May 22, 2026

The Architecture of a Global Energy Crisis Most Markets Still Don't Fully Understand

The global energy trading system was never designed with resilience as its primary virtue. It was built around efficiency, and efficiency, by its very nature, concentrates flow through the path of least resistance. For decades, that path has run through a narrow body of water connecting the Persian Gulf to the Arabian Sea, a channel barely 33 kilometres wide at its narrowest point. When that channel functions normally, the world barely notices it. When it doesn't, the consequences reach far beyond oil rigs and shipping lanes, threading through fertilizer factories, grain harvests, manufacturing supply chains, and the sovereign balance sheets of nations that have no meaningful alternative.

Understanding the Strait of Hormuz closure and global oil supply crisis requires moving beyond headlines about barrel prices. It demands a structural examination of how an integrated, interdependent global economy responds when its single most critical energy artery is severed. Furthermore, the implications extend across currency systems, food security, and long-term geopolitical architecture in ways that most mainstream commentary has not yet fully captured.

When big ASX news breaks, our subscribers know first

Why the Strait of Hormuz Is the World's Most Dangerous Energy Chokepoint

The Geography of Vulnerability

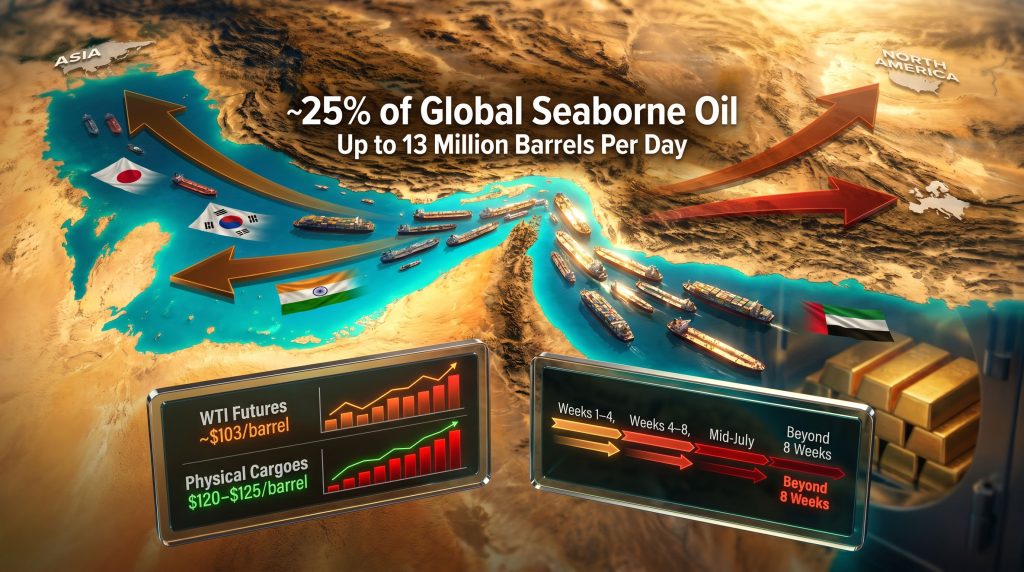

The Strait of Hormuz sits between Oman and Iran, and its significance cannot be overstated. Under normal operating conditions, approximately 20 to 21 million barrels of crude oil and petroleum products transit this passage every single day. That volume represents roughly one-quarter of all seaborne oil traded globally, alongside an equivalent share of the world's liquefied natural gas exports — for context on broader supply dynamics, the LNG supply outlook for 2025 underscores just how concentrated these flows have become.

No other maritime chokepoint comes close to concentrating this volume of energy trade in such a physically constrained geography.

| Metric | Estimated Scale |

|---|---|

| Share of global seaborne oil transiting the strait | ~25% |

| Global LNG volumes passing through | ~25% |

| Estimated daily supply loss under full closure | Up to 13 million barrels per day |

| Physical North Sea crude spot price (recent) | $120–$125 per barrel |

| Brent futures price (recent) | ~$110 per barrel |

| WTI futures price (recent) | ~$103 per barrel |

| Historical comparison | Exceeds the scale of the 1973 oil embargo |

The numbers above reveal something important: the gap between futures prices and physical spot prices is not a minor discrepancy. It reflects a structural breakdown in price discovery that has profound implications for markets, governments, and energy consumers worldwide.

A sustained closure of the Strait of Hormuz would not simply tighten oil markets. It would structurally sever the single largest artery of global energy trade, triggering cascading shortages across fuel, chemicals, fertilizers, and food systems simultaneously.

