June 20, 2026

The Hidden Fragility at the Heart of Global Hydrogen Trade

Most energy security frameworks are built around crude oil. Analysts track tanker movements, OPEC production quotas, and refinery throughput with obsessive precision. Yet a quieter, more structurally complex vulnerability has been accumulating for years in the hydrogen-based commodity system, one that the ongoing Middle East crisis and global hydrogen supply chains issue has now forced into sharp relief. The relationship is not a peripheral concern for specialists. It is a stress test that touches fertiliser prices, food security, industrial chemical supply, and the credibility of the entire low-emissions hydrogen transition simultaneously.

Understanding why this matters requires a reframing of what hydrogen trade actually looks like in practice, because it looks nothing like what most people imagine.

When big ASX news breaks, our subscribers know first

Hydrogen Is Not Shipped as Hydrogen: The Derivative Trade That Shapes Global Markets

The Real Exposure Lies in Chemical Carriers

Pure hydrogen gas is extraordinarily difficult and expensive to transport at scale. As a result, the global hydrogen economy functions largely through derivative products: ammonia, urea, methanol, and various refined petrochemicals. These are the physical vehicles through which hydrogen-embedded value moves across continents. When supply chain analysts discuss hydrogen trade exposure, they are almost entirely discussing disruptions to these derivative flows.

This distinction matters enormously. An ammonia terminal shortage in a receiving port creates fertiliser deficits for farmers within weeks. A methanol supply disruption ripples through marine fuels, plastics feedstocks, and specialty chemical manufacturing. The leverage that the Middle East holds over the global hydrogen economy is exercised primarily through these derivative pathways, not through direct hydrogen exports.

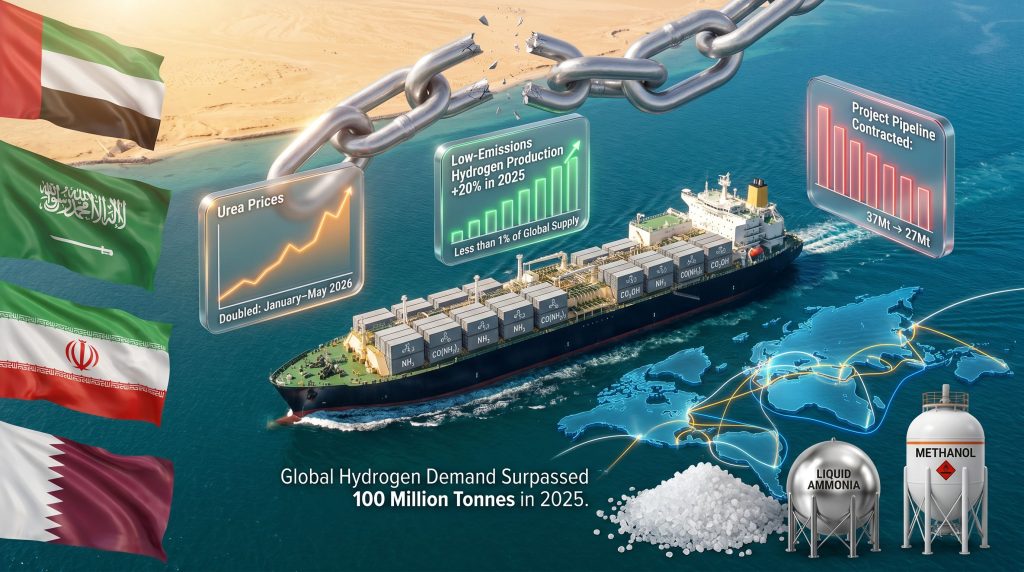

According to the IEA's Global Hydrogen Review 2026, the Middle East accounts for approximately one-sixth of global hydrogen production, which translates to roughly 16 to 17 million tonnes of hydrogen equivalent embedded in traded commodities annually, given that global demand surpassed 100 million tonnes in 2025 for the first time in recorded history. That production anchors ammonia and urea exports flowing to agricultural markets across Asia, Africa, and Europe, and methanol supplies serving industrial sectors worldwide.

