May 22, 2026

The Logistics Trap: How a Transit Crisis Is Exposing Aluminium's Hidden Vulnerability

Global commodity markets are built on assumptions. Assumptions about shipping lanes remaining open, insurance premiums staying manageable, and feedstock arriving on schedule. For decades, the aluminium industry operated under a relatively stable set of these assumptions, particularly in the Gulf region. The Middle East crisis and bauxite alumina market dynamics have not simply disrupted trade routes — they have exposed the structural fragility baked into one of the world's most capital-intensive industrial ecosystems.

Understanding the full scope of how the Middle East crisis and bauxite alumina market dynamics are now intertwined requires moving beyond headline price movements and examining the mechanics of what is actually breaking down, and why it matters well beyond the region itself.

When big ASX news breaks, our subscribers know first

The Gulf's Structural Blind Spot: Smelting Power Without Upstream Security

The Gulf aluminium sector presents a paradox that is rarely discussed in mainstream commodity analysis. The UAE and Bahrain, two of the region's most prominent producers, have built world-class smelting infrastructure over the past two decades. Yet neither operates any meaningful upstream mining or refining capacity. Every tonne of bauxite and virtually every tonne of alumina that feeds these smelters arrives by ship, primarily from West Africa and Australia.

This creates what analysts describe as a structurally exposed supply model: significant smelting output underpinned by near-total import dependency. The Gulf accounts for roughly 9% of global aluminium smelting capacity, a material enough share that operational disruptions ripple through global supply and pricing dynamics. When freight corridors come under pressure, that 9% becomes a systemic lever.

The critical insight here is that the current crisis did not create this vulnerability — it simply made it impossible to ignore. Gulf smelters have historically operated with lean alumina inventory buffers, a rational efficiency choice under stable conditions that becomes an acute operational liability the moment shipping reliability deteriorates. Even a disruption lasting only a few weeks can compress inventory positions to uncomfortable levels, forcing producers to choose between accelerated procurement at elevated cost or controlled production curtailments.

Furthermore, bauxite production leaders such as Guinea and Australia have continued mining at pace — the bottleneck is not at the mine but in the transit corridors connecting origin to consumer.

Industry analysts have noted that the Gulf's upstream dependency is not a recent development but a structural design choice embedded in the region's industrial model, one that prioritised smelting efficiency and low-cost energy over feedstock security. The current environment is effectively billing for that choice.

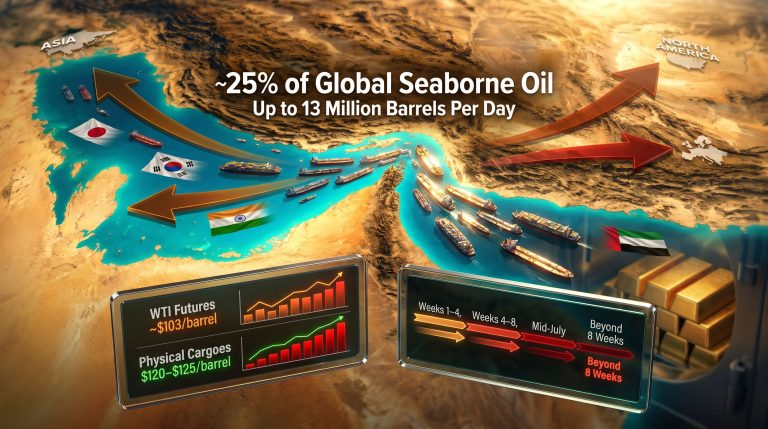

How the Strait of Hormuz Became a Bauxite Chokepoint

Why Transit Infrastructure Matters More Than Mining Output

The Strait of Hormuz is most commonly discussed in the context of oil exports. What receives far less analytical attention is its function as the primary inbound maritime gateway for raw materials entering Gulf aluminium facilities. Bauxite shipments from Guinea and Australia, along with alumina from refineries in multiple geographies, must transit this corridor to reach UAE and Bahraini smelters.

When vessel diversions, route uncertainty, and elevated risk assessments push shipping operators to reconsider their schedules and pricing, the effects compound rapidly across the supply chain. According to reporting from the AFR, aluminium markets are now operating in conditions that analysts describe as among the most fragile in a generation.

