June 22, 2026

Global trade dynamics are experiencing unprecedented shifts as manufacturing nations reassess their strategic dependencies on critical industrial inputs. The interconnected nature of modern supply chains means that policy decisions in one region can create cascading effects across entire continental markets, fundamentally altering competitive landscapes for both producers and consumers. Furthermore, the implementation of chinese steel imports tariffs has become a pivotal tool for countries seeking to protect domestic industries while managing complex international relationships.

Understanding the Strategic Context Behind Mexico's Steel Import Tariff Implementation

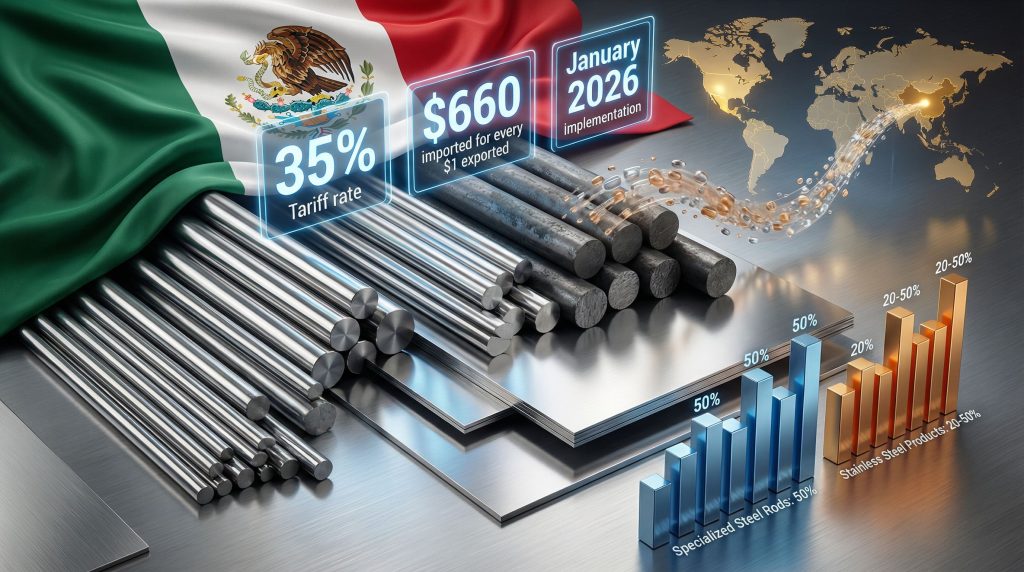

Mexico's implementation of comprehensive tariff structures on Chinese steel imports tariffs represents a calculated response to mounting trade imbalances that have reached critical thresholds. The country's new regulatory framework, effective January 1, 2026, establishes graduated protection mechanisms targeting non-free trade agreement nations, with China bearing the primary impact of these measures.

Consequently, these measures reflect broader concerns about economic sovereignty and the need to address structural dependencies that have developed over decades of trade liberalisation.

Trade Policy Framework – Mexico's Response to Non-FTA Import Dependencies

The trade imbalance between Mexico and China in steel products has reached extraordinary proportions. For every dollar Mexico exported in steel products to China in November 2025, it imported $660 worth of Chinese steel goods, creating one of the most lopsided bilateral trade relationships in the global metals sector. This dramatic disparity underscores the strategic vulnerability that Mexican policymakers sought to address through protective tariff measures.

Mexican steel exports to China, while showing impressive percentage growth of 590% year-over-year in November 2025 (rising from 19 metric tons in 2024 to 129 metric tons in 2025), remain negligible in absolute terms. Significantly, 92.9% of these exports consisted of metal scrap rather than finished steel products, highlighting Mexico's position as a raw material supplier rather than a value-added manufacturer in this relationship.

This scrap metal export pattern reveals deeper structural challenges. Despite ranking as the 15th largest global exporter of metal scrap, Mexico shipped only 1.2 million metric tons in 2024, representing less than 10% of the 14.9 million metric tons exported by the United States. This comparison demonstrates significant untapped potential in Mexico's secondary steel materials sector.

Regulatory Timeline – January 2026 Implementation and Market Preparation Phases

The federal government's decree reforming the General Import and Export Tax Law created a definitive regulatory timeline that market participants closely monitored throughout the final quarter of 2025. The January 1, 2026 effective date provided sufficient advance notice for both importers and domestic producers to adjust their strategies accordingly.

