August 1, 2026

The Hidden Architecture of a Global Supply Crisis

Few industrial materials carry as much systemic weight as aluminium. It underpins packaging, transportation, aerospace, construction, and consumer electronics simultaneously, making any meaningful supply disruption a cross-sectoral event rather than a contained commodity problem. When the source of that disruption sits at one of the world's most strategically sensitive maritime corridors, the consequences ripple outward far faster than most market participants anticipate.

That is precisely the dynamic now reshaping global aluminium markets in 2026. Middle East aluminium supply disruptions have exposed a structural vulnerability that existed long before any conflict began: the world's dependence on Gulf Cooperation Council smelters is deep, geographically concentrated, and poorly understood outside specialist commodity circles.

When big ASX news breaks, our subscribers know first

Why the GCC Is the World's Most Underappreciated Aluminium Pillar

The Gulf Cooperation Council collectively represents approximately 9% of global aluminium output, with production capacity concentrated across the UAE, Bahrain, and Qatar. What makes this concentration particularly consequential is the region's orientation: GCC smelters are not domestic consumption hubs. They are export engines, meaning any curtailment transmits almost immediately into international trade flows, unlike production disruptions in markets with large domestic absorption buffers.

Wood Mackenzie estimates that up to 6.8 million tonnes of GCC production sits within the risk envelope under sustained conflict scenarios. To contextualise that figure, it represents roughly one-third of China's entire annual aluminium output, and approximately twice the total annual production of Canada. Furthermore, the major aluminium producers operating outside the GCC region lack the spare capacity to absorb a shortfall of this magnitude in any realistic near-term timeframe.

The Strait of Hormuz: More Than an Oil Chokepoint

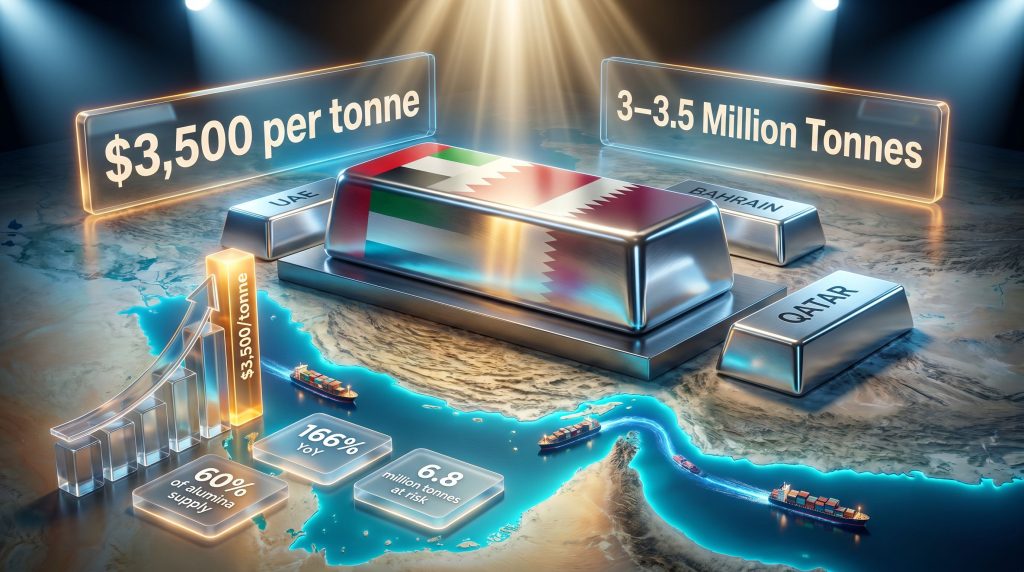

Public understanding of the Strait of Hormuz is filtered almost entirely through the lens of petroleum. What receives far less attention is the strait's parallel role as an aluminium supply artery. According to Wood Mackenzie analysis, up to 60% of the alumina supply required by GCC smelters transits through or adjacent to Hormuz-connected sea lanes.

This matters because aluminium production is a two-stage process. Bauxite ore is first refined into alumina, which is then smelted into primary aluminium metal. The bauxite supply chain feeding GCC smelters relies heavily on imported alumina at a scale insufficient to cover domestic needs. When maritime freight through the Hormuz corridor becomes constrained by conflict-related risk, smelters face a raw material starvation scenario that can idle capacity within weeks rather than months.

"The Strait of Hormuz is not merely an energy chokepoint. For the aluminium industry, it functions as a critical alumina supply corridor, and any sustained disruption to freight through this route can cascade into primary metal shortfalls across multiple continents within a matter of weeks."

