July 31, 2026

Market Concentration Drives Industry Consolidation

The electric vehicle battery manufacturing landscape reflects sophisticated industrial economics where production scale determines market survival. Manufacturing facilities require billions in capital investment, specialised supply chain relationships, and years of operational refinement before achieving competitive cost structures. This capital intensity creates natural barriers that favour established players with deep financial resources and operational expertise.

Within this framework, market concentration patterns reveal the fundamental characteristics of modern battery manufacturing. Companies achieving significant scale benefits can reduce per-unit costs through automated production lines, bulk raw material procurement, and integrated quality control systems. These advantages compound over time, creating sustainable competitive moats that smaller manufacturers struggle to overcome.

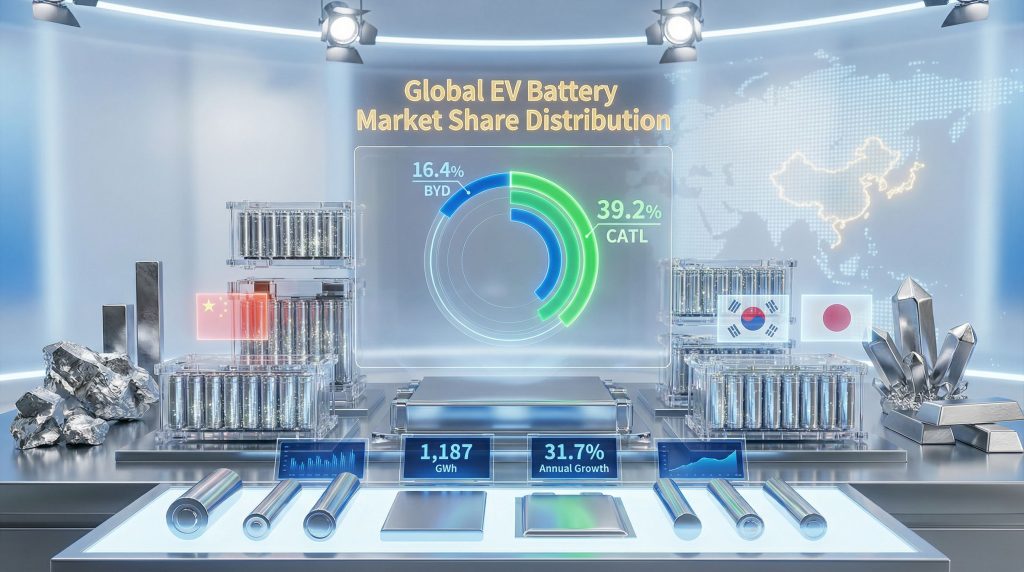

The global EV battery market share distribution demonstrates extreme concentration among leading manufacturers. According to SNE Research data compiled by CnEVPost, the top two producers control 55.6% of total installations, representing 659.5 GWh of the 1,187 GWh global market in 2025. This duopoly effect creates significant supply chain dependencies for automotive manufacturers worldwide.

The market hierarchy reveals distinct competitive tiers with limited overlap between performance levels:

| Concentration Level | Market Share | Combined GWh | Strategic Position |

|---|---|---|---|

| Top 2 Players | 55.6% | 659.5 | Supply gatekeepers |

| Top 3 Players | 64.8% | 768.3 | Oligopoly formation |

| Top 10 Players | 89.5% | 1,062.1 | Entry barrier threshold |

Source: SNE Research data via CnEVPost, February 2026

Market growth of 31.7% year-over-year expansion from 901.4 GWh to 1,187 GWh indicates robust demand fundamentals supporting industry expansion. However, this growth primarily benefits established players rather than enabling new entrant success, as evidenced by the consistent market share concentration among the top manufacturers.

The remaining 10.5% market share distributed among smaller manufacturers highlights the challenges facing emerging battery companies. These players compete for limited market segments while contending with established relationships between major manufacturers and automotive original equipment manufacturers (OEMs).

When big ASX news breaks, our subscribers know first

CATL Maintains Manufacturing Scale Leadership

Contemporary Amperex Technology Co. Limited (CATL) achieved 39.2% market share with 464.7 GWh of installations in 2025, representing 35.7% growth from the previous year's 342.5 GWh. This performance exceeded the overall market growth rate of 31.7%, indicating continued market share capture from competitors.

