July 29, 2026

The global materials landscape faces unprecedented transformation as space economy applications drive demand for precision-engineered materials. Traditional terrestrial mining operations must now adapt to space-specific requirements that demand molecular-level precision and extreme performance characteristics. Furthermore, this evolution represents more than market expansion; it signals a complete recalibration of critical material supply chains worldwide.

The convergence of geopolitical tensions, technological breakthroughs, and unprecedented private capital deployment has created what financial strategists now recognise as a structural inflection point. However, asteroid mining advances demonstrate how this paradigm shift extends beyond terrestrial operations. Morgan Stanley's recent analysis positions five mining companies in space economy supply chains as uniquely positioned to capitalise on this transformation, though the implications extend far beyond simple commodity exposure.

Understanding the Critical Materials Foundation of Space Infrastructure

The materials science requirements for space applications fundamentally differ from terrestrial counterparts in ways that reshape entire mining value propositions. Space-grade materials must withstand temperature differentials exceeding 500 degrees Celsius, radiation exposure levels thousands of times greater than Earth-based environments, and mechanical stresses that would destroy conventional components.

Essential Metals That Power Space Technology

Copper's thermal management capabilities become exponentially more critical in space environments where heat dissipation occurs solely through radiation. Advanced propulsion systems require copper with purity levels exceeding 99.9%, processed under controlled atmospheric conditions that eliminate trace contaminants. Moreover, the material specifications for rocket engine components demand thermal conductivity values that only copper market insights reveal can be consistently delivered through specialised mining operations.

Aluminium alloy engineering for spacecraft applications involves metallurgical processes far removed from standard industrial production. Space-qualified aluminium requires specific grain structures, controlled cooling rates, and alloying elements that enhance performance in vacuum conditions. Consequently, the weight-to-strength ratios demanded by orbital mechanics create premium markets for aerospace-grade materials that command pricing multiples over commodity grades.

Rare earth elements enable magnetic field generation and electronic systems that function reliably across extreme temperature ranges. Neodymium, dysprosium, and terbium concentrations must meet specifications measured in parts per million, requiring mining operations with sophisticated separation and purification capabilities. In addition, the magnetic properties essential for satellite orientation systems and rover mobility depend on rare earth compositions achievable through highly specialised processing techniques.

Tungsten applications in space environments exploit the material's unique combination of high density, temperature resistance, and radiation absorption characteristics. Deep space missions require tungsten components that maintain structural integrity at temperatures approaching 3,400 degrees Celsius, creating demand for mining operations capable of producing ultra-pure tungsten powder and specialised alloys.

Gallium semiconductor properties enable advanced radar systems and high-frequency communication equipment essential for space-based operations. The material's low melting point and unique electronic characteristics create applications in satellite communication arrays and planetary exploration equipment that require gallium with controlled impurity levels measured in parts per billion.

Supply Chain Vulnerabilities in Space-Critical Materials

Geographic concentration risks in critical materials production create potential bottlenecks that could constrain space industry expansion. Current rare earth element production remains heavily concentrated in specific regions, with processing capabilities even more geographically constrained than raw material extraction. For instance, this concentration creates strategic vulnerabilities that a critical raw materials facility must address through diversified supply chains.

Processing bottlenecks for aerospace-grade materials often represent more significant constraints than raw material availability. The technical requirements for space-qualified materials demand specialised facilities, trained personnel, and quality control systems that cannot be rapidly scaled. Therefore, mining industry evolution shows that companies positioning for space economy growth must invest in processing capabilities that can meet aerospace specifications whilst maintaining cost competitiveness.

Strategic stockpiling considerations for national space programmes introduce additional demand variables that traditional commodity analysis often underestimates. Government procurement patterns for critical materials follow strategic rather than economic optimisation, creating demand stability that partially insulates suppliers from commodity price volatility while generating premium pricing for certified space-grade materials.

When big ASX news breaks, our subscribers know first

How Are Traditional Mining Companies Positioning for Space Market Growth?

The strategic repositioning of established mining companies toward space economy exposure reflects fundamental changes in how materials demand patterns are evolving. Traditional mining operations built around terrestrial industrial applications must now consider space-specific requirements that demand different extraction, processing, and quality control approaches.

