July 31, 2026

Middle East conflict impact on sulphur and ammonia markets creates unprecedented vulnerabilities for industrial chemical supply chains when geopolitical tensions disrupt established production networks. The concentration of critical manufacturing capacity within specific geographic regions creates systemic risks that extend far beyond immediate conflict zones, affecting everything from agricultural productivity to advanced manufacturing processes across multiple continents. Furthermore, these disruptions highlight the interconnected nature of global chemical dependencies and their far-reaching economic implications.

Regional Chemical Dependencies in Industrial Markets

The global chemical industry's reliance on Middle Eastern production facilities creates cascading vulnerabilities that ripple through diverse industrial sectors. This dependency stems from the region's abundant natural gas reserves and established petrochemical infrastructure, which together form the backbone of worldwide sulphur and ammonia production networks. Consequently, any disruption to these facilities can have immediate global ramifications.

Middle Eastern facilities contribute approximately 45-50% of globally traded sulphur volumes, with major production centers concentrated in Saudi Arabia, Qatar, and the UAE. These facilities primarily source sulphur as a byproduct of natural gas processing and oil refining operations, creating an integrated production ecosystem that can be disrupted when geopolitical tensions affect regional operations. Moreover, Saudi Arabia dynamics play a crucial role in determining global supply stability.

The ammonia production landscape shows similar concentration patterns, with Gulf region facilities accounting for roughly 35% of global export capacity. This dependency becomes particularly critical given ammonia's role as both a direct fertilizer input and a precursor chemical for nitrogen-based compound production. Additionally, understanding oil price rally insights helps explain the economic pressures affecting these integrated facilities.

Key regional production facilities include:

- Saudi Arabia: Ras Tanura complex producing 2.1 million tonnes annually

- Qatar: Multiple petrochemical facilities with combined capacity exceeding 1.8 million tonnes

- UAE: Distributed production network across Abu Dhabi and Dubai regions

- Kuwait: Integrated refinery operations producing both sulphur and ammonia derivatives

The interdependency between these facilities means that disruptions affecting transportation corridors, port operations, or production scheduling can simultaneously impact multiple chemical supply chains across different commodity categories.

When big ASX news breaks, our subscribers know first

Industrial Sectors Under Supply Chain Stress

Mining Operations and Acid Dependencies

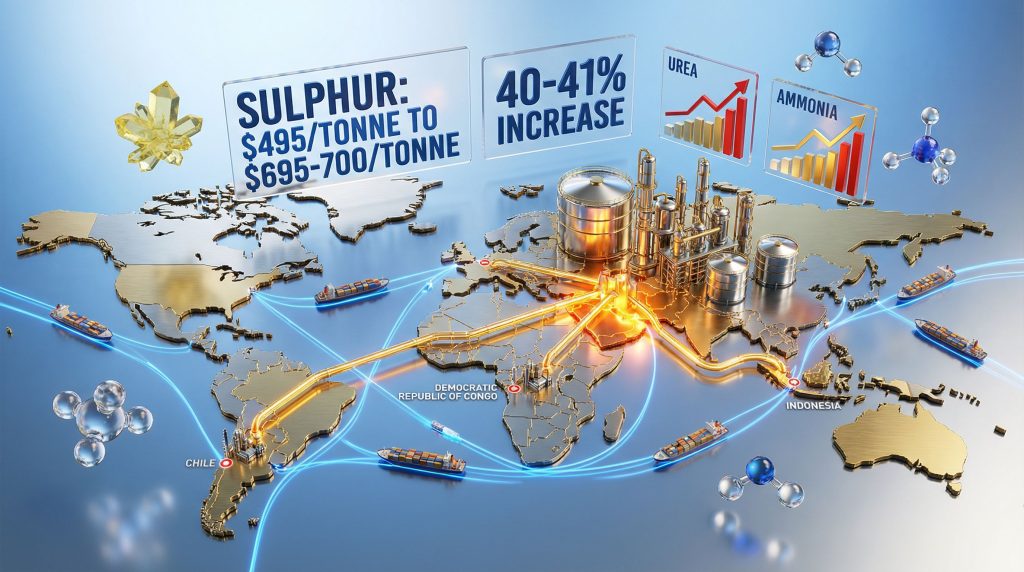

Copper and nickel extraction operations worldwide demonstrate extreme vulnerability to sulphur supply disruptions due to their reliance on sulphuric acid leaching processes. Major mining regions including Chile's Atacama Desert, the Democratic Republic of Congo's copper belt, and Indonesia's nickel laterite deposits depend heavily on consistent acid supplies for ore processing operations.

