June 13, 2026

The Hidden Economics of Vertical Integration in Copper Mining

Vertical integration sounds compelling on paper. The logic appears straightforward: if you control the raw material, why not capture every dollar of margin all the way down the chain? In copper, however, this intuition repeatedly collides with a set of market mechanics that make downstream processing far less attractive than it appears. Understanding Vale copper cathodes in Brazil requires looking past the surface narrative of industrial self-sufficiency and into the actual economics of how copper value is distributed across its supply chain.

For Brazil specifically, this tension is playing out in real time. With a major critical minerals demand policy framework now moving through the legislature and one of the world's great copper provinces sitting in the eastern Amazon, the country faces a deceptively complex question: does producing more refined copper actually create more wealth, or does it simply add cost?

When big ASX news breaks, our subscribers know first

Where Copper Value Actually Lives: The Supply Chain Breakdown

The copper supply chain is conventionally divided into three distinct stages: mining and concentration, smelting, and electrorefining. What is less commonly understood is how unevenly economic value is distributed across these stages.

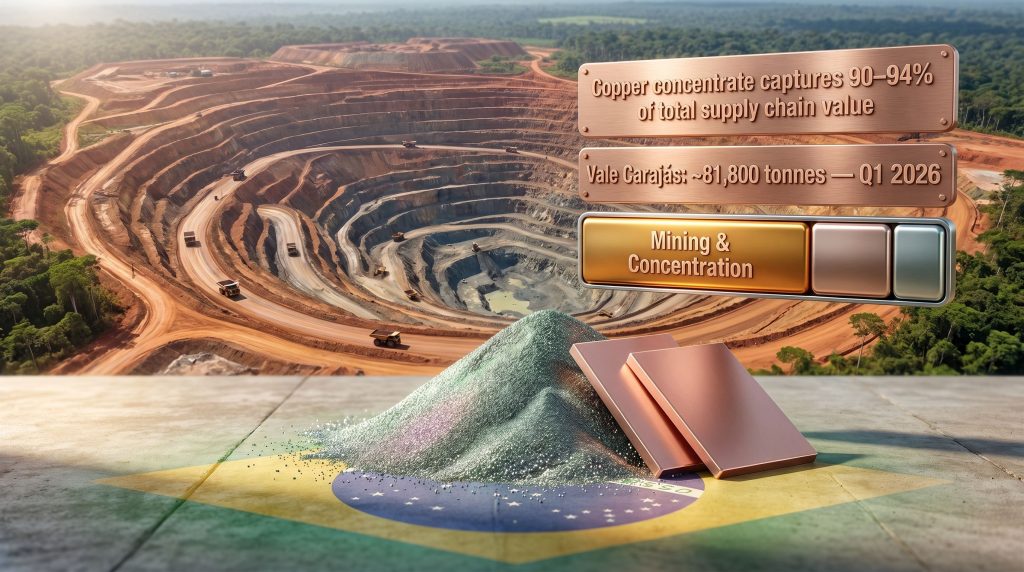

Copper concentrate production captures an estimated 90 to 94 percent of the total embedded value in the copper supply chain. This figure is not static; it shifts with market conditions. However, its structural dominance over downstream stages is consistent enough to fundamentally reshape how mining companies should think about capital allocation.

The three stages can be summarised as follows:

- Mining and concentration — ore extraction, crushing, flotation processing, and delivery of copper concentrate typically containing 25 to 35 percent copper by weight

- Smelting — pyrometallurgical conversion of concentrate into blister copper or anode copper, typically achieving purity of 97 to 99 percent

- Electrorefining — electrochemical processing of anode copper to produce Grade A copper cathodes at 99.99 percent purity

The value gap between stages two and three combined, relative to stage one, is the central economic reality that shapes Vale Base Metals' strategic decisions in Brazil.

How TC/RC Dynamics Amplify Concentrate Value in Bull Markets

The pricing mechanism for copper concentrate is built around a benchmark formula linked to the London Metal Exchange. Producers receive the LME copper price, minus treatment charges paid to smelters per dry metric tonne of concentrate (TC), minus refining charges applied per pound of payable copper (RC), and minus penalty deductions for impurities such as arsenic, bismuth, or fluorine in the concentrate.

