June 23, 2026

Why Mexico's State-Controlled Lithium Strategy Is Failing to Compete Globally

Mexico's limited funding regulations mexico lithium race has positioned the country at a significant disadvantage in the global competition for lithium development. When constitutional amendments in 2022 designated lithium as a strategic mineral reserved exclusively for state control, Mexico effectively eliminated private sector participation from exploration through production phases. This regulatory transformation occurred precisely as global lithium demand accelerated, creating a timing mismatch that continues to impact the nation's competitive position.

The 2022 Mining Law Amendment's Restrictive Framework

The creation of LitioMx as the sole authorised entity for lithium operations represents a fundamental shift from Mexico's previous mixed approach, where companies like Bacanora Lithium held active concessions. This regulatory transformation exemplifies how critical minerals strategy decisions can significantly impact national resource development trajectories.

Chile's hybrid model demonstrates an alternative framework that balances state interests with private sector efficiency. The South American nation operates through coordinated participation between state-owned Codelco and private producers SQM and Albemarle, achieving approximately 382,200 tonnes of lithium carbonate equivalent (LCE) production in 2023. Chile's National Lithium Commission, established in 2023, coordinates rather than replaces private investment, enabling rapid scaling of production capacity.

Moreover, Mexico's constitutional reservation creates structural barriers that extend beyond exploration rights. The framework restricts lithium export channels to state-only sales, limiting opportunities for private sector value-chain participation in refining and processing stages. This contrasts sharply with Australia's market-oriented approach, where companies like Pilbara Minerals and Core Lithium allocate USD $30-100 million annually for exploration under secure tenure frameworks.

Budget Allocation Versus Development Requirements

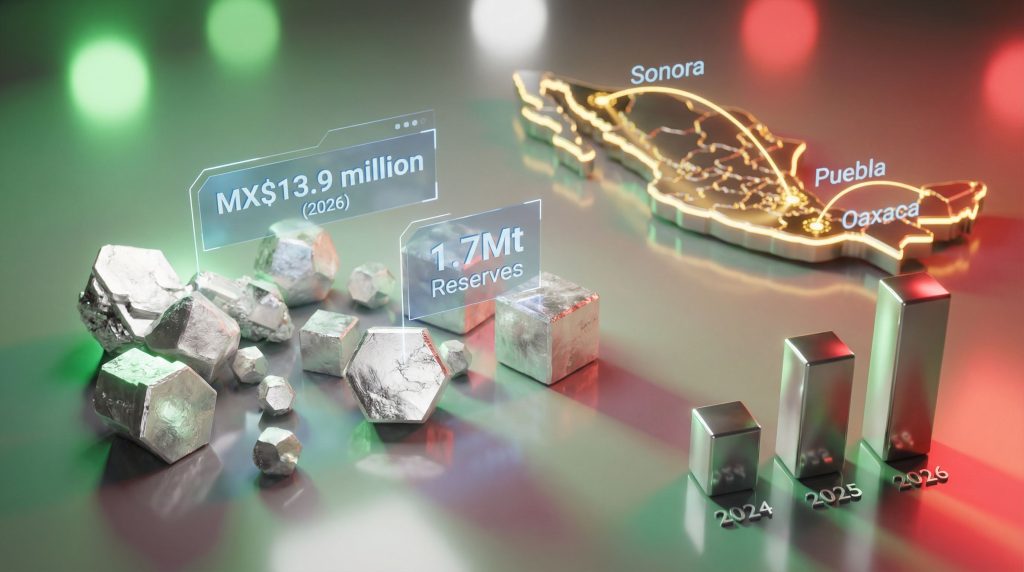

The funding trajectory for Mexico's state lithium enterprise reveals the scale of resource constraints facing the sector. LitioMx's budget progression from MX$9.8 million in 2024 to MX$13.9 million in 2026 represents approximately USD $825,000-875,000 at current exchange rates, covering primarily administrative and operational expenses.

