June 17, 2026

Market Forces Reshaping Global Copper Strategy

The mining industry stands at a critical inflection point where technological advancement intersects with resource scarcity. As traditional commodity markets face unprecedented demand from emerging technologies, major mining corporations are repositioning their portfolios to capture value from the structural shift toward electrification and artificial intelligence infrastructure.

This strategic realignment has triggered consolidation discussions that could fundamentally alter global supply dynamics across critical minerals, particularly copper, which has emerged as the cornerstone metal for the modern economy's digital and energy transformation.

When big ASX news breaks, our subscribers know first

Strategic Drivers Behind Mining Sector Consolidation

Portfolio Diversification Imperatives

Mining giants face mounting pressure to reduce dependence on single commodity exposures that have historically defined their operations. Companies heavily weighted toward iron ore production confront particular challenges as China's property sector experiences structural headwinds, creating vulnerability that diversified mineral portfolios could mitigate.

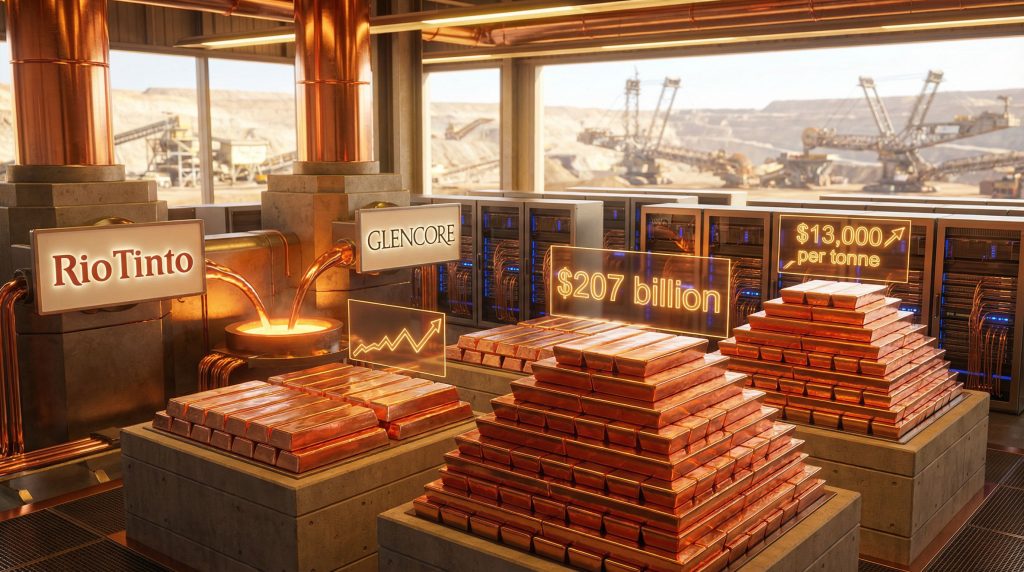

The Rio Tinto Glencore copper acquisition discussions exemplify this strategic imperative. Rio Tinto's market capitalisation of $142 billion positions it as the world's largest iron ore producer, whilst Glencore's $65 billion valuation reflects its diversified metals exposure across copper, coal, and other commodities.

Market Response Indicators:

- Glencore shares surged approximately 6% following confirmation of discussions

- Rio Tinto shares declined up to 6.4%, representing the largest intraday drop since July 2022

- Combined entity valuation would reach approximately $207 billion

- BHP Group shares increased 0.6% as markets recalibrated competitive positioning

Regulatory Timeline Pressures

Under UK takeover regulations, specifically the City Code on Takeovers and Mergers, Rio Tinto faces a February 5, 2026 deadline to present a formal offer or withdraw from discussions. This regulatory framework creates defined decision-making windows that accelerate strategic evaluation processes.

Industry analysts have noted concerns about premium payments potentially destroying shareholder value. Allan Gray fund analyst Tim Hillier indicated that excessive valuations could diminish returns for Rio Tinto shareholders, highlighting the delicate balance between strategic positioning and financial prudence.

Reuters reported that the potential merger could create the world's biggest mining company, further emphasising the significant implications of these discussions.

Copper's Strategic Importance in the Global Economy

Energy Infrastructure Demand Fundamentals

Copper's conductivity properties make it irreplaceable across multiple electrification applications simultaneously. The metal's criticality extends throughout renewable energy deployment, electric vehicle manufacturing, data center expansion, and battery storage facility construction.

Recent price performance reflects these demand fundamentals, with copper exceeding $13,000 per tonne and trading above $6 per pound as supply constraints intersect with accelerating consumption from energy transition technologies. Moreover, copper investment insights reveal growing interest from institutional investors seeking exposure to critical minerals.

