June 17, 2026

What Economic Forces Drive Brazil's R$ 298.8 Billion Mineral Export Powerhouse?

Global commodity markets operate through complex networks of supply, demand, and geopolitical leverage that fundamentally reshape national economic strategies. Brazil's mineral sector demonstrates how strategic resource positioning can generate massive trade surpluses while simultaneously creating vulnerabilities to price volatility and external demand fluctuations, making mineral exports Brazil a cornerstone of the nation's economic framework.

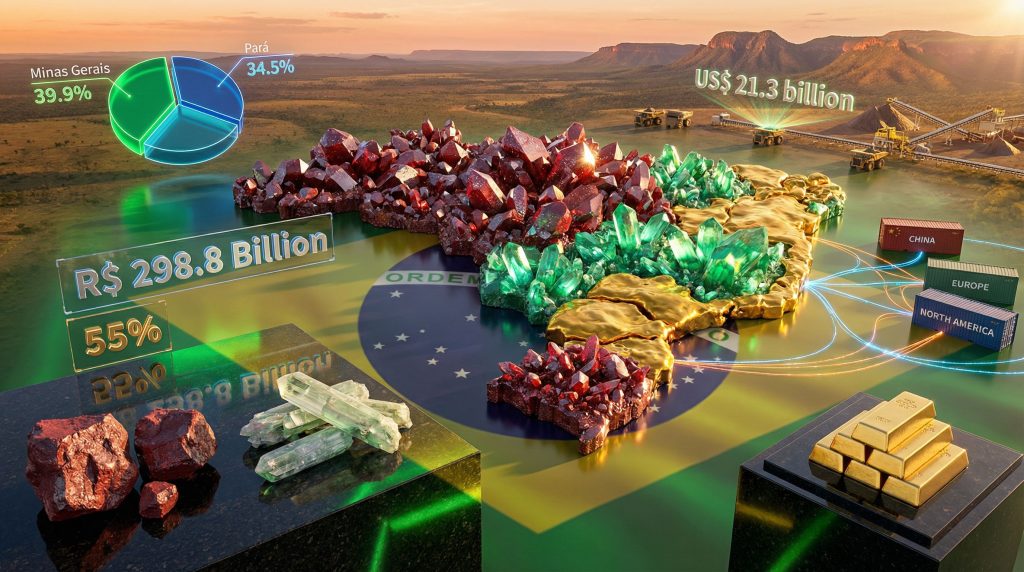

The Brazilian mining industry achieved remarkable financial performance in 2025, generating R$ 298.8 billion in total revenue, representing a robust 10.3% growth from the previous year. This exceptional performance stems from Brazil's geological advantages, established infrastructure networks, and strategic positioning within global supply chains that serve major industrial economies.

When big ASX news breaks, our subscribers know first

Understanding Brazil's Strategic Position in Global Commodity Markets

Brazil's mineral exports Brazil generated approximately US$ 46 billion in foreign trade receipts during 2025, marking a 6.2% increase in dollar terms despite challenging global economic conditions. The sector's contribution to Brazil's trade balance reveals its fundamental importance to national economic stability, accounting for 55% of the country's total trade surplus of US$ 68.3 billion.

This represents a significant 8 percentage point increase from 2024, when minerals contributed 47% of the trade surplus. Such dramatic improvement demonstrates Brazil's enhanced competitiveness in international markets and its ability to capitalise on global demand for raw materials essential to infrastructure development and industrial production.

The volume metrics provide additional context: Brazil exported 431 million tonnes of mineral products in 2025, reflecting a 7.1% increase in physical output. However, the disparity between volume growth (7.1%) and value growth (6.2%) suggests slight price compression, indicating market pressures on commodity pricing that could impact future revenue projections.

Iron Ore Dependency vs. Diversification Economics

Brazil's mineral export profile reveals both strength and vulnerability through its heavy concentration in iron ore production. Iron ore comprises 62.8% of total mineral export volume, generating R$ 157.2 billion in revenue, equivalent to 52.6% of total sector income. Despite achieving overall sector growth, iron ore revenues declined 2.2% year-over-year, highlighting the risks of commodity concentration.

