructure, an accessible skilled workforce, an identifiable buyer for the product, and a jurisdiction that functions.

Few projects in the world meet even three or four of these criteria simultaneously. The Lumina Metals Poland copper silver project, centred on the Nowa Sól deposit in southwestern Poland, meets all of them. Understanding why requires a working knowledge of one of the most remarkable geological formations in existence, a company that has quietly become one of the most important silver producers on the planet without most investors ever noticing, and a franchise builder with an unmatched track record of creating and monetising mining value across multiple commodity cycles.

When big ASX news breaks, our subscribers know first

The Geology That Built a 70-Year Industry

The Kupferschiefer Formation and What It Contains

The Kupferschiefer, meaning copper shale in German, is a sedimentary rock horizon that extends across a significant portion of central Europe. In Poland specifically, this formation has supported the mining operations of KGHM Polska Miedź for seven continuous decades, making it one of the most productive copper-silver geological systems in recorded history. The mineralisation style is sediment-hosted, meaning copper and silver are distributed through the rock matrix rather than concentrated in veins or porphyry intrusions, which produces a predictable and consistent grade profile across large areas.

What makes the Kupferschiefer exceptional is the persistent association between copper and silver within the same mineralised horizon. This co-product relationship is not incidental. It is a defining characteristic of the entire belt. At current commodity price levels, the silver content of deposits hosted within this formation contributes approximately half of the total economic value of the extracted ore, making silver a genuine co-product rather than a trace byproduct.

KGHM and the Secret at the Heart of Poland's Mining Industry

KGHM Polska Miedź is a partially state-owned company that rarely appears on the radar of retail precious metals investors, despite the fact that it produces approximately 42 million ounces of silver annually, placing it second globally among silver producers, behind only Mexico's Fresnillo. This near-invisibility is a function of corporate culture rather than commercial relevance. KGHM is described by those familiar with it as a traditionally managed Polish enterprise with limited promotional activity, no meaningful retail investor following outside Poland, and a preference for operational continuity over market-facing communications.

This paradox is commercially significant. One of the world's two largest silver producers is essentially unknown to the global silver investor community, which means the geological system that has powered its output for 70 years has similarly escaped broader market attention. Lumina Metals is positioned directly on that same Kupferschiefer horizon.

The smelter KGHM constructed approximately 50 years ago at Głogów, located roughly 20 kilometres from the Nowa Sól deposit, was originally built with a nameplate capacity of 600,000 to 650,000 tonnes of copper throughput annually. Today it processes approximately 380,000 tonnes, meaning it operates well below its designed capacity and currently imports copper concentrate from international sources to partially fill that gap. This situation creates a commercially logical alignment between KGHM's operational requirements and Lumina's projected production profile.

Nowa Sól: Defining the Resource at Scale

What the Measured and Indicated Resource Actually Represents

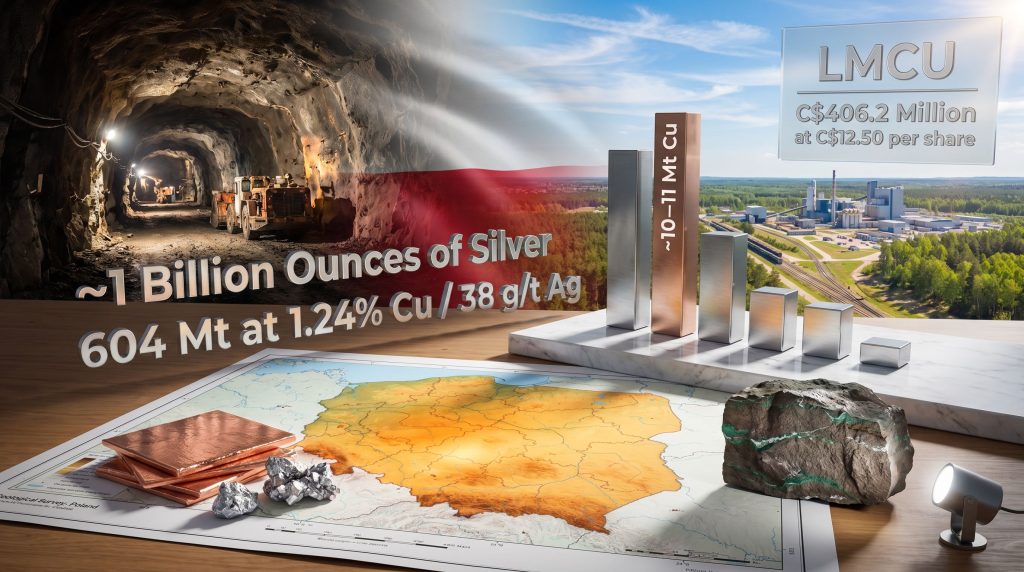

The Nowa Sól deposit has been delineated through more than 51,000 metres of drilling across a 120 square kilometre concession area. The resulting Measured and Indicated resource stands at 604 million tonnes grading 1.24% copper and 38 grams per tonne silver. The combined metal content within these classifications is reported at approximately 10 million metric tonnes of copper and more than one billion ounces of silver.