What makes this formula particularly powerful for concentrate producers in high-price environments is the inverse relationship between LME copper prices and TC/RC rates. When copper price drivers push prices higher, smelters compete aggressively for feed material and their negotiating leverage diminishes, compressing the TC/RC deductions. The net result is that concentrate producers see their realised prices rise faster than the LME copper price alone would suggest.

| Market Condition | LME Copper Price | TC/RC Level | Benefit to Concentrate Producer |

|---|---|---|---|

| Bull market | High | Low/Compressed | Maximum — concentrate price rises sharply |

| Bear market | Low | High | Reduced — smelters extract more margin |

| Neutral market | Moderate | Moderate | Balanced returns across chain |

This dynamic is not academic. It represents a structural advantage that concentrate producers hold in precisely the market conditions most investors associate with mining sector outperformance.

Vale Base Metals has publicly indicated that the aggregate value contribution of copper concentrate would need to fall to approximately 60 to 65 percent of total supply chain value before cathode production becomes a financially rational next step. Current market conditions in Brazil do not approach that threshold.

Vale Copper Cathodes in Brazil: What the Operations Actually Produce

A persistent misconception in market commentary is that Vale's Brazilian copper operations are somehow incomplete because they stop at concentrate. This reflects a misunderstanding of both the economics and the operational structure.

Vale's Brazilian copper production is entirely concentrated within the Carajás mineral province in Pará state in the eastern Amazon, one of the richest mineral districts on the planet. Both of its primary operating assets produce copper concentrate exclusively.

| Asset | Location | Q1 2026 Output | Primary Product |

|---|---|---|---|

| Salobo | Carajás, Pará | ~52,800 tonnes | Copper concentrate |

| Sossego | Carajás, Pará | ~29,000 tonnes | Copper concentrate |

| Brazil Total | Carajás region | ~81,800 tonnes | Copper concentrate |

Full-year 2024 copper production across Vale's Brazilian operations reached 348,000 metric tonnes, with Salobo serving as the dominant contributor. Vale copper cathode production, where it exists, is associated with the company's Canadian refining infrastructure, not its Brazilian assets.

Important clarification: The absence of copper cathode production in Brazil is not a strategic gap or missed opportunity. It is a deliberate, economically grounded decision rooted in supply chain value analysis.

The Bacaba Project and Vale's Long-Term Carajás Vision

The next major growth asset within the Carajás complex is the Bacaba copper project, which has received a preliminary environmental licence and is targeting first production in the first half of 2028. Bacaba forms the central pillar of Vale's stated ambition to double its copper production capacity by 2035, supported by a capital commitment of $10 billion across the Carajás complex over the next decade.

| Milestone | Timeline |

|---|---|

| Bacaba preliminary environmental licence | 2025-2026 |

| Bacaba first production target | H1 2028 |

| Carajás copper capacity doubling target | 2035 |

| Total 10-year capital commitment | $10 billion |

Bacaba's development is occurring in proximity to environmentally sensitive conservation units within the Amazon biome, adding layers of regulatory and social complexity that are likely to influence the project timeline. Furthermore, the preliminary licence represents meaningful progress, but it is only the first of several regulatory hurdles that greenfield copper projects in Brazil must navigate.

Why Building a Copper Smelter in Brazil Doesn't Add Up

Constructing a greenfield copper smelter is among the most capital-intensive decisions in base metals mining. Capital outlays routinely run into multiple billions of dollars, construction timelines extend across years, and the ongoing energy and operational cost burden is substantial.

Set against the 6 to 10 percent of total supply chain value available at the smelting and refining stage, the investment case simply does not close in Brazil's current cost environment. Several compounding factors make the economics even less favourable:

- Brazil's industrial energy costs are elevated relative to major copper smelting nations, particularly China and parts of Southeast Asia

- The country lacks a sufficiently large domestic copper fabrication base to efficiently absorb cathode output at competitive volumes

- Logistics infrastructure between the Carajás region and potential coastal refining locations adds cost and operational complexity

- The global smelting industry is already structurally oversupplied in certain segments, further compressing the margins available to new market entrants

What Would Need to Change for Cathode Economics to Shift

For downstream copper processing to become economically viable in Brazil, a specific and demanding set of conditions would need to converge simultaneously:

- Sustained structural compression of global smelting capacity, driving TC/RC rates persistently higher for concentrate sellers

- The emergence of a substantial domestic copper demand base, driven by industries such as electric vehicle manufacturing or national grid infrastructure rollout

- Energy cost reform or industrial co-investment sufficient to offset smelter operating costs at a competitive level

- The aggregate value contribution of concentrate falling below the 60 to 65 percent threshold identified by industry participants

None of these conditions are imminent. Critically, waiting for them to converge while building smelting infrastructure prematurely would destroy value, not create it.