The timing of implementation coincided with seasonal patterns in steel demand, as construction and manufacturing sectors typically experience increased activity in the first quarter of calendar years. This strategic timing maximizes the protective effect during periods of peak domestic demand while allowing Mexican producers to capture market share during crucial seasonal cycles.

Sectoral Impact Assessment – Steel Industry Protection Mechanisms

The tariff structure demonstrates sophisticated sectoral analysis by Mexican trade policymakers. Rather than implementing uniform protection rates, the framework establishes differentiated tariffs based on strategic importance and manufacturing complexity:

- Critical Manufacturing Inputs: Specialized steel rods face the highest protection at 50% tariff rates

- Commodity Products: Standard steel products receive 35% protection

- Value-Added Materials: Stainless steel products encounter graduated rates from 20% to 50% depending on specifications

- Complementary Metals: Aluminum imports face 10% to 35% tariffs based on processing levels

This graduated approach balances domestic industry protection with downstream manufacturing competitiveness, recognizing that excessive input costs could undermine Mexico's broader industrial objectives.

When big ASX news breaks, our subscribers know first

How Do China's Steel Export Strategies Respond to Global Tariff Pressures?

Chinese steel exporters demonstrated remarkable strategic agility in the months preceding Mexico's tariff implementation, accelerating shipments and optimising product mix to maximise market penetration before regulatory barriers increased costs. However, these strategies must also adapt to the broader context of the us-china trade war and its implications for global trade patterns.

Export Volume Analysis – November 2025 Pre-Tariff Surge Patterns

Chinese steel exports to Mexico surged 16.9% in November 2025, reaching 85,076 metric tons compared to the previous year. This represented an absolute increase of 12,290 metric tons, occurring despite the existence of 21 active anti-dumping duties against Chinese steel products in the Mexican market.

The timing of this surge correlates directly with the announced January 2026 tariff implementation, suggesting sophisticated market intelligence and inventory management by Chinese exporters. This pre-emptive strategy allowed both Chinese suppliers and Mexican importers to establish inventory positions before tariff-inflated pricing took effect.

The volume increase occurred against a backdrop of intensifying trade defence measures, with Mexican authorities initiating 11 new anti-dumping investigations in 2025 alone, nearly doubling the annual rate from previous years. This regulatory pressure makes the continued export growth even more remarkable from a strategic perspective.

Product Category Prioritisation – Hot-Rolled Bars and Specialty Steel Focus

Chinese exporters concentrated their Mexican market strategy on high-value industrial inputs rather than commodity steel products. The product mix reveals deliberate targeting of Mexico's manufacturing ecosystem:

Primary Export Categories (November 2025):

- Hot-rolled bars: 18,850 metric tons (19.8% of total volume)

- Chromium-plated flat-rolled products: 11.8% of total imports

- Silicon electrical steel (transformer applications): 10.7% of volume

- CRNGO steel (motor/generator components): 6,733 metric tons

- Corrugated rebar (construction): 3,350 metric tons

The top three categories combined accounted for 42.3% of total imported volume, demonstrating concentrated focus on specialised applications. This strategy suggests Chinese exporters prioritised maintaining relationships with Mexican manufacturers requiring specific technical specifications over competing purely on commodity pricing.

Market Diversification Tactics – Beyond Traditional Export Destinations

The emphasis on transformer steel and motor components (CRNGO steel) indicates Chinese suppliers are positioning themselves as essential partners in Mexico's power generation and industrial machinery sectors. These products require precise metallurgical specifications and established supply relationships, creating higher barriers to supplier substitution compared to commodity steel products.

The focus on electrical steel applications aligns with Mexico's expanding renewable energy infrastructure and manufacturing modernisation initiatives. By securing market position in these growth sectors, Chinese exporters demonstrate long-term strategic thinking beyond immediate volume maximisation.

What Are the Key Tariff Rate Structures in Mexico's New Import Regulation?

Mexico's tariff architecture establishes a comprehensive protection framework that differentiates between product categories, processing complexity, and strategic importance to domestic manufacturing. In addition, these measures complement broader trends in tariffs impact investment markets globally.

| Product Category | Tariff Rate | Strategic Rationale |

|---|---|---|

| Standard Steel Products (ingots, flat-rolled, bars) | 35% | Baseline domestic industry protection |

| Specialised Steel Rods | 50% | Critical manufacturing input security |

| Stainless Steel (thickness-dependent) | 20-50% | Graduated protection by value addition |

| Aluminium Products (bars, profiles) | 10-35% | Complementary metal sector coverage |

Anti-Dumping Duty Integration – Existing 21 Active Cases Against Chinese Steel

The new tariff regime operates alongside an extensive anti-dumping duty framework that has been developing over multiple years. Twenty-one active anti-dumping cases against Chinese steel products create overlapping protection mechanisms that compound the effective import barriers facing Chinese exporters.