This dependency creates significant exposure to steel industry cycles, Chinese infrastructure demand, and global iron ore price trends that directly influence Brazil's economic performance across entire regions dependent on mining activities. Major steel-producing economies, particularly China, India, and developing Asian markets, drive demand patterns that shape the sector's future.

The economic resilience strategy involves diversifying into critical minerals essential for energy transition technologies. Investment projections indicate US$ 21.3 billion allocated specifically to critical minerals energy transition through 2030, representing a 15.2% increase compared to previous investment cycles and demonstrating sector recognition of diversification imperatives.

Which Regional Economic Clusters Dominate Brazil's Mineral Production Landscape?

Brazil's mineral wealth concentrates in three primary economic clusters that generate distinct competitive advantages through geological endowments, infrastructure development, and accumulated human capital specialisation.

Minas Gerais Economic Hub Analysis (39.9% Market Share)

Minas Gerais dominates Brazilian mineral production with 39.9% of national output, leveraging centuries of mining experience dating to colonial gold extraction. The state's economic advantages include established transportation corridors connecting inland mining operations to coastal export terminals, concentrated skilled workforce populations, and mature regulatory frameworks supporting large-scale operations.

The state's infrastructure investment patterns create multiplier effects throughout regional economies. Transportation networks, including the Estrada de Ferro Vitória a Minas railroad and highway systems, facilitate efficient mineral movement from extraction sites to ports in Espírito Santo and Rio de Janeiro. These logistics advantages reduce per-tonne transportation costs and enhance profit margins for mining companies operating in the region.

Labour market dynamics in Minas Gerais reflect decades of mining industry development, with technical universities, specialised training programmes, and engineering expertise concentrated in cities like Belo Horizonte, Itabira, and Ouro Preto. This human capital accumulation creates competitive advantages that attract continued investment and maintain the state's dominant market position.

Pará's Emerging Mineral Economy (34.5% Market Share)

Pará represents Brazil's fastest-growing mineral production region, capturing 34.5% of national market share through strategic development of Amazon region deposits. The state's mineral economy centres on large-scale operations that leverage proximity to Atlantic shipping routes and access to significant ore body reserves.

Port infrastructure in Pará provides direct access to international markets without requiring complex inland transportation. The Port of Vila do Conde and other facilities enable efficient loading of bulk mineral cargoes destined for Asian, European, and North American markets, reducing logistics costs compared to inland operations requiring rail or truck transport to distant ports.

Environmental considerations create both challenges and opportunities for Pará's mining development. Furthermore, sustainable extraction practices, community engagement protocols, and environmental monitoring systems represent necessary investments that can enhance long-term operational viability while addressing stakeholder concerns about Amazon region development.

Bahia's Specialised Mineral Sectors (4.5% Market Share)

Bahia contributes 4.5% of national mineral production through specialised operations focused on specific commodities and value-added processing activities. The state's smaller production base relative to Minas Gerais and Pará enables focus on niche markets and higher-margin mineral products that require specialised processing capabilities.

Regional economic diversification strategies in Bahia emphasise technology transfer, processing innovation, and integration with petrochemical industries located in the state. These synergies create opportunities for mineral processing operations that serve both domestic and export markets while generating higher value-added employment opportunities.

How Do Critical Minerals Transform Brazil's Long-Term Economic Strategy?

The global transition toward renewable energy systems, electric vehicle adoption, and advanced technology manufacturing creates unprecedented demand for critical minerals that Brazil possesses in significant quantities. This transition fundamentally alters the economic value proposition of mineral exports Brazil from traditional bulk commodities toward strategic materials essential for national security and industrial policy objectives.