| Year | Budget (MX$ millions) | % Increase | USD Equivalent | Primary Allocation |

|---|---|---|---|---|

| 2024 | 9.8 | — | ~$580,000 | Administrative costs |

| 2025 | 12.9 | 27.3% | ~$760,000 | Salaries & operations |

| 2026 | 13.9 | 7.7% | ~$825,000 | Operating expenses |

Industry analysis reveals the fundamental mismatch between allocated resources and exploration requirements. Lithium exploration projects globally typically require USD $5-20 million per site to advance from initial discovery to resource definition, depending on geological complexity and accessibility. Furthermore, development phases demand USD $50-150 million investment over 3-5 years to reach pilot production stages.

According to Rubén del Pozo, President of AIMMGM, the Mexican Mining Industry Association, LitioMx receives funding that covers operational survival rather than exploration advancement. The organisation functions with resources sufficient for administrative operations but insufficient for executing its core mandate of lithium exploration and development.

State-controlled mining enterprises in comparable jurisdictions operate with substantially different resource allocations. Chile's Codelco maintains annual exploration and development budgets exceeding USD $5 billion, with dedicated lithium divisions. This represents approximately 6,000 times Mexico's lithium budget allocation, highlighting the scale disparity between state approaches.

The funding gap extends beyond absolute amounts to strategic allocation patterns. While australia lithium innovations enable private explorers to dedicate 85-90% of budgets to technical activities including drilling, geological assessment, and metallurgical testing, Mexico's allocation prioritises organisational maintenance over resource development.

When big ASX news breaks, our subscribers know first

How Regulatory Contradictions Undermine Mexico's Lithium Potential

The Open-Pit Mining Paradox

Mexico's lithium regulations contain a fundamental technical contradiction that undermines the sector's development potential. While lithium has been designated as a strategic mineral capable of transforming Mexico's economic position, existing mining regulations restrict open-pit operations essential for lithium extraction.

Lithium extraction from clay deposits, Mexico's dominant resource type, requires surface mining methods due to geological characteristics. Clay-based lithium deposits typically occur at depths of 50-200 meters in horizontal layers, necessitating open-pit access for commercial viability. Consequently, underground mining techniques applicable to other minerals cannot economically extract lithium from these geological formations.

The technical requirements extend beyond extraction methods to processing infrastructure. Lithium processing from clay deposits requires large surface footprints for acid leaching facilities, precipitation systems, and waste management areas. Even Mexico's brine deposits in Sonora and Zacatecas require extensive evaporation ponds covering hundreds of hectares for commercial lithium recovery.

According to industry experts, this regulatory inconsistency reflects limited technical understanding of lithium extraction requirements. The contradiction creates uncertainty for project development, as environmental impact assessments often restrict open-pit operations without clear exceptions for strategic minerals.

Competing jurisdictions have addressed this challenge through regulatory clarity. For instance, Chile's mining regulations specifically authorise large-scale surface operations for strategic minerals under environmental permits designed for lithium projects. Similarly, Australia's Western Australian mining regulations designate lithium as a priority mineral with streamlined permitting processes that recognise extraction method requirements.

The regulatory contradiction has practical implications for Mexico's 82 identified lithium deposits across 18 states. Projects in Sonora (13 deposits), Puebla (12 deposits), and Oaxaca (9 deposits) face uncertain permitting timelines due to the open-pit restriction paradox, creating additional barriers to development beyond funding limitations.

Concession Termination Impact on Investor Confidence

The termination of existing lithium concessions following Mexico's 2022 constitutional amendments created precedent-setting investor confidence impacts that continue to influence foreign direct investment patterns. Bacanora Lithium's concession cancellation in Sonora represents the most significant case study of regulatory reversal consequences.