Brazil's Critical Minerals Bill: A Policy Framework With a Copper Problem

Brazil's lower house approved a critical minerals bill on 7 May 2026 that ties approximately half of its available financial benefits to domestic processing and transformation of critical minerals. For copper concentrate producers, who are already capturing the economically rational share of supply chain value, this creates a structural disadvantage.

The bill's architecture applies a broadly uniform framework across minerals with fundamentally different market characteristics. Copper operates in a mature, highly liquid, globally benchmarked market with LME-linked pricing. Rare earths and lithium, by contrast, face genuine geopolitical supply concentration risks and lack the depth of liquid global markets that copper enjoys.

| Dimension | Copper | Rare Earths | Lithium |

|---|---|---|---|

| Global market liquidity | Very high (LME-traded) | Low to moderate | Moderate |

| Domestic processing rationale | Weak — economics unfavourable | Strong — geopolitical imperative | Moderate |

| Value capture at concentrate stage | 90-94% | Variable | Variable |

| Brazil's current processing capability | Minimal | Very limited | Early stage |

By treating copper identically to strategically scarce minerals such as rare earths, the bill risks penalising producers who are already maximising economic value at the concentrate stage. The financial consequence is significant: copper concentrate producers in Brazil could be excluded from an estimated R$5 billion in tax credits over a five-year period because they are declining to invest in processing infrastructure that the economics do not support.

Policy design flaw: Requiring domestic processing as a condition of financial incentives works for minerals where in-country value addition is both feasible and strategically justified. Applying the same logic to copper, where concentrate already captures the overwhelming majority of chain value, effectively penalises rational economic behaviour.

The Regulatory Bottleneck: Brazil's Deepest Structural Problem

Beyond policy design, industry participants consistently identify bureaucratic speed as the single most binding constraint on Brazil's copper sector competitiveness. The capital is available, and the resource endowment is world-class. What is missing is the institutional capacity to convert geological wealth into operating mines within a commercially relevant timeframe.

The average timeline to bring a new copper project from discovery to first production in Brazil is approximately 17 years. Global copper supply deficits are projected to emerge within 15 years. The arithmetic is stark: a project initiated in Brazil today would, on average, not enter production until approximately 2042, well after projected supply shortfalls are expected to intensify.

The operational constraints at Brazil's National Mining Agency (ANM) illustrate the depth of the problem. Consequently, the copper supply crunch risks being exacerbated by these institutional delays:

- The ANM is operating at approximately 60 percent below full staffing capacity

- Its critical minerals division has only 4 employees assigned to it

- Approximately 15,000 economic plans are pending review across the agency

| Metric | Brazil | China (Reference) |

|---|---|---|

| Average copper project development timeline | ~17 years | Significantly shorter |

| ANM critical minerals division staffing | 4 employees | N/A |

| Pending economic plans at ANM | ~15,000 | N/A |

| Smelting capacity growth (last decade) | Negligible | ~+33% |

China added roughly one-third of its total copper smelting capacity over the past decade, a benchmark that illustrates what streamlined industrial policy and rapid permitting frameworks can achieve. Brazil's trajectory, by comparison, reflects what happens when regulatory velocity fails to match resource ambition.

Slow environmental licensing, limited bureaucratic predictability, and timeline uncertainty compound the delay problem at every stage of project development. Industry participants at Brazil's Ibram mining institute seminars have consistently described regulatory speed as a more urgent priority than any downstream processing mandate. In addition, mining permitting reforms are widely viewed as the most direct lever available to Brazilian policymakers.

Brazil's Reserve-to-Production Gap: Is Geology the Constraint?

Brazil holds significant copper reserves within the Carajás province. Despite this geological endowment, the country's share of global copper production remains disproportionately small relative to its known resource base. Brazil reportedly holds between 24 and 25 percent of global critical mineral reserves across categories, yet produces less than 1 percent of global output in several key minerals, according to Brazil's economics ministry.