CATL's market share progression demonstrates sustained leadership expansion:

- 2024 full year: 38.0% market share

- January-November 2025: 38.2% market share

- 2025 full year: 39.2% market share

The company remains the only manufacturer globally exceeding 30% market share, suggesting achievement of a production scale threshold that competitors have not replicated. This scale advantage likely derives from earlier infrastructure investments and supply chain integration across the battery manufacturing value chain.

Within China's domestic market, CATL's dominance appears even more pronounced with 43.42% market share and 333.57 GWh of installations powering 5.07 million vehicles according to domestic market data from CnEVPost. This domestic strength provides a stable revenue base supporting international expansion initiatives.

CATL's ability to grow faster than the overall market while maintaining pricing competitiveness indicates operational excellence in manufacturing efficiency and cost management. The company's technology portfolio spans multiple battery chemistries, enabling customised solutions for different automotive applications and regional preferences.

BYD's Vertical Integration Creates Unique Market Position

Build Your Dreams (BYD) secured 16.4% global market share with 194.8 GWh of installations in 2025, representing 27.7% growth from 152.6 GWh the previous year. Despite this substantial growth, BYD's market share declined slightly from 16.9% in 2024 and 16.7% for January-November 2025.

BYD's vertical integration model fundamentally differs from dedicated battery manufacturers like CATL. The company produces batteries primarily to support internal vehicle manufacturing operations, creating several strategic advantages:

- Supply chain control: Direct alignment between battery specifications and vehicle platform requirements

- Cost optimisation: Elimination of external supplier margins and negotiation complexities

- Technology integration: Coordinated development between battery and vehicle systems

- Market timing flexibility: Internal demand buffering against external market fluctuations

The 194.8 GWh production volume corresponds closely to BYD's vehicle manufacturing needs, with 27.7% growth reflecting the company's expanding automotive sales. This internal consumption model reduces dependency on external customer relationships while maintaining technological advancement aligned with vehicle platform evolution.

"BYD's approach represents a strategic alternative to pure-play battery manufacturing, prioritising integrated value chain control over external market maximisation."

Within China's domestic market, BYD achieved 21.58% market share, combining with CATL's 43.42% for 64.0% of the domestic battery market. This concentration demonstrates the competitive challenges facing international manufacturers seeking market entry in China's EV ecosystem.

Regional Supply Chain Patterns Shape Global Competition

Asian manufacturers dominate global EV battery market share with Chinese companies controlling approximately 70.4% of worldwide installations based on SNE Research data. This concentration reflects decades of policy support, manufacturing infrastructure development, and raw material processing integration.

Chinese Manufacturing Concentration

Chinese battery manufacturers achieved the following market positions in 2025:

- CATL: 39.2% (464.7 GWh)

- BYD: 16.4% (194.8 GWh)

- CALB: 5.3% (62.8 GWh)

- Gotion High-tech: 4.5% (53.5 GWh)

- Eve Energy: 2.6% (31.3 GWh)

- Svolt: 2.4% (28.5 GWh)

Combined Chinese total: 70.4% of global installations

This dominance stems from integrated supply chains encompassing lithium processing, cathode material production, cell manufacturing, and module assembly within China's industrial ecosystem. Furthermore, lower labour costs and supportive government policies reinforce manufacturing competitiveness. The success of Chinese manufacturers has driven significant lithium industry innovations and lithium refinery innovations globally.

South Korean Technology Focus

South Korean manufacturers maintain 15.3% combined market share through technology differentiation and established OEM relationships:

- LG Energy Solution: 9.2% (108.8 GWh)

- SK On: 3.7% (44.5 GWh)

- Samsung SDI: 2.4% (28.9 GWh)

These companies focus on premium battery chemistries, energy density optimisation, and international automotive partnerships. Their positioning reflects deliberate strategy emphasising technology leadership over cost competition, targeting higher-margin applications.

Japanese Strategic Partnerships

Panasonic maintained 3.7% market share with 44.2 GWh of installations, primarily through its strategic partnership with Tesla. This focused approach demonstrates viability of niche positioning within specific customer relationships rather than broad market diversification.