Bacanora had invested tens of millions of dollars in exploration, feasibility studies, and infrastructure development before the constitutional amendments eliminated private lithium rights. The company's investment write-offs demonstrate the financial risks associated with sudden regulatory changes in Mexico's mining sector.

However, the concession terminations occurred without compensation frameworks or grandfathering arrangements, distinguishing Mexico's approach from regulatory restructuring in other jurisdictions. When Chile modified lithium arrangements in 2023, existing concession-holders received opportunities for participation in new frameworks or compensation mechanisms rather than simple cancellation.

Under the USMCA framework, the termination of North American investor concessions without compensation could theoretically trigger Investor-State Dispute Settlement claims. Nevertheless, no formal USMCA disputes related to lithium concession terminations have been publicly filed as of January 2026, though the precedent influences risk assessments for future investments.

The investor confidence impact extends beyond terminated projects to future investment evaluation processes. International mining companies now factor higher political risk premiums into Mexican project assessments, increasing capital costs and reducing willingness to commit resources to exploration phases.

Furthermore, Australia's contrasting approach demonstrates the importance of tenure security for mining investment. Australian Mineral Tenement legislation provides explicit security frameworks where concessions can only be cancelled for specific operational breaches, not policy reversals. This regulatory stability enables long-term investment commitments essential for lithium project development.

What Mexico's Limited Funding Regulations Reveal About State Capacity

LitioMx's Operational Budget Analysis

Three consecutive years of operational-only funding for LitioMx reveals structural limitations in Mexico's state-controlled lithium strategy. The limited funding regulations mexico lithium race becomes evident when examining the budget trajectory from MX$9.8 million to MX$13.9 million, which represents administrative scaling rather than exploration investment, highlighting fundamental capacity constraints.

The currency conversion context underscores the resource limitation severity. Mexico's MX$13.9 million (approximately USD $825,000) represents 0.017% of Chile's Codelco exploration budget and 0.85-2.8% of typical Australian private explorer allocations. This disparity indicates systemic underfunding rather than temporary budget constraints.

Budget composition analysis reveals prioritisation of organisational survival over technical execution. Administrative costs including salaries, office operations, and regulatory compliance consume the majority of LitioMx's allocation, leaving minimal resources for geological assessment, drilling programmes, or metallurgical testing essential for lithium development.

The funding pattern suggests Mexico's lithium enterprise operates as a regulatory placeholder rather than an active exploration entity. Without substantial budget increases for technical activities, LitioMx cannot realistically advance any of Mexico's 82 identified deposits toward development phases within competitive global timelines.

Comparative state mining enterprise analysis demonstrates alternative funding models. Codelco's lithium division employs hundreds of geologists and engineers with dedicated technical budgets exceeding USD $100 million annually for exploration alone. This staffing and resource model enables systematic assessment of Chile's lithium reserves at commercial scales.

Exploration Investment Gap Analysis

Mexico's lithium reserves of 1.7Mt require substantial geological assessment and development investment to contribute meaningfully to global supply chains. Current funding levels prevent comprehensive evaluation of deposit quality, extraction costs, and processing requirements necessary for commercial viability determinations.

Global lithium exploration benchmarks indicate Mexico needs USD $400-1,600 million in total investment to systematically assess its 82 identified deposits, assuming USD $5-20 million per site for resource definition. LitioMx's current annual budget covers approximately 0.05-0.2% of this requirement, indicating 500-2,000 year timelines for comprehensive exploration under existing funding levels.

The geographic distribution of Mexico's deposits across 18 states creates additional logistical and technical challenges requiring coordinated exploration programmes. Sonora's 13 deposits, Puebla's 12 deposits, and Oaxaca's 9 deposits each require separate geological assessment campaigns with distinct metallurgical testing requirements.

Resource quality assessment represents another critical funding requirement. Mexico's lithium occurs primarily in clay deposits with different processing characteristics than the brine deposits dominating Chilean and Argentine production. Consequently, clay-based lithium extraction requires specialised metallurgical testing costing USD $1-5 million per deposit to determine commercial viability.