The table below illustrates how disruption at this chokepoint cascades across multiple cost and operational dimensions:

| Impact Category | Near-Term Effect | Extended Disruption Scenario |

|---|---|---|

| Transit Times | Moderate extension via rerouting | Significant delays; inventory drawdown accelerates |

| War-Risk Insurance Premiums | Rising sharply | Can become prohibitive for smaller operators |

| Marine Freight Rates | Elevated on Gulf-bound routes | Broader global freight tightening via displacement |

| Cargo Availability | Reduced on key corridors | Vessel diversion reduces capacity across trade lanes |

| CIF Delivered Bauxite Prices | Upward pressure despite soft FOB | Widening CIF-FOB spread becomes entrenched |

A less commonly understood dynamic is the cargo displacement effect. When vessels are rerouted away from Gulf corridors, total available shipping capacity across interconnected global trade lanes tightens. This is not a regional freight problem — it is a global freight architecture problem that reprices logistics risk for operators with no direct exposure to the Middle East whatsoever.

Rising war-risk insurance premiums operate similarly. Underwriters do not price risk in isolation, and elevated assessments in one high-risk corridor tend to raise baseline assumptions across the broader marine insurance market, affecting vessels and routes far removed from the original conflict zone. These global bulk commodity trade risks are increasingly interconnected across asset classes.

ALBA and EGA: What Operational Decisions Reveal About Market Fragility

Two Case Studies in Feedstock Insecurity

Two case studies from Gulf producers illustrate the speed and severity with which feedstock insecurity translates into operational consequences.

ALBA's production reduction of 19% was a direct and public acknowledgement that supply uncertainty had reached a threshold requiring output adjustment. The rationale cited was inventory preservation and facilitation of refinery maintenance, but the underlying driver was straightforward: when feedstock security is uncertain, smelter operators must choose between drawing down inventory aggressively to maintain output or cutting production to extend operational runway. ALBA chose the latter — a rational response that nonetheless signals Gulf producers are not insulated from disruption in the way their smelting credentials might imply.

The EGA Al Taweelah smelter shutdown produced a different but equally instructive market dynamic. When EGA curtailed operations at this facility, alumina that had previously been consumed internally was redirected into the open market. For approximately one year following the shutdown, regional alumina availability was measurably altered as a result of this single operational decision.

The episode is a reminder that large producers are not just participants in commodity markets — they are, at scale, market-making entities whose internal operational choices reshape regional supply and demand balances.

When two or more major Gulf smelters simultaneously curtail production due to feedstock shortages, the resulting alumina surplus in some corridors, combined with aluminium supply tightening globally, can create divergent price pressures across the value chain simultaneously. This asymmetric outcome is rarely modelled in standard supply-demand frameworks.

The CIF-FOB Divergence: A Pricing Signal Most Market Participants Are Misreading

One of the most analytically significant and underreported dynamics to emerge from the current disruption is the simultaneous movement of CIF and FOB bauxite prices in opposite directions. Understanding this divergence is essential for anyone attempting to interpret current market signals accurately.

-

FOB Guinea prices are trending downward, driven by expanding Guinea export volumes and rising inventory accumulation in China. This reflects ample supply availability at the origin point, not a weakening of underlying demand fundamentals.

-

CIF delivered prices are under upward pressure, driven entirely by logistics cost escalation: elevated freight rates, war-risk insurance premiums, and longer routing distances are inflating the cost of delivery independent of the commodity's origin price.

The practical consequence is striking. Buyers are paying progressively more to receive bauxite even as the commodity's price at the point of origin falls. Logistics costs have effectively become a larger component of total procurement expense than the commodity price itself under current conditions.

This inverts the traditional procurement calculus and forces sourcing strategists to reassess assumptions about cost structure that may have been stable for years. Consequently, the commodity price impacts are flowing through in ways that standard supply-demand models fail to capture.

For investors and analysts tracking the sector, the CIF-FOB spread is currently functioning as the most accurate real-time indicator of logistical stress in the system — more informative in many respects than headline commodity prices alone.

