May 15, 2026

The Anatomy of a Billion-Dollar Copper Bet: How Project Finance Is Shaping the Next Generation of Critical Mineral Development

When institutional capital flows toward a single undeveloped copper deposit at the scale of several billion dollars, it rarely happens by accident. It happens because a confluence of geological quality, feasibility economics, regulatory architecture, and strategic alignment creates conditions that lenders cannot afford to ignore. Understanding how these forces converge at the McEwen Copper Los Azules project financing reveals as much about the broader mechanics of critical minerals development as it does about any single company's ambitions.

The copper industry is navigating one of its most structurally complex periods in decades. Critical minerals demand is accelerating from multiple directions simultaneously: electrical grid modernisation, utility-scale renewable energy installations, electric vehicle manufacturing, and data centre infrastructure all require copper at volumes that existing production cannot comfortably sustain. Yet the pipeline of large, advanced-stage, development-ready copper projects globally remains remarkably thin. Bringing a major greenfield copper asset into production in this environment is not merely a financial transaction. It is, in industry terms, an exercise in assembling bankability from the ground up.

When big ASX news breaks, our subscribers know first

Why Los Azules Commands Attention at the Global Scale

Located at high altitude in Argentina's San Juan province within the Andean cordillera, the Los Azules deposit has long been recognised as one of the world's most substantial undeveloped copper resources. What elevated the project from a promising geological asset into a credible financing candidate was the completion of a definitive feasibility study in October 2025, which provided the numerical foundation that institutional lenders require before engaging seriously with a transaction of this complexity.

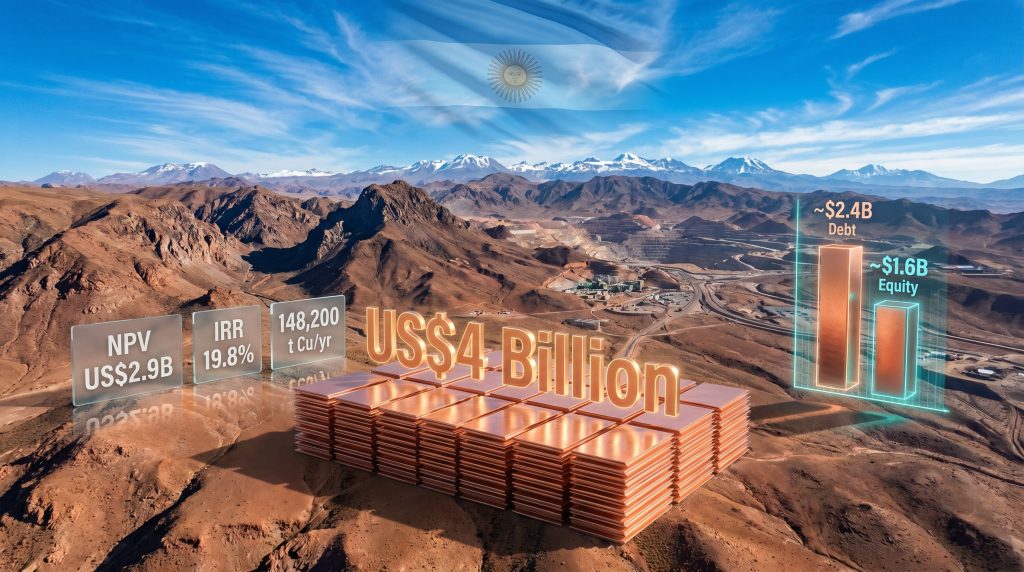

The key metrics from that study establish the investment case clearly:

| Economic Metric | Value |

|---|---|

| Estimated capital development cost | US$3.15 billion |

| After-tax NPV at 8% discount rate | US$2.9 billion |

| Internal rate of return (post-tax) | 19.8% |

| Average annual copper cathode production | ~148,200 tonnes |

A post-tax IRR approaching 20% on a project requiring more than three billion dollars in capital is a notably competitive return in the current environment. For context, greenfield mining projects at this scale typically face significant pressure to demonstrate returns well above the weighted average cost of capital to attract institutional debt, given the execution risks inherent in large-scale construction in remote, high-altitude environments. Los Azules clears that threshold with meaningful headroom.

Industry Insight: In project finance, the feasibility study is not merely a technical document. It functions as the primary risk-assessment instrument for lenders. A study that produces an after-tax IRR substantially above the cost of debt signals that even under moderate copper price stress scenarios, the project can service its obligations while generating residual equity returns.