Technical expertise development represents an additional capacity constraint beyond funding limitations. LitioMx's current staff levels cannot realistically manage exploration programmes across multiple states simultaneously, requiring substantial personnel expansion and training programmes that exceed current budget allocations.

How Mexico's 1.7Mt Reserves Compare in the Global Context

Regional Lithium Reserve Distribution

Mexico's 1.7Mt lithium reserves position the country as a secondary player in Latin America's lithium landscape, significantly below Chile's reserves but potentially competitive with targeted development strategies. Regional reserve distribution reveals Mexico's opportunity within North American supply chain security frameworks.

Global Lithium Reserve Rankings:

- Chile: 9.3Mt (largest global reserves)

- Argentina: 2.7Mt (second-largest in region)

- Mexico: 1.7Mt (third in Latin America)

- Brazil: 0.95Mt

- Peru: 0.88Mt

Mexico's reserves concentration in 18 states provides geographic diversification advantages compared to Chile's Atacama Desert concentration or Argentina's "lithium triangle" focus. This distribution could support multiple development projects with reduced single-region dependency risks.

However, reserve quality analysis reveals important distinctions. Mexico's clay-based deposits require different extraction and processing technologies than the brine deposits dominating Chilean production. Clay extraction typically involves higher processing costs but can achieve production faster once facilities are constructed, as they avoid lengthy evaporation periods required for brine operations.

Resource assessment quality represents a critical knowledge gap. Mexico's 1.7Mt reserve estimate requires verification through systematic drilling and metallurgical testing to confirm commercial viability. Many estimates derive from preliminary geological surveys rather than comprehensive resource definition programmes conducted in Chile and Argentina.

Production Capacity Projections Under Current Framework

Mexico's lithium production potential under existing regulatory and funding frameworks faces severe timeline and capacity constraints. Current state-only development approaches cannot realistically deliver commercial production within globally competitive timeframes.

Realistic Production Timeline Analysis:

- Years 1-3: Administrative setup and preliminary surveys (current phase)

- Years 4-8: Resource definition and feasibility studies (if funding increases substantially)

- Years 9-12: Construction and commissioning (if projects prove viable)

- Year 13+: Commercial production commencement

This 13+ year timeline assumes substantial funding increases and regulatory streamlining. Under current MX$13.9 million annual budgets, meaningful production development becomes unlikely within relevant market windows.

Global supply projections highlight Mexico's opportunity cost. Current global lithium production exceeding 1Mt LCE in 2024 is projected to reach 1.22Mt in 2025, representing 20% annual growth. Industry forecasts indicate 3Mt annual demand by 2030, creating substantial supply opportunities that Mexico cannot access under current development constraints.

Competing jurisdictions demonstrate alternative development velocities. Australian lithium projects typically advance from discovery to production in 5-8 years under favourable regulatory frameworks and private sector investment. Similarly, Chile's new projects achieve similar timelines through coordinated public-private approaches.

Mexico's production capacity potential remains theoretical without substantial policy and funding reforms. The country's 82 identified deposits could theoretically support 200-400kt annual production capacity if developed systematically, representing 6-13% of projected 2030 global demand.

What Global Demand Growth Means for Mexico's Market Position

The 3Mt by 2030 Supply Challenge

Global lithium demand evolution creates a rapidly expanding market opportunity that Mexico risks missing under current development frameworks. Production growth from 1Mt LCE in 2024 to projected 3Mt by 2030 represents a 200% increase in global supply requirements within six years.

Annual Growth Trajectory:

- 2024: >1Mt LCE (actual production)

- 2025: 1.22Mt LCE (projected, +20% growth)

- 2026-2027: Continued 15-25% annual growth rates expected

- 2030: 3Mt LCE (industry demand projections)

This growth trajectory indicates 2Mt of additional annual production capacity must come online between 2024 and 2030 to meet projected demand. Mexico's theoretical production potential of 200-400kt annually could capture 10-20% of this growth market if development accelerates substantially.