The Japanese approach emphasises partnership depth over market breadth, concentrating on technological excellence within selected applications. This strategy contrasts with Chinese manufacturers' scale-focused expansion and South Korean companies' technology differentiation.

Mid-Tier Manufacturers Navigate Consolidation Pressures

Companies ranking between fourth and tenth positions face intensifying competitive pressures as market consolidation accelerates. These manufacturers must identify sustainable differentiation strategies to avoid being compressed between leading players' scale advantages and smaller companies' specialisation focus.

CALB achieved 5.3% market share through cost-competitive lithium iron phosphate (LFP) battery solutions, positioning between premium offerings and commodity pricing. The company's 62.8 GWh installation volume provides sufficient scale for operational efficiency while maintaining manufacturing flexibility.

Gotion High-tech secured 4.5% market share via international expansion partnerships and strategic customer relationships. The company's 53.5 GWh production volume supports sustainable operations while pursuing geographic diversification to reduce market concentration risk.

Eve Energy captured 2.6% market share focusing on premium applications and energy storage system markets. This specialisation approach enables differentiated positioning despite lower production volumes compared to mass-market competitors.

These mid-tier manufacturers employ several common strategies:

- Technology specialisation: Development of advanced battery chemistries or manufacturing processes

- Regional partnerships: Joint ventures with local automotive manufacturers or government entities

- Application diversification: Expansion into energy storage systems and specialty battery markets

- Supply chain optimisation: Vertical integration in specific value chain segments

Market Growth Fundamentals Support Continued Expansion

The 31.7% annual growth from 901.4 GWh to 1,187 GWh reflects multiple demand-side and supply-side catalysts driving industry expansion. Understanding these growth drivers provides insight into long-term market trajectory and competitive positioning sustainability.

Demand Acceleration Factors

Global electric vehicle adoption continues accelerating through policy mandates, consumer acceptance, and infrastructure development. Key demand drivers include:

- Government incentives: Purchase subsidies and tax credits reducing EV cost disadvantages

- ICE phase-out timelines: Regulatory mandates requiring automaker electrification transitions

- Charging infrastructure expansion: Reducing range anxiety through increased charging availability

- Battery cost reductions: Declining per-kWh costs improving EV price competitiveness

- Model variety expansion: Increased EV options across vehicle segments and price points

Consequently, the EV impact on mining operations continues to grow as demand for raw materials increases significantly.

Supply Chain Scaling

Manufacturing capacity expansion supports demand growth through new facility construction and production line automation. Supply-side enablers include:

- Gigafactory construction: New manufacturing facilities adding production capacity globally

- Raw material availability: Lithium, nickel, and cobalt mining expansion supporting battery production

- Technology improvements: Manufacturing process innovations reducing production costs and time

- Quality assurance systems: Standardised testing and safety protocols enabling scale production

- Recycling infrastructure: Battery material recovery systems reducing raw material dependence

The recent battery recycling breakthrough demonstrates significant progress in creating sustainable supply chains for battery materials.

The next major ASX story will hit our subscribers first

Investment Implications of Market Concentration

The global EV battery market share concentration creates distinct investment opportunities and risks across different market participant categories. Understanding these dynamics enables strategic positioning within the evolving battery manufacturing ecosystem.

Scale Advantage Amplification

Leading manufacturers benefit from compounding advantages as market size expands:

- Manufacturing cost reductions: Higher production volumes enabling automated production line investments

- Raw material procurement power: Large-scale purchasing agreements securing favourable pricing

- Technology development resources: Greater R&D budgets supporting innovation and patent development

- Supply chain integration: Vertical integration opportunities reducing external dependencies

These advantages create self-reinforcing competitive moats that become increasingly difficult for smaller players to overcome as market matures.

Acquisition Target Identification

Mid-tier manufacturers facing consolidation pressure may become attractive acquisition targets for:

- Technology capabilities: Specialised battery chemistries or manufacturing processes

- Geographic presence: Established manufacturing facilities in strategic locations

- Customer relationships: Existing automotive OEM supply agreements

- Talent acquisition: Experienced engineering and manufacturing teams

Companies with 2-5% market share likely face the greatest consolidation pressure, potentially creating acquisition opportunities for both leading manufacturers and private equity investors.