Energy Transition Mineral Economics

Brazil's strategic mineral investment pipeline totals US$ 21.3 billion through 2030, representing 27.7% of total sector investment allocation. This concentration reflects global recognition that energy transition minerals command premium pricing, longer-term supply contracts, and enhanced geopolitical significance compared to traditional commodities.

Critical minerals essential for energy transition include:

• Lithium: Battery technology for electric vehicles and energy storage systems

• Nickel: Stainless steel production and battery cathode materials

• Copper: Electrical systems for renewable energy infrastructure

• Rare earth elements: Wind turbine magnets and high-technology applications

• Cobalt: Advanced battery component manufacturing

The 15.2% growth rate for critical mineral investments significantly exceeds the 12.5% overall sector investment increase, demonstrating capital reallocation toward higher-priority minerals aligned with international energy policies and industrial transformation initiatives. For instance, this strategic shift reflects the broader critical minerals strategy being implemented globally.

Geopolitical Economic Implications

Brazil's critical mineral resources create leverage opportunities in bilateral trade negotiations and multilateral cooperation agreements with major consuming economies. Countries implementing aggressive decarbonisation policies, including European Union members, Japan, South Korea, and the United States, require reliable access to critical mineral supplies that Brazil can provide.

Supply chain security considerations motivate consuming nations to diversify mineral sources away from concentrated suppliers, particularly for materials essential to national defence and energy security. Brazil's political stability, established mining industry, and geographic accessibility create competitive advantages in securing long-term supply agreements that provide revenue predictability for mining operators.

The current geopolitical environment amplifies interest in critical minerals among nations pursuing clean energy development plans and technological advancement initiatives. Brazil's mineral resources position the country as an essential partner in global supply chains supporting renewable energy deployment and electric transportation adoption.

What Investment Patterns Signal Future Economic Growth Trajectories?

Investment allocation patterns across Brazil's mineral sector reveal strategic priorities that will determine long-term economic performance and competitive positioning in evolving global markets.

Capital Allocation Trends Across Mineral Sectors

| Investment Category | 2026-2030 Projection | Growth Rate | Strategic Focus |

|---|---|---|---|

| Critical Minerals | US$ 21.3 billion | +15.2% | Energy transition |

| Traditional Mining | US$ 55.6 billion | +11.8% | Efficiency gains |

| Infrastructure | US$ 12.4 billion | +8.9% | Logistics optimisation |

| Total | US$ 76.9 billion | +12.5% | Comprehensive growth |

The total investment pipeline of US$ 76.9 billion represents a 12.5% increase compared to the previous cycle projection of US$ 68.4 billion for 2025-2029, indicating expanding confidence among mining companies regarding future market conditions and regulatory stability.

Traditional mining operations will receive US$ 55.6 billion in investment, comprising 72.3% of total capital allocation. This substantial commitment to established operations reflects the continued importance of iron ore, copper, and other bulk commodities while incorporating efficiency improvements and technological upgrades to maintain competitive advantages.

Infrastructure investments totalling US$ 12.4 billion focus on logistics optimisation, transportation capacity expansion, and port facility enhancements that support increased production volumes and improved export capabilities. These investments create shared benefits across multiple mining operations while reducing per-unit transportation costs.

Regional Investment Distribution Economics

The three-state concentration of mining activities creates competitive dynamics as Minas Gerais, Pará, and Bahia implement policies designed to attract investment capital. Tax incentive programmes, infrastructure development commitments, and regulatory streamlining initiatives represent tools available to state governments seeking to capture larger shares of investment flows.

State-level competition generates benefits for mining companies through reduced tax burdens, improved infrastructure access, and expedited permitting processes. However, this competition can also create inefficiencies if states engage in destructive bidding wars that reduce overall fiscal revenues without generating proportional economic benefits.

Investment prioritisation frameworks must balance immediate revenue generation against long-term sustainability considerations, particularly regarding environmental protection, community impact management, and resource conservation strategies that maintain extraction viability across extended time horizons.

How Does Brazil's Mineral Export Performance Compare Globally?