The Strait of Hormuz as a Structural Chokepoint

The Strait of Hormuz has long been recognised as a critical node for oil and liquefied natural gas flows. Its role as a chokepoint for hydrogen-derivative commodities has received far less attention, yet the exposure is structurally comparable. Gulf shipping lanes carry ammonia tankers, methanol carriers, and chemical product vessels alongside hydrocarbons. When these routes are threatened or circumnavigated, the consequences differ from an oil shock in one important way: resolution timelines are substantially longer.

Oil markets can often absorb short-term disruptions through strategic petroleum reserve releases and rapid rerouting. Ammonia and urea supply chains do not have equivalent buffer mechanisms. Production facilities cannot be stood up quickly, shipping rerouting adds significant insurance premiums and delivery delays, and agricultural input purchasing cycles mean that a supply shortfall in one quarter can translate into food production deficits in the next growing season. This slower propagation dynamic is precisely what makes hydrogen-derivative supply disruptions structurally more persistent than conventional energy price shocks.

| Chokepoint | Primary Commodity Exposure | Hydrogen-Derivative Relevance | Buffer Mechanism Available? |

|---|---|---|---|

| Strait of Hormuz | Oil, LNG, ammonia, methanol | High | Limited |

| Suez Canal | Oil, LNG, mixed cargo | Moderate | Partial |

| Strait of Malacca | Oil, LNG | Low-Moderate | Partial |

A Sector-by-Sector Breakdown of What the Crisis Is Actually Disrupting

Fertiliser Markets: The Most Immediate and Visible Casualty

Of all the sectors exposed to Middle East hydrogen-derivative supply disruptions, fertiliser markets have borne the most acute and immediate pressure. The IEA's Global Hydrogen Review 2026 documents that urea prices approximately doubled between January and May 2026, driven by the convergence of three simultaneous pressures: production disruptions at Gulf facilities, elevated natural gas input costs feeding through into ammonia production economics, and export restrictions imposed as the regional crisis deepened.

The downstream consequences extend well beyond commodity price volatility. Nitrogen fertilisers, which are manufactured from ammonia derived from hydrogen, underpin crop yields for billions of people. For import-dependent agricultural economies across Sub-Saharan Africa, South Asia, and Southeast Asia, a doubling of urea prices within a five-month window is not an abstract market event. It is a direct threat to planting decisions, crop yields, and food affordability in the following harvest cycle.

This is the dimension of the Middle East crisis and global hydrogen supply chains that receives the least coverage in energy market analysis: the food security transmission mechanism. The nitrogen fertiliser supply chain is, in structural terms, a downstream expression of fossil-fuel-derived hydrogen dependency. Disruptions to that hydrogen supply propagate within one or two supply chain steps into staple food production costs.

Methanol, Refined Products, and Secondary Pressure Points

Methanol occupies a particularly complex position in the current disruption landscape. It serves simultaneously as an industrial solvent, a petrochemical feedstock, and an increasingly significant marine fuel as the shipping industry seeks lower-emission alternatives to conventional bunker fuels. Middle East producers account for a substantial share of global methanol output, meaning that production-side disruptions create compound pressure across multiple end-use markets at once.

Refining disruptions add a further layer of complexity. When hydrogen feedstock availability tightens at Gulf refineries, hydrocracking and hydrotreating operations that depend on hydrogen as a process input are constrained. This feeds reduced output of refined petroleum products back into global markets, creating indirect pressure on fuel prices in regions already contending with energy cost inflation.

Industrial Feedstocks: The Slow-Building Downstream Impact

Beyond fertilisers and methanol, hydrogen functions as a critical process input for steel production through direct reduction of iron ore, glass manufacturing, and the specialty chemicals sector. Unlike fertiliser markets where price impacts are rapid, industrial feedstock disruptions typically propagate through value chains with a 3 to 6 month lag, as manufacturers draw down inventories before feeling the full pressure of upstream shortfalls.

Europe's integrated chemicals sector and Japan's manufacturing base are particularly exposed through this pathway. Furthermore, India's LNG import structure and heavy dependence on fertiliser imports from Gulf sources creates a dual vulnerability, encompassing both the direct food security risk and potential industrial chemicals shortfalls affecting domestic manufacturing.

