June 17, 2026

The Governance Gap Choking Mexico's Mining Sector

There is a pattern observable across resource-rich economies that consistently confounds investors: the presence of world-class geology does not guarantee world-class output. The bottleneck is almost never underground. It sits above ground, buried in interagency workflows, administrative backlogs, and the compounding friction of multi-layered regulatory systems that were never designed to move quickly. Mexico offers one of the clearest contemporary examples of this dynamic, and in early 2026, permits slow non-oil mining in Mexico with a force that is beginning to reshape how capital is allocated across the sector.

Understanding why this is happening requires more than a surface-level read of permit approval rates. It demands a structural analysis of the regulatory architecture itself, the policy trajectory that shaped it, and the commodity-level consequences now flowing from it.

When big ASX news breaks, our subscribers know first

Mexico's Mining Endowment Versus Its Regulatory Reality

Mexico consistently ranks as the world's leading producer of silver, a position it has held for years, while also sitting among the top global suppliers of copper, zinc, lead, and gold. These are not marginal contributions to global supply. Silver from Mexico feeds industrial applications from electronics to photovoltaic panels. Its copper output is strategically relevant to electrification infrastructure across North America.

Zinc and lead production, often co-extracted from polymetallic deposits in states like Zacatecas and Chihuahua, underpin galvanizing, battery, and construction industries globally. Furthermore, the broader surge in critical minerals demand makes Mexico's position all the more strategically significant on the world stage.

Yet despite this endowment, the gap between resource potential and active production capacity has been widening since approximately 2019. The constraint is not geological. Mexico's known ore bodies are extensive and, in many cases, economically compelling at current commodity prices. The constraint is institutional, driven by a permitting environment that has grown progressively more difficult to navigate.

The core tension in Mexico's mining sector is not between investors and geology. It is between investors and governance. The resource is there. The regulatory pathway to access it has become the defining variable.

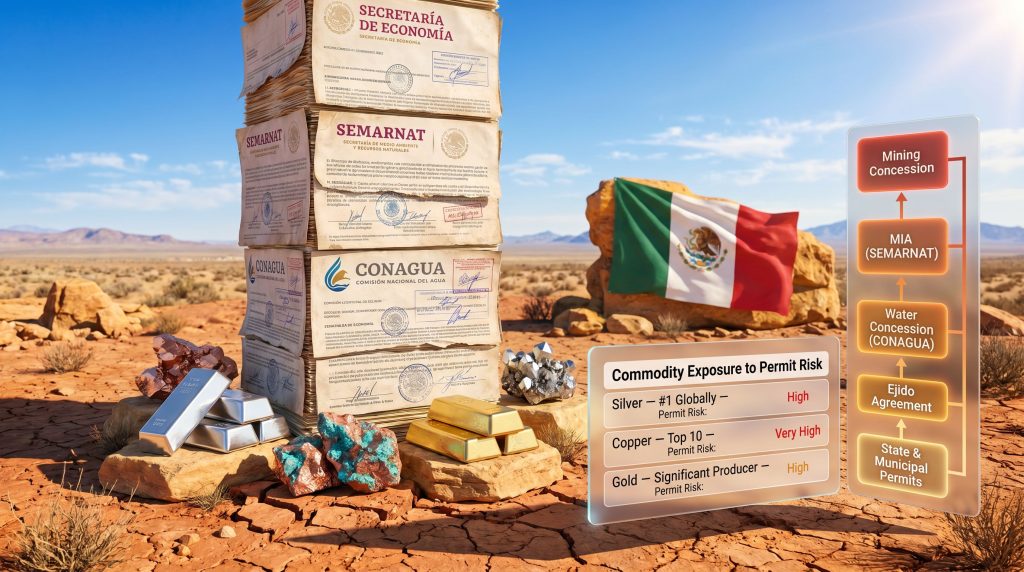

The Five-Layer Permit Stack: How It Works and Where It Breaks Down

To understand how permits slow non-oil mining in Mexico, it helps to map the full approval architecture. Projects do not face a single permit. They face a sequential and partially parallel stack of authorizations, each issued by a different authority, each with its own timeline, criteria, and failure modes.

| Permit Type | Issuing Authority | Primary Function | Key Risk Factor |

|---|---|---|---|

| Mining Concession | Secretaría de Economía | Mineral extraction rights | Near-moratorium on new grants since 2019 |

| Environmental Impact Authorization (MIA) | SEMARNAT | Environmental compliance clearance | Longest approval timeline; socially sensitive |

| Water Concession | CONAGUA | Water use rights | Scarcity constraints in northern mining regions |

| Surface Use / Ejido Agreement | Landowner / Ejido Assembly | Land access rights | Community opposition risk |

| State and Municipal Permits | State/Municipal Government | Construction, land use, operations | Jurisdictional fragmentation |

Each layer introduces its own timeline uncertainty and its own political exposure. Critically, a failure or delay at any single layer can suspend the entire development process, even when all other approvals are already in hand.