Brazil's mineral export performance demonstrates competitive strengths while revealing vulnerabilities that require strategic management to maintain market position against other major mineral-producing nations.

Competitive Position Analysis

Brazil's 431 million tonnes of mineral exports in 2025 establish the country amongst the world's largest mineral exporters by volume. However, the 6.2% value increase compared to 7.1% volume growth indicates price realisation challenges that could impact competitiveness against suppliers offering premium products or superior logistics capabilities.

The concentration of 62.8% of export volume in iron ore creates both advantages and risks. While Brazil benefits from large-scale production efficiencies and established market relationships with major steel producers, this concentration exposes the economy to iron ore demand insights and demand fluctuations in primary consuming markets.

International market positioning requires continuous monitoring of competitor capabilities across key mineral categories. Australia's iron ore operations, Chile's copper production, and emerging suppliers in Africa and Asia represent competitive threats that could capture market share through technological improvements, cost reductions, or superior product quality.

Economic Vulnerability Assessment

Currency fluctuation impacts significantly affect mineral export revenues reported in Brazilian reais versus US dollars. The disparity between domestic revenue growth (10.3% in reais) and export value growth (6.2% in dollars) reflects exchange rate movements that can either enhance or diminish economic benefits from export activities.

Commodity price shock absorption capacity depends on operational flexibility, cost structure management, and financial hedging strategies employed by individual mining companies. Brazil's large-scale operations typically possess greater resilience to short-term price volatility compared to smaller producers, but remain vulnerable to sustained downturns in global commodity markets.

Supply chain disruption resilience requires diversified transportation options, redundant infrastructure capacity, and flexible logistics arrangements that can adapt to port closures, rail interruptions, or other operational challenges that could impact export capabilities.

The next major ASX story will hit our subscribers first

What Fiscal and Employment Economics Define the Sector's National Impact?

Brazil's mineral sector generates substantial fiscal contributions while creating employment opportunities that extend far beyond direct mining operations through multiplier effects across regional economies.

Tax Revenue Generation Analysis

The mineral sector contributed R$ 103 billion in total taxes and charges during 2025, representing 10% growth from the previous year's R$ 93.4 billion. This substantial fiscal contribution provides government revenues that support public infrastructure development, social programmes, and economic development initiatives across Brazil.

CFEM (Compensação Financeira pela Exploração Mineral) mining royalties generated R$ 7.9 billion in 2025, representing direct compensation to federal and local governments for mineral extraction activities. These royalty payments fund regional development projects and provide ongoing revenue streams that extend beyond the operational life of individual mining projects.

The effective tax rate on mineral operations reflects Brazil's competitive position relative to other mining jurisdictions worldwide. Excessive taxation can reduce investment attractiveness, while insufficient taxation fails to capture appropriate public benefits from resource extraction activities that deplete non-renewable national assets.

Labour Market Economics and Regional Development

The mineral sector provided 229,312 direct employment positions as of November 2025, excluding petroleum and natural gas operations. Between January and November 2025, the sector created 8,330 new formal employment positions, demonstrating continued expansion despite global economic uncertainties.

Employment multiplier effects extend far beyond direct mining jobs to include transportation workers, equipment maintenance specialists, professional services providers, and retail establishments serving mining communities. Economic studies typically estimate employment multipliers ranging from 2.5 to 4.0 additional jobs for each direct mining position, depending on regional economic integration levels.

Skill premium analysis reveals that mining operations typically offer wages significantly above regional averages, particularly for technical positions requiring specialised training. This wage premium attracts workers from other sectors and stimulates local economic development through increased consumer spending and business investment.

Regional wage differentials created by mining operations can transform local economies while potentially creating labour shortages in other sectors. Effective workforce development policies must balance mining industry needs against broader regional economic development objectives.

Which Market Dynamics Will Shape Brazil's Mineral Export Future?

Future market conditions will determine whether Brazil can maintain and expand its mineral export competitiveness against evolving global supply and demand patterns.