"The current crisis is not primarily an energy price event. It is a supply chain integrity event affecting the physical availability of hydrogen-based industrial inputs across multiple sectors simultaneously, with resolution timelines measured in years rather than months."

How This Crisis Compares to Previous Hydrogen Supply Shocks

Historical Analogues and Their Limits

The 2021 to 2022 European natural gas crisis provides the most instructive partial analogue. As gas prices spiked across Europe, ammonia plants became uneconomical to operate, several major facilities curtailed production, and fertiliser shortages cascaded into agricultural markets. That disruption took between 12 and 18 months to substantially resolve as gas prices moderated and production resumed.

Russia's invasion of Ukraine in 2022 added a second shock layer, disrupting Black Sea ammonia export routes and contributing to the fertiliser price spikes that compounded food security pressures globally. That disruption remains only partially resolved, with trade route restructuring still ongoing.

The current Middle East crisis is structurally distinct because it combines three disruption mechanisms simultaneously: production-side shocks at Gulf facilities, shipping route disruption through threatened Hormuz transit corridors, and export restrictions imposed as the conflict deepens. No previous hydrogen-derivative supply disruption has combined all three mechanisms concurrently. This simultaneity is precisely why the resolution timeline remains open-ended.

| Disruption Event | Primary Channel | Key Commodity Affected | Resolution Timeline |

|---|---|---|---|

| 2021-22 European Gas Crisis | Input cost spike | Ammonia, urea | 12-18 months |

| Russia-Ukraine War (2022) | Export route disruption | Ammonia, grain | Ongoing |

| Middle East Crisis (2025-26) | Production + shipping + export restriction | Ammonia, urea, methanol, refined products | Unresolved |

Low-Emissions Hydrogen: Strategic Case Strengthened, Operational Scale Still Years Away

The Arithmetic of the Gap

The crisis has unquestionably strengthened the strategic argument for scaling low-emissions hydrogen. It has also made brutally clear how far current production falls short of providing any meaningful near-term buffer. According to the IEA's Global Hydrogen Review 2026, low-emissions hydrogen production grew by approximately 20% in 2025, reaching close to 1 million tonnes. Against total global demand of more than 100 million tonnes, this represents less than 1% of global hydrogen supply.

Low-emissions hydrogen production is forecast to exceed 1% of global output for the first time in 2026, a milestone that underscores genuine progress while simultaneously illustrating the scale of the challenge. Even tripling current low-emissions output would represent only around 3 million tonnes in a market consuming over 100 million tonnes annually. The arithmetic alone makes clear that low-emissions hydrogen cannot provide a crisis buffer in any operationally meaningful timeframe without a fundamental acceleration in deployment rates.

Why Investment Momentum Weakened in 2025

Despite the strengthened strategic case, investment momentum in low-emissions hydrogen actually deteriorated in 2025. The announced project pipeline targeting 2030 operation has contracted by approximately 25%, falling from 37 million tonnes to 27 million tonnes, as project delays and cancellations accumulated. More concerning still, the subset of projects assessed as having a strong probability of reaching operation by 2030 declined from 10 million tonnes to just above 6 million tonnes in the latest IEA assessment.

Three structural barriers are driving this retreat:

-

Persistent cost premium: Low-emissions hydrogen and hydrogen-based products remain significantly more expensive than conventional alternatives across most markets. The cost of supply chain resilience through hydrogen diversification is real and must be explicitly priced into policy design.

-

Demand uncertainty: Offtake agreement volumes in 2025 were broadly unchanged from the prior year, signalling stagnant commercial confidence. Critically, only around 20% of newly signed offtake volumes were supported by firm contractual commitments rather than memoranda of understanding or indicative agreements. Developers cannot commit capital without revenue certainty; buyers will not commit to long-term contracts without competitive pricing. This circular impasse is the defining commercial barrier to project progression.

-

Regulatory complexity and infrastructure gaps: The absence of harmonised international certification standards, port infrastructure limitations, pipeline repurposing constraints, and storage capacity deficits create a fragmented market environment that compounds financing risk, particularly for projects in emerging economies where capital costs are already elevated.