Market timing considerations reveal Mexico's competitive disadvantage. Projects initiated today in Australia or Chile can achieve production by 2027-2029, capturing growth market opportunities. Moreover, Mexico's 13+ year development timeline under current frameworks means missing the primary demand expansion window.

Electric vehicle industry contract allocation patterns demonstrate supply chain security priorities. Major automotive manufacturers increasingly prioritise geographic diversification and supply security over lowest-cost sourcing, creating opportunities for North American lithium suppliers including Mexico.

However, automotive industry procurement operates on 3-5 year planning cycles for battery supply contracts. Mexico's extended development timelines prevent participation in current contracting cycles, potentially excluding the country from established supply relationships when production eventually commences.

Supply Chain Security Implications

Mexico's geographic position within North American trade frameworks provides strategic advantages for lithium supply chain security that remain underdeveloped due to regulatory and funding constraints. USMCA provisions create preferential access for Mexican lithium in automotive and battery supply chains.

North American Supply Chain Advantages:

- Transportation cost reductions compared to Chilean/Australian sources

- USMCA trade preference for automotive applications

- Currency stability relative to other Latin American producers

- Proximity to major battery manufacturing facilities in Texas and Mexico

Current battery gigafactory investments in North America create substantial proximate demand for lithium supplies. Facilities under construction or planning in Texas, Tennessee, and northern Mexico could absorb 300-500kt annual lithium carbonate equivalent, representing potential anchor demand for Mexican production.

Supply chain diversification strategies by major consumers increasingly prioritise multi-continental sourcing to reduce single-region dependency risks. Mexico could serve as a third continental source alongside Australian/Asian and Chilean/South American supply chains, providing strategic value beyond production costs.

Nevertheless, supply chain security advantages require actual production capacity to materialise. International battery and automotive companies cannot include Mexico in supply chain plans without credible production timelines and capacity commitments that current regulatory frameworks cannot provide.

Critical mineral designation discussions in North America may create additional advantages for Mexican lithium development. If lithium receives critical mineral status under North American security frameworks, Mexico could access development financing and technical assistance programmes currently unavailable.

How Competing Jurisdictions Structure Lithium Development

Chile's Public-Private Partnership Model

Chile's lithium development framework demonstrates how state strategic interests can coexist with private sector efficiency and investment capacity. The hybrid model combines state oversight through Codelco with private sector technical expertise and capital through SQM and Albemarle operations.

Chilean Regulatory Framework Components:

- State participation through Codelco lithium division

- Private operator licensing with production and environmental requirements

- Revenue sharing between state and private entities

- Technology transfer requirements for advanced processing methods

Chile's approach enables rapid scaling while maintaining state strategic control. SQM and Albemarle operations contribute technical expertise, international market access, and investment capital whilst generating tax revenues and employment for Chilean state interests.

Production results demonstrate the hybrid model's effectiveness. Chile's 382,200 tonnes LCE production in 2023 represents 38% of global output, achieved through coordinated public-private investment rather than state-only development approaches.

Environmental management under Chile's framework requires private operators to meet stringent water use and habitat protection standards whilst maintaining commercial viability. This approach addresses environmental concerns without prohibiting necessary extraction methods for strategic mineral development.

Investment attraction mechanisms in Chile include guaranteed tenure security, streamlined environmental permitting, and stable fiscal frameworks. These elements provide investor confidence essential for multi-hundred million dollar lithium project investments that Mexico's framework currently discourages.

Australia's Market-Oriented Approach

Australia's lithium sector leadership derives from market-oriented regulatory frameworks that encourage private sector competition whilst maintaining strategic oversight. The approach prioritises technical efficiency and rapid development over direct state control.

