August 1, 2026

The mining and metals forecast 2026 reveals that commodity markets operate within intricate webs of macroeconomic forces, geopolitical tensions, and technological disruptions that create both opportunities and challenges for investors navigating the complex mining and metals landscape. As global economies transition toward renewable energy systems while simultaneously managing inflationary pressures and supply chain vulnerabilities, the mining industry finds itself at the center of competing demands that will define market dynamics throughout 2026 and beyond.

The intersection of monetary policy normalisation, decarbonisation investment requirements, and resource nationalism creates a unique environment where traditional market mechanisms interact with state-directed industrial policies. Understanding these forces becomes essential for stakeholders seeking to position themselves effectively in an increasingly strategic sector where geological constraints meet geopolitical realities.

What Economic Forces Will Shape Mining and Metals Markets in 2026?

Global Monetary Policy Transitions and Commodity Pricing

The completion of the Federal Reserve's rate-cutting cycle represents a pivotal shift in global commodity pricing dynamics. Following 100 basis points of rate reductions during 2024, from 5.25-5.50% to 4.25-4.50%, the Fed's current positioning in the 4.00-4.25% range signals the end of accommodative monetary expansion that historically supported precious metals demand.

Central bank gold purchasing reached 1,037 tonnes in 2024, marking the second-highest annual level on record according to World Gold Council data. This institutional demand reflects ongoing currency diversification strategies, even as gold prices exceeded $2,700 per ounce in late 2024. However, the monetary policy transmission mechanism typically requires 12-18 months to fully impact commodity markets, suggesting potential price pressure for precious metals in the second half of 2026.

Currency volatility amplifies these effects across global mining operations. The U.S. Dollar Index experienced 8-12% volatility throughout 2024-2025, directly affecting production costs for operations outside the United States. Mining companies in emerging markets face particular challenges as local currency weakness increases the relative cost of dollar-denominated equipment and materials whilst potentially improving export competitiveness.

Key Monetary Policy Implications:

- Real 10-year Treasury yields stabilising around 1.8-2.2% continue supporting gold demand

- Policy divergence between Federal Reserve and European Central Bank creates cross-currency volatility

- Institutional commodity allocation strategies increased 23% year-over-year through Q3 2025

Decarbonisation Investment Flows and Capital Allocation

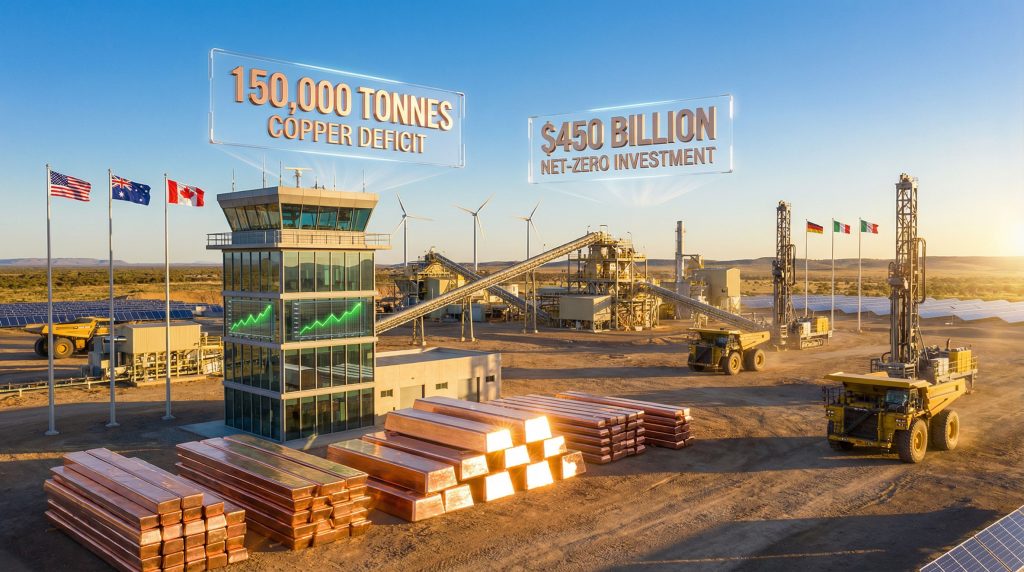

The global transition toward net-zero emissions requires unprecedented capital deployment in mining infrastructure. Industry estimates suggest $450 billion in mining investment will be necessary through 2030 to meet decarbonisation targets, with critical minerals energy transition materials experiencing particularly strong demand elasticity.

