June 30, 2026

Understanding the Strategic Importance of Maritime Energy Chokepoints

Global petroleum transportation networks operate through a series of critical maritime passages, each representing potential vulnerability points for worldwide energy security. These chokepoints function as essential arteries in the global oil supply system, where disruptions can cascade through international markets with remarkable speed and intensity.

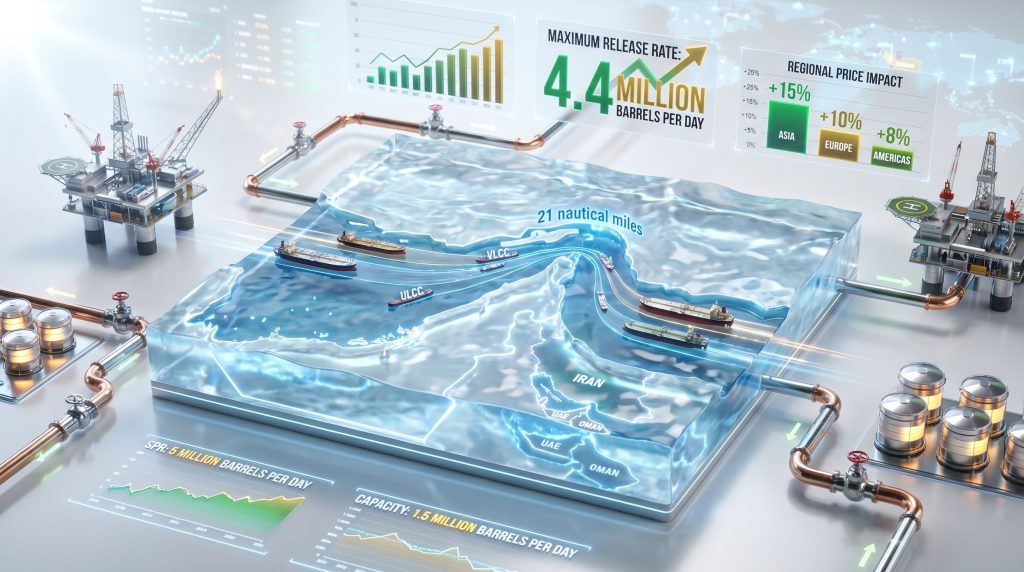

The physical geography of these passages creates inherent operational constraints that affect global energy flows. When examining the Strait of Hormuz oil disruption specifically, the narrow waterway's 21-nautical-mile width at its most constrained point forces all Very Large Crude Carriers (VLCCs) and Ultra Large Crude Carriers (ULCCs) through designated shipping corridors. This geometric limitation means that any incident affecting passage safety immediately impacts the entire flow of petroleum through the region.

Geographic and Operational Constraints

The strait's physical dimensions create a bottleneck effect that amplifies any operational disturbance. Before the April 2026 disruption, approximately 20 million barrels per day transited through this passage, representing roughly one-fifth of global crude oil production flows. The concentration of such massive volumes through a single geographic point creates systemic risk that extends far beyond regional boundaries.

Critical Infrastructure Dependencies:

• Loading terminals positioned throughout the Persian Gulf

• Offshore production platforms serving multiple national oil companies

• Pipeline networks connecting onshore fields to export facilities

• Storage tank farms providing buffer capacity during operational variations

• Navigation and communication systems ensuring safe passage coordination

When big ASX news breaks, our subscribers know first

What Are the Primary Mechanisms Behind Strait of Hormuz Supply Disruptions?

The April 2026 Strait of Hormuz oil disruption demonstrates how supply shocks propagate through interconnected operational layers, creating cumulative effects that exceed simple transit interruptions. Understanding these mechanisms requires examining both immediate physical constraints and longer-term systemic adjustments across the global petroleum system.

Cumulative Supply Loss Assessment

According to data from Kpler analytics, the Middle East conflict resulted in cumulative crude and condensate supply losses reaching 430 million barrels by April 10, 2026, with projections indicating 500 million barrels lost by the seventh week of disruption. This represents approximately $50 billion in lost revenue when calculated at the average oil price of $100 per barrel maintained since February 28, 2026.