The gap between geological potential and operational output reflects systemic institutional barriers rather than any deficiency in the underlying resources:

- Slow environmental licensing that extends project timelines across multiple regulatory stages

- Underfunded regulatory agencies operating well below required staffing levels

- Limited geological survey coverage in frontier and transitional areas adjacent to known deposits

- Workforce constraints in specialised mining, processing, and geoscience disciplines

The next major ASX story will hit our subscribers first

Frequently Asked Questions: Vale Copper Cathodes in Brazil

Does Vale produce copper cathodes in Brazil?

No. Vale's Brazilian copper operations produce copper concentrate exclusively, primarily from the Salobo and Sossego mines within the Carajás region of Pará state. Copper cathode production associated with Vale is linked to Canadian refining operations, not Brazilian assets.

Why has Vale declined to build a copper smelter in Brazil?

The economics do not support it under current conditions. Copper concentrate already captures 90 to 94 percent of the value embedded in the copper supply chain. The capital cost of smelter construction, combined with Brazil's energy cost structure and absence of a large domestic fabrication market, means the marginal value added by cathode production cannot generate an acceptable return on investment.

What threshold would make copper cathode production viable in Brazil?

Industry analysis suggests the aggregate value contribution of concentrate would need to fall to approximately 60 to 65 percent of total supply chain value. Reaching this threshold would require a significant structural shift in global TC/RC dynamics and the emergence of substantial domestic copper demand.

How much copper does Vale produce in Brazil?

In Q1 2026, Vale's Brazilian copper output reached approximately 81,800 tonnes, with Salobo contributing around 52,800 tonnes and Sossego approximately 29,000 tonnes. Full-year 2024 production totalled 348,000 metric tonnes.

What is Vale's next major copper project in Brazil?

The Bacaba project within the Carajás complex has received a preliminary environmental licence and is targeting first production in the first half of 2028, forming a central pillar of Vale's plan to double copper production capacity by 2035.

How does Brazil's critical minerals bill affect copper producers?

Approximately 50 percent of the bill's financial incentives are tied to domestic processing and transformation. Since building copper smelting infrastructure in Brazil is currently uneconomic for concentrate producers, they risk exclusion from an estimated R$5 billion in tax credits over five years.

Strategic Takeaways for Investors and Industry Observers

The debate over Vale copper cathodes in Brazil ultimately reveals a broader truth about how value is created and distributed in commodity supply chains. Vertical integration is not inherently value-accretive. In copper, under current market conditions and within Brazil's cost environment, it is value-destructive.

Furthermore, copper investment strategies that fail to account for where value actually sits in the supply chain risk misallocating capital at precisely the wrong moment. Several high-leverage conclusions emerge from this analysis:

- Concentrate production is not a lesser form of participation in the copper market. It is the economically optimal position in the chain for producers operating in high-price environments with compressed TC/RC rates.

- Policy frameworks must account for commodity-specific economics. Applying uniform processing mandates across minerals with structurally different market dynamics risks penalising sectors that are already performing at their rational optimum.

- Regulatory reform is the single highest-leverage intervention available to Brazil's copper sector. Halving the average project development timeline would unlock far more economic value than any downstream processing requirement.

- The supply deficit window is closing. Brazil's ability to capitalise on its copper endowment depends on accelerating project pipelines now, not diverting capital toward processing infrastructure the market does not yet justify.

- Vale's $10 billion Carajás commitment signals genuine long-term conviction, but that capital will generate the greatest return when directed toward high-value concentrate expansion rather than marginally economic downstream stages. For further context on Vale's expansion plans, their evaluation of iron ore, copper, and nickel projects offers useful perspective on capital prioritisation across commodities.

It is also worth noting that Brazil's broader Amazon proximity challenges are well documented. Recent reporting on copper activity near protected areas highlights the environmental complexity that sits alongside every major expansion decision in the Carajás region.

This article is intended for informational purposes only and does not constitute financial or investment advice. Forecasts, projections, and market estimates discussed herein are subject to material uncertainty and should not be relied upon as the basis for investment decisions. Readers should conduct independent due diligence and consult qualified financial advisers before making any investment decisions related to companies or projects mentioned in this analysis.

Want to Know When the Next Major Copper Discovery Hits the ASX?

Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time, delivering instant alerts on significant mineral discoveries — including copper — so subscribers can identify actionable opportunities before the broader market reacts. Explore historic discoveries and the exceptional returns they have generated, then begin your 14-day free trial at Discovery Alert to position yourself ahead of the market.