July 9, 2026

When the Ore Leaves the Mine, the Margin Battle Has Already Begun

Commodity markets tend to fixate on port throughput, vessel loading rates, and spot price movements. Yet for South Africa's manganese exporters, the most consequential cost decisions happen hundreds of kilometres from any coastline. The economics of moving ore from the Northern Cape's Kalahari Manganese Field to an export vessel are shaped by a single fork in the logistics road: truck or train. That choice, made across millions of tonnes annually, is now one of the most commercially significant variables in the country's manganese supply chain.

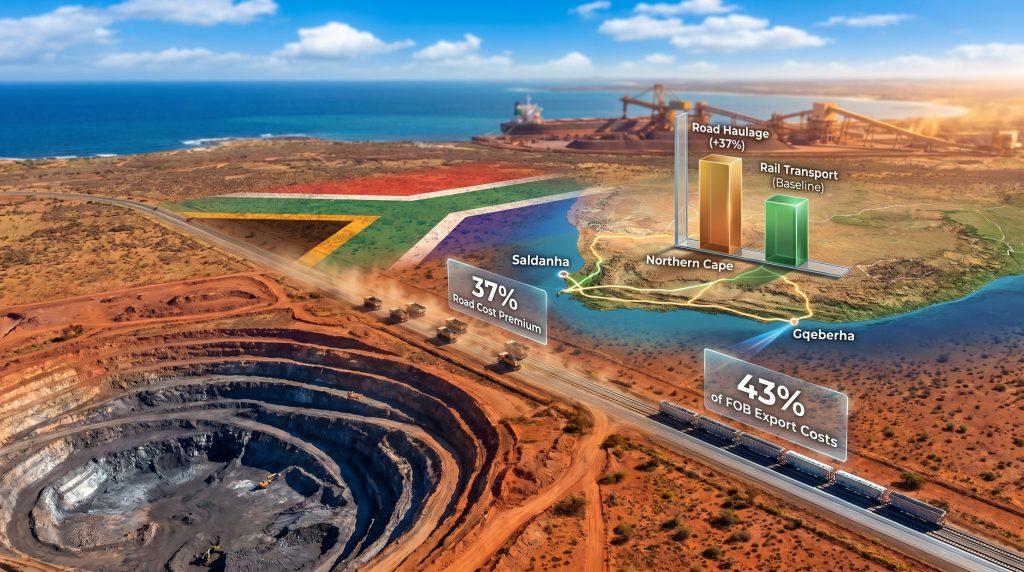

Operational data disclosed by Exxaro Resources in mid-2026 has quantified what many in the industry suspected but rarely measured with precision. Road haulage for manganese ore costs approximately 37% more per tonne than equivalent rail transport across the same corridors. When viewed alongside the broader cost structure, where logistics represent roughly 43% of free-on-board (FOB) export costs, the implication is stark: nearly half of the entire delivered cost burden is absorbed before a single tonne of ore touches a vessel. The Exxaro road cost premium for South Africa manganese exporters is not an operational footnote. It is a structural margin problem.

When big ASX news breaks, our subscribers know first

The FOB Cost Structure Most Analysts Overlook

Understanding why inland transport costs carry such outsized weight requires unpacking what FOB pricing actually means in a manganese export context. Free-on-board is the cost benchmark at which the seller's responsibility ends and the buyer's begins, specifically at the point where cargo is loaded onto the vessel. Everything that happens before that moment, including mining, processing, haulage, and port handling, sits within the seller's cost envelope.

For South African manganese producers, the geography of that pre-FOB journey is punishing. The Kalahari Manganese Field, which contains the world's largest known manganese ore reserves, sits in the Northern Cape, separated from the nearest suitable export ports by distances exceeding 800 kilometres in many cases. Ore destined for Gqeberha (formerly Port Elizabeth) or Saldanha Bay must traverse this distance entirely by land before it can be loaded for international markets.