Australian Framework Characteristics:

- Competitive tenement allocation based on technical and financial capacity

- Secure tenure frameworks with explicit cancellation protections

- Environmental permitting designed for large-scale mineral extraction

- Export facilitation supporting global market access

Private sector participation levels in Australia demonstrate the investment response to supportive regulatory environments. Companies like Pilbara Minerals, Core Lithium, and Sayona Mining allocate USD $30-100 million annually for exploration and development under secure regulatory frameworks.

Technical expertise development results from competitive private sector participation. Australian lithium companies lead globally in spodumene processing technologies, waste management practices, and integrated mining-processing operations due to competitive innovation incentives.

Production scaling achievements in Australia highlight market-oriented advantages. The country achieved 63,000 tonnes LCE production in 2023 from a near-zero base in 2018, demonstrating rapid development velocity under supportive regulatory conditions.

Export-oriented production strategies enable Australian producers to access premium pricing in Asian battery markets whilst maintaining domestic supply security. This dual-market approach maximises economic returns whilst serving strategic mineral supply requirements.

Furthermore, technology transfer and knowledge development occur naturally through competitive private sector operations, creating specialised expertise that benefits the broader Australian mining sector through employee mobility and technical service provider development.

The next major ASX story will hit our subscribers first

What Policy Reforms Could Accelerate Mexico's Lithium Development

Hybrid Ownership Models for Strategic Resources

Mexico could accelerate lithium development through hybrid ownership frameworks that maintain state strategic control whilst accessing private sector investment and technical capabilities. Several Latin American countries demonstrate successful strategic mineral partnerships that balance national interests with development efficiency.

Potential Hybrid Framework Elements:

- Joint venture structures between LitioMx and qualified international partners

- State ownership majority (51%+) ensuring strategic control

- Private sector operational management leveraging technical expertise

- Technology transfer requirements building domestic capabilities

Risk-sharing mechanisms could address exploration phase uncertainties whilst preserving state interests in successful projects. Private partners could fund exploration and feasibility studies in exchange for production phase participation rights, reducing state financial exposure during high-risk development phases.

Revenue optimisation through hybrid models could exceed state-only development returns. Whilst state ownership provides 100% of limited production under current frameworks, shared ownership of substantially larger production volumes could generate higher absolute state revenues through partnership structures.

International precedents demonstrate hybrid model viability. Kazakhstan's uranium sector, Russia's diamond industry, and Chile's copper operations utilise state-private partnerships that maintain strategic control whilst achieving competitive production levels and technological advancement.

Technical expertise development represents a critical hybrid model benefit. International partnerships could establish training programmes, technology transfer initiatives, and domestic engineering capacity building that serve broader Mexican mining industry trends beyond lithium.

Regulatory Streamlining for Technical Compliance

Regulatory reform priorities should address the open-pit mining paradox that prevents lithium extraction whilst promoting lithium as a strategic mineral. Clear exception protocols for strategic minerals could resolve this fundamental contradiction.

Streamlining Proposals:

- Strategic mineral classification with extraction method exceptions

- Expedited environmental assessment processes for lithium projects

- Clear permitting timelines with automatic approval provisions

- Investor protection enhancements preventing sudden regulatory reversals

Environmental assessment modification could maintain ecological protection whilst enabling strategic mineral development. Risk-based assessment frameworks could distinguish between high-impact extractive operations and strategic mineral projects with appropriate mitigation requirements.

Regulatory certainty improvements could restore international investor confidence through grandfathering clauses, compensation frameworks, and dispute resolution mechanisms that prevent repeat concession cancellation scenarios.

Permitting timeline standardisation could establish 12-18 month maximum periods for lithium project environmental approvals, comparable to timeframes in competing jurisdictions whilst maintaining thorough environmental review requirements.

Technical capacity building within regulatory agencies could improve geological assessment capabilities, mining engineering expertise, and environmental impact evaluation specific to lithium extraction technologies and requirements.