Carbon pricing mechanisms increasingly influence operational cost structures across major mining jurisdictions. European Union carbon credits trading above €80 per tonne create direct costs for energy-intensive processing operations, whilst similar schemes in Canada and proposed U.S. systems add complexity to project economics. These mechanisms favour operations with renewable energy integration and penalise high-carbon extraction methods.

Green financing availability has expanded significantly, with specialised funds targeting critical mineral projects offering preferential terms for operations meeting specific environmental criteria. However, this capital often comes with stringent reporting requirements and operational restrictions that traditional mining finance does not impose.

The International Energy Agency projects copper demand growth of 3.6% annually through 2030 for clean energy applications alone, requiring cumulative production increases of approximately 8.2 million tonnes over five years. Furthermore, the mining decarbonisation benefits create premium pricing opportunities for strategically positioned producers.

When big ASX news breaks, our subscribers know first

How Will Supply-Demand Imbalances Drive Market Dynamics?

Critical Mineral Deficit Projections

Supply constraints across critical minerals have reached levels that fundamentally alter market pricing mechanisms. The International Copper Study Group confirms annual demand growth of 3.0-3.5% whilst production declined 1.2% in 2024 despite elevated prices, highlighting the structural nature of current imbalances.

2026 Supply-Demand Gap Analysis

| Mineral | Projected Deficit | Key Demand Drivers | Primary Supply Constraints |

|---|---|---|---|

| Copper | 150,000 tonnes | Grid infrastructure, EVs | Grade decline, aging mines |

| Lithium | 40,000 tonnes LCE | Battery storage, automotive | Processing bottlenecks |

| Rare Earths | 15% shortage | Wind turbines, magnets | Geographic concentration |

| Nickel | 85,000 tonnes | Stainless steel, batteries | Indonesian export restrictions |

| Cobalt | 12,000 tonnes | Battery cathodes | Democratic Republic of Congo instability |

Lithium markets demonstrate the complexity of modern mineral supply chains. Global production reached approximately 130,000 tonnes of lithium carbonate equivalent in 2024, whilst demand approached 170,000 tonnes LCE. However, the constraint lies not in raw mineral availability but in processing capacity, which operates at 85-90% utilisation in key markets including China, Chile, and Australia.

Rare earth elements face even more severe geographic concentration challenges. China controls approximately 70% of global processing capacity despite holding only 35-40% of proven reserves. Wind turbine permanent magnet demand requires 8-12% annual growth through 2030, with neodymium and dysprosium facing the tightest supply conditions according to International Renewable Energy Agency assessments.

Ore Grade Deterioration Economics

The mining industry confronts a fundamental challenge as accessible high-grade deposits become increasingly scarce. Copper ore grades have declined 40% since 1991, from approximately 1.5% to 0.7% by 2024. This degradation creates cascading effects throughout the production chain that extend far beyond simple cost increases.

Lower-grade ore processing requires approximately 2.1 times more ore to extract equivalent copper tonnage compared to 1991 levels, assuming similar recovery rates. Energy requirements increase by 45-60% per tonne of ore processed, whilst water consumption and environmental footprints expand proportionally. These factors contribute to the 40-50% increase in average capital expenditure for new copper projects from 2015-2025.

Technological Adaptation Requirements:

- Heap leach technology now requires 0.8-1.0% efficiency improvements through enhanced acid treatment

- Solvent extraction and electrowinning represents 28% of global copper production, up from 18% in 2010

- Underground expansion projects like Escondida's $5.6 billion development demonstrate capital intensity escalation

- Custom processing solutions become necessary for marginal ore bodies

The industry's response involves both technological advancement and operational restructuring. Escondida's underground expansion in Chile, requiring $5.6 billion compared to $1.8 billion for comparable projects in 2010, illustrates how deeper deposits demand specialised infrastructure and ventilation systems that dramatically increase development costs.