"The crisis accelerates the strategic case for low-emissions hydrogen while simultaneously exposing that the operational case — that of sufficient scale to provide near-term supply chain resilience — remains years away from realisation."

However, Wood Mackenzie's analysis of how Middle East conflict adds a new dimension to hydrogen strategies offers a more granular view of the commercial and geopolitical trade-offs that developers and governments now face. This broader energy security challenge underscores why the strategic pivot to diverse, low-emissions supply is not merely theoretical but operationally urgent.

Regional Capability Assessment: Where Low-Emissions Hydrogen Is Actually Advancing

China: Leading Deployment, But Showing First Signs of Slowdown

China's dominance in electrolyser manufacturing and deployment is not contested. The country accounted for approximately 75% of new electrolyser installations globally in 2025, as total installed global electrolyser capacity doubled to 4 gigawatts. That doubling, however, was almost entirely a function of Chinese domestic deployment rather than a globally distributed acceleration.

The IEA's 2026 review identifies a significant inflection signal: investment decisions for new electrolysis projects in China declined for the first time on record in 2025. This suggests that early-mover momentum is encountering the same demand certainty and cost competitiveness barriers that constrain deployment in other markets. New policy support measures introduced by Chinese authorities in late 2025 are expected to partially arrest this trend, but the inflection itself deserves attention from investors tracking the sector's trajectory.

Europe: Regulatory Architecture in Place, Execution Lagging

Europe has built the most comprehensive regulatory framework for low-emissions hydrogen of any major economy, encompassing certification standards, demand mandates for the refining and transport sectors, and financial support programmes. The practical challenge is that slow transposition of key regulations into member state law continues to defer final investment decisions.

Support programmes are advancing refining-sector projects in particular, but the gap between the ambition expressed in European hydrogen strategy documents and the confirmed project pipeline remains the defining challenge. In addition, the broader renewable energy transition that underpins green hydrogen ambitions continues to face its own execution bottlenecks across member states.

North America, India, and Japan: Progress Under Persistent Uncertainty

In North America, the hydrogen production tax credit established under the US Inflation Reduction Act has created a meaningful improvement in project economics for specific production pathways, though regulatory guidance on emissions accounting continues to create uncertainty. India's National Green Hydrogen Mission is generating early-stage project activity, but without anchor offtake agreements from domestic industrial buyers, the development pipeline remains fragile.

Japan's hydrogen import strategy is advancing through bilateral agreements with prospective export partners, though cost competitiveness relative to domestic alternatives continues to slow uptake.

Africa: Substantial Potential, Near-Zero Deployment, and an Underappreciated Food Security Angle

Africa's position in the global low-emissions hydrogen landscape combines extraordinary long-term potential with almost negligible current output. The continent currently produces approximately 6,000 tonnes of low-emissions hydrogen, a fraction so small it barely registers against global totals. Of the 34 announced projects targeting operation by 2030 across African nations, not a single one has yet reached a final investment decision.

The strategic opportunity is real and material. Africa's solar and wind resources in key regions — including Morocco, Namibia, and parts of southern and eastern Africa — position the continent as a credible long-term export platform for green ammonia and green hydrogen. The IEA's 2026 review notes that hydrogen could support industrial development and improve food security through domestic fertiliser production, reducing the import dependency that the current Middle East crisis has made acutely visible. Consequently, the energy transition demand for green hydrogen feedstocks could meaningfully accelerate African project pipelines if offtake certainty improves.

The enablers required to bridge the gap between potential and deployment are specific and known:

- Reduced financing costs, given that the cost of capital in many African markets makes project economics uncompetitive even where resource quality is world-class

- Integration of hydrogen strategies with broader national economic development priorities, rather than treating hydrogen as a standalone export opportunity

- Anchor offtake agreements from creditworthy international buyers that provide the revenue certainty developers need to reach final investment decisions

The next major ASX story will hit our subscribers first

A Strategic Response Framework: From Crisis Management to Structural Resilience

Immediate Priorities

The short-term response to supply disruption in ammonia and urea markets requires emergency diversification of procurement across alternative producing regions, including Russia (subject to sanctions constraints), North Africa, and the United States Gulf Coast. Governments in the most exposed agricultural economies should consider the establishment of strategic fertiliser reserves, analogous in design to oil strategic petroleum reserves, as a buffer against acute supply shocks.