This distance dynamic is what pushes logistics costs to such a dominant share of the FOB cost structure. Furthermore, when nearly half of export costs are consumed by inland transport, the choice of transport mode becomes the primary lever available to producers seeking margin improvement. Unlike commodity prices and mining margins, which are set by global markets, transport mode is an operational decision. That makes it, in theory, manageable, provided the infrastructure exists to support the more cost-efficient choice.

The 37% Road Cost Premium: What It Means at Scale

A 37% cost premium sounds significant in isolation. Translated into volume terms, it becomes commercially material very quickly.

| Transport Metric | Road Haulage | Rail Transport |

|---|---|---|

| Cost Premium vs. Rail | +37% | Baseline |

| Share of FOB Export Costs (Logistics) | ~43% | ~43% |

| Estimated Volume Still Trucked (Tshipi Borwa) | ~46% of total | ~54% of total |

| Volume Targeted for Rail Shift | >1.5 million tonnes/year | Existing rail users |

To make this concrete: if rail transport costs approximately $15 per tonne across the relevant corridors, road haulage costs roughly $20.55 per tonne for the same journey. Applied to a volume of 460,000 tonnes, which represents 46% of one million tonnes of annual exports, the excess cost burden approaches $2.5 million per year on that parcel alone. Scaled to Tshipi Borwa's full annual production of approximately 3.5 million tonnes, with around 1.6 million tonnes still moving by truck, the aggregate cost disadvantage becomes deeply commercially significant.

These figures are illustrative, based on publicly disclosed cost differentials and modal split data, and should not be treated as audited financial projections.

What makes the Exxaro road cost premium for South Africa manganese exporters particularly difficult to absorb is that it is not a temporary disruption. As long as rail access remains constrained and trucking fills the gap, this premium is a recurring, compounding cost embedded into every tonne exported via the higher-cost route.

Tshipi Borwa and the Kalahari Manganese Field: Understanding the Scale of the Problem

Tshipi Borwa is one of the largest open-pit mines in the world and a central asset in South Africa's manganese export profile. Its annual production of approximately 3.5 million tonnes places it among the highest-volume single-mine operations in the Kalahari Manganese Field, a geological formation that holds an estimated 70 to 80% of the world's known manganese ore reserves according to industry assessments.

The Kalahari Manganese Field ore is predominantly sedimentary in origin, deposited in the Transvaal Supergroup around 2.2 billion years ago. The orebody is broadly stratiform, meaning it follows relatively consistent horizontal layers, which makes large-scale open-pit mining operationally efficient. Manganese grades in the Kalahari field typically range from around 30% to 48% manganese content, with higher-grade lump ore commanding price premiums in steel and ferroalloy markets. The mineralogy is dominated by braunite and hausmannite, which are relatively well-suited to direct export without extensive beneficiation at the mine site.

This geological efficiency at the mine gate is, however, offset by logistical inefficiency at the transport stage. The same remote inland location that allows low-cost open-pit extraction creates the long-haul transport problem that now defines the margin equation. With roughly 46% of Tshipi Borwa's volumes still reaching export ports by road, more than 1.5 million tonnes per year from a single mine is absorbing the higher-cost trucking premium every year.

The critical insight here is that Tshipi Borwa's geology makes it one of the most efficient mines to operate in the world, but that operational efficiency can be significantly undermined by transport cost structures that sit entirely outside the mine gate. A world-class deposit does not automatically produce world-class delivered margins.

Why Expanding Port Capacity Alone Cannot Solve This Problem

The planned 16-million-tonne Ngqura manganese export terminal in the Eastern Cape represents a meaningful expansion of South Africa's loading throughput potential. If developed to capacity, it would significantly increase the volume of manganese that can be processed and loaded for international buyers. However, port terminal capacity and inland transport cost are separate problems that require separate solutions.

A larger port terminal increases the ceiling on how much ore South Africa can physically export. It does not reduce the cost of moving ore from the Kalahari to the coast. If the modal split remains unchanged, meaning the same proportion of ore continues arriving by truck, then the terminal amplifies volume while locking in the higher unit cost structure at greater scale.

