June 17, 2026

The Mining Production Cycle: Strategic Value Creation in Commodity Markets

The global mining industry operates on multi-year production cycles where temporary output reductions often signal strategic positioning rather than operational weakness. Understanding these patterns becomes critical for investors seeking to decode complex capital allocation decisions in volatile commodity markets. Furthermore, gold's historic surge has intensified focus on production planning strategies. Mining companies frequently sacrifice short-term volume metrics to optimise long-term value creation through deliberate operational sequencing, infrastructure development, and grade optimisation strategies.

Modern mining enterprises must balance immediate shareholder returns against substantial capital requirements for maintaining and expanding operations across decades-long mine lives. This dynamic creates periodic troughs in production profiles that can mislead surface-level analysis while representing calculated positioning for enhanced future performance.

When big ASX news breaks, our subscribers know first

Strategic Mine Sequencing: The Architecture of Production Planning

Mining operations require sophisticated sequencing strategies to maintain sustainable production over extended time horizons. Newmont 2026 production dip represents a coordinated approach across multiple assets, demonstrating how integrated portfolio management creates temporary volume reduction for long-term optimisation.

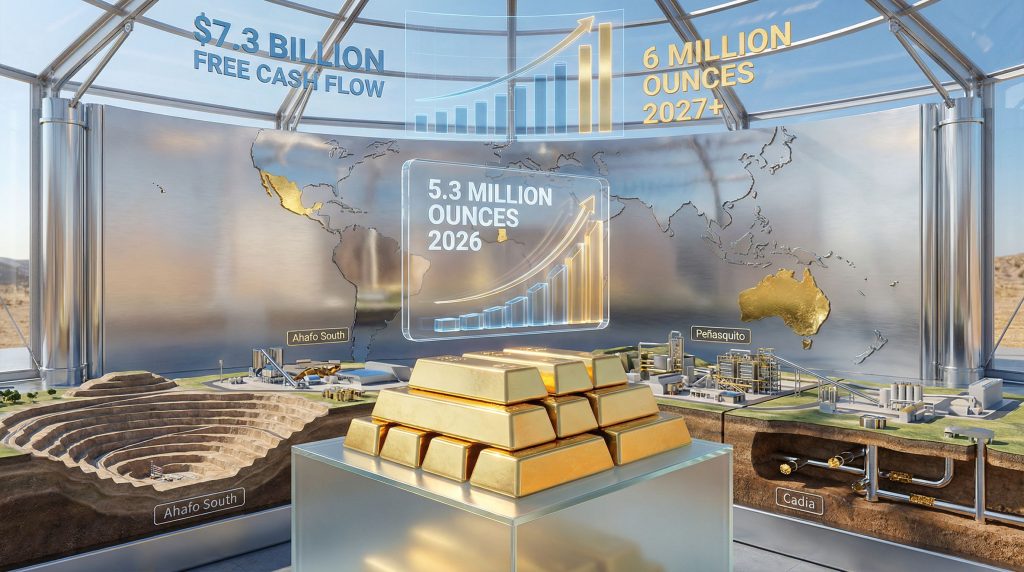

The company plans to produce 5.3 million attributable ounces in 2026, representing a deliberate reduction from 2025's 5.9 million ounces. This 600,000-ounce decrease reflects synchronised operational transitions rather than market pressures or operational challenges.

Key Operations in Transition

Ahafo South (Ghana): Transitioning between mining phases to access higher-grade ore zones requires careful timing to maintain processing capacity while advancing pit development. This sequencing approach maximises long-term grade profiles rather than maintaining consistent short-term volumes.

Peñasquito (Mexico): Coordinating waste stripping operations with processing optimisation creates temporary production impacts while positioning the operation for improved efficiency and grade access in subsequent years.

Cadia (Australia): Advanced panel cave development continues alongside current production maintenance, requiring significant capital allocation and operational coordination to ensure seamless transitions between mining methods. Additionally, infrastructure recovery insights demonstrate how mining operations can successfully navigate major transitions.

Boddington (Australia): Recovery from December bushfire impacts demonstrates operational resilience capabilities, with critical infrastructure repairs enabling full processing resumption after environmental disruptions.