The absence of such mechanisms was not a critical vulnerability when the Middle East operated as a reliable supplier. It has become one now.

Medium-Term Supply Chain Restructuring

The medium-term priority is building geographic diversification into hydrogen-based commodity procurement at the structural level, not merely as a crisis response. This means prioritising low-emissions hydrogen deployment in sectors with the highest conventional hydrogen dependency and establishing bilateral hydrogen trade frameworks with politically stable, renewables-rich candidate exporters including Australia, Chile, Morocco, and Namibia. Furthermore, sourcing green transition materials through diversified supply chains will be essential to underpinning those bilateral frameworks effectively.

Long-Term Structural Resilience

The long-term task is integrating hydrogen supply chain risk into national energy security frameworks in a way that moves beyond oil-centric security models. This requires policy design that simultaneously addresses demand certainty through mandates and purchase incentives, and supply development through capital support and regulatory clarity.

Multilateral development finance institutions have a specific role to play in reducing the cost of capital for low-emissions hydrogen projects in Africa and other emerging markets, where the resource endowment exists but the financing conditions do not yet support commercial deployment. For instance, Green Building Africa's coverage of Middle East conflict and hydrogen supply chain risks outlines how the development finance gap directly compounds the delays in bringing new low-emissions capacity online.

Frequently Asked Questions: Middle East Crisis and Global Hydrogen Supply Chains

What hydrogen-based products are most affected by the Middle East crisis?

Ammonia, urea, methanol, and refined petrochemical products face the most direct disruption. The Middle East's central role in producing and exporting these commodities makes it a structural anchor for global supply chains across fertilisers, chemicals, and marine fuels.

Why can't low-emissions hydrogen immediately replace disrupted supply?

Low-emissions hydrogen currently represents less than 1% of global hydrogen production. The infrastructure, cost structures, and long-term offtake agreements required to scale it as a functional crisis buffer do not yet exist at sufficient operational scale.

How much did urea prices increase during the crisis?

Urea prices approximately doubled between January and May 2026, according to the IEA's Global Hydrogen Review 2026, driven by production disruptions, higher natural gas input costs, and export restrictions from key Middle East producing regions.

Which regions face the greatest vulnerability?

Import-dependent agricultural economies across Sub-Saharan Africa, South Asia, and Southeast Asia carry the most acute near-term food security risk. Europe's chemicals sector and Japan's manufacturing base also hold significant industrial feedstock exposure.

What is the current state of the low-emissions hydrogen project pipeline?

The announced pipeline targeting 2030 has contracted by approximately 25% to 27 million tonnes. Projects with a strong probability of reaching operation by 2030 have declined from 10 million tonnes to just above 6 million tonnes, according to the IEA's most recent assessment.

What role can Africa play in future hydrogen supply chains?

Africa holds substantial long-term potential as a green hydrogen and green ammonia export hub. However, none of the 34 announced projects targeting 2030 operation across the continent have yet reached a final investment decision.

Disclaimer: This article draws on publicly available analysis from the IEA's Global Hydrogen Review 2026 and related institutional research. It contains forward-looking statements, market projections, and scenario analysis that involve uncertainty. Nothing in this article constitutes financial or investment advice. Readers should conduct independent due diligence before making any investment decisions related to the hydrogen sector or commodity markets.

For further institutional analysis, the IEA's Global Hydrogen Review 2026 and related Middle East energy market coverage are available at iea.org.

Want to Track the ASX Mineral Discoveries Shaping the Energy Transition?

As hydrogen supply chain vulnerabilities reshape global commodity markets and accelerate demand for critical minerals, Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries — instantly translating complex geological data into actionable investment insights for traders and long-term investors alike. Explore the historic returns that major mineral discoveries have generated and begin your 14-day free trial today to position yourself ahead of the market.