Demand-Side Economic Projections

Chinese infrastructure demand remains the primary driver for Brazilian iron ore exports, with steel production capacity and urbanisation rates directly influencing commodity consumption. China's economic transition toward services and technology sectors may reduce steel intensity per unit of GDP growth, potentially constraining long-term iron ore demand growth.

European green transition initiatives create significant demand opportunities for critical minerals essential to renewable energy deployment, electric vehicle manufacturing, and industrial decarbonisation. The European Union's strategic autonomy objectives motivate diversification away from concentrated suppliers, creating market access opportunities for Brazilian producers.

North American supply chain diversification efforts, particularly regarding critical minerals for defence and technology applications, represent substantial market opportunities. Trade policy developments and bilateral cooperation agreements could enhance Brazil's access to premium pricing in North American markets.

Supply-Side Capacity Economics

Production capacity utilisation rates across major Brazilian mining operations currently support volume expansion without requiring massive new project development. However, maintaining competitive cost structures requires continuous productivity improvements and technological adoption to offset labour cost increases and resource depletion effects.

Brownfield expansion projects typically offer superior economic returns compared to greenfield developments due to existing infrastructure, established workforces, and reduced permitting complexity. Brazil's mature mining operations provide numerous opportunities for capacity expansion through brownfield investments that leverage existing assets.

Technology adoption impacts productivity gains through automated equipment, advanced processing techniques, and optimisation systems that reduce operational costs while improving safety performance. Digital mining technologies, including autonomous vehicles and remote monitoring systems, represent investment priorities that enhance long-term competitiveness.

How Do Environmental Economics Influence Mining Investment Decisions?

Environmental considerations increasingly influence capital allocation decisions as investors, regulators, and communities demand sustainable mining practices that minimise ecological impact while maintaining economic viability.

ESG Investment Premium Analysis

Environmental, Social, and Governance (ESG) criteria create both costs and benefits for mining operations. Companies demonstrating superior environmental performance often access capital at lower interest rates, command premium valuations in equity markets, and secure preferential treatment in government permitting processes.

Carbon pricing mechanisms, whether through direct taxation or cap-and-trade systems, add operational costs that favour energy-efficient operations and renewable energy adoption. The mining sustainability transformation involves mining companies investing in clean energy systems and emission reduction technologies position themselves advantageously for potential future carbon pricing implementations.

Water usage economics become increasingly important as climate change and competing demands create water scarcity in certain regions. Mining operations requiring extensive water consumption must invest in recycling systems, alternative water sources, and efficiency improvements that reduce environmental impact while controlling operational costs.

Circular Economy Integration Opportunities

Mineral recycling markets offer emerging opportunities for companies willing to invest in processing technologies that recover valuable materials from waste streams. Urban mining initiatives that extract metals from electronic waste and industrial byproducts could provide additional revenue sources while reducing environmental impact.

Waste-to-resource conversion technologies enable mining companies to generate value from previously discarded materials. Tailings reprocessing, slag utilisation, and byproduct recovery systems can improve overall project economics while reducing environmental liabilities.

Secondary mineral recovery from existing operations often provides attractive investment returns through relatively low capital requirements and reduced permitting complexity compared to new extraction projects. These opportunities become increasingly valuable as primary ore grades decline and environmental standards tighten.

Frequently Asked Questions About Brazil's Mineral Export Economics

What percentage of Brazil's trade surplus comes from mineral exports?

Brazil's mineral sector accounted for 55% of the country's total trade surplus in 2025, contributing US$ 37.6 billion out of US$ 68.3 billion in total surplus. This represents a significant increase from 47% in 2024, demonstrating the growing importance of minerals to Brazil's international trade balance.

Historical analysis reveals fluctuating contributions ranging from 35% to 60% over the past decade, depending on commodity price cycles and global demand conditions. Future projections suggest continued dominance, though the percentage may vary based on iron ore price movements and critical mineral market development.

Compared to other commodity-dependent economies like Australia, Chile, and Peru, Brazil's 55% contribution falls within the typical range for major mineral exporters, though it represents higher concentration than more diversified economies.

