June 13, 2026

The Permitting Paradox at the Heart of Mexico's Copper Ambitions

Few variables in global mining carry as much weight right now as the speed at which environmental agencies process applications. Across Latin America, the gap between a world-class mineral deposit and a producing mine has widened considerably, and nowhere is this tension more visible than in Mexico. The country sits on geology that could meaningfully reshape its copper output trajectory before 2030, yet the critical constraint is not ore grade, metallurgy, or even capital availability. It is the administrative machinery that governs access to the ground itself.

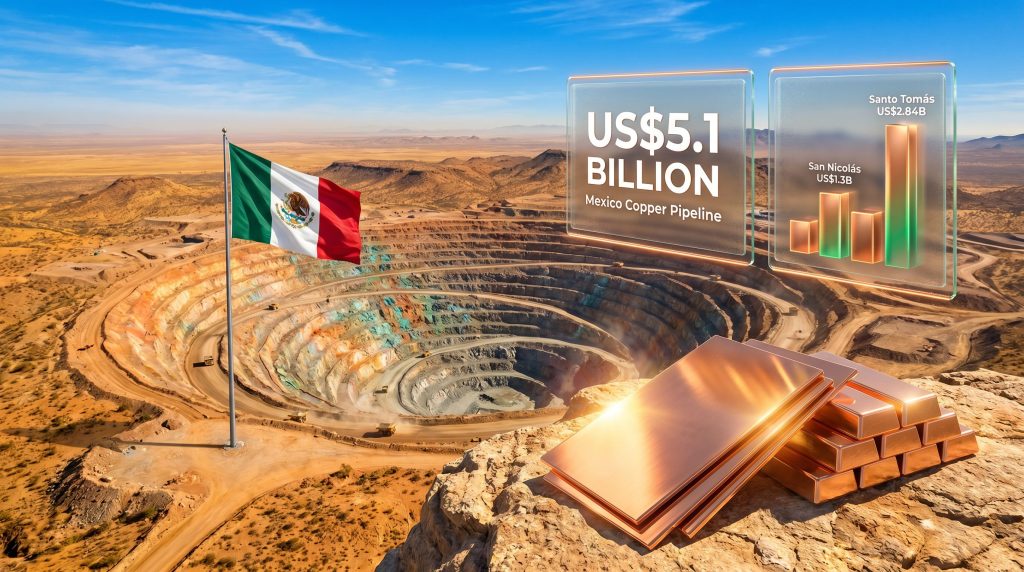

With at least US$5.161 billion in copper and polymetallic investment advancing through various stages of development, Mexico copper permits have become the single most consequential variable in its mining cycle. The projects in this pipeline span open-pit giants, underground expansions, and brownfield growth assets. What they share is a common dependency: regulatory clearance before capital can be fully committed and construction mobilised.

When big ASX news breaks, our subscribers know first

What Mexico Copper Permits Actually Require

Understanding why timelines stretch across years rather than months requires a working knowledge of Mexico's multi-agency approval architecture. Unlike jurisdictions where a single environmental body holds primary authority, copper mine development in Mexico demands parallel engagement with several regulatory arms of the federal government. These mining permitting frameworks share certain structural similarities with other resource-rich nations, though Mexico's layered system presents its own unique complexities.

The four primary approval categories that large-scale copper projects must navigate are:

- Mining Concession issued by the Secretaría de Economía, granting the legal right to explore and exploit a defined area

- Environmental Impact Assessment (MIA) filed with and assessed by SEMARNAT, required before any surface disturbance begins

- Forestry Land-Use Change (ETJ) also processed through SEMARNAT, mandatory where projects intersect forested or ecologically sensitive land

- Water Use Permits (Concesión de Aguas) issued by CONAGUA, particularly critical for heap-leach and flotation operations that depend on sustained process water access

A copper project requiring all four approvals simultaneously, as most large-scale open-pit operations do, historically faces a review process extending 18 to 36 months under normal administrative conditions, and considerably longer during periods of backlog or regulatory transition.

The layered nature of this system creates a compounding risk: a delay in any single approval stream can stall downstream processes entirely, since construction financing typically cannot be finalised until the full approval suite is secured. Furthermore, for projects in or adjacent to Natural Protected Areas, indigenous consultation requirements add another procedural layer with its own timeline dynamics.