Which Geopolitical Strategies Will Reshape Resource Security?

Industrial Policy Competition Between Major Economies

Resource security has evolved from market-driven procurement to state-directed strategic positioning. The European Union's Critical Raw Materials Act, which entered force in September 2024, establishes explicit targets for domestic production and processing that fundamentally alter global supply chain economics.

EU Critical Raw Materials Act Key Provisions:

- 10% of critical raw materials needs through domestic EU production by 2030

- Processing capacity targets: 40% for lithium and cobalt; 25% for rare earths

- Recycling targets: 25% by 2030, rising to 50% by 2040

- Traceability requirements creating 2-4% compliance costs for non-EU suppliers

The United States implements parallel strategies through Section 45X of the Inflation Reduction Act, providing tax credits up to $35 per kilogram for domestically produced critical minerals including lithium, cobalt, nickel, and rare earths. The Strategic and Critical Materials Stock Pile programme received $500 million in funding through FY2025 for strategic mineral stockpiling.

These policies create competitive advantages for aligned operations whilst penalising non-compliant supply chains. Projects designated as "strategic" under EU regulations receive accelerated permitting timelines of 18-24 months versus standard 36-48 month processes. Consequently, significant first-mover advantages emerge for properly positioned operations.

Resource Nationalism and Trade Policy Evolution

Mining-dependent nations increasingly assert control over their mineral resources through revised ownership structures, taxation frameworks, and export restrictions. Peru increased mining royalty rates from 2-3% to 3-5% in 2024, with ongoing discussions for further increases to 8-10% for copper projects.

Mongolia restricted foreign ownership in new mining ventures to maximum 49% in 2023, whilst Zambia renegotiated agreements to increase government stakes from 20-25% to 35-40%. In addition, trade war impacts continue affecting global supply chain security and mineral pricing strategies.

China's resource security strategy combines domestic capacity expansion with strategic overseas investments under clarified regulatory frameworks. The Ministry of Commerce requires government pre-approval for outbound investments exceeding $50 million in rare earths, lithium, and cobalt sectors. Simultaneously, China has implemented export restrictions on refined rare earths, permanent magnets, and rare earth alloys, controlling 65-70% of global processing capacity.

Strategic Partnership Structures Emerging:

- Bilateral agreements establishing preferential trade terms for critical minerals

- Offtake agreements including "stability clauses" guaranteeing price floors and volumes for 10-15 years

- Technology-sharing arrangements linking resource access to technological cooperation

- Joint venture requirements ensuring technology transfer and local capacity building

What Investment Patterns Will Define Sector Capital Allocation?

M&A Activity Concentration in Energy Transition Metals

Merger and acquisition activity increasingly focuses on assets strategic to the energy transition, with deal valuations reflecting premium pricing for copper, lithium, and rare earth properties. Companies prioritise brownfield development opportunities that offer faster production timelines and reduced regulatory complexity compared to greenfield projects.

Collaboration between mining companies and downstream users has intensified as supply security concerns drive vertical integration strategies. Technology, automotive, and aerospace companies increasingly seek direct relationships with mineral producers through offtake agreements, joint ventures, and strategic investments that bypass traditional commodity trading mechanisms.

Investment Capital Allocation Trends:

- Brownfield expansions preferred over greenfield development for timeline advantages

- Risk-adjusted returns favour existing asset optimisation over new discoveries

- Cross-sector partnerships linking mineral supply to end-user applications

- Regulatory approval complexity favouring established operational jurisdictions

The shift toward strategic partnerships reflects recognition that traditional spot market procurement cannot guarantee supply security for critical applications. For instance, gold and copper exploration projects increasingly attract long-term agreements from battery manufacturers, renewable energy developers, and electric vehicle producers.

Brownfield vs. Greenfield Development Economics

Capital efficiency considerations strongly favour expansion of existing operations over new mine development. Brownfield projects typically achieve production 3-5 years faster than comparable greenfield developments whilst requiring 30-40% less capital investment per unit of production capacity. This timeline compression becomes critical as demand growth outpaces traditional development cycles.