How Decades of Energy Security Planning Left Markets Exposed

The dependency on this single passage did not emerge by accident. It was the product of rational economic decisions made across decades, each individually sensible, collectively catastrophic in a disruption scenario. Gulf producers invested in infrastructure oriented toward deep-water export terminals. Importing nations built their refinery and storage ecosystems around Gulf crude grades.

Energy security planning in Western capitals focused extensively on demand-side efficiency, renewable energy transition timelines, and strategic petroleum reserve volumes. However, what it underweighted was the physical geography problem: that no viable alternative pipeline or maritime route exists at sufficient scale to replace Hormuz throughput within any short-to-medium-term planning horizon. According to analysis from the Atlantic Council, policymakers now face a stark choice between managed rationing and severe economic consequences.

The expansion of BRICS and the deepening of Gulf geopolitical alignments with non-Western power blocs has further complicated the picture, introducing a layer of strategic uncertainty that was not seriously modelled in most Western energy security frameworks.

What Happens to Global Oil Supply When the Strait Stays Closed

The Timeline from Buffer Stocks to Crisis

The mechanism by which a Hormuz closure transmits into a full supply crisis is not instantaneous. It unfolds in stages, each progressively more difficult to reverse:

- Weeks 1 to 4: Strategic petroleum reserves and commercial inventory buffers absorb initial supply shortfalls, masking the severity of the disruption in headline price data.

- Weeks 4 to 8: Reserve drawdowns accelerate sharply. Import-dependent nations begin internal discussions about rationing frameworks and demand curtailment measures.

- By mid-July (estimated): Inventory buffers across Asia, Europe, and North America approach critically low levels. India, in particular, is understood to be approaching the bottom of its available reserves.

- Beyond 8 weeks: Demand destruction becomes involuntary rather than managed. Industrial curtailments, transportation fuel rationing, and acute energy poverty risks escalate in parallel.

Countries across Southeast Asia, including Thailand, Vietnam, and the Philippines, have already begun implementing emergency energy conservation measures, a signal that the buffer period is compressing faster than official communications from major governments have indicated.

Why Reopening the Strait Does Not Mean an Immediate Return to Normal

A widespread assumption embedded in current futures pricing is that the reopening of the strait would rapidly normalise supply. This assumption is almost certainly wrong, and the gap between that assumption and physical market reality may represent one of the most significant pricing distortions in recent commodity market history.

Even under an optimistic reopening scenario, analysts estimate a recovery window of three months to one year before anything resembling normal oil flow is restored. The reasons are structural rather than operational:

- Maritime insurance markets, including Lloyd's of London, must formally certify the strait as safe for vessel transit before commercial shipping operators will commit vessels to Gulf routes.

- Vessel operators are conducting independent risk reassessments that will not simply reset when a geopolitical ceasefire is announced.

- Supply chain reconfiguration already underway in major importing economies cannot be reversed overnight.

- Persistent geopolitical uncertainty deters the long-term shipping commitments that underpin sustained cargo flow.

The physical market is already pricing some of this reality. North Sea crude cargoes are transacting at $120 to $125 per barrel while Brent futures remain near $110 and WTI near $103. That $10 to $22 per barrel discount in futures relative to physical markets suggests that paper markets are not yet reflecting the full supply picture. Indeed, the oil price rally dynamics observed earlier in 2025 look modest by comparison to what physical spot markets are now signalling.

Which Regions Face the Severest Disruption

Asia: The Most Immediately Exposed Region

Asia's exposure to a Hormuz disruption is not marginal. It is foundational. Japan, South Korea, and Taiwan have minimal domestic oil production and depend on Gulf imports for the overwhelming majority of their refinery feedstock. India's strategic reserves are understood to be approaching critically low levels. Across Southeast Asia, emergency measures are already being implemented.

The asymmetric access currently being extended to Chinese-flagged vessels, which appear able to transit the strait in limited numbers under some form of selective passage arrangement, creates a significant competitive advantage for Chinese energy importers and refiners relative to their regional peers.

Europe: Gas Markets and Fertilizer Chain Stress

Europe's direct oil exposure is less acute than Asia's, but the indirect transmission channels are significant:

- Natural gas prices are elevated across European markets, compressing industrial energy margins.

- Fertilizer production chains are disrupted by sulfur and ammonia supply shortfalls, both of which have significant Gulf exposure.

- Manufacturing competitiveness is being eroded by rising input costs at a time when European industrial capacity is already under structural pressure.

The United States: Insulated but Not Immune

Domestic production provides a meaningful partial buffer for the United States, but the insulation is incomplete. Futures markets appear to be anchored to a benign official narrative rather than physical supply conditions. The WTI futures price near $103 per barrel reflects a significant discount to the physical spot reality of $120 to $125 per barrel for North Sea cargoes.