Understanding the US$4 Billion Capital Architecture

The McEwen Copper Los Azules project financing is structured around a total capital target of approximately US$4 billion, with a deliberate 60/40 split between debt and equity contributions. This translates to a senior debt package of roughly US$2.4 billion and an equity component of approximately US$1.6 billion.

| Capital Component | Target Amount | Proportion |

|---|---|---|

| Senior debt (all sources) | ~US$2.4 billion | ~60% |

| Equity contributions | ~US$1.6 billion | ~40% |

| Total project financing | ~US$4.0 billion | 100% |

This structure follows the classic project finance model, where debt is secured against the project's own cash flows rather than against the balance sheet of the sponsoring entity. This distinction matters considerably for both the sponsor and the lender. For the sponsor, it limits recourse and preserves balance sheet capacity. For the lender, it concentrates risk assessment on the specific project's operating profile, reserve quality, commodity price assumptions, and jurisdiction.

A 60% debt loading is achievable at Los Azules because the feasibility economics provide sufficient confidence in cash flow generation relative to debt service requirements. Lenders will scrutinise copper price sensitivity models carefully, assessing whether debt service coverage ratios remain acceptable across a range of price scenarios below the base case. The strength of the reserve base, the projected operating cost structure, and the presence of institutional co-investors all contribute to improving lender comfort on this dimension.

Furthermore, the financing architecture is expected to draw from multiple source categories:

- Export credit agency facilities: government-backed lending from nations with equipment supply or service sector exposure to the construction programme

- Commercial bank debt: syndicated term loans from international project finance institutions

- Multilateral and development finance institution debt: facilities from World Bank group entities and regional development banks

- Capital markets instruments: potential project bonds providing long-tenor tranches suited to the mine's operating life

Blending these sources is not simply a cost optimisation exercise. It also extends the overall debt maturity profile, matching repayment schedules more closely to the mine's long-term production horizon. Export credit agencies typically offer tenors that commercial banks alone cannot match, while multilateral involvement often brings concessional pricing and reputational credibility that encourages other lenders to participate.

The Appointment of Societe Generale: What It Signals

In May 2026, McEwen Copper confirmed the appointment of Societe Generale as the sole financial advisor responsible for structuring and arranging the senior debt package for the Los Azules project. This is a substantive mandate, not a symbolic one.

The scope assigned to Societe Generale encompasses both the preparatory and implementation phases of the debt process, including:

- Development of the overarching financing strategy and debt tranche architecture

- Preparation of the lenders' information memorandum, which serves as the primary marketing document for prospective debt providers

- Coordination of independent technical, environmental and social, insurance, audit, and tax due diligence on behalf of the lender group

- Assistance with term sheet and loan agreement negotiations across multiple lender categories

Each of these workstreams contributes directly to what practitioners call project bankability — the collective assessment by lenders that a project is sufficiently well-structured, technically sound, and commercially viable to warrant long-tenor debt commitment. The appointment of a global bank with established ECA and multilateral relationships to lead this process is itself a signal to the market that the project has crossed an informal threshold of institutional credibility.

Michael Meding, managing director of McEwen Copper, characterised the appointment as a meaningful step toward construction, emphasising that Societe Generale's network across export credit agencies, multilateral institutions, and commercial banks positions the bank to help assemble a competitively priced debt package for a project of this global significance. (Creamer Media / Mining Weekly, May 15, 2026)

What Financial Advisor Appointment Actually Means: Many observers conflate the role of financial advisor with that of lender. They are distinct functions. The advisor structures the deal, prepares documentation, and coordinates the lender group. The lenders provide the capital. Societe Generale's appointment signals that the deal architecture work has begun in earnest, but it does not represent committed lending.

The Institutional Equity Stack and Its Strategic Dimensions

Debt cannot be assembled without a credible equity foundation. At Los Azules, the equity stack carries significant strategic weight beyond its purely financial function.

Rio Tinto's Nuton copper technology venture holds a 17.2% stake in McEwen Copper, representing a total investment of US$100 million to date. Nuton's involvement is notable for two reasons. First, a major mining company's equity participation provides lenders with a degree of technical credibility that financial-only investors cannot replicate.

