June 17, 2026

Understanding Mexico's Energy Investment Paradigm Through Partnership Models

Mexico's upstream oil sector stands at a strategic crossroads where traditional state-controlled development models intersect with market-driven capital requirements. The evolution of mixed contracts in PEMEX oil production represents more than a policy adjustment—it reflects fundamental tensions between resource nationalism and economic pragmatism that define energy development across Latin America.

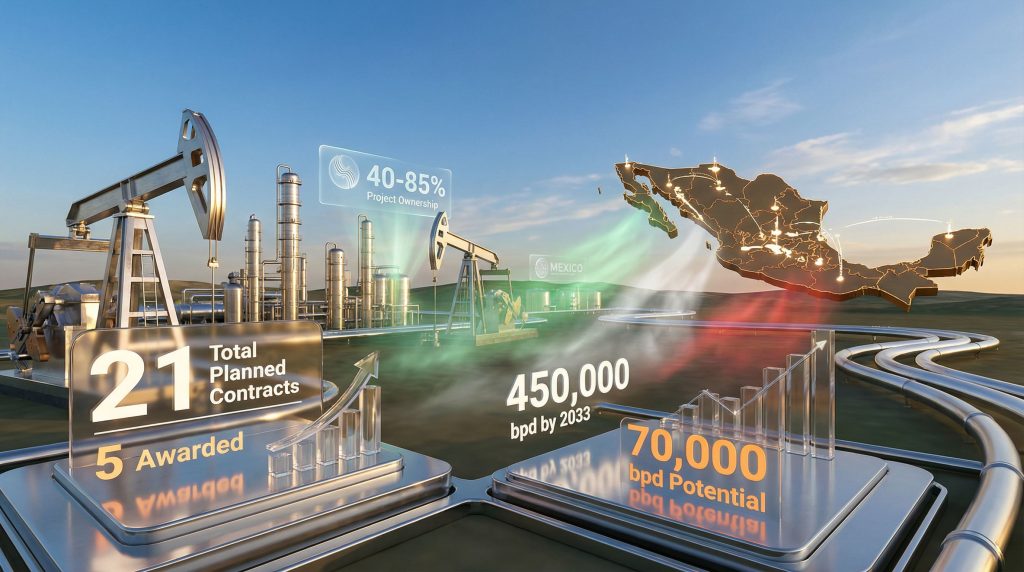

Mixed contracts in PEMEX oil production emerged as Mexico's attempt to maintain constitutional requirements for state energy control while accessing private sector capital and technical expertise. This hybrid framework allows PEMEX to retain majority ownership ranging from 40-85% whilst enabling private partners to contribute operational capabilities and investment funding.

Current market dynamics reveal significant implementation challenges. Of the 21 planned mixed contracts, only five have been awarded as of early 2026, representing a 24% completion rate. The production impact from these initial contracts amounts to approximately 40,000-70,000 barrels per day, substantially below the framework's ambitious targets.

When big ASX news breaks, our subscribers know first

Technical Framework Analysis: How Mixed Contracts Reshape Production Strategy

The mixed contract structure in PEMEX oil production operates through several distinct mechanisms that differentiate it from traditional concession or service agreement models prevalent elsewhere in Latin America.

Core Structural Elements:

• State ownership preservation through minimum 40% PEMEX participation requirements

• Private sector contributions of technical expertise and capital investment

• Shared production arrangements with negotiable revenue distribution

• Focus on conventional onshore fields rather than frontier exploration

This framework maintains Mexico's constitutional mandates while attempting to address PEMEX's capital constraints. However, the legal rigidity of participation requirements—embedded directly in Mexican law rather than negotiable at the contractual level—creates structural inflexibility that limits private sector interest.

Production Baseline and Target Analysis

Mexico's current production baseline of approximately 1.6 million barrels per day in 2025 falls significantly short of the Strategic Plan 2025-2035 target of 1.8 million barrels per day by 2030. The mixed contracts framework was designed to contribute 450,000 barrels per day of additional production through successful implementation of all 21 planned contracts.