To contextualise this magnitude, 500 million barrels equals nearly one full month of oil consumption in the United States or more than one month of total European oil demand. The scale illustrates how concentrated geographic vulnerabilities translate into global supply shortages affecting major consuming regions worldwide.

Infrastructure Vulnerability Assessment

| Infrastructure Component | Vulnerability Level | Typical Recovery Timeline | Geographic Impact Scope |

|---|---|---|---|

| Offshore Platforms | High | 6-18 months | Regional production zones |

| Pipeline Networks | Medium | 3-9 months | National export capacity |

| Storage Facilities | Medium | 2-6 months | Local buffer availability |

| Loading Terminals | High | 12-24 months | International shipping access |

The disruption cascades through multiple operational tiers, beginning with immediate shipping route closures and expanding into upstream production adjustments. Middle Eastern crude supply declined by an average of 9 million barrels per day in March 2026 compared to February baseline levels, with Saudi Arabian production representing a significant portion of this reduction.

Operational Disruption Cascades

Primary Effects (Immediate Impact):

• Complete cessation of commercial tanker traffic through the strait

• Emergency rerouting protocols activated for vessels already en route

• Immediate activation of alternative transportation systems

• Strategic reserve deployment considerations initiated

Secondary Effects (24-72 Hours):

• Tanker fleet repositioning toward alternative loading facilities

• Upstream production shutdown decisions as export logistics fail

• Refinery feedstock shortage alerts in dependent regions

• Commercial inventory acceleration to cover demand gaps

Tertiary Effects (1-4 Weeks):

• Price volatility amplification across petroleum product markets

• Strategic reserve deployment by major consuming nations

• Long-term contract renegotiation as supply reliability deteriorates

• Investment redirection toward alternative infrastructure projects

Wood Mackenzie estimates indicate approximately 11 million barrels per day of upstream production shut-ins across the Middle East region during the disruption period. The International Energy Agency characterised the March 2026 global supply decline of 10.1 million barrels per day as the largest disruption in recorded history, reducing global production from approximately 107 million barrels per day to 97 million barrels per day.

How Do Alternative Transportation Routes Mitigate Hormuz Disruptions?

Alternative pipeline systems and maritime routes provide partial mitigation for Strait of Hormuz oil disruption events, though none can fully replace the strait's massive throughput capacity. These backup systems represent critical infrastructure investments that become essential during crisis periods, despite operating at sub-optimal economic efficiency under normal conditions.

Pipeline Bypass Capacity Analysis

Saudi Arabia's East-West Pipeline System:

- Capacity: 5 million barrels per day

- Route: Eastern oil fields to Red Sea export terminals

- Strategic value: Provides Hormuz bypass for Saudi production only

- Current status: Fully operational with expansion potential under evaluation

UAE Abu Dhabi Crude Oil Pipeline:

- Capacity: 1.5 million barrels per day

- Route: Habshan production areas to Fujairah terminal on Arabian Sea

- Geographic advantage: Direct access to Indian Ocean shipping lanes

- Limitation: Serves UAE production exclusively

Iraq's Northern Export System:

- Capacity: 1.6 million barrels per day

- Route: Kirkuk oil fields through Turkey to Mediterranean port of Ceyhan

- Market access: European and Atlantic Basin destinations

- Operational challenges: Security concerns affecting throughput reliability

The combined capacity of these three primary pipeline alternatives totals 8.1 million barrels per day, covering approximately 40.5% of the strait's pre-disruption throughput. This leaves a shortfall of roughly 11.9 million barrels per day that must utilise maritime alternatives or face supply curtailment.

Maritime Route Diversification

Cape of Good Hope Alternative Route Analysis:

| Parameter | Specification | Economic Impact |

|---|---|---|

| Additional Transit Time | 15-20 days | Reduced fleet efficiency |

| Cost Increase | $1-2 per barrel | Higher delivered prices |

| Tanker Availability | Limited during peak disruption | Demurrage cost escalation |

| Insurance Coverage | Standard maritime rates | No Hormuz-specific premiums |

The Cape of Good Hope routing requires vessels to transit southbound through the Indian Ocean and around the southern tip of Africa, adding substantial time and cost to petroleum deliveries. During the April 2026 disruption, this alternative became critical for maintaining some level of Middle Eastern crude exports, despite the economic penalties involved.