This dual-mechanism approach (tariffs plus anti-dumping duties) means that specific Chinese steel products may face combined duties significantly exceeding the stated tariff rates. Products subject to both regimes encounter cumulative protection that could reach or exceed 60-70% of import value in certain categories.

Investigation Pipeline – 11 New Cases Initiated in 2025 vs. Previous Years

The acceleration of anti-dumping investigations in 2025, with 11 new cases initiated compared to historical averages of approximately 5-6 cases annually, signals coordinated policy escalation. This doubling of investigation activity occurred simultaneously with tariff policy development, suggesting systematic preparation for comprehensive trade defence implementation.

These investigations follow established World Trade Organisation procedures, requiring evidence of material injury to domestic industry, dumping margin calculations, and causal links between unfair pricing and market damage. The increased investigation frequency indicates Mexican authorities identified substantial evidence supporting multiple simultaneous cases.

Transitional Mechanisms – Ministry of Economy Supply Chain Safeguards

Recognising the potential disruption to established supply chains, the tariff decree includes transitional provisions authorising the Ministry of Economy to implement competitive supply mechanisms for imports from non-FTA countries. This flexibility allows authorities to adjust protection levels if domestic manufacturing suffers from input cost increases or supply shortages.

These transitional mechanisms provide policy safety valves that can prevent excessive downstream cost impacts while maintaining protective intent. The Ministry retains discretionary authority to modify application in cases where domestic competitiveness faces unintended consequences.

How Does Mexico's Steel Trade Imbalance Reflect Broader Economic Dependencies?

The steel trade relationship between Mexico and China exemplifies broader patterns of resource dependency that characterise North-South economic relationships in the modern global economy. Moreover, understanding the tariffs economic implications helps contextualise these dependency patterns within current geopolitical frameworks.

Import-Export Ratio Analysis – $660 Imported for Every $1 Exported

The 660:1 import-to-export ratio in steel trade represents one of the most extreme bilateral trade imbalances in any major commodity sector. This disparity extends beyond simple competitive disadvantage to reflect fundamental differences in industrial development strategies and manufacturing capacity allocation.

Mexico's position as a net raw material exporter (primarily scrap metal) to China, combined with massive imports of finished and semi-finished steel products, mirrors colonial-era trade patterns where peripheral economies supplied raw materials while importing manufactured goods. This dynamic undermines Mexico's industrial sovereignty and value-addition capabilities.

Scrap Metal Export Potential – Mexico's 1.2Mt vs. US 14.9Mt Global Comparison

Mexico's scrap metal export performance of 1.2 million metric tons annually pales compared to the United States' 14.9 million metric tons, despite Mexico's substantial industrial base and growing urbanisation rates that should generate significant secondary steel materials.

This underperformance in scrap collection and export suggests inefficient recycling infrastructure and missed opportunities for circular economy development. Enhanced scrap metal recovery could provide Mexico with increased export revenue while reducing Chinese dependence on virgin steel imports.

Manufacturing Input Requirements – Transformer Steel and Motor Components

The concentration of Chinese imports in specialised categories like silicon electrical steel and CRNGO steel reveals Mexico's dependence on foreign suppliers for critical manufacturing inputs. These materials are essential for power generation equipment, industrial motors, and electrical infrastructure projects.

Domestic production capability in these specialised steel grades requires significant technological investment and metallurgical expertise. Mexico's current reliance on Chinese suppliers creates strategic vulnerability in sectors essential for energy security and industrial modernisation.

What Are the Industrial Value Chain Implications of These Tariff Changes?

The implementation of comprehensive chinese steel imports tariffs creates ripple effects throughout Mexico's interconnected manufacturing ecosystem, with consequences extending far beyond the steel sector itself. Furthermore, these changes reflect broader patterns in us economy tariff effects that influence regional trade dynamics.

Downstream Manufacturing Impact – Construction and Infrastructure Sectors

Construction companies utilising imported Chinese rebar and structural steel face immediate cost pressures as 35% tariffs increase input expenses. Infrastructure projects with locked-in contracts may experience margin compression, while new projects require price adjustments to accommodate higher steel costs.

The timing coincides with Mexico's ambitious infrastructure modernisation plans, including transportation upgrades and energy facility construction. Higher steel costs could slow project timelines or require government budget increases to maintain construction schedules.