These numbers occupy a category of their own in the universe of undeveloped copper-silver systems globally. Furthermore, the silver market supply constraints affecting the broader sector make a deposit of this scale even more strategically significant. Consider the following comparison:

| Metric | Nowa Sól (Lumina Metals) | Typical Tier-1 Copper Project |

|---|---|---|

| Copper resource (Mt) | ~10 | 5 to 8 |

| Silver resource (Moz) | 1,000+ | Less than 100 |

| Concession area (sq. km) | 120 | Varies |

| Drilling completed (m) | 51,000+ | Varies |

| Projected annual copper output (kt) | 290,000 to 300,000 | 100,000 to 200,000 |

| Projected annual silver output (Moz) | 28 to 30 | Less than 5 |

| Mine life (years) | 25 to 30 | 20 to 25 |

The silver resource figure warrants particular attention. Most large undeveloped copper projects contain silver as a minor trace element. Nowa Sól contains silver at a grade and tonnage combination that places it in a completely different competitive category when assessed through the lens of silver resource ownership per share.

A Three-Project Portfolio With Combined Scale Approaching 1.5 Billion Ounces

Beyond Nowa Sól, Lumina has identified additional deposits within its Polish concession holdings. The Sulmierzyce and Mozów deposits, located approximately 100 kilometres from the primary asset, represent early-stage discoveries that the company intends to advance through systematic drilling. Current combined silver resources across the portfolio are estimated at approximately 1.5 billion ounces, with exploration at Sulmierzyce potentially pushing that figure toward 2 billion ounces if results confirm a deposit of similar scale to Nowa Sól.

If realised, this would position Lumina as the largest holder of silver resources of any company globally, a distinction with significant implications for how the silver investment community values the stock.

Why Poland Is a Compelling Mining Jurisdiction

Infrastructure That Takes Decades to Build Elsewhere

The most underappreciated aspect of the Lumina Metals Poland copper silver project is the infrastructure context in which it sits. Mining projects in traditional copper-producing geographies such as Chile, Peru, and the Democratic Republic of Congo face infrastructure development costs and timelines that can consume years and billions of capital before any economic ore is processed. Poland presents an almost opposite situation:

- Rail access exists in the region and does not require greenfield construction

- Power grid connectivity is available without the need for dedicated transmission infrastructure

- Water supply is accessible from existing regional sources

- The deposit sits beneath a managed forest plantation, removing the prospect of community displacement or agricultural interference

- Approximately 100,000 experienced underground miners in Poland are currently transitioning out of the declining domestic coal sector, representing a readily available, skilled, and motivated workforce

- The Głogów smelter, operating at below-capacity and actively importing concentrate from abroad, sits within 20 kilometres of the deposit

This last point deserves emphasis. Most new copper projects must identify a smelter buyer for their concentrate, negotiate commercial terms, and then either ship product internationally or plan for domestic processing infrastructure. Lumina already has a physically proximate, concentrate-hungry buyer with established infrastructure and a commercial interest in sourcing locally.

The European Critical Metals Context

Europe consumes substantially more copper than it produces domestically. This supply-demand imbalance is structural and is expected to widen as the continent accelerates its transition toward electrification, renewable energy deployment, and electric vehicle manufacturing. The broader copper supply crunch unfolding globally reinforces why a project capable of delivering 290,000 to 300,000 tonnes of copper annually represents a material addition to European domestic supply. This is not a project-specific policy designation but rather a factual observation about where Nowa Sól sits within the broader European industrial supply chain.

The KGHM Letter of Intent and What It Signals Commercially

From Geological Neighbour to Commercial Partner

In May 2025, Lumina Metals formalised a cooperation agreement with KGHM Polska Miedź, structured around a framework for supplying copper concentrate to the Głogów smelter. Lumina and KGHM signed a Letter of Intent for strategic cooperation and copper concentrate supply, marking a significant commercial milestone. This is a commercial offtake arrangement between two independent parties. It does not involve KGHM taking an equity position in the Lumina project, and it should not be characterised as a joint venture or government backing given KGHM's partial state ownership.