Nuton brings heap leach technology capabilities that could have meaningful implications for copper recovery rates and potential mine-life extensions at Los Azules — factors that directly affect long-term cash flow projections underpinning debt serviceability. Second, Rio Tinto's involvement suggests that the project has passed an informal technical due diligence threshold set by one of the industry's most sophisticated operators.

The International Finance Corporation's collaboration agreement with McEwen Copper introduces a different but equally important dimension. The IFC Performance Standards have effectively become the global benchmark for environmental, social, and governance compliance in international project finance. Alignment with these standards does not merely satisfy ethical criteria. It materially expands the pool of eligible lenders, since many development finance institutions and certain commercial banks require IFC standard compliance as a precondition for participation.

This alignment, established prior to Societe Generale's appointment, effectively pre-qualifies the project for a broader range of debt sources. US government-linked institutions including the Export-Import Bank and the International Development Finance Corporation have also been identified as potential financing participants. However, it is important to note that no confirmed facility or commitment from these bodies has been publicly confirmed at this stage.

Argentina's RIGI Framework: Sovereign Risk Through a Lender's Lens

One of the most consequential enabling conditions for the McEwen Copper Los Azules project financing is the project's admission to Argentina's RIGI framework, the Régimen de Incentivo para Grandes Inversiones. Designed to attract large-scale foreign direct investment, RIGI provides participating projects with long-term protections across fiscal, regulatory, and foreign exchange dimensions.

For international project lenders, sovereign and regulatory risk in an emerging market jurisdiction is not a marginal concern. It is frequently the primary determinant of whether long-tenor debt is available at all, and at what price. In practical terms, a project exposed to potential retroactive fiscal changes, capital controls, or arbitrary regulatory intervention cannot support the debt service coverage ratios that lenders require, because the predictability of cash flows is fundamentally compromised.

RIGI admission addresses this concern by providing contractual-style protections that reduce the probability of adverse sovereign intervention during the project's operational life. This has a direct and measurable effect on the risk premium embedded in debt pricing, making the overall financing more economically efficient for the project.

| Risk Category | Without RIGI | With RIGI Admission |

|---|---|---|

| Fiscal stability | Subject to legislative change | Long-term rate protections |

| Foreign exchange | Exposure to capital controls | Access and repatriation rights |

| Regulatory certainty | Discretionary | Enhanced contractual framework |

| Lender risk premium | Elevated | Materially reduced |

Argentina's macroeconomic history means that RIGI alone does not eliminate country risk entirely. Lenders will likely complement RIGI protections with political risk insurance from multilateral guarantors, further cushioning the transaction against tail-risk scenarios. The combination of RIGI admission, IFC ESG alignment, and an anticipated political risk insurance layer represents a comprehensive risk mitigation architecture that is increasingly standard for large-scale mining project finance in emerging market jurisdictions.

The next major ASX story will hit our subscribers first

From Advisor Appointment to Financial Close: The Process Ahead

With Societe Generale appointed and the feasibility study complete, the McEwen Copper Los Azules project financing has moved into active transaction preparation. The pathway from current status to financial close involves a structured sequence of interdependent workstreams:

- Financing strategy finalisation: Societe Generale defines the tranche structure, target lender universe, and indicative pricing parameters

- Lenders' information package preparation: A comprehensive package covering technical, financial, ESG, and legal aspects assembled for prospective lenders

- Due diligence coordination: Independent technical, environmental, and insurance advisors appointed by and working on behalf of the lender group

- Term sheet negotiation: Pricing, security structure, financial covenants, and operational undertakings agreed with lead lenders

- Syndication: The debt is distributed across ECA, multilateral, and commercial bank participants

- Financial close: All conditions precedent satisfied and loan agreements formally executed

- Construction commencement: Capital drawdowns begin against verified construction milestones

Large-scale mining project finance transactions of this complexity typically require between 18 and 36 months from financial advisor appointment to financial close, depending on the complexity of the lender group, the pace of due diligence completion, and the stability of the underlying commercial and sovereign environment. Key dependencies for Los Azules include copper price trajectory, Argentine macroeconomic conditions, and the pace of ECA mandate approvals in participating export countries.