The Concession Ceiling

The mining concession, issued by the Secretaría de Economía, is the foundational legal instrument granting the right to extract minerals. Without it, nothing else matters. Since 2019, however, the practical availability of new concessions has contracted sharply. Successive federal administrations have used administrative inaction rather than formal legislative prohibition to achieve this effect, meaning no law explicitly bans new concessions, but the functional rate of issuance has declined to a level that amounts to a soft moratorium.

This asymmetry has a disproportionate impact on junior exploration companies and development-stage operators. Established producers with existing concession portfolios can continue advancing projects. New entrants, however, face a structurally constrained upstream entry point. According to permit delay reporting, these bottlenecks now threaten an estimated $4 billion in mining investment across the country.

SEMARNAT: The Longest and Least Predictable Stage

The Manifestación de Impacto Ambiental, or MIA, is Mexico's environmental impact assessment mechanism administered by SEMARNAT. Historically, this process carried predictable timelines. In recent years, however, review periods have extended significantly as the scope of required documentation has broadened, climate-linked environmental criteria have been layered into assessments, and community opposition has become a more frequent trigger for procedural complications.

The MIA process now represents the most time-intensive and outcome-uncertain stage of the non-oil mining permitting pathway. A project that clears all other approvals can still be suspended indefinitely at the SEMARNAT stage if additional studies are required, if the project is located near protected ecological areas, or if unresolved social conflict prompts administrative caution.

Water Rights: A Compounding Bottleneck

A separate water concession from CONAGUA is required for any operation with material water consumption, and this requirement intersects badly with physical geography. Mexico's most productive mining regions, particularly Sonora and Chihuahua in the north, face genuine and worsening water scarcity. CONAGUA's caution in granting new water rights in these watersheds reflects both hydrological reality and growing political sensitivity around water access.

The result is a compounding delay: operators may clear the SEMARNAT process only to find the CONAGUA application has become a new critical path item. In addition, Mexico mine strikes have further disrupted operational continuity in some of the same water-stressed northern regions where permit delays are most acute.

The Ejido Layer: Non-Governmental but Legally Binding

One of the least-understood features of Mexico's mining regulatory environment for international investors is the legal weight carried by ejido agreements. An ejido is a system of communal land tenure created through Mexico's post-revolutionary land reform, enshrined in Article 27 of the constitution. Mining operations that require surface access across ejido-held land cannot simply proceed with federal permits alone.

A surface-use agreement must be negotiated directly with the ejido assembly, a process that is legally distinct from, and not substituted by, any federal authorisation. Ejido negotiations are not a formality. They require genuine community engagement, often involve benefit-sharing arrangements, and can be withdrawn or contested if the community determines that the process was not conducted in good faith.

For projects in regions with significant indigenous community presence, Free, Prior and Informed Consent requirements add another legally enforceable consultation layer on top of the ejido process. Consequently, this mirrors challenges seen under British Columbia's mining claims framework, where indigenous land rights have similarly reshaped project timelines.

Commodity-Level Consequences: What the Permit Slowdown Means for Output

The permitting environment does not affect all commodities equally. Project geography, mining method, water intensity, and community sensitivity vary across Mexico's key mineral provinces, and these differences translate into differentiated permit risk profiles.

| Commodity | Mexico's Global Rank | Primary Mining Regions | Permit Risk Level | Clean Energy Transition Relevance |

|---|---|---|---|---|

| Silver | #1 globally | Sonora, Chihuahua, Zacatecas | High | Moderate (industrial and solar) |

| Copper | Top 10 globally | Sonora | Very High | Critical (electrification) |

| Gold | Significant producer | Sonora, Guerrero, Oaxaca | High | Low-moderate |

| Zinc | Major producer | Zacatecas, Chihuahua | Moderate-High | Moderate (batteries, galvanizing) |

| Lead | Co-produced with zinc | Zacatecas, Chihuahua | Moderate | Low |

Copper faces the sharpest strategic tension. Global demand for copper is accelerating as electrification programmes expand across North America, Europe, and Asia, yet Mexico's copper-rich Sonora corridor faces a dual constraint of CONAGUA water scarcity and elevated social conflict risk. This is precisely the commodity where the permit slowdown carries the largest strategic opportunity cost.

Silver, as a co-product of many polymetallic operations, is partially buffered because it is often extracted alongside base metals in projects that already hold existing concessions. However, the constraint on new concession access limits the pipeline of next-generation silver assets moving toward development.

Regional Fault Lines: Where Delays Are Most Concentrated

Geography matters enormously in understanding where permits slow non-oil mining in Mexico most severely.

- Sonora carries the highest overall risk concentration: copper and silver projects facing water scarcity-driven CONAGUA delays, community conflict risk in mining corridors, and intense investor scrutiny given the state's proximity to the US border and its visibility in North American supply chain discussions.

- Zacatecas and Chihuahua are historically prolific polymetallic silver, zinc, and lead districts where elevated social conflict indices are extending MIA timelines and adding unpredictability to project development schedules.

- Guerrero and Oaxaca are gold-endowed but politically complex jurisdictions where indigenous consultation requirements under FPIC frameworks are extending approval horizons to multi-year timescales, making financial modelling difficult for project developers.