The February 2026 Concession Recovery: Signal, Not Noise

In February 2026, Mexican authorities announced the recovery of approximately 1,200 mining concessions across six states, covering nearly 890,000 hectares. Of the total, 713 were located within Natural Protected Areas. The primary grounds for cancellation were non-payment of mining duties and failure to submit mandatory annual reports.

For active, administratively compliant developers, this action did not directly affect existing concession holdings. However, its significance as a regulatory signal should not be underestimated. The enforcement action established that:

- Administrative obligations will be enforced with greater rigour going forward

- Concessions in or near protected areas face elevated scrutiny regardless of compliance history

- The government is actively distinguishing between inactive or speculative concession holders and capital-backed development projects with production timelines

This bifurcation in regulatory treatment is the key interpretive lens for understanding Mexico's current mining governance posture.

Mapping the US$5.1 Billion Pipeline: Where Capital Concentrates

The aggregate investment figure of US$5.161 billion is highly concentrated. Two assets, Santo Tomás in Sinaloa and San Nicolás in Zacatecas, account for approximately 81% of identified pipeline capital. This concentration means that the permitting outcomes for just these two projects will determine whether Mexico's copper output trajectory shifts materially before 2030.

| Project | State | Estimated Investment | Primary Commodity | Target Start |

|---|---|---|---|---|

| Santo Tomás | Sinaloa | US$2.84 billion+ | Copper | Post-2029 |

| San Nicolás | Zacatecas | US$1.3 billion | Copper-Zinc | 2026 FID target |

| El Pilar | Sonora | US$310 million | Copper cathodes | 2029 |

| Media Luna Norte | Guerrero | US$108-113 million | Copper-Gold-Silver | Q4 2026 |

| Los Ricos Sur | Jalisco | ~US$227 million | Silver-Copper | Permit pending |

| Los Ricos North | Jalisco | Not disclosed | Silver-equivalent | 2027 |

| San Javier | Sonora | US$117 million | Copper-Gold | Not confirmed |

| La Fortuna | Durango | US$26.9 million | Gold | Not confirmed |

Beyond this window, Southern Copper's El Arco project in Baja California targets approximately 190,000 tonnes per year of copper output at an estimated cost of US$2.9 billion, but its timeline extends toward 2030 and is contingent on the electrical interconnection of the Baja California peninsula with the national grid, a task assigned to the CFE.

Santo Tomás: A Case Study in Capital Escalation

One of the most analytically significant developments across the entire pipeline is the dramatic revision in capital requirements at the Santo Tomás project. Between August 2024 and May 2025, the estimated capital cost escalated from US$1.1 billion to more than US$2.84 billion, representing a 158% increase in under twelve months.

The primary drivers behind this revision include:

- Expansion of the staged open-pit design, ramping from 60,000 tonnes per day in year one to 120,000 tonnes per day by year eight

- Infrastructure demands associated with the project's remote Sinaloa location

- Updated cost assumptions reflecting global construction materials and labour cost inflation

- Refinement of the prefeasibility study incorporating Phase 2 drilling data, with 3,606 metres drilled across 14 boreholes logged by May 2026

At full build-out, the operation is designed to average 99,427 tonnes of copper per year across a 22.6-year mine life. The prefeasibility study is targeted for completion in Q2 or Q3 2027. For investors, the capital escalation at Santo Tomás illustrates a broader dynamic in large-scale copper development: a definitive feasibility study conducted at higher throughput rates and in complex logistical environments routinely generates cost revisions that dwarf initial scoping estimates.

Project-by-Project Regulatory Status in 2026

San Nicolás: The Nearest Final Investment Decision Candidate

San Nicolás in Zacatecas represents the most advanced large-scale copper project in Mexico's current permitting queue. The joint venture between Teck Resources and Agnico Eagle filed both its Environmental Impact Statement and Forestry Land-Use Change application with SEMARNAT in January 2024, with rulings anticipated by the end of Q2 2026.

A favourable SEMARNAT outcome would clear the pathway to a Final Investment Decision targeted for Q3 2026. The deposit's fundamental metrics are compelling:

- Mineable reserves: 118 million tonnes at 1.8% copper and 1.5% zinc

- Planned throughput: 20,000 tonnes per day via open-pit and flotation

- Annual production targets: approximately 125 million pounds of copper and 156 million pounds of zinc

- Mine life: 17 years

- Projected economic spillover: approximately US$3.3 billion over project life

- Potential ranking: Mexico's third-largest copper producer and second-largest zinc producer

The copper grade of 1.8% places San Nicolás firmly in the high-quality tier for new development projects globally. For context, the average grade of copper mines brought into production over the past decade has trended below 0.6%, making deposits above 1% increasingly rare and commercially significant. Indeed, the broader copper supply crunch makes high-grade assets like this even more strategically valuable in the current cycle.