What Economic Mechanisms Drive Oil Price Volatility During Hormuz Crises?

Oil market responses to Strait of Hormuz oil disruption events follow predictable patterns driven by both physical supply constraints and psychological market factors. However, the April 2026 event demonstrated how oil price movements amplify initial supply concerns through multiple feedback mechanisms operating across different time horizons.

Market Response Framework

Historical analysis indicates oil prices typically increase by 15-25% within the first week of confirmed Hormuz disruptions, with premiums persisting until alternative supply arrangements stabilise. During the 2026 event, oil futures averaged approximately $100 per barrel from February 28 onward, representing significant price elevation from pre-crisis levels.

Immediate Price Drivers:

• Physical supply shortage expectations based on transit volume loss

• Inventory drawdown acceleration as existing stocks cover demand gaps

• Speculative trading activity amplifying underlying supply concerns

• Risk premium incorporation reflecting potential escalation scenarios

Extended Market Dynamics:

• Refinery margin adjustments as feedstock costs increase

• Product price differentials reflecting regional supply dependencies

• Forward curve steepening as longer-term supply uncertainty persists

• Regional price disparities based on alternative supply access

Regional Price Impact Variations

| Region | Typical Price Premium | Supply Dependency Level | Alternative Supply Access |

|---|---|---|---|

| Asia-Pacific | 20-30% | Very High | Limited options |

| Europe | 10-15% | Moderate | Multiple source diversity |

| North America | 5-10% | Low | Domestic production base |

| Latin America | 8-12% | Variable | Regional supplier networks |

The oil price rally witnessed during this period reflected both immediate supply concerns and broader geopolitical tensions. Furthermore, the trade war impact on global markets compounded the price volatility, as international trade relationships became increasingly strained.

The International Energy Agency concluded that the Strait of Hormuz has fundamentally altered its operational status from a reliable, predictable energy route to one carrying significant geopolitical risk, representing a critical shift in global energy infrastructure planning assumptions.

How Do Strategic Petroleum Reserves Function During Supply Disruptions?

Strategic petroleum reserves serve as the primary buffer mechanism against acute supply disruptions, though their effectiveness depends heavily on coordinated deployment timing and international cooperation frameworks. The reserve system's capacity to stabilise markets during Strait of Hormuz oil disruption events reflects both storage capabilities and release coordination protocols.

Reserve Deployment Mechanisms

United States Strategic Petroleum Reserve:

- Total storage capacity: 714 million barrels

- Maximum daily release rate: 4.4 million barrels per day

- Duration at maximum rate: Approximately 162 days

- Geographic distribution: Multiple Gulf Coast storage facilities

International Energy Agency Coordination Framework:

- Member country obligations: Maintain 90-day import equivalent reserves

- Emergency response triggers: Collective action thresholds for market intervention

- Release coordination: Synchronised deployment across member nations

- Effectiveness metrics: Price stabilisation and supply gap coverage targets

Reserve Utilisation Strategies

Graduated Response Methodology:

- Initial Assessment Phase: Market disruption monitoring and threat evaluation

- Limited Release Phase: Test releases to assess market response effectiveness

- Full Deployment Phase: Maximum sustainable release rates to cover supply gaps

- Recovery Phase: Strategic planning for reserve replenishment once crisis resolves

During the April 2026 disruption, inventory data revealed accelerating drawdown patterns. Onshore inventories declined by 41 million barrels by mid-April, indicating a drawdown rate of 2.7 million barrels per day. Globally, oil inventories fell by 85 million barrels in March, with non-Middle Eastern stocks depleting by 205 million barrels at a rate of 6.6 million barrels per day.

What Are the Long-Term Infrastructure Implications of Recurring Disruptions?