Three structural reasons help explain why futures markets are lagging physical reality:

- Large institutional participants with established long positions have structural incentives that do not align with aggressive upside price discovery.

- Official government communications consistently emphasise supply control and reserve adequacy, dampening market anxiety regardless of the underlying physical picture.

- Markets are pricing a rapid strait reopening that the geopolitical and physical evidence does not currently support.

Developing Economies: The Most Structurally Vulnerable

Developing nations face a compounding shock of higher fuel costs, elevated fertilizer prices, rising freight rates, and food inflation, with far less fiscal capacity to absorb the combined impact compared to advanced economies. The risk of social instability in the most vulnerable importing nations is not a distant scenario. It is a near-term probability.

How China Is Navigating the Crisis

Why Beijing's Exposure Is Smaller Than Commonly Assumed

The conventional assumption that China faces severe disruption from a Hormuz closure underestimates the structural diversification Beijing has built into its energy supply architecture over the past decade. Financial and geopolitical analyst Simon Hunt, founder of Simon Hunt Strategic Services, has outlined four structural pillars supporting China's resilience:

- Overland pipeline supply from Russia and Kazakhstan bypasses maritime chokepoints entirely.

- Domestic energy mix diversification across solar, wind, and substantial coal capacity reduces the share of economic activity dependent on imported oil.

- Flatlining oil consumption growth means China's oil demand trajectory has plateaued relative to prior decades, reducing the absolute import volume required.

- Strategic petroleum reserve depth estimated at between four and six months of consumption, providing significant buffer time.

Meanwhile, Chinese tankers appear to be transiting the strait in reduced but meaningful numbers under what appears to be a selective passage arrangement, providing a supplementary supply stream unavailable to competing importers.

The Russia-China Energy Architecture Taking Shape

Large-scale commercial negotiations are reportedly underway covering new gas and oil pipeline infrastructure connecting Russia and China directly. This bilateral energy architecture, combined with the coordination of financial and geopolitical policy frameworks between Moscow and Beijing, is reducing China's long-term structural vulnerability to any Gulf disruption scenario. The medium-term effect is an energy supply base that is largely insulated from Western-controlled maritime chokepoints.

Fertilizer Markets, Food Security, and a Convergence of Threats

How an Energy Disruption Reaches the Dinner Table

The transmission from oil supply disruption to food insecurity operates through channels that are frequently underappreciated in mainstream economic commentary. Two primary mechanisms are at work:

- Direct channel: Sulfur, a critical input for phosphate fertilizer production, transits the Gulf in significant volumes. Disruptions to sulfur supply flow directly into fertilizer production costs and availability.

- Indirect channel: Elevated natural gas prices spike urea and ammonia production costs globally, since natural gas is the primary feedstock for nitrogen fertilizer manufacturing.

India is among the most acutely exposed nations, with fertilizer reserves reportedly near depletion. The implications for the 2025 to 2026 growing season are consequently material, compounding an already stressed agricultural outlook.

A Convergence of Three Food System Threats

What makes the current situation particularly serious is not any single shock but the convergence of multiple simultaneous threats to global food production:

| Threat | Mechanism | Timeline |

|---|---|---|

| Fertilizer supply shortfall | Reduced crop yields in the next growing season | 6 to 12 months |

| Potential 99-year Midwest drought cycle | Reduced output in North American grain regions | 1 to 3 years |

| Super El Niño probability | Drought conditions across major global agricultural zones | 12 to 24 months |

Simon Hunt has noted that the risk of civil unrest in vulnerable food-importing nations is not a distant downstream consequence. It is an accelerating parallel shock that could materialise within months, not years.

The next major ASX story will hit our subscribers first

A New Gulf Security Architecture and the End of American Military Primacy

The Proposed Multilateral Framework

Ceasefire negotiations are reportedly structured around the creation of a new multilateral Gulf security arrangement involving Saudi Arabia, Qatar, Turkey, Pakistan, China, and Russia. According to Simon Hunt's analysis, the framework explicitly excludes American military bases and forward-deployed forces from the region.

Saudi Arabia, which initially aligned more closely with the American position, appears to be reassessing its stance after gaining a fuller appreciation of Iran's demonstrated ability to strike critical infrastructure across the Arabian Peninsula. The movement of Pakistani troops and fighter jets into Saudi Arabia in a defensive posture is one visible signal of that reassessment.

