June 6, 2026

When Policy Stability Becomes a Competitive Weapon

In global resource markets, what a government doesn't do can matter just as much as what it does. Capital allocation decisions for long-duration mining projects, which commonly span 10 to 25 years from discovery to depletion, are acutely sensitive to sovereign risk. When a jurisdiction signals fiscal predictability, it competes more effectively for the pools of patient capital that underpin major mine development. The 2026-27 Australian Federal Budget, by leaving mining taxes unchanged faster approvals Australia at its core, sends precisely this kind of signal to international capital markets at a moment when competition for resources investment has rarely been more intense.

The budget's architecture is more coherent than a surface reading might suggest. Stable taxation, accelerated approvals, critical minerals and energy security commitments, fuel security, and domestic industrial capability investment are not isolated line items. Together, they represent a deliberate policy posture designed to strengthen Australia's position as a preferred destination for long-horizon resources capital, particularly in the critical minerals segment where the global energy transition is generating demand cycles that may persist for decades.

When big ASX news breaks, our subscribers know first

Australia's Mining Sector as a Fiscal Cornerstone

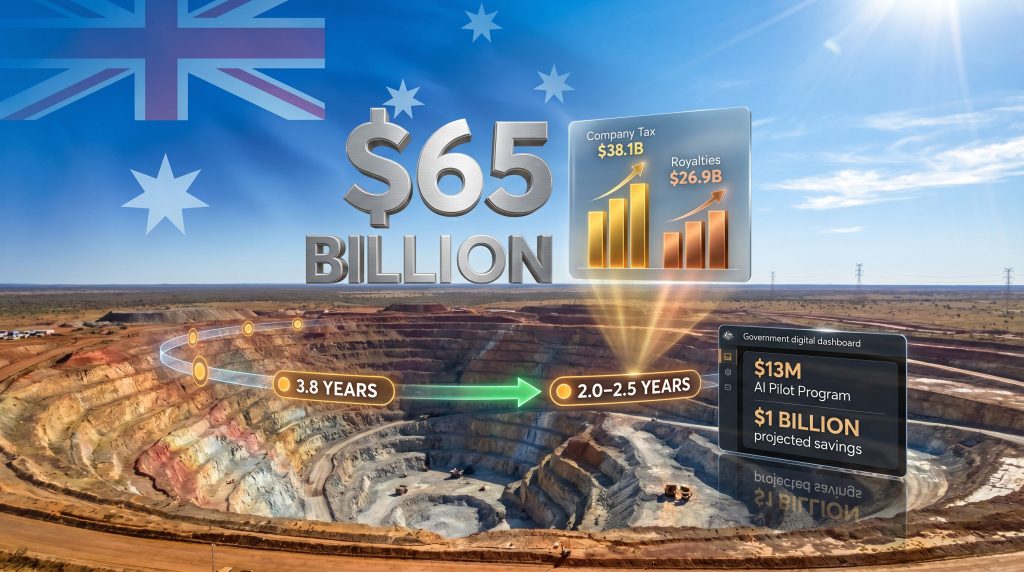

Before examining what changed, it helps to understand what is at stake. Australia's mining industry is not a peripheral contributor to national revenue. In 2023-24, the sector paid a combined $65 billion in company taxes ($38.1 billion) and state royalties ($26.9 billion), exceeding every other industry sector's fiscal contribution for the third consecutive year.

To place this in context, the prior year (2022-23) saw company tax contributions from mining reach $43.1 billion, illustrating that the sector's fiscal footprint has remained substantial even through softer commodity pricing environments. Furthermore, the WA resources sector economic impact alone underscores just how critical regional production is to national revenue.

Mining's share of total government revenue sits at approximately 5%, a figure that recurs frequently in policy debates about whether the sector is contributing proportionally to its economic presence. That debate is complicated by two factors: the $11 billion fuel tax credit scheme, which critics characterise as a subsidy to large operators, and data from 2021-22 showing that nearly half of large mining and energy companies reported zero net tax liability in that year, utilising available deductions within existing legal frameworks.

The mining sector's gross fiscal contribution is structurally significant, yet the effective rate debate remains unresolved. State royalty revenues in New South Wales alone have more than doubled to exceed $4 billion, illustrating how sub-national governments are capturing commodity upside through royalty mechanisms even where federal tax structures remain static.