Current performance metrics reveal substantial gaps between targets and achievements:

| Metric | Target | Current Status | Achievement Rate |

|---|---|---|---|

| Total Contracts | 21 planned | 5 awarded | 24% |

| Production Addition | 450,000 bpd | 70,000 bpd potential | 16% |

| Investment Target | $8 billion | $50 million secured | 0.6% |

| International Participation | Encouraged | Zero participation | 0% |

The mathematical reality suggests that even perfect execution of remaining contracts would fall short of compensating for natural field decline from Mexico's ageing asset base, which has experienced production decrease from peak output of 3.4 million barrels per day in 2004.

Financial Architecture: PEMEX's Debt Crisis and Fiscal Implications

The financial pressures driving Mexico's mixed contract strategy in PEMEX oil production stem from the state company's unprecedented debt burden and its systemic impact on sovereign finances. Furthermore, these pressures reflect broader challenges discussed in the canada energy transition context, where state-owned entities face similar capital constraints.

Debt Structure Analysis

PEMEX's total liability structure exceeds $122 billion, comprised of:

• Financial debt: Approximately $100 billion

• Supplier obligations: $22 billion in short-term commitments

• Contingent liabilities: Multiplying commercial and labour lawsuits requiring accounting reserves

The Mexican government provided $21.7 billion in direct support to PEMEX in 2025, representing an unprecedented level of fiscal commitment that achieved only marginal debt reduction. Supplier debt, measured at $28 billion in Q3 2025, continues to constrain operational capacity and supplier relationships.

Sovereign Debt Interconnection

The technical linkage between PEMEX's financial distress and Mexico's sovereign debt creates compounding risks that extend beyond the energy sector. Federal budget deficits projected to remain at 3% of GDP through 2026 combine with total government debt expectations of 52-56% of GDP by 2026 to create constrained fiscal space for additional PEMEX support.

In addition, these fiscal challenges mirror concerns highlighted in us debt & inflation analysis, where energy sector performance directly impacts sovereign financial stability.

Risk Escalation Pathways:

-

Baseline Scenario: Continued government support maintains current debt levels but pressures fiscal sustainability

-

Stress Scenario: Oil price decline below $50 per barrel triggers additional fiscal pressure and potential credit rating impact

-

Crisis Scenario: Sovereign credit downgrade increases borrowing costs across all government entities, creating systemic financial constraints

The interconnected nature of PEMEX's debt with sovereign obligations means that international credit rating agencies evaluate the company's financial health as a component of Mexico's overall fiscal stability rather than as an isolated corporate entity.

International Operator Hesitancy: Regulatory and Investment Climate Barriers

The absence of international oil company participation in mixed contracts in PEMEX oil production reflects rational business decision-making based on regulatory constraints and competitive regional alternatives rather than ideological opposition to Mexican energy policy.

Structural Investment Barriers

International operators require flexible operational frameworks that allow contract terms to be tailored based on project-specific economics and risk profiles. The current mixed contract structure presents several constraining factors:

• Fixed participation requirements: Minimum PEMEX ownership percentages established by law rather than negotiable terms

• Limited operational control: Private partners constrained in decision-making authority on production rates, capital deployment, and technical approaches

• Regulatory uncertainty: Mexico's recent energy policy shifts create unpredictable institutional environment

• Counterparty risk: PEMEX's financial condition raises concerns about the state company's ability to fulfil project commitments

Regional Competitive Analysis

International oil companies evaluate Mexican opportunities within the context of alternative regional investment options that offer more favourable terms and greater operational flexibility:

Brazil's Pre-Salt Framework: Competitive bidding processes with flexible state company involvement through Pré-Sal Petróleo S.A., allowing negotiated participation based on project economics rather than fixed legal requirements.