Repeated Strait of Hormuz oil disruption events trigger significant infrastructure investment reallocations across the global energy system, with lasting implications for supply chain resilience and energy security planning. These disruptions accelerate strategic shifts that might otherwise develop over decades rather than years.

Investment Redirection Patterns

Pipeline Development Acceleration:

• Trans-Arabian pipeline capacity expansions beyond current 5 million barrel per day limits

• New bypass route construction connecting Middle Eastern production to alternative export terminals

• Capacity upgrade projects for existing systems like the UAE's Habshan-Fujairah pipeline

• Emergency interconnection systems enabling rapid supply rerouting during crisis periods

Storage Infrastructure Enhancement:

• Strategic reserve facility expansions in major consuming regions

• Commercial inventory increases at key distribution hubs

• Regional storage hub development reducing dependency on just-in-time supply models

• Emergency stockpile creation in vulnerable supply corridors

Technology Innovation Drivers

Enhanced Monitoring Systems:

• Satellite-based vessel traffic monitoring providing real-time chokepoint analysis

• Predictive disruption modelling using geopolitical risk assessment algorithms

• Alternative route optimisation systems minimising economic penalties during rerouting

• Real-time flow measurement across multiple transportation modes

Operational Resilience Improvements:

• Rapid deployment capabilities for emergency response equipment

• Enhanced emergency response protocols reducing reaction time during crisis events

• Backup system activation procedures ensuring continuity during primary route failures

• Recovery time minimisation through pre-positioned resources and procedures

The next major ASX story will hit our subscribers first

How Do Geopolitical Factors Influence Disruption Duration and Severity?

The duration and severity of Strait of Hormuz oil disruption events depend heavily on complex geopolitical dynamics operating across regional and international levels. These factors often determine whether disruptions last days, weeks, or extend into months with corresponding market impacts.

Stakeholder Interest Analysis

Regional Power Dynamics:

• Territorial control assertions affecting transit rights and operational safety

• Economic leverage utilisation where energy exports serve broader political objectives

• Security alliance obligations creating external intervention pressures

• Domestic political considerations influencing escalation and de-escalation decisions

International Response Coordination:

• Diplomatic intervention efforts seeking negotiated settlement frameworks

• Military escort operations providing security for commercial vessel transit

• Economic sanction considerations balancing pressure with supply continuity

• Multilateral negotiation frameworks addressing underlying conflict drivers

In addition, the OPEC production impact during such crises often becomes a significant factor in determining global supply stability. Meanwhile, the US oil production decline in recent years has reduced America's ability to compensate for Middle Eastern supply shortfalls.

Escalation and De-escalation Patterns

Typical Escalation Sequence:

- Initial Incident: Trigger event or formal threat declaration affecting transit confidence

- Insurance Response: Maritime insurance rate increases reflecting elevated risk assessment

- Voluntary Reduction: Commercial operators reducing transit frequency due to risk concerns

- Formal Restrictions: Official closure announcements or active interference with vessel traffic

- International Intervention: External powers engaging through diplomatic or military channels

De-escalation Mechanisms:

• Third-party mediation initiatives providing face-saving compromise pathways

• Economic incentive packages addressing underlying grievances driving conflict

• Security guarantee arrangements ensuring safe passage for commercial traffic

• Negotiated settlement frameworks addressing broader regional tensions

What Lessons Can Be Learned from Historical Hormuz Disruptions?

Historical analysis of Strait of Hormuz oil disruption events provides valuable insights into market behaviour patterns, policy response effectiveness, and infrastructure adaptation strategies. These lessons inform current preparedness planning and future resilience investments.