Whether this architecture can be successfully implemented is assessed at roughly 50/50 probability. Critically, even if it is not successfully implemented, that does not automatically mean the strait reopens to all commercial traffic. Iran's estimated hypersonic and advanced missile inventory remains largely intact, at approximately 90% of pre-conflict levels.

Why Washington May Move to Block This Architecture

Loss of Gulf basing rights would represent a fundamental shift in American power projection capacity across the Middle East and into the Indian Ocean. Beyond the military dimension, a successful new Gulf security framework would accelerate the displacement of the US dollar as the dominant currency for energy trade settlement. Furthermore, declining trust in the US dollar was already eroding the petrodollar system that has underpinned American financial hegemony since the 1970s, and this crisis is now accelerating that structural shift considerably.

How the Crisis Is Accelerating De-Dollarisation

The Emerging Multi-Currency Settlement Architecture

The geopolitical shock of the Hormuz disruption is accelerating a structural transformation in how global energy trade is settled financially. Key developments include:

- BRICS nations are progressively settling bilateral trade in non-G7 currencies across a widening range of commodity classes.

- A proposed toll structure for strait transit reportedly includes payment options denominated in Chinese yuan and Iranian rial, with cargo value payments settled in non-dollar currencies at the point of receipt.

- The scale of these toll flows, applied to the world's largest energy transit corridor, represents significant financial volume that would be redirected away from dollar-denominated clearing systems.

The Physical Gold Infrastructure Being Built Across BRICS Nations

Alongside the currency diversification framework, a parallel physical gold settlement infrastructure is being constructed across BRICS member nations. The evolving role of gold in the monetary system is central to this architecture, which Simon Hunt has outlined in considerable detail:

| Development | Status |

|---|---|

| Shanghai Gold Exchange vault in Shanghai | Operational |

| Shanghai Gold Exchange vault in Hong Kong | Reportedly complete |

| Shanghai Gold Exchange vault in Saudi Arabia | Near completion or recently completed |

| Rollout across all BRICS member nations | In progress |

This infrastructure enables member nations to convert surplus bilateral currency holdings directly into physical gold within their own jurisdictions, eliminating the need to route transactions through Western financial clearing systems such as SWIFT.

China's combined government and private sector gold holdings are estimated at approximately 50,000 tonnes. Russia's official gold reserves are estimated at over 12,000 tonnes. Both nations are positioned to benefit significantly from a structural revaluation of gold's role in the international monetary system. Analysts, including Hunt, project that gold's nominal price could double from current levels within five years as currency purchasing power erodes and demand for hard-asset settlement infrastructure intensifies.

The Macroeconomic Pathway to Stagflation and Beyond

The Transmission Mechanism from Energy Shock to Recession

The pathway from a sustained Hormuz closure to broad economic contraction follows a clear and well-established transmission sequence:

- Oil supply contraction drives energy price spikes across all consuming sectors of the economy.

- Elevated energy costs push up input costs for manufacturing, agriculture, and transport simultaneously.

- Margin compression reduces corporate investment and erodes consumer purchasing power.

- Demand destruction produces GDP contraction in energy-importing economies.

- Simultaneous inflation and contraction creates stagflation, the most intractable macroeconomic environment for central bank policy management.

Simon Hunt anticipated an economic slowdown in the third or fourth quarter of 2025 even before the current commodity supply disruption. With the Strait of Hormuz closure and global oil supply crisis layered on top, he now expects recession conditions to be broadly established across most major economies by year-end 2025, with the recession deepening significantly through 2026.

Bond Markets and the Long-Term Debt Stress Signal

Current bond market conditions are sending a warning signal that deserves serious attention. The US 30-year Treasury yield is trading above 5%, with the 10-year yield above 4.65%. Hunt's framework projects that US and global inflation could reach double-digit levels by 2028.

At a global debt load of approximately three times GDP, a scenario in which 10-year government bond yields reach 10% or above creates a debt servicing arithmetic that is simply unsustainable. The logical endpoint of that dynamic is a systemic financial restructuring event, which Hunt frames as a 2030 to 2032 probability.

| Period | Macroeconomic Scenario |

|---|---|

| Late 2025 | Recession conditions emerging across major economies |

| 2026 | Deep recession; emergency central bank stimulus deployed |

| 2027 to 2029 | Stimulus-driven inflation resurgence; commodity price volatility |

| 2030 to 2032 | Potential systemic financial restructuring event |

Hard Assets Through the Crisis Cycle: Gold, Copper, and Critical Minerals

Gold as the Primary Wealth Preservation Instrument

Hunt's framework positions gold as the primary hard asset for wealth preservation through the coming cycle, noting that sophisticated institutional investors are already beginning to price equity valuations in gold terms rather than nominal currency terms. The implication is that even if equity indices rise substantially in nominal terms over the next decade, real returns measured against gold may be flat or negative.