Argentina's Vaca Muerta Model: Unconventional play development with reduced state participation in operational decisions and enhanced private sector control over technical approaches.

Suriname's Offshore Success: Recent discoveries operating under frameworks providing clearer operational authority for private partners and streamlined regulatory processes.

The contrast in regulatory flexibility explains why international capital flows toward these alternatives rather than Mexican mixed contracts, despite Mexico's proven resource base and established infrastructure. For instance, the saudi exploration licenses demonstrate how competitive licensing frameworks can attract significant international investment.

Production Scenario Modelling: Pathways to 2030

Strategic scenario analysis for mixed contracts in PEMEX oil production reveals multiple potential outcomes with varying probability distributions based on policy adjustments and market conditions.

Scenario Probability Assessment

Optimistic Scenario (30% probability):

• All 21 mixed contracts awarded and operational by 2028

• 450,000 barrels per day additional production achieved

• Current fields maintain stable output through enhanced investment

• Result: 1.75-1.8 million barrels per day by 2030

Base Case Scenario (50% probability):

• 12-15 mixed contracts successfully implemented

• 200,000-300,000 barrels per day production addition

• Natural field decline partially offset by new development

• Result: 1.4-1.5 million barrels per day by 2030

Pessimistic Scenario (20% probability):

• Limited mixed contract success (under 10 contracts)

• Continued production decline from mature fields without adequate investment

• Financial constraints limit both PEMEX and government capacity for sector support

• Result: 1.2-1.3 million barrels per day by 2030

Energy Security Implications

The base case scenario creates significant energy security concerns for Mexico. Current natural gas import dependence of 70% from the United States combined with potential crude oil import requirements suggests increasing energy vulnerability.

However, broader energy market trends, including those discussed in us natural gas forecast, indicate that regional supply dynamics will continue to influence Mexico's energy strategy. The International Energy Agency scenario projecting Mexico as a crude oil importer by 2030, requiring 500,000 barrels per day of imports, appears increasingly probable under current mixed contract implementation trends. This transformation would fundamentally alter Mexico's energy profile from net exporter to import-dependent status.

Global Market Dynamics and Regional Competition Effects

Mixed contracts in PEMEX oil production operate within a global energy context characterised by supply abundance and regional production increases that affect project economics and investment attractiveness. Similarly, the oil price rally analysis suggests that geopolitical factors continue to influence regional energy investment decisions.

Oil Price Environment Impact

International oil price expectations significantly influence mixed contract viability and Mexico's fiscal capacity to support PEMEX operations:

• $70+ per barrel: Mixed contracts become financially attractive with manageable debt service requirements

• $54.9 per barrel (budget baseline): Marginal economics with continued fiscal pressure on government support

• Below $50 per barrel: Contract economics deteriorate substantially, creating fiscal crisis risk

Regional Supply Competition

New production capacity additions from Caribbean and South American producers create additional price pressure on Mexican crude exports through increased regional supply:

Expected Regional Production Additions (2025-2030):

• Brazil offshore developments: 400,000 barrels per day

• Caribbean basin projects: 300,000 barrels per day

• Venezuelan potential (contingent on stabilisation): 300,000+ barrels per day

This additional 1 million barrels per day of regional supply creates competitive pressure that could reduce price premiums for Mexican crude exports, affecting the financial returns available to support mixed contract development.

The next major ASX story will hit our subscribers first

Geopolitical Considerations Affecting Energy Strategy

Regional geopolitical dynamics create both constraints and opportunities for Mexico's mixed contract framework, particularly regarding relationships with Venezuela, Cuba, and the United States.

Venezuela Situation Analysis

US intervention in Venezuela creates multiple scenarios that could reshape regional energy dynamics and affect Mexico's strategic positioning:

Venezuelan Stabilisation Impact: Potential return of Venezuelan crude oil production to global markets would increase regional supply and create price pressure on Mexican exports. This scenario could make mixed contracts less economically attractive whilst reducing Mexico's regional energy influence.