Manufacturers of electrical equipment and industrial machinery face particularly acute challenges due to specialised steel requirements. Silicon electrical steel and CRNGO steel often lack readily available domestic alternatives, forcing companies to absorb higher costs or seek alternative suppliers from other countries.

Cost Pass-Through Mechanisms – Consumer Price and Competitiveness Effects

The China Chamber of Commerce and Technology Mexico expressed concerns that tariff measures would directly impact consumers and reduce competitiveness of value chains utilising steel inputs. The organisation specifically warned federal authorities about consequences for consumers and value chain efficiency.

Industries with thin profit margins and high steel content face difficult decisions between absorbing increased costs or passing them through to end customers. Automotive manufacturers, appliance producers, and construction equipment companies must balance competitive positioning against input cost inflation.

Supply Chain Reconfiguration – Alternative Sourcing Strategy Development

Mexican importers are actively evaluating alternative suppliers from India, Japan, South Korea, and Brazil to reduce dependence on Chinese sources. However, establishing new supplier relationships requires time for quality certification, logistics arrangements, and payment terms negotiation.

The transition costs associated with supplier diversification include additional inventory holding, quality testing, and potential production disruptions during changeover periods. These switching costs may temporarily offset tariff-driven price advantages from alternative sources.

How Do These Measures Compare to Global Steel Trade Protection Trends?

Mexico's tariff implementation aligns with broader global trends toward steel sector protectionism, particularly among developed economies seeking to preserve domestic industrial capacity. However, these measures must be evaluated within the context of specialised sectors such as asian ferro alloys trade.

US Section 232 Precedent – 50% Ad Valorem Rates on Chinese Steel

The United States established a precedent for aggressive steel protection through Section 232 national security tariffs, implementing 50% ad valorem rates on Chinese steel imports. Mexico's 35-50% tariff structure closely mirrors this American approach, suggesting policy coordination within the USMCA framework.

This parallel approach indicates North American alignment on steel trade policy, potentially creating a unified regional position against Chinese steel exports. Coordinated protection measures reduce the risk of trade diversion where restricted exports simply redirect to neighbouring markets.

China's Own 2026 Tariff Adjustments – Resource Import Facilitation Strategy

Simultaneously with Mexico's export restrictions, China implemented its own tariff adjustments in 2026, reducing import duties on various raw materials and intermediate goods. This policy shift suggests Chinese recognition that export-focused steel strategies face increasing global resistance.

China's pivot toward import facilitation for raw materials may signal broader strategic reorientation from export-dependent manufacturing toward domestic consumption and resource security. This shift could reduce competitive pressure on foreign steel markets while addressing China's own resource dependency concerns.

Multi-Lateral Trade Agreement Considerations – FTA vs. Non-FTA Treatment

Mexico's explicit differentiation between FTA and non-FTA suppliers creates incentives for trade agreement formation while penalising countries outside preferential trading arrangements. This approach leverages trade policy to advance broader diplomatic and economic integration objectives.

The distinction particularly benefits USMCA partners and other FTA signatories, potentially encouraging increased steel trade within preferential trading blocs. This regionalisation trend could fundamentally reshape global steel trade patterns over the medium term.

The next major ASX story will hit our subscribers first

What Are the Long-Term Strategic Outcomes for Mexico's Industrial Policy?

The tariff implementation represents more than trade protection, signalling a comprehensive strategy to reshape Mexico's position in global manufacturing value chains.

Domestic Steel Industry Development – Production Capacity Building Incentives

Higher import costs create market opportunities for domestic steel producers to expand capacity and upgrade technology. The protection framework provides price umbrellas that support investment in modernisation and expansion projects across Mexico's steel sector.

Government authorities may complement tariff protection with direct investment incentives, technology transfer programmes, and infrastructure development to maximise domestic industry benefits. The combination of market protection and positive incentives could accelerate industrial development beyond what either approach would achieve independently.

Regional Trade Relationship Shifts – USMCA Integration Opportunities

Preferential treatment for USMCA partners under the new tariff regime creates opportunities for deeper North American steel industry integration. Mexican manufacturers may increasingly source from United States and Canadian suppliers, strengthening regional supply chain resilience.

This regional integration could extend beyond steel to encompass broader manufacturing cooperation, with Mexico serving as a competitive production platform for North American markets while sourcing inputs from regional partners rather than Asian suppliers.

Economic Sovereignty Considerations – Critical Material Security Framework

The tariff policy reflects broader concerns about economic sovereignty and strategic material security. By reducing dependence on chinese steel imports tariffs, Mexico enhances its ability to maintain industrial capacity during potential trade disruptions or geopolitical tensions.