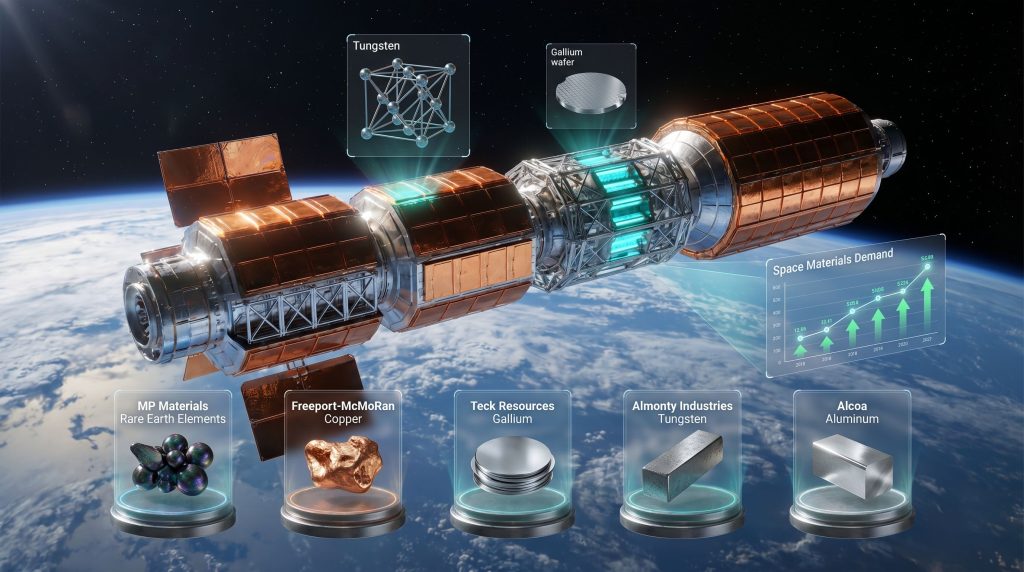

North American Mining Leaders in Space Supply Chains

| Company | Primary Material | Space Applications | Strategic Advantage |

|---|---|---|---|

| MP Materials | Rare Earth Elements | Satellite magnets, guidance systems | US domestic production capacity |

| Freeport-McMoRan | Copper | Rocket engines, thermal management | Global extraction infrastructure |

| Teck Resources | Copper, Gallium | Propulsion systems, radar technology | Diversified material portfolio |

| Almonty Industries | Tungsten | Radiation shielding, high-temperature components | Non-Chinese production base |

| Alcoa | Aluminium | Structural frameworks, spacecraft components | Established aerospace relationships |

The selection criteria for space-focused mining investments extend beyond traditional metrics of reserves, production capacity, and operating costs. Space economy positioning requires assessment of processing capabilities, quality certification systems, and ability to meet aerospace specifications that command premium pricing but demand significant capital investment in specialised equipment and quality control systems.

Investment Thesis Behind Space-Focused Mining Strategies

Morgan Stanley's analytical framework positions space economy exposure as a multi-decade growth theme rather than a cyclical commodity play. The bank's research suggests that space-related demand could fundamentally alter pricing dynamics for critical materials, creating sustained premium markets that justify higher valuation multiples for properly positioned mining companies.

Market capitalisation potential driven by space economy exposure reflects investor recognition that traditional commodity valuation models may underestimate the strategic value of companies controlling supply chains for space-critical materials. Furthermore, the anticipated SpaceX valuation exceeding US$2 trillion demonstrates how space economy growth could create derivative value throughout supply chains, including upstream mining operations.

Diversification benefits for traditional mining portfolios include reduced correlation with terrestrial industrial cycles and exposure to government and strategic procurement patterns that provide demand stability. Space-focused mining investments offer portfolio diversification that extends beyond geographic or commodity-specific risk mitigation.

What Makes These Five Companies Strategic for Space Economy Growth?

MP Materials: America's Rare Earth Independence Strategy

MP Materials operates as the sole US rare earth producer, controlling the Mountain Pass facility that represents America's only operational rare earth extraction and processing capability. This positioning creates strategic value that extends beyond traditional mining economics, as national security considerations increasingly influence rare earth procurement patterns.

The company's production capacity for rare earth elements positions it to benefit from growing demand for high-performance magnets used in satellite systems, planetary rovers, and launch vehicle guidance systems. Space applications require rare earth elements with purity specifications that demand sophisticated separation and processing technologies that MP Materials has developed specifically for aerospace applications.

Strategic positioning advantages include:

• Domestic supply security for US space programmes

• Processing capabilities for aerospace-grade rare earth elements

• Established quality certification for satellite and defence applications

• Capacity expansion potential aligned with projected space industry growth

• Premium pricing power for specialised rare earth formulations

Recent capacity expansion initiatives suggest management recognition of space economy growth potential, though specific investment allocations toward space-grade processing capabilities require monitoring through operational updates and capital expenditure guidance.

Freeport-McMoRan and Teck Resources: The Copper Connection

Freeport-McMoRan's global copper operations provide scale and geographic diversification essential for serving space industry demand patterns that may differ significantly from traditional industrial applications. The company's copper production capabilities span multiple continents, creating supply chain resilience that space industry customers increasingly value.

Teck Resources offers dual exposure through both copper and gallium production, creating unique positioning for companies requiring multiple critical materials from certified suppliers. The combination of copper for thermal management systems and gallium for advanced radar applications provides integrated supply chain solutions that aerospace customers prefer.