This creates a strategic tension that market observers have increasingly noted. South Africa risks becoming a higher-volume but lower-margin manganese exporter if inland transport reform does not keep pace with port infrastructure development. In a commodity already subject to pronounced global price cycles, that margin erosion could prove particularly damaging during periods of softer manganese spot prices. Indeed, China steel demand and evolving green iron production trends add further layers of uncertainty to the global pricing environment.

South Africa's Rail Reform and the Private Train Operator Framework

The structural response to the road cost problem is South Africa's ongoing rail liberalisation process, which has opened Transnet's freight rail infrastructure to private train operating companies. According to information disclosed by Exxaro regarding its strategic positioning, 11 private Train Operating Companies have concluded rail access agreements, with the broader private-access framework spanning 41 routes across six freight corridors.

The combined freight capacity targeted across these operators encompasses 24 million tonnes spanning coal, manganese, containers, fuel, and general freight. Some operators have targeted mainline entry before the end of 2026, with the majority of operators expected to become operationally active during 2027.

However, there is an important distinction between a train slot and an operating train. A train slot is a scheduled right to run a freight service on a defined rail route. It represents allocated capacity on the network. It does not, by itself, move ore. For manganese exporters, the commercial benefit of rail reform will only materialise when those slots translate into actual train movements, when those trains reduce the volume of ore currently being trucked, and when the ports receiving the additional rail volumes are equipped and ready to handle increased throughput efficiently.

The risk for the manganese sector is that rail reform generates policy progress faster than operational progress. Agreements, designations, and capacity targets are necessary preconditions, but they are not the same as ore arriving at port by train instead of truck.

The next major ASX story will hit our subscribers first

Global Competitiveness: How South Africa's Logistics Costs Compare

South Africa's Kalahari Manganese Field gives it an almost unassailable reserve position in global manganese markets. No other country holds comparable geological endowment. However, reserve quality and export competitiveness are not the same thing. Gabon's manganese operations, centred around the Moanda mine operated by Comilog, benefit from a dedicated rail line running directly to the port of Owendo near Libreville, giving Gabonese exports a structurally more efficient transport pathway.

Australia's manganese operations, concentrated in the Northern Territory and Western Australia, similarly benefit from relatively short haul distances to purpose-built export facilities. South Africa's advantage lies in the scale and grade of its resource base. Its challenge lies in monetising that resource base efficiently given the inland geography.

A bulk commodity strategy centred on volume alone is insufficient when inland transport costs compress the mine-gate margin that producers can realise at any given spot price. This is particularly consequential for lower-grade ore parcels, where the margin cushion is thinner and transport cost absorption has a more pronounced impact on profitability.

Indicators to Watch: Measuring Whether Rail Reform Is Delivering

Given the complexity of the transition from policy to operational outcomes, the following indicator matrix provides a practical framework for assessing whether South Africa's manganese logistics are genuinely improving:

| Indicator | What to Monitor | Why It Matters |

|---|---|---|

| Tshipi Borwa Rail Share | % of annual volume shifted from road to rail | Direct measure of cost reduction at source |

| Private Operator Start Dates | Actual first-train movements vs. scheduled dates | Reveals execution gap between policy and operations |

| Rail Slot Delivery Rate | Slots allocated vs. slots actively operated | Distinguishes paper capacity from functional capacity |

| Port Offloading Readiness | Terminal throughput rates at Gqeberha and Saldanha | Determines whether rail gains translate to export flow |

| Road Trucking Exposure | Year-on-year change in road-hauled manganese volumes | Tracks whether the 46% road share is declining |

Each of these indicators measures a distinct layer of the export chain. Together, they reveal whether the full route from the Kalahari mine to the vessel is improving, or whether gains at one stage are being neutralised by bottlenecks at another.

Three Scenarios for South Africa's Manganese Logistics Through 2027

Scenario 1: Rail Reform Accelerates

Private operators enter mainline service before the end of 2026, road haulage share at Tshipi Borwa falls below 30% by late 2027, and port infrastructure keeps pace with increased rail delivery. Under this scenario, per-tonne inland transport costs decline meaningfully, mine-gate margins improve by several dollars per tonne, and South Africa strengthens its delivered price competitiveness in key Asian steel markets.