Which minerals offer the highest economic returns for Brazil?

Iron ore currently generates the largest absolute revenue at R$ 157.2 billion, but critical minerals demonstrate superior growth potential with 15.2% projected investment increases compared to 11.8% for traditional mining operations.

Profit margin analysis indicates that specialised minerals requiring processing capabilities typically command higher per-tonne returns than bulk commodities. Value-added processing opportunities in copper, nickel, lithium, and rare earth elements offer potential for margin expansion beyond raw material extraction.

Export price premiums for processed versus raw materials can range from 15% to 50%, depending on the specific mineral and level of processing. Brazil's investment in downstream processing capabilities could significantly enhance revenue per tonne across multiple mineral categories.

How vulnerable is Brazil's economy to global mineral price fluctuations?

Brazil's 62.8% concentration in iron ore exports creates significant exposure to steel industry cycles and Chinese demand patterns. A 10% decline in iron ore prices typically impacts total mineral exports Brazil revenues by approximately 5-6%, given iron ore's dominant contribution to sector income.

Economic sensitivity analysis indicates that sustained commodity price declines exceeding 20% could reduce mineral sector contributions to trade surplus by 25-30%, significantly impacting Brazil's overall balance of payments and government fiscal revenues.

Hedging strategies employed by major mining companies include forward sales contracts, options positions, and production flexibility that can moderate short-term price impacts. However, sustained price downturns require operational adjustments including cost reduction, production optimisation, and investment timing modifications.

Strategic Economic Outlook for Brazil's Mineral Sector Through 2030

Investment Pipeline Economic Impact Assessment

The US$ 76.9 billion investment pipeline through 2030 represents transformative potential for Brazil's mineral sector and broader economy. Economic multiplier analysis suggests these investments could generate additional GDP contributions ranging from US$ 115 billion to US$ 150 billion through direct, indirect, and induced economic effects across supplier industries and consumer spending.

Regional development acceleration opportunities concentrate in Minas Gerais and Pará, where the majority of investment capital will be deployed. These investments can fund infrastructure improvements that benefit multiple economic sectors while creating permanent employment opportunities that extend beyond mining operations.

Technology transfer and innovation ecosystem development represent additional benefits from international investment partnerships and advanced equipment procurement. Mining technology improvements often find applications in other industries, creating spillover benefits that enhance overall economic productivity.

Global Market Position Strengthening Strategies

Brazil's competitive positioning requires continuous enhancement across multiple dimensions including cost efficiency, product quality, logistics capabilities, and sustainable practices. Value chain integration opportunities enable capture of processing margins while reducing dependence on commodity price fluctuations.

Strategic partnerships with major consuming nations provide market access security while creating opportunities for technology sharing and infrastructure development cooperation. Long-term supply agreements can provide revenue predictability that supports investment planning and operational optimisation.

Competitive positioning against emerging mineral exporters in Africa, Asia, and other regions requires maintaining cost advantages while improving product quality and delivery reliability. Brazil's established infrastructure and political stability provide competitive advantages that must be preserved through continued investment and policy stability.

Disclaimer: This analysis is based on data from the Instituto Brasileiro de Mineração (IBRAM) and reflects market conditions as of February 2026. Mineral market projections involve significant uncertainty due to commodity price volatility, global economic conditions, and geopolitical developments. Investment decisions should consider comprehensive due diligence and professional financial advice. Economic forecasts and multiplier effects represent estimates that may not reflect actual future performance.

Ready to Capitalise on the Next Major Mineral Discovery?

Discovery Alert instantly alerts investors to significant ASX mineral discoveries using its proprietary Discovery IQ model, turning complex mineral data into actionable insights just like those driving Brazil's R$ 298.8 billion mineral export success. Understand why major mineral discoveries can lead to substantial market returns by exploring Discovery Alert's dedicated discoveries page and begin your 14-day free trial today to position yourself ahead of the market.