Navigating the Permitting Pathway: A Practical Step-by-Step Framework

For operators working through Mexico's approval architecture, the sequencing and parallel-tracking of applications is critical to managing total timeline exposure. A well-structured approach generally follows this logic:

- Verify concession status before any other step. Determine whether an existing concession covers the target area or whether new concession access is needed. Given the current issuance environment, projects dependent on new concessions carry materially higher execution risk.

- Commission a comprehensive environmental baseline study early. This document forms the technical foundation of the MIA submission and is the element most commonly responsible for delays when it is underprepared.

- Submit the MIA to SEMARNAT with full technical, environmental, hydrological, and social components. Incomplete submissions trigger additional information requests that can add months to review timelines.

- Initiate the CONAGUA water concession application in parallel with the MIA process where possible, since both can proceed simultaneously and sequential processing creates avoidable delays.

- Begin ejido and surface-use negotiations early, recognising that these are legally independent from federal approvals and cannot be treated as a post-permit formality.

- Satisfy indigenous consultation requirements where applicable. These must be documented, genuine, and completed before formal approvals can be finalised in relevant jurisdictions.

- Pursue state and municipal approvals covering land-use change, construction licensing, and operational authorisations. These are often underweighted in project planning and can become critical path items if deprioritised.

- Integrate all approvals before commencing extraction. A partial approval set does not constitute legal operational authority.

Projects in regions with indigenous community presence that invest early in genuine, documented consultation processes consistently report shorter overall permitting timelines. The consultation phase is not a cost to minimise. It is a timeline variable to manage proactively.

The next major ASX story will hit our subscribers first

Structural Constraint or Temporary Friction? The Investment Calculus

The question that matters most for capital allocation decisions is whether the current permit environment represents a cyclical administrative backlog or a durable structural policy shift. Several indicators point toward the structural interpretation.

The constrained concession issuance rate has persisted across more than one federal administration, suggesting it reflects a broad policy posture rather than a specific government's preferences. Legislative reform proposals circulating in Mexico's congress would, if passed, further tighten environmental and social requirements for the sector. Environmental assessment criteria are being progressively aligned with international ESG frameworks, raising the compliance floor for all operators over time.

Against this, some analysts argue that Mexico's participation in North American supply chain discussions, particularly around copper as a critical mineral for electrification, creates diplomatic and economic pressure toward eventual mining permit reform. The current administration's infrastructure investment agenda also creates implicit demand for domestically sourced minerals, which may eventually translate into more constructive agency behaviour toward compliant projects.

The investment community has largely adapted to the structural interpretation. Capital allocation has shifted toward advancing existing permitted projects over greenfield exploration. Permitting timelines of 12 to 36 months are now treated as baseline assumptions rather than worst-case scenarios in project economics. Furthermore, specialised environmental and legal consultancies with multi-agency navigation expertise have become integral to project development budgets rather than optional advisory services.

The Strategic Opportunity Cost Mexico Is Accumulating

Every quarter in which permits slow non-oil mining in Mexico represents a compounding gap between the country's potential contribution to global clean energy mineral supply and its actual output trajectory. At a moment when copper demand projections linked to electrification infrastructure are reaching historic highs, and when silver's role in photovoltaic manufacturing is expanding, Mexico's administrative gridlock is functioning as an involuntary supply-side constraint on commodities the global economy urgently needs.

Jurisdictions that have successfully accelerated critical mineral permitting share a common architectural feature: they established clear statutory timelines, transparent approval criteria, and structured community engagement protocols at the front end of the process. For instance, Chile's lithium governance model demonstrates how structured state oversight combined with defined approval pathways can reduce investor uncertainty considerably.

Mexico's path to a more competitive permitting environment likely requires similar institutional architecture: streamlined coordination between Secretaría de Economía, SEMARNAT, and CONAGUA; statutory decision timeframes that prevent indefinite administrative suspension; and community benefit-sharing frameworks robust enough to reduce the social conflict risk that currently feeds back into regulatory delays. Until those structural reforms materialise, the permit stack will continue to define the ceiling on what Mexico's extraordinary geological endowment can actually deliver to global markets. For a broader picture of where Mexico's permitting landscape currently stands, the IISD's Mexico mining policy assessment provides useful foundational context on the regulatory trajectory.

Disclaimer: This article contains forward-looking analysis, scenario projections, and regulatory assessments that reflect current conditions and publicly available information as of mid-2026. It does not constitute investment advice. Readers should conduct independent due diligence before making any investment or project development decisions related to Mexico's mining sector.

Want to Know When Major Mineral Discoveries Hit the ASX Before the Market Reacts?

While Mexico's governance bottlenecks continue to constrain output from some of the world's most significant ore bodies, Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time — instantly identifying significant mineral discoveries across copper, silver, gold, and beyond, and translating complex data into actionable insights for investors at every level. Explore Discovery Alert's dedicated discoveries page to see how historic ASX discoveries have generated exceptional returns, and begin your 14-day free trial today to position yourself ahead of the broader market.