Scenario 2: Partial Rail Transition

Some private operators begin limited services during 2027, the road share declines modestly to the 35% to 40% range, but transition logistics and ramp-up delays partially offset cost savings. Exporters remain exposed to diesel price movements and truck availability constraints. The net margin improvement is real but modest.

Scenario 3: Rail Reform Stalls

Operator start dates slip beyond 2027, road haulage share remains above 45%, and any softening of manganese spot prices coincides with sustained high inland transport costs. Under this scenario, South Africa exports volume but surrenders margin, and its competitiveness relative to lower-cost logistics environments in Gabon and Australia deteriorates further.

These scenarios are speculative frameworks intended to structure analysis, not forecasts. Actual outcomes will depend on factors including operator readiness, Transnet network conditions, port capacity execution, and manganese market pricing.

Frequently Asked Questions: Road vs. Rail Costs for South Africa Manganese Exporters

What is the road cost premium for manganese transport in South Africa?

Road haulage for manganese ore costs approximately 37% more per tonne than rail transport across equivalent corridors, based on operational data disclosed by Exxaro Resources in mid-2026. The Exxaro road cost premium for South Africa manganese exporters has become one of the sector's most closely watched cost variables.

Why do logistics costs represent such a large share of manganese export costs?

The Kalahari Manganese Field sits deep in South Africa's Northern Cape, more than 800 kilometres from the nearest suitable export ports. This extended inland haul means transport costs accumulate substantially before ore reaches the FOB loading point, pushing logistics to approximately 43% of total FOB costs.

How much manganese is currently moved by road in South Africa?

At Tshipi Borwa, approximately 46% of annual export volumes, equivalent to more than 1.5 million tonnes per year, still travels to port by road rather than rail, according to Exxaro's transport data.

When will private rail operators begin running manganese freight in South Africa?

Some private Train Operating Companies are targeting mainline entry before the end of 2026, with the majority expected to become operationally active during 2027, following rail access agreements concluded with Transnet Rail Infrastructure Manager.

Does building a new port terminal solve the road cost problem?

Not directly. A larger terminal raises loading capacity but does not reduce the cost of moving ore from inland mines to the coast. Consequently, margin improvement requires both port readiness and a meaningful reduction in the proportion of ore transported by road.

The Real Battleground Is 800 Kilometres from the Port

South Africa's position in global manganese markets is built on geological foundations that no other country can replicate. The Kalahari Manganese Field's reserve scale, ore grade, and mining efficiency are genuinely world-class. But geological endowment does not automatically translate into commercial margin at the FOB point, and this is the core insight that the Exxaro road cost premium for South Africa manganese exporters forces into focus.

For exporters, investors, and market observers, the period from mid-2026 through 2027 will be telling. The rail reform framework is structurally sound on paper. Private operators have signed access agreements, capacity targets have been set, and the route network is defined. What remains unresolved is whether those agreements become operating trains, whether those trains move ore that was previously moving by truck, and whether ports can absorb the additional rail-delivered volumes without creating new bottlenecks.

Infrastructure reform must ultimately be measured in operating data, not agreements. For South Africa's manganese sector, the margin improvement that geology makes possible is waiting on the logistics system to deliver it.

This article is intended for informational purposes only and does not constitute financial or investment advice. All figures relating to cost estimates, volume projections, and scenario outcomes are based on publicly available data and illustrative modelling. Readers should conduct their own due diligence before making investment decisions.

Further coverage of South Africa's manganese export logistics and rail reform developments is available through African Mining Market at africanminingmarket.com.

Want to Stay Ahead of Major ASX Mineral Discoveries Before the Broader Market Does?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, instantly translating complex data across more than 30 commodities into clear, actionable insights for both short-term traders and long-term investors — explore the historic returns major discoveries have generated and begin your 14-day free trial at Discovery Alert to secure your market-leading edge.