The cost structure analysis reveals that sulphur represents 15-25% of total acid production costs for mining operations, making price volatility a significant operational concern. When Middle East conflict impact on sulphur and ammonia markets drives prices higher, mining companies face compressed margins and potential production curtailments.

Alternative sourcing challenges compound these difficulties, as limited refinery capacity outside the Gulf region constrains rapid supply chain pivoting. Canadian oil sands operations and Russian refineries provide alternative sources, but their combined capacity cannot immediately replace Middle Eastern output during crisis periods. According to industry analysis, this capacity limitation creates significant market pressure during supply disruptions.

Mining companies have responded by implementing several adaptation strategies:

- Acid recycling investments: Accelerated development of closed-loop sulphuric acid recovery systems

- Long-term contract restructuring: Negotiating more flexible supply agreements with regional acid producers

- Strategic inventory expansion: Increasing on-site storage capacity for both sulphur and finished acid

- Process optimization: Implementing more efficient leaching technologies to reduce acid consumption per unit of metal produced

Agricultural Input Manufacturing Networks

Nitrogen fertilizer production faces dual pressures from restricted ammonia availability and elevated natural gas feedstock costs when regional conflicts disrupt Middle Eastern operations. The manufacturing process for urea, ammonium nitrate, and other nitrogen compounds requires consistent ammonia inputs, creating supply chain vulnerabilities that affect global food production systems.

Seasonal demand patterns amplify these vulnerabilities, as Northern Hemisphere spring planting cycles create concentrated periods of elevated fertilizer demand. When supply disruptions coincide with peak application seasons, the impacts on agricultural productivity become magnified across major grain-producing regions. The critical materials supply situation further complicates these agricultural dependencies.

Regional food security implications extend beyond immediate supply constraints, particularly affecting import-dependent markets in South Asia and Sub-Saharan Africa. These regions typically rely on competitively priced Middle Eastern fertilizer exports, making them vulnerable to both supply shortages and price volatility during geopolitical crises.

Quantitative Impacts on Global Pricing Mechanisms

Market pricing data reveals substantial volatility when Middle East conflict impact on sulphur and ammonia markets disrupts normal trading patterns. Furthermore, these price movements demonstrate the interconnected nature of global chemical markets and their sensitivity to regional disruptions.

| Chemical Product | Pre-Crisis Baseline | Peak Crisis Pricing | Percentage Increase | Recovery Timeline |

|---|---|---|---|---|

| Sulphur (FOB Middle East) | $495/tonne | $695-700/tonne | 40-41% | 6-8 months |

| Urea (FOB Middle East) | $485/tonne | $665/tonne | 37% | 4-6 months |

| Ammonia (Regional Variants) | Variable baseline | 25-35% premium | 25-35% | 3-5 months |

How Do Freight and Insurance Costs Amplify Market Pressures?

Maritime insurance premiums experience dramatic increases during regional conflicts, with Gulf-origin chemical shipments seeing insurance cost rises of 118% above baseline levels. These additional costs compound the direct pricing impacts on chemical commodities, creating multiple layers of financial pressure for industrial buyers.

Alternative routing costs add substantial expense when primary shipping lanes become compromised or perceived as high-risk. Longer shipping distances typically add $45-65 per tonne in transportation expenses, while alternative ports may lack specialized handling equipment for chemical cargoes.

Port congestion delays at secondary loading facilities create additional complications, with average delays extending 15-20 days beyond normal scheduling expectations. These delays disrupt just-in-time delivery systems and force buyers to maintain larger inventory buffers. The broader implications of tariffs impact markets further complicate these transportation cost structures.

Production Shutdowns and Market Distortions

Inventory Accumulation Dynamics

When export operations face restrictions due to regional conflicts, daily stockpile growth at Middle Eastern production facilities can reach approximately 40,000 tonnes across all affected chemical products. This accumulation creates storage capacity pressures that can force temporary production curtailments if export channels remain blocked.