Technical Applications by Sector:

Wind Energy Systems:

- Turbine generator windings for electrical generation

- Transmission components for power distribution

- Structural elements in tower systems

Solar Infrastructure:

- Panel array electrical connections and wiring

- Inverter components for AC/DC conversion

- Grid interconnection systems

Electric Vehicle Manufacturing:

- Motor windings and electrical components

- High-voltage battery interconnect systems

- Charging infrastructure wiring and transformers

AI and Data Center Infrastructure Requirements

Artificial intelligence's computational demands have created unprecedented copper consumption patterns. Modern data centers require elevated copper concentrations compared to traditional IT infrastructure due to higher power density requirements and enhanced cooling system sophistication.

Data Center Copper Applications:

- High-capacity electrical distribution with redundancy

- Liquid cooling system piping and heat exchangers

- Backup power installation components

- Network connectivity hardware

Between 730,000 and 830,000 tonnes of copper material was economically trapped in the United States in October 2025 due to concerns regarding potential tariffs. This inventory accumulation increased Chicago Mercantile Exchange copper holdings whilst global inventories declined, creating premium pressure across markets.

Market Concentration and Competitive Dynamics

Supply Chain Consolidation Impact

A combined Rio Tinto-Glencore entity would surpass BHP Group's $161 billion market capitalisation, creating the world's largest mining company by market value. This concentration could influence global copper supply through coordinated production scheduling, technology transfer opportunities, and integrated logistics networks.

Furthermore, the mining consolidation trends demonstrate how major players are seeking to enhance operational efficiency through strategic combinations.

Operational Integration Benefits:

- Shared technical expertise across multiple regions

- Combined capital resources for simultaneous project development

- Unified supply chain management

- Streamlined permitting processes through coordinated regulatory engagement

Competitive Response Scenarios

Industry participants anticipate potential counter-moves from other major miners, particularly following the $53 billion Anglo American-Teck Resources merger approved in Canada. This consolidation trend reflects industry-wide positioning around copper supply security as companies balance growth ambitions with operational efficiency.

The London Stock Exchange Group identified the potential Rio Tinto-Glencore transaction as possibly the largest mining agreement in history, surpassing previous major consolidation events across the sector.

Operational Integration Challenges

Coal Asset Resolution Strategies

Rio Tinto divested all coal operations in 2018, creating strategic misalignment with Glencore's significant coal portfolio, which was expanded through the 2023 acquisition of Teck Resources' coal business. This integration challenge requires sophisticated resolution approaches.

Mining.com reported that Rio Tinto may be prepared to accept coal assets as part of the deal, representing a significant strategic shift.

Potential Resolution Mechanisms:

-

Immediate Divestiture:

- Rapid sale to specialised coal operators post-closing

- Eliminates ESG exposure immediately

- Requires market timing optimisation

-

Gradual Phase-Out:

- Predetermined multi-year wind-down timeline

- Maintains operational continuity

- Extended ESG liability period

-

Spin-Off Structure:

- Independent publicly traded entity separation

- Complete operational and financial isolation

- Regulatory complexity requirements

-

Joint Venture Partnership:

- Collaboration with coal-focused operators

- Shared operational responsibility

- Governance coordination challenges

Geographic Portfolio Optimisation

The integrated entity would operate across multiple jurisdictions requiring coordinated management approaches for environmental compliance, labour relations standardisation, tax optimisation strategies, and political risk mitigation across Australian, Chilean, Argentine, and African regulatory frameworks.

Contemporary ESG considerations reflect observable reduction in regulatory green pressure, particularly following political leadership changes. However, certain institutional fund managers maintain explicit restrictions prohibiting investment in companies with thermal coal exposure, creating potential valuation constraints.

Project Development and Production Capacity

Glencore's Argentina Copper Portfolio

Glencore presented ambitious plans to nearly double copper production within the next decade, with specific projects representing major capacity additions through its Argentina operations. The development of the Argentina copper system presents significant opportunities for expanded production.

Key Project Metrics:

MARA/Agua Rica (Alumbrera) Project:

- Production restart planned for first half of 2028

- Operational suspension duration: approximately 10 years

- Projected copper output: 75,000 tonnes over four years

- Additional production: 317,000 ounces gold, 1,000 tonnes molybdenum

RIGI Investment Commitments:

- Combined submission value: $13 billion

- Agua Rica development capital: $4 billion

- El Pachón Phase 1 capital: $9.5 billion over next decade

- El Pachón resource base: greater than 7 billion tonnes of material

Resource Development Acceleration

Merging Rio Tinto's development pipeline expertise with Glencore's existing operational assets could accelerate project timelines through consolidated technical resources, enhanced capital deployment, and coordinated regulatory engagement processes.