Media Luna Norte: Closest to Production Start

Torex Gold's Media Luna Norte expansion at the Morelos complex in Guerrero is the only project in the identified pipeline with a confirmed Q4 2026 production start target. Capital of US$100-105 million has been allocated within a total project envelope of US$108-113 million.

The expansion adds approximately 2,500 tonnes per day of throughput, bringing the total Morelos complex capacity to 12,000-13,000 tonnes per day. Copper output is forecast at 60-65 million pounds in 2026, rising to a sustained 70-75 million pounds annually across 2027-2030.

Los Ricos Sur: Execution-Ready, Awaiting a Single Permit

GoGold Resources has advanced Los Ricos Sur in Jalisco to a state of execution readiness that is unusual for a project still awaiting construction authorisation. Detailed engineering is complete, long-lead equipment has been ordered, underground mining contractor Cominvi has been appointed, and a power supply agreement has been secured with CFE through the La Yesca hydroelectric facility.

The feasibility study outlines a 2,000 tonne per day underground operation requiring approximately US$227 million in capital. The company has characterised the project as ready to commence construction upon receipt of the relevant authorisation. GoGold's second asset in the Jalisco district, Los Ricos North, carries a 2027 startup target in CAMIMEX's latest annual report, with indicated resources of 87.8 million silver-equivalent ounces and a preliminary economic assessment showing an after-tax NPV of US$413 million.

El Pilar: Measured Advancement Under Southern Copper

Southern Copper's El Pilar project in Sonora represents a more methodical development profile. The US$310 million solvent extraction-electrowinning (SX-EW) operation is designed to produce 36,000 tonnes per year of copper cathodes from 2029, supported by 317 million tonnes of proven and probable reserves grading 0.249% copper.

SX-EW technology is particularly relevant here because it enables direct production of high-purity copper cathodes from oxide ores without the need for smelting infrastructure, reducing both capital intensity and logistical complexity for remote operations. Southern Copper CFO Raúl Jacob confirmed the project remains on track and is progressing as planned, while noting that certain assumptions still require validation before the company moves forward.

Mexico's Production Base and Competitive Context

Mexico produced approximately 700,000 tonnes of copper in 2025, ranking it tenth among global producers according to the United States Geological Survey. The domestic production base is heavily concentrated, with CAMIMEX data for 2024 showing the following structure:

| Producer | Estimated Share of National Output |

|---|---|

| Grupo México | ~78% |

| Capstone Copper | Secondary |

| Nemisa | Secondary |

| Industrias Peñoles | Secondary |

| Minera Frisco | Secondary |

The pipeline under development, if fully permitted and constructed, would add meaningful diversification to this concentrated production base. San Nicolás alone could rank as Mexico's third-largest copper producer on a standalone basis.

How Mexico Compares to Peer Latin American Jurisdictions

Assessing Mexico's regulatory environment in isolation understates the competitive context. Investors routinely benchmark permitting risk across Latin American copper jurisdictions when allocating capital.

| Factor | Mexico | Chile | Peru | Argentina |

|---|---|---|---|---|

| Primary permit authority | SEMARNAT + Secretaría de Economía | SEA | MINEM + SENACE | Secretaría de Minería |

| Typical EIA timeline | 18-36+ months | 24-48 months | 24-60 months | 12-24 months |

| Concession freeze risk | Active (2026) | Low | Low-Moderate | Low |

| Recent policy direction | Accelerating for large projects | Stable | Reform-in-progress | Pro-investment (RIGI) |

Note: Timeline comparisons are indicative and vary significantly by project scale, location, and political context. Investors should conduct jurisdiction-specific due diligence before drawing conclusions about comparative regulatory risk.

What this comparison reveals is that Mexico's EIA timelines are not unusually long by Latin American standards, but the concurrent concession enforcement actions create a layer of uncertainty that peers like Chile and Argentina do not currently present. For developers with compliant concession records and strong community relationships, Mexico remains a viable and commercially attractive jurisdiction. Bureaucracy has paralysed several key Mexican mining projects worth more than US$4 billion in the past, however, underscoring that regulatory risk is not merely theoretical.