Storage capacity constraints become critical factors in maintaining production continuity, with regional terminals typically approaching 85-90% capacity utilization within 60-90 days of export restrictions. These constraints create operational pressures that can affect production decisions across multiple facility networks.

Quality degradation risks emerge during extended storage periods, particularly for sulphur products that can experience specification changes affecting their suitability for industrial applications. This technical factor adds complexity to inventory management decisions during crisis periods.

Production Facility Operational Status

Major production facilities experience varying degrees of operational impact during regional conflicts. However, the scale of these disruptions varies significantly based on facility location and operational flexibility.

Critical Infrastructure Assessment: The Ras Tanura complex represents the most significant single-point vulnerability in global sulphur supply chains, with its complete operational suspension affecting 2.1 million tonnes of annual capacity. This facility's strategic importance extends beyond its direct output, as it serves as a logistics hub for multiple smaller production units throughout the region.

Qatar Petrochemical facilities typically maintain operations at reduced capacity levels, often around 60% of normal output due to logistics constraints rather than production limitations. These facilities face particular challenges in coordinating export scheduling when regional shipping patterns become disrupted.

UAE production networks generally demonstrate greater operational resilience, maintaining approximately 75% output levels with restricted export capabilities. The distributed nature of UAE facilities provides some flexibility in managing production adjustments during crisis periods.

Strategic Adaptations by Industrial Buyers

Supply Chain Diversification Initiatives

Alternative sourcing geography has become a critical strategic priority for industrial buyers exposed to Middle Eastern supply dependencies. Increased procurement from Canadian oil sands operations and Russian refineries represents the primary diversification pathway, though capacity limitations constrain the speed of this transition. Nevertheless, companies recognise the importance of reducing geographic concentration risks.

Contract restructuring activities have accelerated across the industry, with force majeure clauses activated across approximately 60% of long-term supply agreements during recent crisis periods. These contractual mechanisms provide legal protection but create operational challenges in securing alternative supplies. Additionally, understanding US tariffs and inflation impacts helps companies evaluate alternative sourcing strategies.

Inventory management shifts reflect changing risk assessments, with industrial consumers increasing strategic stockpile targets by 25-40% compared to pre-crisis levels. This shift represents a fundamental change in working capital allocation strategies across chemical-intensive industries.

What Technology Modifications Are Companies Implementing?

Industrial adaptation strategies extend beyond supply chain adjustments to include fundamental process modifications. These technological shifts represent long-term structural changes in how companies approach chemical dependency management.

- Closed-loop recovery systems: Mining operations investing in sulphuric acid recycling technologies to reduce external dependencies

- Alternative feedstock research: Fertilizer manufacturers exploring bio-based nitrogen production pathways to reduce fossil fuel dependencies

- Regional production capacity: Accelerated development of non-Middle Eastern chemical manufacturing hubs in North America and Europe

- Process efficiency improvements: Implementation of advanced catalyst systems and reaction optimization to reduce chemical input requirements

Market Structure Evolution and Permanent Changes

Long-term Supply Chain Reconfiguration

Geographic redistribution of chemical supply sources appears likely over a 3-5 year horizon, with potential 15-20% reduction in Middle Eastern market share as buyers prioritise supply security over cost optimisation. This structural shift represents a fundamental change in global chemical trade patterns.

Investment flow redirection toward North American and European production capacity reflects strategic decisions to reduce geographic concentration risks. New facility development in these regions benefits from both supply security considerations and proximity to major industrial consumers. Consequently, the traditional Middle Eastern dominance in chemical markets faces unprecedented challenges.

Strategic reserve policies emerge as governmental responses to supply chain vulnerabilities, with import-dependent economies developing stockpiling programs for critical chemical inputs. These policies create additional demand layers that can influence long-term market dynamics.

Pricing Mechanism Transformation

Risk premium incorporation becomes a permanent feature of Middle Eastern chemical pricing, with structural 8-12% price premiums expected to persist even after immediate crisis resolution. This premium reflects market participants' recognition of ongoing geopolitical risks.

Alternative benchmark development gains momentum as regional pricing indices challenge traditional Gulf-centric assessment methodologies. European and North American price discovery mechanisms develop greater influence in global market pricing. Furthermore, fertilizer market analysis suggests these alternative benchmarks are gaining institutional acceptance.