Guinea's 74% Share: Why One Country Now Anchors Global Bauxite Sentiment

Guinea's rise to dominance in seaborne bauxite trade has been one of the defining structural shifts in global aluminium raw material markets over the past decade. The country now accounts for approximately 74% of China's seaborne bauxite imports, a concentration level with profound implications for market stability. The top bauxite-producing mines are overwhelmingly concentrated in a handful of countries, making diversification genuinely challenging.

| Market Factor | Guinea's Current Role |

|---|---|

| FOB Price Direction | High export volumes and China inventory buildup suppressing origin prices |

| CIF Price Inflation | Guinea bauxite remains the primary feedstock, but delivery costs are rising sharply |

| China Import Dependency | 74% concentration creates systemic sensitivity to Guinea supply events |

| Market Sentiment Influence | Policy or infrastructure changes in Guinea rapidly shift global trade expectations |

What makes Guinea's position particularly consequential in the current environment is that the Middle East crisis and bauxite alumina market disruptions have not reduced Guinea's export capacity. The bottleneck is in the delivery architecture, not the mine.

The concentration risk implication deserves emphasis. A market in which a single country supplies nearly three-quarters of the world's largest aluminium producer's bauxite needs carries an embedded systemic vulnerability that most market participants systematically underweight. Any future disruption to Guinea's export capacity would compound the existing Middle East logistics stress by simultaneously threatening the primary feedstock source for global production.

In addition, China commodity demand trends remain a critical variable — any softening of Chinese aluminium demand could reshape global trade flows materially, even as supply-side pressures persist.

The next major ASX story will hit our subscribers first

Scenario Modelling: Three Trajectories for the Aluminium Value Chain

The trajectory of the current disruption is not predetermined. Three distinct scenarios, differentiated by duration and severity, carry materially different implications for bauxite, alumina, and aluminium prices.

Scenario 1: Short-Duration Disruption (Under 3 Months)

- Gulf smelters draw down existing alumina inventories with minor production curtailments

- Freight and insurance costs remain elevated but operationally manageable

- LME aluminium prices rise but stabilise below the $4,000 per tonne stress threshold

- CIF-FOB spreads widen temporarily before normalising as shipping lanes stabilise

Scenario 2: Medium-Duration Disruption (3 to 9 Months)

- Alumina inventory depletion forces more significant production cuts across multiple Gulf facilities

- Alumina redirected away from the Gulf creates temporary oversupply pressure in alternative markets

- Global aluminium supply tightens meaningfully, with LME prices and regional premiums remaining elevated

- Procurement strategies globally are restructured to reduce transit dependency on Gulf corridors

Scenario 3: Extended or Escalating Disruption (Beyond 9 Months)

- Sustained smelter curtailments create a structural reduction in global aluminium output

- Aluminium prices approach or exceed $4,000 per tonne as supply deficit becomes entrenched

- Guinea's bauxite export dominance comes under greater buyer scrutiny as diversification accelerates

- Long-term capital allocation shifts toward upstream bauxite and alumina assets outside the Gulf corridor

Notably, analysis from ING suggests that Middle East escalation could indeed push aluminium above $4,000 per tonne — a threshold that would have material consequences across the entire value chain from mining operations to downstream manufacturing.

Strategic Risk Mitigation: Building Supply Chains for Resilience Rather Than Efficiency

The current crisis has crystallised a strategic imperative that was previously acknowledged but rarely acted upon with urgency. Import-dependent Gulf producers, and indeed any aluminium market participant with concentrated supply chain exposure, must move from efficiency-optimised sourcing models toward resilience-architected supply chain frameworks.

Practical mitigation strategies that leading operators are evaluating include:

- Long-term offtake agreements with diversified origin suppliers to eliminate single-corridor dependency

- Strategic inventory buffers calibrated to absorb 60 to 90 days of supply disruption, substantially above current lean inventory norms

- Route diversification protocols that pre-identify alternative shipping corridors and carrier relationships before disruption events occur, not in response to them

- Supplier geographic diversification across West Africa, Australia, and emerging bauxite origins to reduce concentration risk at the origin level

- Vertical integration assessment evaluating whether partial upstream investment in bauxite or alumina refining assets provides sustainable long-term cost and security advantages relative to continued import dependency

The broader industry implication is that the current disruption is likely to accelerate capital allocation toward upstream assets in geopolitically stable jurisdictions, and may incentivise Gulf producers to pursue vertical integration strategies that would represent a fundamental shift in how the region has historically approached raw material security.