Importantly, Hunt has noted that American households accumulating physical gold should be mindful of historical precedent — specifically that governments have previously moved to confiscate privately held gold during severe financial crises. Holding physical gold outside the banking system is consequently presented as the more prudent approach.

The Copper Super Cycle: A Premature Consensus

The near-universal consensus view that copper has entered a new commodity super cycle driven by electrification and data centre infrastructure deserves scrutiny. Hunt's contrarian analysis identifies two important counterfactors.

First, global business activity is already decelerating. A recession that drives sharp physical demand destruction could overwhelm any supply-side tightening narrative in the near term. Hunt projects copper at approximately $28,000 per tonne by 2030 in nominal terms but notes this is essentially flat in real, gold-adjusted terms.

Second, Nvidia has publicly disclosed that its copper consumption per gigawatt of data centre capacity is approximately 200 tonnes, which is not a large figure when scaled against realistic capacity deployment numbers. More significantly, Nvidia has reportedly acquired two companies specialising in photonic, or light-based, interconnect technology for a combined approximately $4 billion, with reports suggesting the company is targeting a transition away from copper in its data centres by around 2028. This eliminates what many had assumed would be a major incremental copper demand driver.

Critical Minerals: The Processing Bottleneck Western Governments Cannot Quickly Solve

Western governments are actively taking equity stakes in critical mineral projects globally, but the harder problem is not mine ownership. It is processing capacity. The broader dynamics driving critical minerals demand highlight just how concentrated processing infrastructure remains in Chinese hands, covering gallium, antimony, tungsten, and rare earths.

Building processing capacity in Western jurisdictions involves a multi-year construction timeline, significant capital requirements, environmental permitting complexity, and meaningful community opposition. Hunt characterises processing as genuinely difficult to replicate at speed, noting that catching up is underway but that the timeline is measured in years, not months. Furthermore, the EIA's analysis of energy trade flows reinforces how structurally dependent Western supply chains remain on these constrained processing networks.

Frequently Asked Questions: Strait of Hormuz and the Global Oil Supply Crisis

How much oil passes through the Strait of Hormuz daily?

Approximately 20 to 21 million barrels of oil per day transit the strait under normal conditions, representing roughly one-quarter of global seaborne oil trade and a comparable share of global LNG volumes.

What would a full Strait of Hormuz closure mean for oil prices?

A sustained full closure could remove up to 13 million barrels per day from accessible global supply, a shock that analysts compare to exceeding the scale of the 1973 oil embargo. Physical crude prices have already reached $120 to $125 per barrel in some spot markets, while futures markets continue to underreflect the physical supply reality.

Which countries are most affected by the Strait of Hormuz closure?

Asian economies, particularly Japan, South Korea, India, Taiwan, Vietnam, Thailand, and the Philippines, face the most acute near-term exposure. Developing economies globally face compounding shocks through higher fuel, fertilizer, freight, and food costs.

How long would it take for oil markets to recover if the strait reopened?

Analysts estimate three months to one year for full market normalisation, contingent on maritime insurance reinstatement, vessel operator confidence, and the absence of renewed geopolitical escalation.

Is the Strait of Hormuz crisis accelerating de-dollarisation?

The crisis is accelerating the construction of alternative trade settlement infrastructure within BRICS nations, including physical gold vaults, bilateral currency agreements, and a proposed toll structure for strait transit payable in non-G7 currencies.

What is the risk of a global food crisis linked to the Strait of Hormuz?

The risk is material and near-term. Fertilizer supply disruptions, elevated energy costs for agricultural production, and compounding weather risks — including a potential 99-year Midwest drought cycle recurrence and elevated Super El Niño probability — create a convergent threat to food security, particularly in import-dependent developing nations.

This article is intended for informational and educational purposes only. It does not constitute financial, investment, or legal advice. Forecasts, projections, and scenario analyses referenced throughout reflect the views of cited analysts and should not be taken as guarantees of future outcomes. Readers should conduct independent research and consult a licensed financial adviser before making any investment decisions.

Want to Position Ahead of the Resource Opportunities This Global Energy Crisis Is Creating?

As geopolitical shocks reshape commodity markets and accelerate demand for critical minerals, gold, and energy alternatives, Discovery Alert's proprietary Discovery IQ model delivers real-time notifications on significant ASX mineral discoveries — translating complex market shifts into actionable investment opportunities the moment they emerge. Explore how historic mineral discoveries have generated substantial returns and begin your 14-day free trial today to ensure you're positioned ahead of the market.