Supply Chain Security Premiums

Geographically diversified manufacturers command valuation premiums due to supply chain security considerations:

- Political risk mitigation: Production facilities across multiple countries reducing single-country dependencies

- Logistics optimisation: Regional manufacturing reducing transportation costs and delivery times

- Regulatory compliance: Local production meeting domestic content requirements

- Market access: Established operations enabling entry into protected markets

Technology Transitions Reshape Competitive Dynamics

Next-generation battery technologies create opportunities for competitive repositioning as existing manufacturing advantages may not transfer directly to new production processes. Companies investing early in emerging technologies could potentially disrupt established market hierarchies.

Solid-State Battery Development

Multiple manufacturers pursue solid-state battery commercialisation with potential advantages including:

- Energy density improvements: Higher kWh per kg enabling longer vehicle range

- Safety enhancements: Reduced fire risk through solid electrolyte chemistry

- Fast charging capabilities: Improved charge acceptance reducing charging time

- Temperature stability: Better performance across wider temperature ranges

However, solid-state manufacturing requires different production equipment and processes, potentially reducing existing manufacturers' capital asset advantages. This technology transition could enable new entrant success if commercialisation proves viable. Moreover, direct lithium extraction technologies are becoming increasingly important for securing raw material supplies for these advanced batteries.

Manufacturing Process Innovation

Production efficiency improvements create competitive advantages through cost reduction and quality enhancement:

- Dry electrode technology: Reduced solvent usage and drying energy requirements

- Cell-to-pack architecture: Simplified assembly reducing manufacturing complexity

- Automated quality control: AI-powered testing systems improving defect detection

- Recycling integration: Closed-loop material recovery reducing raw material costs

Companies successfully implementing these innovations gain sustainable cost advantages that accumulate over time through operational excellence. Additionally, according to recent research from Carbon Credits, Chinese manufacturers are increasingly focusing on process innovations to maintain their competitive edge.

What Are the Future Market Evolution Forecasts Through 2030?

Global EV battery market share concentration will likely intensify as scale advantages compound and capital requirements for competitive manufacturing continue increasing. Several scenarios could reshape competitive positioning over the next five years.

Consolidation Acceleration Scenario

Market concentration could increase further if:

- Top 3 manufacturers capture 75%+ market share through organic growth and acquisitions

- Mid-tier players face increasing pressure from cost competition and customer consolidation

- New entrants find market entry increasingly difficult due to capital requirements and established relationships

This scenario benefits leading manufacturers through pricing power and operational leverage while creating challenges for automotive OEMs seeking supply chain diversification. Industry analysis suggests that CATL continues to dominate with sustained market expansion.

Technology Disruption Scenario

Competitive dynamics could shift if:

- Solid-state batteries achieve commercial viability earlier than expected

- Alternative chemistries prove superior for specific applications

- New manufacturing processes significantly reduce production costs

Technology disruption could enable new entrant success and reduce existing manufacturers' advantages, creating investment opportunities in innovative companies while threatening established players.

Geographic Rebalancing Scenario

Regional production patterns could change through:

- Trade policy impacts: Tariffs and local content requirements forcing regional manufacturing

- Raw material access: Supply chain security concerns driving domestic production

- Government incentives: Strategic subsidies supporting national battery manufacturing capabilities

Geographic rebalancing would benefit companies with international expansion capabilities while challenging manufacturers dependent on single-region production and export strategies. Consequently, the current concentration of manufacturing in Asia may face significant shifts as geopolitical considerations become more prominent.

Disclaimer: This analysis involves forecasts and speculation about future market developments. Investment decisions should consider multiple factors and professional financial advice. Market conditions and competitive dynamics may change significantly from current projections.

Ready to Capitalise on the Next Battery Materials Discovery?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, instantly empowering subscribers to identify actionable opportunities in lithium, nickel, and other critical battery materials ahead of the broader market. Understand why major mineral discoveries can lead to substantial market returns by exploring Discovery Alert's dedicated discoveries page, showcasing historic examples of exceptional outcomes, and begin your 14-day free trial today to position yourself ahead of the market.