When Will Mexico's Lithium Strategy Show Results?

Timeline Analysis Under Current Policies

Mexico's lithium development timeline under existing regulatory and funding frameworks extends well beyond globally competitive windows. Systematic analysis of required development phases indicates minimum 10-15 year periods before commercial production under current constraints.

Phase-by-Phase Timeline Projection:

- Years 1-2 (2026-2028): Administrative consolidation, staff hiring, initial site selection

- Years 3-5 (2028-2031): Preliminary geological surveys, resource estimation updates

- Years 6-8 (2031-2034): Detailed feasibility studies (if funding increases substantially)

- Years 9-12 (2034-2037): Environmental permitting, project engineering

- Years 13-15 (2037-2040): Construction, commissioning, production ramp-up

This timeline assumes substantial policy modifications including increased funding, regulatory streamlining, and resolution of open-pit mining restrictions. Without such reforms, commercial production timelines extend further into the 2040s or beyond.

Resource definition requirements alone could consume 5-7 years under adequate funding levels. Mexico's 82 identified deposits require systematic drilling, metallurgical testing, and economic assessment programmes that LitioMx cannot currently finance or execute at necessary scales.

Comparative development timelines in other jurisdictions highlight Mexico's competitive disadvantage. Australian lithium projects advance from discovery to production in 5-8 years, whilst Chilean projects achieve similar timelines through coordinated public-private investment frameworks.

Market Window Considerations

Global lithium market evolution may limit Mexico's opportunity window for competitive market entry. Current supply expansion plans by established producers could satisfy projected demand growth before Mexico achieves production capacity under existing development constraints.

Market Window Analysis:

- 2025-2027: Peak demand growth phase, highest pricing opportunities

- 2028-2030: Supply expansion from current producer scaling

- 2031-2035: Market equilibrium phase, competitive pricing pressures

- 2036+: Mexico's earliest realistic production timeline

Price trajectory implications suggest Mexico may enter global markets during equilibrium or declining price phases rather than growth periods with premium pricing opportunities. Early entry producers capture development cost recovery during high-price periods unavailable to late entrants.

Electric vehicle industry supply contract cycles operate on 3-5 year terms with renewal negotiations beginning 2-3 years before contract expiration. Mexico's extended development timeline prevents participation in current contracting cycles (2025-2030) and potentially subsequent cycles (2030-2035).

Technology evolution risks could impact Mexico's clay-based lithium deposits' competitiveness. Direct lithium extraction (DLE) technologies, recycling expansion, and alternative battery chemistries may reduce primary lithium demand growth rates below current projections.

Strategic positioning for second-generation market opportunities may represent Mexico's most realistic path forward. Rather than competing in initial market expansion phases, Mexico could target replacement demand, supply chain diversification needs, and technological advancement opportunities in post-2035 markets.

Frequently Asked Questions About Mexico's Lithium Regulations

Can Private Companies Participate in Mexico's Lithium Sector?

Current Mexican constitutional amendments prohibit private company participation in lithium exploration, extraction, and primary commercialisation activities. The 2022 regulatory framework reserves these activities exclusively for state-controlled entities, specifically LitioMx as the designated operator.

However, potential opportunities may exist in downstream value-chain activities including processing, refining, and manufacturing applications. Mexican regulations do not explicitly prohibit private sector participation in lithium-to-battery production chains, battery manufacturing, or industrial applications using lithium-derived products.

Service provider roles remain accessible to private companies, including geological consulting, drilling services, engineering design, and equipment supply for LitioMx operations. These opportunities provide limited market access compared to direct mining participation but maintain private sector involvement possibilities.

Future regulatory modifications could create joint venture opportunities or technical partnership frameworks that maintain state control whilst accessing private sector investment and expertise. However, such modifications would require constitutional amendments or interpretation changes not currently under active consideration.