Facility-Level Disruption: Quantifying the Production Shock

The current disruption pattern across GCC smelters is not uniform. Each facility faces a distinct combination of operational, logistical, and raw material challenges. According to recent analysis of supply risk in the region, the interaction between facility-level vulnerabilities and broader maritime disruption creates compounding risks that standard contingency models consistently underestimate.

| Producer | Country | Disruption Type | Estimated Capacity Impact |

|---|---|---|---|

| Emirates Global Aluminium (EGA) | UAE | Power plant damage and operational halts | Significant curtailment at Al Taweelah facility |

| Aluminium Bahrain (Alba) | Bahrain | Alumina shortage-driven curtailment | Approximately 19% of total capacity offline |

| Qatalum | Qatar | Reduced throughput | Operating at roughly 60% of nameplate capacity |

| Ma'aden | Saudi Arabia | Emergency supply role | Diverting alumina to support neighbouring smelters |

Combined, current disruptions have removed an estimated 2.3 to 3 million tonnes of GCC aluminium capacity from the market. Wood Mackenzie's 2026 scenario modelling projects that sustained disruption could push cumulative lost output to 3 to 3.5 million tonnes across the full year.

How a 3 Million Tonne Loss Moves Global Markets

To appreciate the market significance of this volume, consider that global aluminium consumption in 2026 is projected in the range of 70 million tonnes. A 3 to 3.5 million tonne supply removal represents approximately 4 to 5% of total world demand disappearing from available supply simultaneously, with no pre-positioned alternative to absorb the shortfall.

The London Metal Exchange aluminium price response has been measurable. Prices approached $3,500 per tonne as market tightness intensified, a level that compresses margins across the downstream sector and forces cost pass-through decisions at every point in the value chain. For comparison, previous supply shock events such as the Rusal sanctions in 2018 demonstrated that even partial supply removals from major producers can trigger sustained price dislocations that outlast the original trigger by many months.

A critical and often overlooked dimension is recovery asymmetry. Even when a geopolitical trigger is resolved, smelter production systems, alumina supply contracts, and freight logistics require six to twelve months to fully normalise. The market cannot simply switch back on.

Regional Stress Testing: Where the Pressure Is Landing

North America: From Modest Recovery to Acute Vulnerability

North America entered 2026 on a stabilising trajectory. The Aluminium Association's most recent Situation Report recorded a 0.8% increase in aluminium demand in 2025, supported by a stronger second half of the year after a sluggish start. That foundation is now being stress-tested.

S&P Global analysis has described the situation facing North American buyers as a potential supply crisis, as GCC metal that would normally flow into US import channels is either curtailed at source or diverted through constrained shipping routes. The US market's reliance on GCC aluminium creates acute near-term vulnerability that existing domestic smelting capacity cannot readily offset.

US aluminium tariffs compound the problem considerably. Existing US trade measures on aluminium imports interact with conflict-driven supply shortfalls to amplify cost pressures from multiple directions simultaneously, leaving downstream manufacturers caught between reduced availability and elevated input costs.

The consumer dimension is becoming visible at the brand level. Monster Beverage Corporation has signalled incremental price increases through 2026, attributing the decision in part to higher aluminium costs and freight expenses driven by both tariff policy and geopolitical supply disruptions. The company has indicated confidence that consumer demand for energy drinks will remain resilient despite the pricing adjustment, drawing on prior experience with price increases.

Europe: Premium Escalation and Strategic Inventory Drawdown

European markets are expected to bear disproportionate impact from GCC supply losses, manifesting primarily through tightening regional premiums on aluminium purchases. Import-dependent downstream sectors including packaging and automotive face dual pressure: rising metal costs and freight delays that extend lead times and compress planning horizons.

European buyers are managing near-term availability gaps through strategic inventory drawdown, a response that defers but does not eliminate procurement pressure. The medium-term structural response increasingly centres on supply chain geographic diversification to reduce the region's concentration exposure to GCC production. In addition, the broader trend toward low-carbon metals demand is accelerating investment in alternative sourcing strategies across the continent.

Asia-Pacific: Front-Loading and Procurement Realignment

Japan's response to anticipated tightening has been measurable in import data. Primary aluminium imports rose 6.6% year-on-year and 16% month-on-month to 89,497 tonnes in March 2026, according to Japan's Finance Ministry. This pattern reflects front-loading behaviour by Japanese buyers seeking to build inventory buffers ahead of expected further tightening.

Automotive demand recovery has supported import volumes, particularly in flat-rolled and extruded aluminium products, while the construction sector has remained soft due to lower housing activity. South Korea faces comparable exposure as another major import-dependent aluminium economy, with procurement strategies undergoing similar recalibration.