Production Recovery Timeline

The strategic nature of the Newmont 2026 production dip becomes evident through management's clear recovery projections:

- 2027: Return to approximately 6 million ounces annually

- 2028+: Sustained production growth supported by development projects

- Long-term: Integration of 150,000 tonnes annual copper production

This trajectory represents roughly 13% production growth from the 2026 trough, demonstrating the temporary nature of the planned reduction.

Capital Deployment Strategy: Building Future Production Capacity

Newmont's capital allocation framework reflects sophisticated long-term planning, with $3.35 billion in combined development and sustaining investments annually. This substantial commitment demonstrates confidence in portfolio optimisation despite near-term production constraints.

Development Capital Allocation: $1.4 Billion

| Project | Strategic Focus | Timeline Impact | Long-term Value |

|---|---|---|---|

| Cadia Panel Caves | Underground expansion | Mine life to 2050+ | 25+ years operational extension |

| Tanami Expansion 2 | Processing capacity | H2 2027 production | Australian portfolio strengthening |

| Red Chris Feasibility | Copper-gold integration | 2028+ diversification | Base metals exposure |

The Cadia panel caves development represents particularly significant strategic value, extending mine life into the middle of the century and providing operational sustainability through multiple commodity cycles.

Sustaining Capital Investment: $1.95 Billion

Sustaining capital focuses heavily on tailings facility upgrades at Cadia and Boddington, representing proactive infrastructure management. This investment category addresses critical long-term operational requirements while maintaining regulatory compliance and environmental stewardship standards.

Tailings management represents one of the mining industry's most significant long-term liabilities, making proactive facility upgrades essential for operational sustainability and risk mitigation.

Financial Performance Excellence: Record Cash Generation Metrics

Despite production planning constraints, Newmont achieved exceptional financial performance in 2025, generating $7.3 billion in free cash flow from $10.3 billion in operating cash flow. This performance demonstrates operational excellence and strategic price realisation during favourable market conditions.

Key Financial Metrics

- Free Cash Flow: $7.3 billion (record achievement)

- Operating Cash Flow: $10.3 billion

- Q4 Free Cash Flow: $2.8 billion

- Net Income: $7.2 billion

- Adjusted Net Income: $7.6 billion ($6.89 per share)

Cost Management Discipline

Gold by-product All-In Sustaining Costs (AISC) of $1,358 per ounce demonstrates cost discipline during strong commodity price environments. However, 2026 guidance projects AISC increasing to $1,680 per ounce, reflecting operational sequencing costs and anticipated inflationary pressures.

This $322 per ounce increase represents the cost impact of strategic mine sequencing decisions, illustrating how operational optimisation can temporarily affect unit cost metrics while positioning for long-term value creation. Consequently, data-driven operations become increasingly important for cost management.

Co-product AISC of $1,609 per ounce provides alternative cost metrics for operations producing multiple commodities, offering insight into portfolio diversification benefits.

Balance Sheet Transformation

The company's evolution to a $2.1 billion net cash position represents significant balance sheet strengthening, supported by:

- $7.6 billion in cash

- $11.6 billion total liquidity

- $3.4 billion debt reduction during 2025

- $4.5 billion in divestiture proceeds from portfolio optimisation

This financial flexibility provides strategic options for growth investments, acquisition opportunities, and market volatility management.

Portfolio Optimisation and Shareholder Returns

Newmont's approach to shareholder value creation balances growth investment with direct returns, returning $3.4 billion to shareholders through dividends and share repurchases during 2025. The enhanced quarterly dividend of $0.261 per share reflects confidence in sustainable cash generation capabilities.

Strategic Divestiture Program

The completion of noncore asset divestitures generated $4.5 billion in after-tax proceeds, demonstrating disciplined portfolio management. For instance, ongoing mining industry consolidation trends support such strategic decisions. This capital redeployment strategy focuses resources on highest-return opportunities while maintaining operational flexibility.

Management's satisfaction with the existing portfolio despite merger and acquisition speculation indicates confidence in organic growth potential through the established development pipeline.

Operational Resilience and Risk Management

Mining operations face diverse operational risks requiring sophisticated management approaches. Newmont's experience with the December bushfires at Boddington illustrates both vulnerability and resilience capabilities within large-scale mining operations.