Contract term modifications become industry standard, with shorter-duration agreements featuring enhanced flexibility clauses replacing traditional long-term fixed-price structures. This evolution reflects buyers' preferences for operational adaptability over price certainty.

The next major ASX story will hit our subscribers first

Macroeconomic Stress Indicators

Downstream Industry Performance Impacts

Global copper production faces projected 3-5% reduction in output during peak crisis periods due to sulphuric acid leaching constraints. This impact cascades through construction, electronics, and renewable energy sectors that depend on steady copper supplies.

Agricultural yield forecasts indicate potential 2-4% reduction in nitrogen-dependent crop productivity for affected growing seasons. These impacts are most severe in regions with limited fertilizer stockpiling capacity or restricted access to alternative suppliers.

Industrial chemical margins experience compression of 15-25% across sulphur-dependent manufacturing processes, affecting sectors including paper production, pharmaceuticals, and specialty chemical manufacturing. However, companies with diversified supply chains demonstrate greater resilience during crisis periods.

Regional Economic Vulnerability

Several regions demonstrate particular vulnerability to Middle East chemical supply disruptions. These vulnerabilities reflect both geographic dependencies and limited alternative sourcing capabilities.

- China's industrial output: Manufacturing PMI declining due to chemical input shortages affecting production scheduling

- Sub-Saharan Africa mining sector: Production curtailments affecting 12-15% of regional copper output due to acid supply constraints

- European fertilizer distribution: Supply chain disruptions impacting 25% of spring application schedules in major agricultural regions

Market Recovery Scenarios and Probability Assessment

Short-term Resolution Pathway (3-6 months)

Rapid price normalisation typically follows crisis resolution, with 60-70% price correction occurring within 90 days of shipping lane reopening and normal export operations resuming. This correction reflects the release of accumulated inventory and restoration of normal supply flows.

Inventory liquidation phases create temporary oversupply conditions as accumulated stocks enter markets simultaneously. This dynamic can drive prices below long-term equilibrium levels before normal market balances restore. Moreover, the speed of normalisation depends on the extent of accumulated stockpiles during the crisis period.

Logistics infrastructure restoration proceeds gradually, with shipping schedules and insurance rates returning to pre-crisis levels over 3-6 month periods. Port capacity and specialised handling equipment requirements influence the speed of this normalisation process.

Extended Disruption Scenario (6-12 months)

Permanent supply chain restructuring accelerates when crises extend beyond short-term disruption periods. Alternative production regions receive accelerated investment and development support as buyers seek long-term supply security. Consequently, the traditional Middle Eastern market structure faces fundamental challenges.

Technology adoption acceleration occurs as industrial processes adapt to sustained higher input costs through efficiency improvements and alternative production methodologies. These adaptations can reduce future dependence on traditional supply sources.

Market consolidation patterns emerge as smaller chemical consumers face unsustainable cost structures during extended crisis periods. This consolidation can permanently alter demand patterns and competitive dynamics in chemical-intensive industries.

The current analysis of Middle East conflict impact on sulphur and ammonia markets demonstrates the interconnected nature of global chemical supply chains and their vulnerability to geographic concentration risks. Industrial stakeholders must balance immediate operational requirements with long-term strategic positioning as market structures continue evolving in response to ongoing geopolitical uncertainties.

Organisations with significant exposure to these supply chains should evaluate comprehensive risk management strategies that encompass both tactical supply adjustments and strategic investment decisions. The emerging market dynamics suggest that operational flexibility and supply chain diversification will become increasingly important competitive advantages in chemical-intensive industries.

Disclaimer: This analysis is based on historical market patterns and current industry trends. Actual market developments may vary significantly due to changing geopolitical conditions, technological innovations, or unexpected supply-demand shifts. Readers should conduct their own research and consult with industry experts before making investment or operational decisions based on this information.

Are You Considering Industrial Chemical Investments Amid Supply Chain Volatility?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, including companies involved in critical industrial chemical supply chains and mining operations requiring sulphur-dependent processes. Start your 14-day free trial today and gain actionable insights into mining and chemical sector opportunities before broader markets recognise their potential.