The commercial logic is straightforward. KGHM needs concentrate. Lumina has a deposit capable of producing the precise volume that would bring the Głogów smelter to approximately full nameplate capacity. Geographic proximity eliminates long-haul transport costs and logistical complexity. Both parties benefit from formalising a supply pathway before capital commitments are made.

A signed Letter of Intent at this stage of project development is a commercially meaningful signal, not a guarantee. It communicates that the region's dominant copper processor views Lumina's deposit as a credible future supply source and is willing to invest early-stage commercial attention in the relationship. For investors, it represents de-risking at the offtake end of the value chain.

Why Smelter Proximity Is a Structural Advantage

Processing copper concentrate into refined metal requires either a nearby smelter or long-distance concentrate shipping, which carries penalties in the form of moisture charges, payable metal deductions, and freight costs. Projects without a proximate smelter must negotiate with buyers who may be geographically distant and commercially indifferent. Lumina's situation inverts this dynamic entirely. The smelter is not just nearby. It is actively undersupplied and currently paying international shipping costs to source the concentrate it needs.

The IPO: Canada's Largest Mining Listing in Recent Years

Capital Structure and Market Context

Lumina Metals listed on the Toronto Stock Exchange under the ticker symbol LMCU on April 30, 2025, raising approximately C$406.2 million at C$12.50 per share, implying an initial market capitalisation of approximately C$1.3 billion. This was described as one of the largest Canadian mining IPOs in recent years and was anchored by institutional investors including Capital Group, one of the world's largest asset managers.

The institutional composition of the shareholder register matters for long-duration assets like this one. Sticky, long-horizon capital from recognisable institutions signals that sophisticated investors have conducted deep diligence and are willing to hold through the multi-year development cycle ahead.

Why the Share Price Dipped Below IPO Price

Early post-IPO share price weakness is common in large mining listings and does not necessarily reflect deteriorating project fundamentals. Several specific dynamics explain the price behaviour in Lumina's case:

- Legacy investors with a very low cost base who entered the company as early as 2011 used the IPO as a liquidity event after 15 years of capital lock-up

- Institutional allocation compression, where some investors who requested large positions received as little as 5% of their requested allocation, making the resulting position too small to be meaningful within their portfolio mandate and prompting early exits

- Brand recognition lag, where many retail and mid-tier institutional participants were unfamiliar with the Lumina Metals name or confused it with predecessor Lumina entities from earlier in the franchise's history

Historical precedent across large mining IPOs consistently shows that initial selling pressure from these dynamics resolves as the institutional base stabilises, research coverage initiates, and the broader investment community develops familiarity with the asset. Lumina has eight investment banks preparing independent research reports, which will materially expand awareness of the investment case.

The next major ASX story will hit our subscribers first

Ross Beaty and the Lumina Franchise Model

A Career Defined by Repeatable Value Creation

Ross Beaty's track record in mining represents one of the most consistent records of discovery, development, and monetisation in the history of the junior and mid-tier mining sector. This is his 16th public company, and the Lumina franchise model he pioneered in the early 2000s has been applied across multiple asset classes, geographies, and commodity cycles.

The model is straightforward in concept, though demanding in execution:

- Identify undervalued geological systems during periods of commodity price weakness

- Acquire concessions or early-stage rights at low cost

- Apply systematic exploration to define and expand resources

- De-risk the asset through feasibility work, environmental baseline studies, and commercial agreements

- Either monetise to a major mining company or advance to development independently

The historical exit record across the Lumina franchise illustrates the model's commercial outcomes:

| Asset | Acquirer | Outcome |

|---|---|---|

| Regalo (Chile copper) | Japanese consortium | US$4 billion mine constructed; now part of Lundin Mining |

| Lumina Resources (Canada) | Western Copper and Gold | Casino deposit ongoing development asset |

| Lumina Copper Peru | Major Chinese mining group | Strategic acquisition |

| Lumina Copper Chile (second) | Teck Resources | Portfolio integration |

| Lumina Copper Argentina | First Quantum Minerals | Strategic acquisition |

| Lumina Gold Ecuador | Major Chinese company | Sold May 2024 |

An important and often overlooked aspect of this track record is the long-cycle nature of the value creation. Early seed investors in the Lumina group circa 2002 have realised returns described as hundreds of times their original capital across the various exits. This is not a feature of short-cycle speculation but of holding high-quality assets through multiple commodity cycles until strategic buyers are compelled to act.