Comparative Analysis of Past Events

1980-1988 Tanker War Period:

- Duration: Eight years of intermittent disruptions

- Peak impact: 2.5 million barrels per day supply loss

- Resolution mechanism: United Nations-mediated ceasefire agreement

- Long-term consequence: Enhanced international naval protection protocols

2019 Tanker Attack Incidents:

- Duration: Six months of elevated tension and uncertainty

- Supply impact: Minimal direct physical supply loss

- Price effect: 10-15% oil price premium during peak concern periods

- Resolution approach: International maritime patrol coordination and diplomatic engagement

Operational Lessons Learned

Effective Response Strategies:

• Rapid alternative route activation minimising supply gap duration

• Coordinated strategic reserve releases preventing panic buying and hoarding

• Enhanced maritime security cooperation protecting commercial vessel transit

• Diplomatic engagement prioritisation addressing root causes rather than symptoms only

System Vulnerabilities Identified:

• Insurance market fragility amplifying risk perceptions beyond physical threat levels

• Tanker fleet concentration creating bottlenecks during rapid rerouting requirements

• Communication system dependencies affecting coordination during crisis periods

• Emergency response coordination gaps between national and international authorities

The April 2026 disruption revealed additional operational complexities. According to Wood Mackenzie analysis, Iraqi production restoration would require between 6 and 9 months even after Hormuz reopening, reflecting reservoir management complexities and resource constraint challenges that extend recovery periods beyond simple route restoration.

Future Outlook: Building Resilience Against Hormuz Disruptions

Building long-term resilience against Strait of Hormuz oil disruption events requires coordinated investment in infrastructure diversification, technology enhancement, and international cooperation frameworks. The lessons from the April 2026 event highlight both immediate vulnerabilities and systemic adaptation opportunities.

Infrastructure Development Priorities

Short-term Enhancements (1-3 years):

• Pipeline capacity expansions for existing bypass systems

• Storage facility upgrades increasing buffer capacity at key distribution points

• Emergency response system improvements reducing reaction time during disruptions

• Alternative route optimisation reducing economic penalties for backup transportation

Medium-term Transformations (3-7 years):

• New bypass pipeline construction connecting Middle Eastern production to diverse export terminals

• Regional distribution hub development reducing dependency on single-route systems

• Advanced technology integration providing real-time supply chain visibility

• Enhanced international cooperation frameworks improving crisis response coordination

Long-term Strategic Shifts (7+ years):

• Accelerated energy transition reducing absolute dependency on petroleum imports

• Supply chain diversification spreading risk across multiple geographic sources

• Renewable energy infrastructure development providing alternative energy security

• Reduced chokepoint dependency through distributed energy system architecture

Risk Mitigation Strategies

Operational Resilience Building:

• Multiple route redundancy ensuring alternative pathways during primary route disruption

• Flexible supply arrangements enabling rapid source substitution during crisis periods

• Enhanced storage capabilities providing extended buffer periods during supply interruptions

• Rapid response protocols minimising disruption impact duration and severity

Market Stability Mechanisms:

• Coordinated reserve policies preventing competitive depletion during crisis periods

• Price volatility dampening through strategic market intervention capabilities

• Information sharing systems improving market transparency during uncertainty periods

• Emergency cooperation agreements ensuring collective response to supply disruptions

The International Energy Agency's assessment that resuming flows through the Strait of Hormuz remains the single most important variable in easing pressure on energy supplies, prices, and the global economy underscores the continued strategic importance of this waterway. However, the April 2026 disruption demonstrated that even temporary reopening windows may prove insufficient to restore market stability without sustained, unconditional access.

Qatar's assessment that damage to the Ras Laffan LNG facility would require up to five years for full recovery, with $20 billion in annual lost revenue, illustrates how infrastructure damage extends disruption impacts far beyond initial incident periods. This reinforces the importance of protective measures and backup capacity development for critical energy infrastructure.

Furthermore, experts suggest that finding alternative routes for Middle East oil becomes crucial for maintaining global energy security during such disruptions.

Investment decisions and risk assessments based on geopolitical events carry inherent uncertainties. Market participants should consider multiple scenarios and consult professional advisors when making energy security or investment decisions related to chokepoint disruptions.

Ready to Invest in the Next Major Mineral Discovery?

Discovery Alert instantly alerts investors to significant ASX mineral discoveries using its proprietary Discovery IQ model, turning complex mineral data into actionable insights. Understand why historic discoveries can generate substantial returns by visiting Discovery Alert's dedicated discoveries page, showcasing examples of exceptional outcomes, and begin your 14-day free trial today to position yourself ahead of the market.