Technical specifications for space applications include:

• High-purity copper (>99.9% purity) for rocket engine components

• Controlled atmosphere processing to eliminate contamination

• Specialised alloy formulations for extreme temperature environments

• Gallium semiconductor grades for advanced communication systems

• Traceability documentation meeting aerospace quality standards

The copper demand from space applications represents a premium market segment that commands higher prices than commodity copper, though volumes remain relatively small compared to traditional industrial demand. However, the growth trajectory and pricing stability of space-related copper demand create strategic value for mining companies capable of meeting aerospace specifications.

Almonty Industries: Tungsten Beyond Earth

Almonty Industries operates as the largest tungsten producer outside China, with facilities in Europe and South Korea that provide geographic diversification away from Chinese tungsten dominance. This positioning becomes strategically important as space programmes seek supply chain security for critical materials.

Tungsten applications in space environments exploit the material's unique properties:

• High-temperature performance up to 3,400°C for propulsion systems

• Radiation shielding capabilities for deep space missions

• Density characteristics for specialised aerospace applications

• Corrosion resistance in extreme space environments

• Mechanical stability under thermal cycling conditions

The company's production capabilities include tungsten powder metallurgy and specialised alloy production that meet aerospace specifications. Space industry demand for tungsten represents a premium market with limited supplier competition, creating pricing power for companies with established aerospace relationships.

Strategic considerations for tungsten in space applications include long-term supply agreements with aerospace contractors, government strategic stockpiling requirements, and potential demand growth from lunar base construction and deep space exploration missions that require extensive radiation shielding.

Alcoa: Aerospace Aluminium Excellence

Alcoa's aerospace industry relationships span decades, providing established customer connections and technical expertise that position the company for space economy growth. The company's aluminium production capabilities include specialised alloys designed specifically for aerospace applications that meet stringent performance requirements.

Space-qualified aluminium requires:

• Controlled alloy compositions optimised for weight-to-strength ratios

• Specialised heat treatment for enhanced performance characteristics

• Quality control systems meeting aerospace certification standards

• Traceability documentation for component tracking and safety compliance

• Manufacturing scale capable of supporting large satellite constellations

The company's processing capabilities extend beyond raw aluminium production to include value-added manufacturing services that aerospace customers increasingly demand. This vertical integration creates competitive advantages and higher margin opportunities compared to commodity aluminium production.

Structural applications in space vehicles require aluminium with specific grain structures, controlled cooling rates, and mechanical properties that maintain integrity across extreme temperature ranges. Alcoa's technical expertise in aerospace aluminium production positions the company to capitalise on growing space industry demand.

How Does Space Economy Demand Differ from Traditional Mining Markets?

Quality Specifications and Processing Requirements

Aerospace-grade material standards impose requirements that fundamentally differ from traditional industrial specifications. Space applications demand materials with controlled impurity levels, documented traceability, and performance characteristics verified through extensive testing protocols that add significant value and complexity to mining operations.

Key differentiation factors include:

• Contamination control during extraction and processing

• Quality certification through aerospace industry standards

• Traceability systems tracking materials from mine to application

• Performance testing under simulated space conditions

• Documentation requirements for safety and regulatory compliance

Processing infrastructure for space-grade materials requires specialised equipment, controlled environments, and technical expertise that represents significant capital investment beyond traditional mining operations. Companies positioning for space economy growth must evaluate whether their existing processing capabilities can be adapted or whether new facility investments are required.

Volume Projections and Market Growth Scenarios

Current space industry material demand remains relatively small compared to traditional industrial applications, but growth projections suggest potential for significant market expansion over the next decade. Satellite constellation deployments, commercial space tourism development, and government space exploration programmes create multiple demand drivers with different timing and volume characteristics.

Demand growth scenarios consider:

• Satellite mega-constellations requiring thousands of units annually

• Commercial space stations demanding specialised materials

• Lunar exploration missions with unique material requirements

• Mars programme development creating long-term demand projections

• Space tourism infrastructure requiring safety-certified materials

Manufacturing capacity expansion timelines must align with projected space industry growth to avoid either insufficient supply capabilities or excess capacity investment. Mining companies require strategic planning that balances space economy exposure with traditional market stability.

What Investment Opportunities Exist in Space-Focused Mining?

Thematic Investment Portfolio Construction

Space-focused mining investments offer portfolio diversification that extends beyond traditional commodity exposure whilst providing participation in space economy growth themes. Investment strategies must balance the growth potential of space applications with the fundamental mining company characteristics of operational efficiency, reserve quality, and financial stability.