Benchmarking Los Azules Against Comparable Copper Project Financings

Context matters when assessing whether the Los Azules capital structure is realistic. Comparing it against other Tier-1 copper project financings that have proceeded to construction or operation provides useful reference points:

| Project | Location | Total CapEx (approx.) | Financing Model | Current Status |

|---|---|---|---|---|

| Los Azules | Argentina | ~US$4.0B | ECA + DFI + Commercial + bonds | Financing phase |

| Quellaveco | Peru | ~US$5.5B | ECA + commercial bank syndication | Operational |

| Kamoa-Kakula | DRC | ~US$7.0B+ | Equity-heavy + DFI | Operational |

| Resolution Copper | USA | TBD | Pending permitting resolution | Pre-development |

The Quellaveco transaction, developed by Anglo American in Peru, established a useful precedent for ECA-backed copper project finance in a South American jurisdiction, demonstrating that blended debt structures involving export credit agencies and commercial banks can be executed successfully at multi-billion dollar scale. Kamoa-Kakula, developed in the Democratic Republic of Congo, illustrated the viability of a more equity-intensive structure where sovereign risk profiles made conventional debt structuring more challenging.

Los Azules sits between these two models, benefiting from a South American location and the RIGI framework while still requiring the kind of institutional debt participation that characterises the Quellaveco model. In addition, the copper supply crunch currently facing global markets reinforces the strategic urgency of progressing projects of this calibre toward production.

Risk Factors That Lenders and Investors Are Monitoring

Strong feasibility economics and institutional alignment do not eliminate execution risk. Informed observers are monitoring several specific risk categories:

- Construction cost inflation: At high altitude in a remote Andean location, logistics, labour, and equipment costs are subject to pressures not present in lower-elevation projects

- Argentine macroeconomic volatility: Currency dynamics and broader economic conditions remain a monitoring priority for lenders despite RIGI protections

- Copper price sensitivity: Debt service coverage ratios must remain acceptable across a realistic range of copper price scenarios below the base case used in the feasibility study

- Water resource management: High-altitude Andean environments present specific challenges for water sourcing and management that require careful technical and regulatory navigation

- Community and social licence considerations: Operating in a remote region with local communities requires sustained engagement throughout construction and operation

Investor Caution: The financial metrics from the October 2025 feasibility study are compelling, but feasibility-stage economics are inherently subject to change as detailed engineering, procurement, and contracting processes advance. Capital cost estimates on large greenfield projects have historically experienced upward revision as engineering definition increases. Investors and analysts should treat feasibility-stage figures as directional rather than definitive.

How Should Investors Approach copper capital allocation at This Stage?

For investors evaluating exposure to Los Azules, understanding copper capital allocation at this stage of a project's lifecycle is essential. The period between financial advisor appointment and financial close carries its own risk-return profile, distinct from both the exploration phase and the operational phase. Prudent copper investment strategies involve monitoring key milestones — lender information package release, due diligence completion, and term sheet signing — as leading indicators of transaction progress.

What Financial Close at Los Azules Would Mean for the Copper Industry

Successfully financing and constructing a project of Los Azules' scale would have consequences extending well beyond McEwen Copper's own production profile. With average annual output projected at approximately 148,200 tonnes of copper cathode, the project would represent a meaningful addition to global supply at a time when the gap between projected demand growth and anticipated production capacity continues to widen.

More broadly, a successful Los Azules financing would establish a replicable template for how large greenfield copper projects can be structured in today's capital environment: blending export credit agency debt, multilateral facilities, development finance institution participation, and commercial bank tranches within a regulatory framework designed to provide investor certainty. It would also reinforce Argentina's positioning as a viable destination for major mining capital following years of investor uncertainty about the country's fiscal and monetary environment.

For the global copper market, the McEwen Copper Los Azules project financing represents one of the most closely watched transactions of this decade. Its progress through the stages from financial advisor appointment to financial close will be read by analysts, lenders, and competing project developers as a real-time indicator of both institutional appetite for large-scale copper development and the broader viability of emerging-market critical mineral project finance in an era of structural demand growth.

Disclaimer: This article contains forward-looking statements and financial projections drawn from published feasibility study data and publicly available reporting. All figures are subject to change as the project advances through engineering and financing processes. This article does not constitute financial advice. Readers should conduct independent research and consult qualified advisors before making investment decisions. References to government-linked financing institutions reflect publicly reported engagement only and do not imply confirmed commitments or facilities.

Want to Track the Next Major Copper Discovery Before the Market Moves?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries — instantly translating complex geological data into actionable investment insights for both short-term traders and long-term investors. Explore historic examples of major mineral discoveries and their market returns, then start your 14-day free trial at Discovery Alert to position yourself ahead of the next significant find.