Continued Instability Scenario: Ongoing Venezuelan energy sector constraints maintain current market dynamics, allowing Mexico to preserve its regional position whilst avoiding additional competitive pressure.

US-Mexico Energy Cooperation: Enhanced partnership frameworks could improve investment climate for mixed contracts through reduced regulatory uncertainty and increased access to US capital and technology.

Cuba Oil Supply Geopolitical Implications

Mexico's crude oil supply to Cuba, now estimated to exceed $3 billion annually, represents a potential geopolitical pressure point that could affect overall energy policy flexibility. This supply arrangement, conducted through a PEMEX subsidiary operating as a trading entity, creates exposure to US policy shifts regarding Cuba.

The scale of this commitment—representing significant volumes that could otherwise be directed to commercial export markets—may require strategic recalibration as regional geopolitics evolve and US priorities shift under changing administrations.

Alternative Frameworks for Enhanced Private Investment

The limited success of current mixed contracts in PEMEX oil production suggests the need for regulatory modifications that could improve investment attraction whilst maintaining state strategic interests.

Regulatory Flexibility Options

Current constraints stem from legal requirements embedded in Mexican constitutional and statutory law rather than contractual negotiations. Potential modifications could include:

• Variable PEMEX participation: Allowing participation percentages to be determined by project economics rather than fixed legal minimums

• Enhanced operational control: Providing private partners with greater decision-making authority over technical and operational matters

• Alternative partnership structures: Exploring joint ventures, production sharing agreements, or other models beyond the current mixed contract framework

• Streamlined regulatory processes: Reducing approval timelines and administrative complexity for private sector participation

International Best Practice Integration

Successful international models offer insights for potential Mexican regulatory evolution:

Norway's State Participation Model: Flexible government involvement through Equinor (formerly Statoil) with participation levels determined by project characteristics rather than legal requirements.

Brazil's Regulatory Evolution: Transition from rigid state control to competitive bidding with state company partnership, allowing market forces to determine optimal participation structures.

UK Continental Shelf Evolution: Historical progression from complete state control to private sector leadership, demonstrating successful transition pathways whilst maintaining regulatory oversight.

These models suggest that maintaining strategic state interests does not require rigid participation requirements, and that flexibility can actually enhance state benefits through increased investment and production.

Technical Challenges and Unconventional Resource Development

Mixed contracts in PEMEX oil production face additional complexity when applied to unconventional resources that require hydraulic fracturing technology and specialised operational expertise.

Shale and Tight Oil Development Constraints

Mexico possesses unconventional deposits similar to those in Texas, but geographical and technical differences create additional investment challenges:

• Logistical complexity: Mexico's geography creates greater transportation and infrastructure challenges compared to established US shale regions

• Technical expertise requirements: Unconventional development requires specialised knowledge and equipment that PEMEX currently lacks

• Profit margin compression: Current mixed contract economics may not support the higher capital requirements and technical complexity of unconventional development

• Regulatory framework adaptation: Existing mixed contract structure may require modification to accommodate unconventional development requirements

Natural Gas Development Challenges

The Lakach offshore development, primarily focused on natural gas production, illustrates the economic challenges facing mixed contracts in gas-focused projects:

Economic Constraint Analysis:

• Expected production costs significantly exceed imported US natural gas prices

• Technical challenges increase capital requirements beyond current mixed contract financial structures

• Mexico's 70% natural gas import dependence on the United States creates price competition that affects domestic development economics

This situation demonstrates how mixed contracts must address not only regulatory and financial constraints but also fundamental resource economics that may not support development under current market conditions.

Strategic Inflection Point Assessment

The current trajectory of mixed contracts in PEMEX oil production suggests that 2026 represents a critical juncture for Mexico's energy future, with policy decisions determining whether the country can stabilise oil production or continue structural decline.