Jordan Pandoff and the Glencore Pedigree

Lumina Metals' Chief Executive Officer, Jordan Pandoff, brings a commercial development background from Glencore, one of the world's largest commodity trading and mining companies. Within that organisation, Pandoff focused on copper business development, which involved evaluating copper deposits globally for strategic acquisition interest. This background is directly applicable to Lumina's situation: Pandoff has seen the full spectrum of what major mining companies look for in a development asset, and he is now building one to those specifications.

The Lassonde Curve and Where Lumina Sits

Understanding the Value Cycle in Mining

The Lassonde Curve describes the typical progression of a mining company's market valuation from initial discovery through to sustained production. It was developed by Pierre Lassonde of Franco-Nevada and is widely used as a conceptual framework in the mining investment community.

The curve follows three broad phases:

Stage 1: Discovery and Exploration Premium. The market assigns speculative value to a new discovery. Valuation rises rapidly as resource estimates grow and the scale of the deposit becomes apparent. Lumina currently occupies the transition between early exploration and resource development, a period that typically attracts the highest narrative-driven valuation premium.

Stage 2: The Development Trough. Feasibility studies, environmental impact assessments, permitting, and pre-construction activities consume years and capital without producing revenue. The market often loses interest during this phase, compressing valuation relative to fundamental value. For Lumina, this period encompasses the path toward a mining licence, expected around 2030.

Stage 3: Production Re-Rating. Once construction commences and production begins, the market re-rates the company against cash flow multiples rather than resource multiples. This phase, which for a 25 to 30-year mine like Nowa Sól extends across multiple commodity cycles, produces the second major value inflection.

For investors with a multi-year time horizon, the strategic question is not whether a major mining company will eventually approach Lumina, but at what point along this curve the offer arrives and whether the board at that time considers it adequate given the project's stage and commodity price environment.

Key Risks Investors Should Understand

Poland's Mining Taxation Regime

The single most significant jurisdictional risk attached to the Lumina Metals Poland copper silver project is the current Polish copper-silver tax structure. Introduced in 2012 and calibrated around KGHM's partially state-owned structure, the tax creates an effective combined burden on copper-silver mining activities that approaches approximately 70% under current parameters.

This rate is substantially above the approximately 40% effective rate considered standard across European mining jurisdictions. The commercial impact is material: at 40%, Nowa Sól generates very large cash flows; at 70%, the economics are significantly constrained.

Several points moderate this risk:

- The tax was designed for a single company in a specific ownership structure, not for new private entrants

- Government officials have communicated willingness to revise the framework in advance of any development decision for a new project

- A tax revision would represent normal regulatory modernisation to attract investment, not a project-specific concession

- The commercial viability of Nowa Sól is not contingent on the current rate; it depends on what rate applies at the time of a development decision

Permitting Timeline and Capital Requirements

Key administrative milestones, including the mining licence decision, are expected around 2030, subject to completion of environmental impact assessments, mine design documentation, and approvals from Polish regulatory authorities. The permitting challenges associated with projects of this scale are well understood, and the approximate C$240 million US equivalent raised in the IPO is intended to fund operations through this licensing process.

Total construction capital for a project of this scale will run into the tens of billions of Polish zlotys, which places it firmly in the category of assets that require major mining company involvement or significant project financing structures. This capital scale is itself a filter that narrows the pool of credible acquirers to the largest operators in the copper sector globally.

Could Sulmierzyce Double the Silver Resource Base?

The Case for a Second Billion-Ounce System

The Sulmierzyce deposit, located approximately 100 kilometres from Nowa Sól, represents one of the most compelling exploration opportunities attached to the Lumina portfolio. Early results and geological analysis suggest the potential for a deposit of comparable scale to the primary asset. If subsequent drilling confirms this thesis, the combined silver resource base across Lumina's Polish portfolio could exceed 2 billion ounces, a figure that would make it the largest silver resource holder of any company globally by a significant margin.

The market implications of this scenario are substantial. The global silver investment community is substantial and price-sensitive. A company with confirmed 2-billion-ounce silver resources, located in a functioning EU jurisdiction with established processing infrastructure nearby and an institutional shareholder base, would represent a fundamentally different investment proposition than almost anything currently available in the silver equities market. Micon International's assessment of Lumina's key milestones further reinforces the technical credibility underpinning these resource estimates.