Infrastructure Recovery Capabilities

The Boddington bushfire response demonstrates operational resilience through:

- Rapid assessment of critical infrastructure damage

- Coordinated repair of water supply infrastructure

- Full processing operations resumption

- Minimal long-term operational impact

This incident provides valuable insight into mining operations' vulnerability to environmental events and the importance of robust emergency response capabilities.

Nevada Gold Mines Joint Venture Challenges

The 38.5%-owned Nevada Gold Mines joint venture with Barrick Gold presents ongoing performance challenges. Management's issuance of a notice of default regarding operational performance indicates significant concerns about this substantial portfolio component.

Current discussions focus on performance improvements rather than structural changes, suggesting confidence in the asset's underlying value while acknowledging operational execution issues. In addition, the CEO perspective on gold mining provides valuable context for such strategic decisions.

The next major ASX story will hit our subscribers first

Long-term Growth Catalysts and Development Pipeline

Newmont's development pipeline provides multiple growth catalysts extending well beyond the Newmont 2026 production dip. These projects demonstrate the company's strategic positioning for sustained long-term value creation.

Phase 1 Development (2026-2027)

- Ahafo North ramp-up completion: Full production capacity achievement

- Boddington stripping campaign conclusion: Access to higher gold and copper grades from 2027

- Tanami Expansion 2 delivery: Enhanced processing capacity in H2 2027

Phase 2 Expansion (2027-2030)

- Cadia panel caves operational integration: Seamless transition to underground mining methods

- Enhanced copper production from Boddington: Diversified commodity exposure

- Lihir nearshore barrier project advancement: Access to substantial additional reserves

Strategic Value Drivers

The Lihir nearshore barrier project represents exceptional long-term value, providing access to over 5 million ounces and extending mine life beyond 2040. This single project demonstrates the portfolio's capacity for multi-decade operational sustainability.

Combined with other development initiatives, these projects provide a clear path to renewed production growth supported by disciplined capital allocation and integrated portfolio management.

Market Position and Competitive Dynamics

As the world's largest gold producer, Newmont's production decisions influence global supply dynamics. The planned 2026 reduction of approximately 600,000 ounces creates potential market tightness during a period of sustained gold price strength.

This market position provides pricing leverage while requiring careful balance between volume optimisation and market share maintenance. The company's ability to generate record cash flow while managing planned production reductions demonstrates operational excellence and strategic market positioning.

According to industry analysis, Newmont's strategic positioning continues to strengthen despite temporary production constraints. Furthermore, earnings performance has consistently exceeded market expectations.

Commodity Diversification Strategy

Beyond gold production, the portfolio includes significant silver and copper production, with 2025 output of 28 million ounces of silver and 135,000 tonnes of copper. Long-term targets include 150,000 tonnes annual copper production, providing valuable diversification against single-commodity price volatility.

Investment Implications and Strategic Outlook

The Newmont 2026 production dip represents calculated strategic positioning rather than operational weakness. The combination of record cash generation, strategic project investments, and disciplined capital allocation creates a foundation for sustained growth through the next production cycle.

The company's ability to generate $7.3 billion in free cash flow while managing a planned production reduction demonstrates operational excellence and strategic foresight that positions it advantageously for long-term value creation in global gold markets.

Key Investment Considerations

- Temporary production reduction enables long-term optimisation

- Record cash generation provides financial flexibility

- Strategic project pipeline supports multi-year growth trajectory

- Strong balance sheet enables opportunistic capital deployment

- Operational resilience demonstrated through challenge recovery

The strategic production reduction, combined with substantial development investments, positions Newmont for enhanced performance when production returns to targeted levels in 2027 and beyond. This approach prioritises long-term value creation over short-term volume metrics, aligning with disciplined capital allocation principles during favourable commodity price environments.

Management's confidence in the recovery trajectory, supported by specific project timelines and production targets, provides clear visibility into the company's strategic direction through the current production cycle and into sustained long-term growth.

Want to Identify the Next Major Mining Discovery?

Discovery Alert's proprietary Discovery IQ model provides real-time alerts on significant ASX mineral discoveries, helping subscribers identify actionable opportunities before they become mainstream market knowledge. Begin your 14-day free trial today and discover why strategic positioning in emerging mineral discoveries can generate exceptional returns for both short-term traders and long-term investors.