Key Indicators for Monitoring the Evolving Market

For investors and procurement professionals tracking the intersection of the Middle East crisis and bauxite alumina market dynamics, the following forward-looking indicators provide the most actionable signals:

| Indicator | Why It Matters | Signal Direction |

|---|---|---|

| Strait of Hormuz shipping flow data | Primary feedstock transit route for Gulf smelters | Disruption equals immediate supply risk |

| Force majeure announcements from Gulf producers | Confirms operational impact of supply disruption | Escalating signals production cuts are imminent |

| Alumina inventory levels at Gulf smelters | Determines output sustainability under disruption | Declining levels indicate price and premium pressure |

| LME aluminium spreads and regional premiums | Market's real-time pricing of supply risk | Widening signals market is pricing in sustained disruption |

| War-risk and marine insurance premium indices | Proxy for logistics cost inflation across corridors | Rising premiums confirm CIF-FOB spread widening |

| Guinea export policy and infrastructure developments | Systemic risk to 74% of China's bauxite supply | Any restriction creates a major market event |

| China bauxite import and inventory data | Demand signal and FOB price anchor | Inventory buildup suppresses origin pricing |

Frequently Asked Questions

Does the Middle East crisis directly affect global bauxite mining output?

The crisis does not primarily affect bauxite mining volumes at source. The core disruption is a logistics and transit security problem. Bauxite continues to be mined, but delivering it to Gulf smelters has become more expensive, slower, and operationally uncertain — fundamentally altering the economics of the entire delivery chain.

Why are aluminium prices rising if there is no actual shortage of bauxite?

Aluminium markets are responding to forward-looking supply risk rather than current shortages. Markets are pricing in the probability that Gulf smelters representing roughly 9% of global capacity may be forced to curtail production if alumina shipments are delayed long enough to deplete operational inventory buffers.

What does the CIF-FOB price divergence mean for procurement teams?

Buyers are paying progressively more to receive bauxite even as the commodity's origin price falls. Logistics costs have become a larger component of total procurement expense than the underlying commodity price in current conditions — a dynamic that fundamentally restructures sourcing economics and cost-modelling assumptions.

How exposed is the global aluminium market to prolonged Gulf disruption?

With Gulf producers accounting for approximately 9% of global smelting capacity, a sustained curtailment scenario would create a meaningful supply deficit globally, with stress-case analysis pointing toward aluminium prices potentially exceeding $4,000 per tonne under extended disruption conditions.

Logistics Resilience as the New Competitive Frontier

The aluminium industry's traditional competitive frameworks centred on production cost efficiency, energy access, and smelting scale. However, the Middle East crisis and bauxite alumina market pressures are adding a fourth dimension to that framework: supply chain architecture and logistics resilience.

Operators who have invested in diversified sourcing networks, strategic inventory positions, and flexible routing capabilities are navigating the current environment from a position of strength. Those who optimised purely for cost efficiency under stable conditions are facing a structural reckoning.

The deeper lesson applies across commodity markets broadly. In periods of geopolitical stability, lean inventory and concentrated supply chains deliver measurable cost advantages. In periods of disruption, those same characteristics become liabilities that can threaten operational continuity.

The current crisis is making the cost of under-investment in supply chain resilience visible in a way that quarterly earnings reports and cost-optimisation models never fully captured. For procurement strategists, investors, and producers across the global aluminium value chain, that visibility may prove to be the most durable legacy of the current disruption — regardless of how long the geopolitical uncertainty itself persists.

Want to Stay Ahead of the Next Major Mineral Discovery Before the Market Reacts?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, transforming complex commodity data into actionable investment insights for both short-term traders and long-term investors — explore historic examples of major discovery returns to understand the opportunity, and begin your 14-day free trial at Discovery Alert to position yourself ahead of the broader market.