The Tax Reform That Wasn't: Understanding the Post-MRRT Landscape

The last major structural reform to Australian mining taxation was the abolition of the Minerals Resource Rent Tax (MRRT) in 2014, which eliminated a projected $3.4 billion in four-year revenue. More than a decade later, no equivalent mechanism has been legislated, though reform proposals continue to circulate in policy discussions.

One hybrid model that received attention ahead of the 2026-27 Budget proposed a 20% rate for small-to-medium operators with revenue up to AU$1 billion, rising to 28% for larger producers, supplemented by a 5% net cashflow tax. Industry opposition has kept this off the legislative agenda as of 2026. The government's decision to proceed without introducing such a mechanism reflects a deliberate calculation: the revenue upside of structural reform is outweighed by the investment confidence cost during a period of critical minerals opportunity.

What did shift incrementally was a $3.7 billion adjustment in mining-specific levy structures, including changes to exploration deductibility. This represents targeted modification rather than systemic overhaul, and it is important for investors to understand the distinction. In addition, junior explorers funding measures reveal how the government is simultaneously trying to stimulate early-stage discovery alongside these structural settings.

A Snapshot of Australia's Current Tax Architecture

| Tax Mechanism | 2026 Status | Trajectory |

|---|---|---|

| Company Tax Rate (Mining) | Unchanged | Stable |

| State Royalties | Unchanged federally; rising at state level | Upward |

| Fuel Tax Credits | Retained | Under political scrutiny |

| Minerals Resource Rent Tax | Abolished (2014) | No reinstatement proposed |

| Hybrid Tax Reform Proposal | Discussed, not legislated | Stalled |

| Exploration Deductibility | Adjusted (~$3.7B impact) | Modified |

For investors modelling project economics, the key takeaway is that mining taxes remain unchanged at the federal level, removing a meaningful sovereign risk variable from near-term capital allocation decisions.

The $51 Billion Bottleneck: Why Approvals Reform Matters More Than Taxation

For many projects currently in development, approval timelines represent a more material risk than tax rates. Assessment timeframes under the Environment Protection and Biodiversity Conservation (EPBC) Act increased by 60% between baseline periods and 2025, reaching an average of 3.8 years per major project decision. The cumulative GDP cost of mining project delays attributable to this bottleneck is estimated at $51 billion, a figure that reframes the approvals conversation from administrative process to macroeconomic priority.

This is particularly acute for critical minerals. The pipeline of projects requiring federal environmental clearance has expanded substantially as the global energy transition accelerates demand for lithium, cobalt, nickel, graphite, and rare earth elements. Assessment capacity has not kept pace with this expansion, creating a structural mismatch that the 2026-27 Budget begins to address. Australia targets quicker mining approvals as a deliberate economic strategy, and this budget reinforces that direction.

Artificial Intelligence Enters the Approvals Workflow

The most technically novel initiative in the approvals reform agenda is a $13 million, three-year AI pilot program proposed at Minerals Week 2026 by the Minerals Council of Australia. The program aims to embed artificial intelligence directly into EPBC environmental decision-making workflows, targeting specific inefficiencies that have compounded assessment timelines:

- Elimination of manual document review bottlenecks that create lag between submission and substantive assessment

- Reduction in Requests for Further Information (RFIs), which are one of the most common sources of timeline extension

- Standardisation of assessment criteria to reduce inconsistency between decision-makers

- Projected long-term system savings of $1 billion across the approvals infrastructure

The program's ambition is that a first operational AI solution could be delivered within 12 to 20 weeks of program launch, drawing on proof-of-concept validation from comparable AI-assisted permitting tools already deployed in New South Wales and British Columbia, Canada.

It is worth noting that AI integration into regulatory processes does not resolve the legal standing of environmental and community stakeholders to challenge approvals. Administrative acceleration and litigation risk are separate variables, and no technology solution fully addresses the latter.

State-Level Reform: Where Practical Acceleration Is Already Occurring

Federal initiatives operate alongside meaningful state-level reforms that are already reshaping the project approval landscape for Australian miners.