Portfolio construction considerations:

• Geographic diversification across mining operations

• Material diversification spanning multiple critical elements

• Processing capability assessment for aerospace applications

• Financial stability evaluation for long-term investment horizons

• Management expertise in both mining operations and aerospace markets

Risk management across commodity price cycles requires understanding how space-related demand patterns differ from traditional industrial cycles. Energy transition insights demonstrate how space industry growth may provide partial insulation from commodity price volatility whilst creating new risk factors related to technology development and aerospace industry dynamics.

Competitive Positioning Analysis

Barriers to entry in space-grade material production include technical expertise, processing capabilities, quality certification systems, and established customer relationships that create competitive advantages for properly positioned mining companies. These barriers provide downside protection for investments whilst limiting competitive threats from new market entrants.

Long-term supply agreements with aerospace contractors create revenue stability and predictability that enhances investment attractiveness compared to spot commodity market exposure. Space mining companies often prefer supplier relationships that provide supply security over pure cost optimisation, creating opportunities for premium pricing and long-term partnerships.

Research and development partnerships between mining companies and aerospace contractors can create technological advantages and market access that enhance competitive positioning. Companies investing in space-specific material development may gain first-mover advantages in emerging applications.

Future Scenarios: Mining's Role in Space Economy Expansion

2030 Demand Projections and Supply Readiness

Satellite constellation deployment schedules suggest material demand could increase significantly over the next decade, with multiple companies planning mega-constellations requiring thousands of satellites annually. This demand growth would stress existing supply chains and potentially create material shortages that benefit properly positioned mining companies.

Projected demand drivers include:

• Global internet satellite networks requiring standardised components

• Earth observation systems demanding specialised sensor materials

• Communication satellite replacements with enhanced capabilities

• Defence satellite programmes requiring security-certified suppliers

• Commercial space stations creating new material applications

Supply readiness assessment must consider both raw material availability and processing capacity capable of meeting aerospace specifications. Mining companies require strategic planning that anticipates space industry growth whilst maintaining financial discipline in capacity expansion decisions.

Geopolitical Considerations in Space Materials

National security implications of material sourcing increasingly influence space industry procurement patterns, creating opportunities for mining companies operating in politically stable jurisdictions with allied government relationships. Strategic material independence becomes more important as space capabilities gain military and economic significance.

International cooperation in space exploration programmes may create multinational procurement frameworks that benefit mining companies with diversified geographic operations and established quality certifications. Trade policy impacts on critical material access require ongoing monitoring as governments develop space industry strategies.

Strategic reserve planning for space applications may create government stockpiling demand that provides market stability and premium pricing opportunities for mining companies capable of meeting aerospace specifications and security requirements.

The next major ASX story will hit our subscribers first

Key Takeaways for Investors and Industry Stakeholders

Risk Assessment Framework

Technology development uncertainties in space applications create both opportunities and risks for mining companies positioning for space economy growth. Material requirements may evolve as space technologies advance, potentially obsoleting current specifications whilst creating demand for new material formulations.

Primary risk factors include:

• Technology substitution reducing demand for specific materials

• Regulatory changes affecting space industry development

• Market timing mismatches between investment and demand growth

• Competitive threats from alternative suppliers or materials

• Economic cycles affecting space industry investment patterns

Regulatory environment evolution requires monitoring as governments develop frameworks for space commerce, material sourcing, and safety standards that may create new requirements or opportunities for mining companies.

Strategic Positioning Recommendations

Portfolio allocation strategies for space economy exposure should balance growth potential with risk management through diversified mining investments that provide multiple pathways for space industry participation. Concentration risk in single companies or materials may expose investors to technology or market development risks.

Due diligence considerations must evaluate both traditional mining company fundamentals and space-specific capabilities including processing technology, quality certification, customer relationships, and management expertise in aerospace markets. Furthermore, Morgan Stanley's mining analysis provides insights into how these five mining companies in space economy supply chains are positioned for long-term growth.

Long-term value creation opportunities require strategic thinking about how space economy development may reshape materials demand patterns over multi-decade timeframes. Mining companies with early positioning advantages may capture disproportionate value as space industry growth accelerates.

Monitoring indicators for market development include space industry funding levels, satellite launch schedules, government space programme budgets, and materials pricing trends that signal demand growth or supply constraints. Investment decisions require ongoing assessment of how space economy development aligns with mining company positioning and capabilities.

This analysis is for informational purposes only and does not constitute investment advice. Space economy development involves significant uncertainties, and mining company investments carry inherent risks including commodity price volatility, operational challenges, and market development timing. Investors should conduct thorough due diligence and consider their risk tolerance before making investment decisions.

Ready to Position Yourself Ahead of the Space Economy Boom?

Discovery Alert's proprietary Discovery IQ model delivers instant notifications on significant ASX mineral discoveries, including those companies positioning for space-critical material demand that could drive the next wave of mining sector growth. With space economy applications creating unprecedented demand for precision-engineered materials, subscribers gain immediate insights into actionable discovery opportunities that position portfolios ahead of transformative market shifts.