India: Consumer-Visible Disruption

The cascade from GCC supply disruption to Indian retail shelves has become one of the more striking illustrations of how upstream commodity shocks travel downstream. Coca-Cola's Diet Coke product faced supply shortages in India triggered by disruptions in aluminium can availability linked to Gulf supply chain constraints. The product returned to market in glass bottle format, accompanied by significantly higher prices.

Retailers have indicated that pricing and supply conditions may remain volatile until aluminium availability and shipping routes connected to the Gulf region stabilise more fully. This consumer-level visibility of an industrial commodity disruption is unusual and signals the depth of the supply chain penetration.

China's Strategic Pivot: Processing Over Primary Metal

China's response to the Gulf supply gap has taken a form that is reshaping trade flow architecture in ways that deserve careful attention. Rather than exporting primary aluminium ingots, Chinese producers and traders have pivoted decisively toward semi-fabricated and processed aluminium products, capturing the value uplift created by price differentials generated by the Hormuz disruption.

In April 2026, China exported 15,565 tonnes of aluminium stranded wire, cables, and related products, representing a 166% year-on-year increase and approximately 95% above March 2026 levels. This is not a marginal adjustment. It reflects a deliberate strategic response by Chinese market participants to arbitrage the Gulf supply gap through downstream value addition.

| Export Category | Pre-Conflict Baseline | April 2026 Volume | Year-on-Year Change |

|---|---|---|---|

| Aluminium stranded wire and cables | Historical average | 15,565 tonnes | +166% YoY |

| Semi-fabricated products (broader category) | Baseline period | Escalating | Significant uplift |

Whether this represents a temporary arbitrage response or a structural shift in Chinese export strategy carries significant implications. If destination markets respond with anti-dumping or safeguard measures, the partial offset that Chinese processed products provide to global supply chains could be further constrained. Australia's decision to extend anti-dumping duties on Malaysian mill-finish aluminium extrusions, effective from June 3, 2026, offers a relevant precedent for how import-sensitive markets respond to surging processed product volumes.

Downstream Sector Scenarios: Winners, Losers, and Adapters

Aluminium Packaging: Confronting a 3.5 Million Tonne Risk

Global aluminium packaging consumption reached approximately 16.70 million tonnes in 2025 and is projected to approach 17.16 million tonnes in 2026. Against that demand backdrop, the conflict-driven supply risk of 3 to 3.5 million tonnes represents a potential shortfall equivalent to roughly 20% of annual packaging-grade aluminium demand, a figure that cannot be absorbed quietly.

The geographic exposure is broad, with packaging industries across Asia, Europe, the United States, and Brazil all facing mounting pressure. Three strategic responses are emerging across the sector:

- Procurement diversification to reduce single-region dependency on GCC-sourced aluminium.

- Accelerated recycled aluminium integration to substitute secondary metal where primary supply is constrained.

- Packaging format substitution toward glass, plastic, or alternative materials where the economics support a temporary or permanent switch.

Aerospace and Automotive: Elevated Demand Meets Tightening Supply

Healthy air travel recovery and rising aircraft production are sustaining strong demand for aluminium alloys used in fuselage and wing applications. The electric vehicle sector continues to drive growing requirements for lightweight aluminium platforms. Both sectors are encountering a tightening supply environment simultaneously, creating a demand-supply tension that is likely to persist through the second half of 2026.

Companies such as Constellium SE and Ryerson Holding Corporation are drawing investor attention as elevated aluminium prices remain a structural feature of the current market environment, with strong downstream demand providing partial support for margins even as input costs escalate.

Recycling: The Structural Beneficiary

Supply disruptions historically improve the relative economics of recycled aluminium by widening the cost differential between primary and secondary metal. The current disruption cycle is following that pattern. Furthermore, recycling capacity expansion across the sector is gaining momentum as the economics of secondary metal become increasingly compelling relative to constrained primary supply.

Novelis's Bay Minette recycling and rolling facility in Alabama is progressing through commissioning at a strategically well-timed moment, positioned to capture demand that cannot be met through primary supply channels. The Aluminium Association's data shows that scrap and flat-rolled product momentum was already driving demand resilience in the second half of 2025, a trajectory being reinforced rather than interrupted by the GCC supply shock.