The integrated approach would enable simultaneous project development across multiple jurisdictions, potentially reducing the traditional timeline constraints that have historically limited major mining project advancement.

The next major ASX story will hit our subscribers first

Financial Market Implications

Valuation Metrics and Investor Sentiment

The divergent market reactions revealed investor uncertainty regarding premium payment levels and strategic value creation. Glencore shareholders demonstrated enthusiasm for potential value realisation, whilst Rio Tinto investors expressed concerns about acquisition pricing relative to organic growth alternatives.

Market Positioning Context:

- Rio Tinto maintains significant development pipeline with growth potential

- Question of acquisition necessity versus organic expansion efficiency

- Leadership changes: Simon Trott replaced Jakob Stausholm as CEO

- Dominic Barton serves as chairman, potentially facilitating negotiations

Historical Precedent and Relationship Dynamics

The 2014 attempted merger between these companies was rejected by Rio Tinto, resulting in public conflict that exposed fundamental strategic and cultural differences. Subsequent leadership changes and market evolution have created conditions for renewed discussions.

Both Rio Tinto CEO Gary Nagle and Glencore leadership were received by Argentine President Javier Milei in August 2024 to discuss mining investments, suggesting renewed diplomatic channels and strategic alignment opportunities.

Regional Asset Portfolio Analysis

Rio Tinto's Argentina Operations

Rio Tinto operates as Argentina's principal lithium producer following its $6.7 billion acquisition of Arcadium Lithium in March 2025. The company currently manages two of Argentina's six active lithium projects.

Production Facilities:

Fénix Project (Catamarca):

- Current capacity: 32,000 tonnes

- Phase 1B expansion: additional 10,000 tonnes

- RIGI approval: $251 million

Salar de Olaroz (Jujuy):

- Joint venture with Toyota Tsusho Corporation

- Annual production: 42,500 tonnes

- Shared operational structure

Development Pipeline:

- Cauchari project: 25,000 tonnes LCE potential

- Sal de Vida: 15,000 tonnes annual carbonato de litio

- Rincón (Salta): 60,000 tonnes capacity with $2.7 billion RIGI

- Güemes plant: cloruro de litio processing facility

Glencore's Copper Development Strategy

Glencore represents a historical copper operator in Argentina with substantial undeveloped resources requiring capital deployment and regulatory advancement.

Primary Assets:

El Pachón (San Juan):

- Resource estimate: over 7 billion tonnes

- Development status: feasibility stage

- Strategic significance: major undeveloped copper deposit

MARA Project (Catamarca):

- Copper, gold, and molybdenum asset

- Alumbrera infrastructure integration

- Potential for major cupriferous development

After nearly a decade of operational silence, Glencore confirmed Alumbrera's production restart for 2028, representing a significant reactivation of Argentina's copper production capacity.

Industry Transformation and Future Outlook

Supply Security and Market Structure

The potential transaction represents more than corporate consolidation. It signals fundamental mining industry adaptation to demand shifts driven by technological transformation and environmental imperatives across global markets.

Market concentration among major copper suppliers could theoretically influence price discovery mechanisms through reduced competition, enhanced customer bargaining power, coordinated production decisions, and strategic inventory management capabilities. Additionally, the US copper production overview highlights the importance of securing domestic supply chains.

Investment and Development Implications

Whether completed or abandoned, these discussions highlight copper's strategic importance and industry evolution toward securing critical mineral supplies for global energy transition requirements. The global copper supply forecast suggests that major consolidation may be necessary to meet future demand.

Strategic Considerations:

- Enhanced supply chain resilience through geographic diversification

- Operational redundancy across production regions

- Technology development focus areas

- Capital allocation priority optimisation

The outcome will likely influence mining sector strategies across multiple timeframes, as companies balance expansion objectives with operational efficiency and environmental responsibility in an increasingly complex global marketplace. Consequently, the Rio Tinto Glencore copper acquisition discussions represent a watershed moment for the global mining industry.

Disclaimer: This analysis contains forward-looking statements and speculative assessments regarding potential corporate transactions, market conditions, and industry developments. Actual outcomes may differ materially from projections discussed. Investment decisions should be based on comprehensive due diligence and professional financial advice. Commodity prices and mining operations involve significant risks including geological, regulatory, environmental, and market uncertainties.

Are You Positioning Yourself for the Next Major Copper Discovery?

The potential Rio Tinto-Glencore merger highlights copper's critical role in the modern economy, but savvy investors know that some of the most significant returns come from emerging discoveries rather than established giants. Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, instantly empowering subscribers to identify actionable copper and critical mineral opportunities ahead of the broader market. Begin your 30-day free trial today and secure your market-leading advantage in this rapidly evolving landscape.