The US Listing and the Silver Narrative

Accessing the World's Largest Retail Investor Market

Lumina's current TSX listing reflects the practical reality that Canada is the world's primary capital market for mining companies. However, the company has stated its intention to apply for a listing on the New York Stock Exchange or NASDAQ as soon as eligible under the Multi-Jurisdictional Disclosure System, which requires a minimum 12-month trading period on the TSX before application.

The US listing strategy is not incidental. The retail silver investor community in the United States is large, engaged, and responsive to silver resource stories at significant scale. Ross Beaty's experience founding Pan-American Silver and building it into one of the world's leading primary silver producers gives him direct insight into this investor base and how it responds to narrative, scale, and management credibility.

A definitive feasibility study will be a critical milestone in advancing the project and attracting the next tier of institutional capital. Furthermore, eight investment banks are preparing independent research reports, which will introduce the investment case to a substantially broader institutional and retail audience over the coming months.

Frequently Asked Questions

What is Lumina Metals' ticker symbol?

Lumina Metals Corp. trades on the Toronto Stock Exchange under the ticker symbol LMCU.

How much silver does the Nowa Sól deposit contain?

The project hosts more than one billion ounces of silver within its Measured and Indicated resource of 604 million tonnes grading 38 grams per tonne silver and 1.24% copper.

What is the relationship between Lumina Metals and KGHM?

In May 2025, Lumina signed a Letter of Intent with KGHM Polska Miedź to negotiate terms for a copper concentrate supply agreement. This is a commercial offtake arrangement and does not involve equity ownership by KGHM in the Lumina project.

How much did Lumina Metals raise in its IPO?

Lumina raised approximately C$406.2 million at C$12.50 per share, implying an IPO market capitalisation of approximately C$1.3 billion.

What is the projected annual production from Nowa Sól?

At full development, the project is designed to produce approximately 290,000 to 300,000 tonnes of copper and approximately 28 to 30 million ounces of silver annually over a mine life of 25 to 30 years.

When could Lumina Metals receive its mining licence?

Key administrative decisions are anticipated around 2030, subject to completion of environmental impact assessments, mine design documentation, and regulatory approvals from Polish authorities.

Is Lumina Metals planning a US stock exchange listing?

Yes. Following the mandatory 12-month trading period on the TSX, Lumina intends to apply for a listing on the New York Stock Exchange or NASDAQ using the Multi-Jurisdictional Disclosure System.

What Separates This From an Ordinary Mining Story

Scale, Infrastructure, and Strategic Buyer Logic

World-class mining deposits share a specific set of attributes: they are large enough to sustain multi-decade production, consistent enough in grade to support long-range financial modelling, located close enough to processing infrastructure to avoid prohibitive logistics costs, and situated in jurisdictions with functional regulatory frameworks. Projects meeting all of these criteria simultaneously are genuinely rare. Industry participants estimate that across the past two decades, the number of globally significant copper discoveries that meet these combined criteria can be counted on one hand.

The Lumina Metals Poland copper silver project sits at the intersection of geological scale, infrastructure availability, an identifiable commercial buyer, an experienced management team with a documented exit track record, and a commodity price environment that is increasingly favourable to both copper and silver. Each of these factors is meaningful in isolation. Together, they define an asset that the world's largest mining companies will be compelled to evaluate.

The strategic buyer universe for an asset of this scale is narrow by definition. Only companies with the balance sheet strength, operational expertise, and concentrate processing capacity to absorb a 290,000-tonne annual copper producer need apply. That narrows the field considerably and, in doing so, concentrates the competitive dynamic among precisely the parties most motivated to acquire rather than lose access to a resource of this magnitude.

This article is intended for informational purposes only and does not constitute financial advice. Mining projects involve significant risks including commodity price volatility, permitting delays, capital requirement uncertainty, and jurisdictional factors. Readers should conduct their own due diligence and consult a licensed financial adviser before making any investment decisions. Forward-looking statements, production estimates, and resource figures referenced in this article are subject to change and are not guarantees of future performance.

Want to Track the Next Major ASX Mineral Discovery Before the Market Moves?

Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time, instantly translating complex mineral data across more than 30 commodities into actionable insights for both short-term traders and long-term investors — explore historic discoveries and the returns they generated, then begin your 14-day free trial at Discovery Alert to position yourself ahead of the broader market.