International private companies evaluate supply contract opportunities for processed lithium products once Mexican production commences. Long-term supply agreements could provide market access without direct mining participation rights.

How Does Mexico's Approach Compare to Other Latin American Countries?

Mexico's state-exclusive lithium framework contrasts sharply with hybrid approaches adopted by other major Latin American lithium producers, creating different competitive dynamics and development trajectories. This comparison becomes particularly relevant when examining argentina lithium insights.

Regional Approach Comparison:

Chile: Public-private partnership model combining state participation (Codelco) with private operators (SQM, Albemarle). Results: 382,200 tonnes LCE production (2023), global market leadership, substantial investment attraction.

Argentina: Provincial government regulation with private company operations under concession agreements. Results: 39,000 tonnes LCE production (2023), multiple projects under development, significant Chinese and North American investment.

Bolivia: State-controlled development similar to Mexico, but with international technical partnerships. Results: Limited commercial production, extended development timelines, periodic policy reversals affecting investor confidence.

Investment climate comparisons reveal Mexico's competitive disadvantages. Chile and Argentina attract billions in annual lithium investment through frameworks that balance state interests with private sector participation. Mexico's exclusive state model limits investment to government budget allocations.

Production outcome assessments demonstrate hybrid model advantages. Countries combining state oversight with private sector technical capabilities achieve faster development timelines, larger production volumes, and higher technical standards compared to state-exclusive approaches.

What Are the Long-term Implications for Mexico's Energy Transition?

Mexico's lithium development constraints create potential supply security risks for domestic energy transition initiatives and electric vehicle manufacturing plans. The limited funding regulations mexico lithium race could significantly impact Mexico's ability to develop domestic battery supply chains despite substantial domestic reserves.

Energy Transition Impact Assessment:

Electric Vehicle Manufacturing: Mexico's automotive sector transformation toward EV production requires secure battery supply chains. Domestic lithium development delays could disadvantage Mexican EV manufacturing competitiveness compared to countries with developed domestic supply capabilities.

Grid Storage Applications: Mexico's renewable energy expansion requires large-scale battery storage systems for grid stabilisation. Import dependence for battery materials increases project costs and supply security risks.

Industrial Policy Integration: Mexico's lithium strategy must align with broader industrial development policies supporting battery manufacturing, EV production, and renewable energy deployment. Current regulatory frameworks may not provide sufficient coordination between mining and manufacturing sectors.

Economic opportunity costs from delayed lithium development could reach billions of dollars annually in foregone export revenues, employment creation, and related industry development. Mexico risks becoming a lithium importer despite substantial domestic reserves.

Regional competitiveness implications extend beyond mining to entire battery value chains. Countries developing domestic lithium production gain advantages in attracting battery gigafactory investments, EV manufacturing facilities, and related technology industries that Mexico could forfeit through development delays.

In addition, Mexico's situation reflects broader trends seen in junior explorers funding patterns globally, where state funding limitations often constrain exploration activities despite significant mineral potential.

Moreover, Mexico's mining policy shift under President Sheinbaum continues to influence investor confidence and international development partnerships, potentially affecting long-term supply chain security for North American markets.

Disclaimer: This analysis is based on publicly available information and industry expert insights as of January 2026. Lithium market projections, policy developments, and production timelines involve substantial uncertainties and may change significantly based on technological developments, regulatory modifications, and market conditions. Readers should conduct independent research and consult qualified professionals before making investment or policy decisions related to Mexico's lithium sector.

Looking to Capitalise on Global Lithium Market Opportunities?

While Mexico's state-controlled lithium strategy faces significant hurdles, the global lithium market presents compelling opportunities for investors positioned to identify emerging discoveries and developments. Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, including lithium and critical minerals announcements, instantly empowering subscribers to identify actionable opportunities ahead of the broader market. Begin your 30-day free trial today and secure your market-leading advantage in the rapidly evolving critical minerals sector.