However, brownfield expansion strategies face limitations as easily accessible ore bodies become exhausted. Companies must balance short-term capital efficiency against long-term reserve replacement requirements, creating tension between immediate cash flow optimisation and sustainable production growth.

Mine discovery rates have declined significantly, with only 2-3 major copper deposits discovered annually in recent years compared to 8-10 in the 1990s. This exploration challenge compounds the preference for brownfield development but raises concerns about industry sustainability as existing deposits approach depletion.

How Will Operational Complexity Drive Cost Structures?

Technological Innovation Requirements for Productivity

Mining operations increasingly rely on advanced technologies to maintain productivity as geological conditions become more challenging. Additionally, AI transforming mining operations shows potential for 30-40% cost reduction through improved target identification and drilling optimisation.

Digital Technology Investment Priorities:

- IoT sensor networks for real-time operational monitoring

- Machine learning algorithms for ore grade prediction and processing optimisation

- Automated haulage systems reducing labour requirements and improving safety

- Remote monitoring capabilities enabling centralised operational control

Underground automation adoption accelerates as labour constraints and safety requirements drive technological solutions. Autonomous drilling systems, remote-operated loaders, and automated transportation networks become standard equipment for new underground developments, requiring substantial capital investment but offering operational advantages in challenging environments.

The integration of renewable energy systems presents both opportunities and challenges for mining operations. Whilst solar and wind power can reduce operational costs in suitable locations, the intermittent nature of renewable generation requires investment in battery storage systems or hybrid generation approaches that increase capital complexity.

Workforce Transformation and Skills Premium

The mining industry faces a significant demographic challenge as approximately 50% of the North American workforce approaches retirement eligibility over the next decade. This experience drain coincides with 10% workforce expansion requirements in Australian mining operations, creating unprecedented labour market tightness.

Specialised skills for deep mining operations command premium wages that significantly impact project economics. Technical positions requiring underground expertise, geological interpretation, and equipment maintenance increasingly face supply constraints that drive compensation levels well above general industrial wages.

Workforce Development Investment Requirements:

- Technical training programmes for specialised underground operations

- Cross-training initiatives to improve workforce flexibility

- Safety certification programmes for automated equipment operation

- Mentorship programmes to transfer institutional knowledge before retirements

Companies must simultaneously invest in workforce development whilst implementing automation technologies that reduce long-term labour requirements. This dual approach requires careful balance to maintain operational continuity during the transition period whilst building capabilities for future operations.

What Climate Resilience Factors Will Affect Operational Viability?

Water Scarcity and Energy Security Planning

Mining operations increasingly confront water availability constraints that affect both operational feasibility and social licence to operate. Chile's Atacama Desert lithium operations face regulatory pressure to reduce water consumption, whilst copper mines in Arizona and Nevada implement increasingly sophisticated water recycling systems to maintain production levels.

Renewable energy integration offers long-term cost advantages but requires substantial upfront investment and technical adaptation. Solar installations at mining sites must account for dust accumulation, equipment durability, and integration with existing electrical systems. Wind power faces similar technical challenges whilst offering different operational profiles that may better match continuous mining power requirements.

Climate Resilience Investment Areas:

- Water recycling and treatment systems reducing freshwater requirements

- Renewable energy generation with battery storage for operational continuity

- Climate risk assessment integration into long-term planning processes

- Extreme weather event preparedness and response systems

Energy security planning becomes critical as mines increasingly rely on renewable sources that may not provide the same reliability as traditional grid connections. Hybrid systems combining renewable generation, battery storage, and backup power sources require complex engineering solutions tailored to specific operational requirements.

ESG Performance Integration into Financial Metrics

Environmental, social, and governance performance increasingly affects access to capital and operational approvals. Financing availability correlates strongly with sustainability performance metrics, with green bonds and ESG-focused investment funds offering preferential terms for operations meeting specific environmental criteria.

Tailings management represents a particular focus area following high-profile failures that highlighted industry risks. Advanced monitoring systems, alternative storage methods, and improved closure planning require significant investment but become essential for maintaining operational licences and accessing capital markets.