This sovereignty agenda extends beyond steel to encompass critical materials, technology, and industrial capabilities essential for national security and economic independence. The steel sector serves as a testing ground for broader industrial policy approaches.

Industry Stakeholder Response Analysis – Balancing Protection and Competition

The implementation of chinese steel imports tariffs has generated diverse reactions from industry stakeholders, reflecting the complex tradeoffs between protection and competition inherent in trade policy decisions.

China Chamber of Commerce Mexico Position – Value Chain Competitiveness Concerns

The China Chamber of Commerce and Technology Mexico articulated concerns about impacts on consumer welfare and value chain competitiveness. Their position emphasises that tariff measures could reduce efficiency in supply chains that depend on Chinese steel inputs for manufacturing operations.

The chamber's statement specifically urged federal authorities to carefully review measures that would have direct consequences for consumers while reducing competitiveness of value chains using these inputs in Mexican manufacturing. This perspective highlights tensions between protection and efficiency objectives.

Mexican Manufacturing Sector Adaptation – Input Cost Management Strategies

Mexican manufacturers face strategic choices in responding to higher steel input costs. Some companies are accelerating inventory accumulation of Chinese steel products purchased before tariff implementation, while others are actively evaluating alternative suppliers from non-Chinese sources.

The adaptation process varies significantly across industries, with companies requiring specialised steel grades facing greater challenges than those utilising commodity products. Electrical equipment manufacturers and automotive suppliers must balance cost increases against quality and delivery reliability considerations.

Government Policy Flexibility – Competitive Input Supply Mechanisms

The transitional provisions within the tariff decree demonstrate policymaker recognition that excessive protection could undermine broader industrial competitiveness objectives. The Ministry of Economy retains authority to implement supply mechanisms ensuring competitive input availability when market conditions warrant intervention.

This policy flexibility provides mechanisms to address unintended consequences while maintaining protective intent. The government can modify application in specific cases where downstream manufacturing faces severe competitiveness challenges due to input cost increases.

Implementation Monitoring and Future Policy Adjustments

The success of Mexico's tariff strategy depends on careful monitoring of market responses and willingness to adjust policies based on empirical outcomes rather than theoretical predictions. In addition, policymakers must consider recent economic data when evaluating policy effectiveness.

Market Response Tracking – Import Volume and Price Elasticity Measurement

Monitoring systems must track changes in import volumes, domestic production levels, and price relationships to assess tariff effectiveness. The 16.9% pre-implementation surge in Chinese imports provides a baseline for measuring post-tariff market adjustments.

Price elasticity measurements will reveal whether tariffs successfully redirect demand toward domestic suppliers or simply increase costs across the entire steel supply chain. These metrics determine whether protection achieves intended industrial development objectives or primarily redistributes costs.

Economic Impact Assessment – GDP and Employment Effect Evaluation

Comprehensive economic impact assessment requires tracking employment changes in both protected steel industries and downstream manufacturing sectors. Job creation in domestic steel production must be weighed against potential job losses in steel-intensive manufacturing industries facing higher input costs.

GDP effects depend on whether protection stimulates domestic investment and productivity growth sufficient to offset efficiency losses from higher steel costs. The net economic outcome determines long-term sustainability of the protection strategy.

Policy Refinement Pathways – Tariff Rate Review and Modification Protocols

Regular review mechanisms should evaluate whether initial tariff rates achieve desired protection levels without creating excessive downstream disruption. The graduated rate structure provides flexibility for fine-tuning protection intensity across different product categories.

Future modifications could include temporary duty suspensions for specific products facing supply shortages, graduated phase-outs as domestic capacity develops, or enhanced protection for emerging strategic materials. Policy evolution should reflect changing market conditions and industrial development progress.

Disclaimer: This analysis is based on publicly available information and market data as of January 2026. Trade policy outcomes depend on numerous variables including global economic conditions, technological changes, and policy responses by other nations. Readers should consult current official sources and professional advisors before making business or investment decisions based on this information. Forecasts and projections represent analytical estimates rather than guaranteed outcomes.

Looking to Capitalise on Shifting Global Trade Dynamics?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant mineral discoveries across the ASX, helping investors identify opportunities as global supply chains undergo major disruptions like Mexico's new steel tariffs. With manufacturing nations increasingly seeking domestic alternatives to traditional suppliers, mineral discoveries become critical for meeting industrial demand. Start your 30-day free trial today and position yourself ahead of these transformative market shifts.