The next major ASX story will hit our subscribers first

Government Policy: Acceleration and Enforcement in Parallel

The Mexican government's regulatory posture in 2026 reflects a deliberate dual strategy. On one hand, enforcement of concession obligations has been tightened significantly, as demonstrated by the February recovery action. On the other, explicit commitments to accelerate approvals for large-scale projects have been made at the ministerial level.

Key policy developments shaping the operating environment include:

- Economy Minister Marcelo Ebrard announced plans to accelerate mining permit processing in 2026, targeting large-scale exploration and development projects

- Officials reported that 110 of 176 previously stalled projects had been resolved, with administrative normalisation projected by mid-2026

- Up to US$7 billion in mining investment is identified as pending permit approvals, according to government and industry sources

- Sonora state authorities report 83 active projects under monitoring, including El Pilar as part of Southern Copper's US$10.2 billion national investment pipeline

- Mexico announced the simplification of 42 mining and extractive procedures, reducing administrative friction for compliant developers

The simultaneous cancellation of 1,200 concessions and the announced acceleration of permit approvals for large-scale projects reflects a deliberate bifurcation in Mexico's mining governance. The government appears to be distinguishing between non-compliant or inactive concession holders and major capital-backed developers. For investors, the central question is whether this distinction will be applied consistently and transparently as the pipeline matures.

The Electrification Demand Thesis and Mexico's Strategic Relevance

The urgency surrounding Mexico copper permits cannot be fully understood without situating it within the global copper demand outlook. Copper is a foundational material in electric vehicles, power grid infrastructure, renewable energy systems, and the data centre construction boom. Every sector driving the clean energy transition requires substantially more copper per unit of output than the fossil fuel systems it is replacing. Understanding these copper demand drivers is therefore essential context for evaluating Mexico's pipeline significance.

Several factors position Mexico's copper pipeline as strategically relevant beyond its borders:

- Global copper demand is forecast to grow significantly through 2030 as electrification programmes scale across North America, Europe, and Asia

- Mexico's geographic proximity to the United States positions its copper output as directly relevant to North American industrial supply chains

- The USMCA framework creates preferential conditions for Mexican mineral exports to US manufacturers

- New mine supply globally faces extended development timelines, meaning projects advancing through permitting today will be among the marginal producers when demand peaks

The 2026-2029 project window in Mexico consequently represents more than a domestic investment story. The projects advancing through Mexico's permitting system today are potential contributors to North American electrification infrastructure at a moment when alternative supply sources face their own development timelines and geopolitical complications.

Key Indicators and Decision Triggers to Monitor

For investors and developers tracking Mexico's copper permitting environment, the following milestones carry the highest signal value through the remainder of 2026 and into 2027:

- San Nicolás SEMARNAT ruling (expected by end of Q2 2026): A positive outcome triggers the Q3 2026 Final Investment Decision process for the US$1.3 billion Teck-Agnico Eagle joint venture

- Los Ricos Sur construction authorisation (GoGold Resources): Mobilisation timing will determine whether the 2027 production target remains achievable

- Media Luna Norte first ore (Torex Gold, Q4 2026): The earliest confirmed production milestone in the entire pipeline

- Santo Tomás prefeasibility study (Q2-Q3 2027 target): Will incorporate Phase 2 drilling results and provide the first rigorous capital and production estimate for the now US$2.84 billion+ project

- El Pilar investment decision (Southern Copper, 2027-2028 estimated): The final validation of assumptions cited by CFO Raúl Jacob will determine whether the 2029 cathode production target holds

Furthermore, those exploring copper investment strategies should note that Mexico's permitting trajectory over the next 18 months will serve as a key barometer for whether the broader pipeline can deliver within commercially viable timeframes. Monitoring how junior developers navigate the approval process for smaller projects also provides early signals about systemic improvements in processing efficiency. Mexico copper permits, in this respect, are not merely a country-level story but a lens through which global copper supply adequacy can be meaningfully assessed.

Disclaimer: This article is for informational purposes only and does not constitute financial or investment advice. All project timelines, capital estimates, and production forecasts are subject to change based on regulatory outcomes, commodity prices, and company decisions. Investors should conduct independent due diligence before making any investment decisions.

Want to Track the Next Major Copper Discovery Before the Market Does?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries — instantly transforming complex mineral data into actionable investment insights for both short-term traders and long-term investors. Explore historic examples of exceptional discovery returns and begin your 14-day free trial today to position yourself ahead of the market.