Carbon footprint reduction pathways demand operational changes that affect cost structures across mining operations. From equipment electrification to processing optimisation, emissions reduction strategies require capital investment whilst potentially improving long-term operational efficiency through energy optimisation and waste reduction.

The next major ASX story will hit our subscribers first

Which Regional Markets Will Experience the Strongest Growth?

Frontier Market Investment Risk-Return Profiles

Emerging mining jurisdictions offer significant resource potential but require careful risk assessment regarding political stability, regulatory frameworks, and infrastructure development requirements. Resource nationalism probability assessments become essential evaluation criteria as governments increasingly assert control over strategic mineral resources.

Infrastructure development requirements for new projects in frontier markets can exceed mine development costs in established jurisdictions. Transportation systems, power generation, water supply, and telecommunications infrastructure may require substantial investment before mining operations become viable, extending development timelines and capital requirements.

Frontier Market Evaluation Criteria:

- Political stability metrics affecting long-term project viability

- Regulatory framework clarity and consistency over time

- Infrastructure development costs and timeline requirements

- Currency hedging strategies for emerging market operations

The Democratic Republic of Congo's cobalt resources illustrate both the potential and challenges of frontier market development. Despite containing approximately 70% of global cobalt reserves, operational challenges including infrastructure limitations, regulatory uncertainty, and security concerns create significant risk premiums that affect project economics.

Developed Market Reshoring Economics

OECD countries increasingly prioritise domestic mining capacity development through policy incentives and regulatory streamlining. However, higher labour costs, stricter environmental regulations, and more complex permitting processes create cost disadvantages that require policy support to achieve economic viability.

Processing capacity expansion in developed markets faces similar challenges but benefits from proximity to end-users and reduced supply chain vulnerability. Lithium processing facilities in North America and Europe receive substantial government support through tax incentives and loan guarantees that improve project economics despite higher operational costs.

Strategic stockpiling programmes affect demand patterns by creating government purchasing programmes that provide price floors and volume commitments. The U.S. Strategic and Critical Materials Stock Pile and similar programmes in other developed nations create market stability that encourages private investment in domestic production capacity.

How Will Technology Disruption Accelerate Industry Transformation?

Equipment Market Evolution and Capital Requirements

The global mining equipment market projects growth to $81.58 billion by 2030, driven by technological advancement requirements and fleet modernisation needs. Electric vehicle adoption in mining fleets accelerates as battery technology improves and charging infrastructure develops, though implementation requires significant capital investment and operational adaptation.

According to industry analysis, metal prices are expected to continue rising through 2026, driven by sustained demand and supply constraints. Hydrogen fuel cell technology pilot programmes demonstrate potential for heavy mining equipment applications where battery weight becomes prohibitive. Whilst still in early development stages, hydrogen systems offer advantages for continuous-duty applications and rapid refueling requirements that characterise mining operations.

Equipment Technology Investment Priorities:

- Electric and hydrogen fuel cell powertrains for mobile equipment

- Autonomous navigation systems for improved safety and productivity

- Predictive maintenance sensors and analytics for equipment optimisation

- Integrated communication systems for remote monitoring and control

Custom underground equipment development increasingly addresses specific operational requirements that standard industrial equipment cannot meet. Narrow-vein mining, deep underground operations, and challenging geological conditions require specialised solutions that command premium prices but offer operational advantages justifying the investment.

Digital Infrastructure Investment Priorities

Internet of Things implementation across mining operations creates massive data streams requiring sophisticated analytics platforms and communication systems. Real-time monitoring of equipment performance, ore grade analysis, and environmental conditions enables operational optimisation but requires substantial digital infrastructure investment.

Cybersecurity investment requirements escalate as mining operations become increasingly connected and dependent on digital systems. Remote monitoring capabilities, automated control systems, and integrated supply chain management create potential vulnerabilities that require comprehensive security frameworks protecting both operational continuity and proprietary information.

Data analytics platform integration offers opportunities for operational optimisation through machine learning applications that improve decision-making processes. Ore grade prediction, equipment maintenance scheduling, and production optimisation algorithms require both technical expertise and substantial data processing capabilities that justify significant technology investment.

What Market Scenarios Should Investors Prepare For?