Window for Strategic Plan Achievement

The Strategic Plan 2025-2035 target of 1.8 million barrels per day by 2030 faces increasing feasibility challenges based on current implementation rates. The PEMEX operational performance has been mixed, with limited success in attracting major international players:

• Only 24% of planned mixed contracts awarded after substantial implementation time

• Zero international oil company participation despite global industry capacity

• Production additions from completed contracts representing less than 5% of required growth

• Natural field decline continuing to erode baseline production capacity

Mathematical analysis suggests that achieving the official target would require dramatic acceleration in both contract awards and production ramp-up rates that exceed historical precedent for similar projects globally.

Market Reality vs. Policy Objectives

The fundamental tension between maintaining state control and attracting necessary private investment creates a strategic paradox that requires pragmatic resolution:

Ideological Preferences: Preserving state majority control and resource nationalism principles embedded in Mexican constitutional framework.

Market Requirements: Private sector demands for operational flexibility, regulatory certainty, and competitive returns on investment that enable international capital participation.

Fiscal Constraints: Government financial limitations that prevent adequate public investment whilst requiring increased private sector participation to maintain production levels.

The convergence of these factors suggests that policy adjustments favouring increased regulatory flexibility may be necessary to prevent continued production decline and energy import dependence.

Energy Transition and Long-term Competitiveness

Mixed contracts in PEMEX oil production must also be evaluated within the context of global energy transition trends that affect long-term oil demand and investment attractiveness.

Investment Horizon Considerations

Oil and gas projects typically require 10-20 year investment horizons to achieve adequate returns, but global energy transition policies create uncertainty about long-term demand:

• Demand peak expectations: Various scenarios suggest oil demand may peak within the next decade

• Carbon pricing trends: Increasing carbon costs may affect project economics over investment lifecycles

• Technology substitution: Electric vehicle adoption and renewable energy growth could reduce oil demand growth rates

• Regulatory evolution: Climate policies may create additional compliance costs for fossil fuel development

These factors suggest that mixed contracts must not only address immediate regulatory and financial constraints but also position Mexico's energy sector for competitiveness within a transitioning global energy system.

Conclusion: Navigating Toward Energy Security Through Pragmatic Policy Evolution

The mixed contracts framework in PEMEX oil production represents Mexico's attempt to balance competing priorities of resource nationalism, fiscal sustainability, and energy security. Current implementation challenges—characterised by limited international participation, below-target production additions, and constrained financial returns—suggest the need for strategic recalibration.

Furthermore, the mixed contracts face significant challenges in attracting major international oil companies, highlighting fundamental structural issues with the current approach. The window for achieving Mexico's 2030 production targets through the existing mixed contract structure is narrowing rapidly. Success requires enhanced regulatory flexibility that allows market forces to determine optimal partnership structures whilst preserving strategic state interests. Without such adjustments, Mexico risks continued production decline, increased energy import dependence, and reduced regional competitiveness.

The convergence of PEMEX's financial constraints, Mexico's fiscal pressures, and global energy market dynamics creates urgency for pragmatic policy evolution. The choice facing Mexico's energy sector is clear: adapt regulatory frameworks to attract disciplined international capital, or maintain rigid structures that risk locking the sector into structural decline.

Future success will depend on Mexico's ability to reconcile ideological preferences with market realities, potentially through innovative partnership frameworks that achieve state strategic objectives whilst providing the operational flexibility and investment returns necessary to attract international participation. The stakes extend beyond energy policy to encompass broader questions of economic competitiveness, fiscal sustainability, and energy security that will define Mexico's development trajectory for decades to come.

Looking to Capitalise on Emerging Market Energy Opportunities?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, helping investors identify actionable opportunities ahead of the broader market, particularly as global energy transitions create new commodity demands. Begin your 30-day free trial today and understand why major mineral discoveries can generate substantial returns by exploring proven examples of exceptional market outcomes.