The next major ASX story will hit our subscribers first

Corporate Performance: Reading the Bifurcation

The divergence in corporate results across the aluminium sector reflects a bifurcated market landscape. Scale, supply chain diversification, and recycling capability are the primary differentiators between companies absorbing disruption and those experiencing meaningful margin compression.

| Company | Key Metric | Performance | Strategic Signal |

|---|---|---|---|

| Shyam Metalics and Energy | Profit after tax (Q4 FY26) | +42% YoY to INR 3.12 billion | INR 27 billion expansion plan including aluminium projects |

| Shyam Metalics and Energy | Quarterly revenue | +27% to INR 52.4 billion | EBITDA +33% |

| Novelis | FY26 net loss | USD 15 million (vs. USD 683 million prior year) | Oswego restart ahead of schedule; Bay Minette commissioning ongoing |

| Novelis | FRP shipments | -5% to 3.56 million tonnes | Fire-related disruption; long-term demand outlook maintained as positive |

| Maan Aluminium | Net sales (Q3 FY26) | Approximately INR 1.52 billion | PAT roughly 27% below four-quarter average; stock up 580% over five years |

Novelis's experience is instructive. The company absorbed an estimated USD 104 million Adjusted EBITDA impact from two separate fires at its Oswego, New York facility in September and November 2025, with approximately 145 kilotonnes of lost shipments resulting from those incidents. Despite this, the Oswego hot mill restart is now progressing ahead of schedule, and long-term positioning around low-carbon aluminium demand remains central to the company's strategic narrative.

Shyam Metalics and Energy presents a contrasting picture, with profit growth, revenue expansion, and a substantial forward capital commitment signalling confidence in aluminium sector fundamentals despite near-term market turbulence. The MBK Partners acquisition of Altemira Holdings at approximately YEN 117.5 billion (USD 760 million) further reflects confidence in long-term structural demand for aluminium packaging across Asia.

Three Forward Scenarios for Aluminium Markets Through 2026

Scenario 1: Rapid Resolution (Low Probability)

GCC smelters return to full operations within 60 to 90 days. Alumina supply chains through Hormuz normalise, freight premiums recede, and aluminium prices correct from near-$3,500 per tonne levels. However, even under this optimistic pathway, the structural risks facing western supply remain unaddressed. The 6 to 12 month normalisation lag means near-term tightness persists regardless of geopolitical resolution speed.

Scenario 2: Prolonged Disruption with Managed Adaptation (Base Case)

Conflict continues through the second half of 2026. GCC output remains partially curtailed. Chinese processed product exports continue to partially offset primary metal shortfalls whilst creating new trade policy friction in destination markets. Downstream sectors accelerate recycling integration and procurement diversification. Consequently, aluminium prices remain elevated, and consumer-facing price increases become normalised across multiple product categories.

Scenario 3: Escalation and Extended Supply Crisis (Tail Risk)

Further facility damage or sustained Hormuz disruption activates a larger portion of the 6.8 million tonne at-risk production estimate identified by Wood Mackenzie. Global aluminium deficit deepens materially. LME prices breach $3,500 per tonne on a sustained basis. North American and European buyers face acute inventory depletion. In this scenario, strategic stockpiling, emergency trade policy interventions, and accelerated domestic capacity investment programmes become necessary responses rather than optional strategies.

Key Takeaways for Markets, Industries, and Investors

- Middle East aluminium supply disruptions are operating simultaneously across multiple dimensions: production curtailments, raw material sourcing constraints, freight disruption, and price escalation are all compounding at once.

- The GCC's structural role as a global aluminium supplier has been exposed as a systemic concentration risk that predates the current conflict and will persist after it ends unless supply chain diversification accelerates.

- Recycled aluminium and domestic capacity investment are the two most actionable strategic responses available to markets seeking to reduce exposure to GCC supply concentration.

- Corporate performance is bifurcating visibly, with scale players possessing diversified supply chains and recycling capabilities demonstrably outperforming import-dependent operators facing margin compression.

- China's shift toward processed and semi-fabricated aluminium exports is partially offsetting primary metal shortfalls but carries its own trade policy risks as destination markets evaluate anti-dumping responses.

- Even in optimistic resolution scenarios, the six to twelve month recovery lag built into aluminium production systems means near-term tightness will remain a structural feature of the market through the remainder of 2026.

This article is intended for informational purposes only and does not constitute financial or investment advice. Forecasts, scenario projections, and production estimates referenced herein are derived from third-party industry sources including Wood Mackenzie, the Aluminium Association, S&P Global, and Japan's Finance Ministry, and are subject to revision as market conditions evolve. Readers should conduct independent research before making investment or procurement decisions.

Want to Capitalise on the Next Major Commodity Discovery Before the Broader Market Moves?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries — instantly transforming complex commodity data into actionable investment insights across aluminium, bauxite, and more than 30 other commodities. Explore historic examples of exceptional discovery returns and begin your 14-day free trial today to position yourself ahead of the market.