Base Case: Cautious Optimism Realisation

The most probable scenario for the mining and metals forecast 2026 involves 2% demand growth moderation from 2024-2025 levels as economic growth stabilises and energy transition deployment proceeds at steady but not accelerated pace. Price appreciation across most mineral categories reflects supply constraint persistence despite technological advancement and brownfield expansion efforts.

Gradual supply constraint resolution through technology adoption and operational optimisation provides modest production increases without eliminating structural deficits. Stable geopolitical environments support international trade flows whilst resource nationalism continues affecting specific jurisdictions rather than creating systemic disruptions.

Base Case Scenario Characteristics:

- Moderate demand growth across energy transition minerals

- Steady price appreciation reflecting supply-demand fundamentals

- Technology adoption improving operational efficiency gradually

- Political stability supporting established trade relationships

This scenario favours diversified mining companies with strong operational capabilities and strategic positioning in critical minerals markets. Investment returns likely reflect steady appreciation rather than dramatic price volatility, supporting long-term capital allocation strategies focused on operational excellence.

Risk Scenarios: Downside Protection Strategies

China's property sector prolonged weakness represents the primary downside risk for base metals markets. Further deterioration in real estate development could reduce steel and copper demand by 5-8% globally, creating oversupply conditions that pressure prices despite supply constraints in other applications.

Trade war escalation between major economies could disrupt critical mineral flows and create artificial scarcity in specific markets whilst simultaneously reducing demand in others. Furthermore, mining sector prospects remain cautiously optimistic, with tariff increases, export restrictions, and strategic stockpiling potentially fragmenting global markets and increasing price volatility significantly.

Risk Mitigation Strategies:

- Geographic diversification across multiple mining jurisdictions

- End-market diversification beyond single application areas

- Currency hedging for operations in volatile monetary environments

- Flexible production systems capable of responding to demand changes

Climate event disruption to major mining operations becomes increasingly probable as extreme weather events intensify. Flooding, drought, extreme temperatures, and severe storms can halt production for extended periods whilst requiring substantial recovery investments that affect long-term project economics.

Upside Scenarios: Acceleration Opportunities

Faster-than-expected energy transition deployment could create demand surges that exceed current projections by 20-30% for critical minerals. Government policy acceleration, breakthrough battery technologies, or rapid electric vehicle adoption could create supply shortages that drive significant price appreciation across energy transition materials.

Breakthrough mining technology commercialisation could dramatically reduce extraction costs and expand economically viable resources. Advanced ore processing, improved recovery rates, or novel extraction methods could alleviate supply constraints whilst maintaining healthy profit margins for efficiently operated facilities.

Upside Scenario Catalysts:

- Government policy acceleration supporting faster energy transition

- Technology breakthroughs improving mining productivity substantially

- Geopolitical stability encouraging increased infrastructure investment

- Demand surge from emerging technology applications requiring critical minerals

Geopolitical stability combined with coordinated international cooperation could unlock investment flows to developing mining jurisdictions whilst reducing political risk premiums. Infrastructure development partnerships and multilateral investment frameworks could accelerate project development timelines and reduce capital requirements.

Conclusion

The mining and metals forecast 2026 indicates cautious optimism will characterise market conditions, with price support from decarbonisation demand and supply constraints balanced against operational complexity challenges requiring significant technology investment and workforce development strategies for sustainable growth.

"The intersection of energy transition demands and geological constraints creates unprecedented opportunities for mining companies positioned to navigate technological advancement whilst managing operational complexity increases."

Note: This analysis incorporates publicly available information and industry forecasts. Investment decisions should consider individual risk tolerance and consult qualified financial advisers. Market conditions and regulatory environments may change, affecting projections and recommendations contained herein.

Ready to Capitalise on Critical Mineral Discoveries Before the Market?

Discovery Alert provides instant notifications on significant ASX mineral discoveries, powered by its proprietary Discovery IQ model that transforms complex mining announcements into actionable insights within minutes. With critical mineral supply deficits intensifying through 2026 and major discoveries offering exceptional return potential, positioning yourself ahead of market-moving announcements through Discovery Alert's dedicated discoveries page could provide the competitive advantage necessary to capitalise on the next transformative mineral discovery.