Western Australia: Risk-Tiered Pathways Under the EMA Framework

Western Australia's Eligible Mining Activity (EMA) Framework, rolled out under the Mining Amendment Act 2022, introduces a risk-tiered classification system with practical implications for project timelines:

- Low-risk, routine mining activities are routed through an expedited administrative pathway, potentially compressing approval timelines from 12-18 months to 3-6 months for qualifying operations

- Higher-risk or complex proposals retain the requirement for full environmental assessment, preserving rigour where it is most needed

- The Mining Development and Closure Proposal (MDCP) mechanism merges previously separate mining proposals and mine closure plans into a single integrated document, eliminating duplicative processes that previously required sequential completion

- Single Approvals Statements now replace multiple compliance instruments, reducing the administrative load on operators across WA's resource-intensive regions

Queensland: Expedited Environmental Authorities for Critical Minerals

Queensland moved decisively in December 2025 with new guidelines establishing a dedicated expedited Environmental Authority (EA) pathway for critical minerals including graphite, copper, nickel, and rare earth elements. The accelerated pathway is not without conditions:

- Stricter proactive notification requirements apply, including mandatory complaint notification protocols as a condition of faster processing

- Industry participants have flagged a potential trade-off: timeline gains from the expedited pathway may be partially offset by reduced operational flexibility under the new conditions framework

- The net effect on project economics depends on the specific mineral, location, and community context of each operation

Critical Minerals, Stockpiling, and Strategic Resource Architecture

Perhaps the most strategically significant element of the 2026-27 Budget's mining policy package is the inclusion of critical minerals stockpiling as a distinct budget line item. This represents a philosophical shift: resource policy moving from purely commercial framing toward strategic resource security, a framework more commonly associated with defence procurement.

The global context matters here. Since 2022, the United States, European Union, Japan, and South Korea have all moved to establish or expand national critical minerals reserves in response to supply chain vulnerabilities exposed by geopolitical disruption. Australia's critical minerals strategic reserve formalisation aligns with this allied-nation trend and is reinforced by the G7 minerals alliance membership Australia secured through agreements with Canada in March 2026.

Fuel Security: Operational Risk Elevated to Strategic Priority

The Federal Government's commitment to a permanent fuel reserve, accompanied by modelling suggesting oil prices could reach $200 per barrel under stress scenarios, elevates fuel security from an energy market variable to a national infrastructure priority.

For the mining sector specifically, this has direct operational implications:

- Remote mining operations in Western Australia, Queensland, and the Northern Territory are heavily diesel-dependent, making fuel price volatility and supply disruption a first-order operational risk

- The fuel security agenda provides political durability to the existing fuel tax credit scheme. Eliminating an $11 billion credit mechanism during a period of deliberate strategic reserve-building would create an internally contradictory policy signal

- Operators in remote regions should monitor fuel reserve policy development as a potential buffer against the supply disruption scenarios underpinning the $200 per barrel stress modelling

The next major ASX story will hit our subscribers first

Investment Implications: Modelling the Value of Stability and Speed

For investors and project developers, the budget's combined effect on mining taxes unchanged faster approvals Australia can be translated into concrete project economics. However, understanding the full picture requires examining both timeline improvements and the tax stability that underpins them.

Scenario Analysis: What Approval Acceleration Is Worth

| Scenario | Current Average Timeline | Post-Reform Estimate | Primary Value Driver |

|---|---|---|---|

| Major Critical Minerals Project | 3.8 years | 2.0-2.5 years (projected) | Earlier cashflow, reduced holding costs |

| Low-Risk WA Operation (EMA Pathway) | 12-18 months | 3-6 months | Capital deployment acceleration |

| Queensland Critical Minerals EA | 18-24 months | 12-15 months (estimated) | Reduced opportunity cost |

The discount rate implications of these timeline improvements are not trivial. For a project with a 20-year mine life, accelerating first production by 12 to 18 months can meaningfully shift net present value calculations, even before accounting for the reduction in holding and carrying costs during the assessment period.

Tax stability contributes a different but complementary form of value. Long-duration mining investments are modelled against a range of policy scenarios, and sovereign risk premiums are applied where policy uncertainty is high. The government's explicit decision to leave the tax structure unchanged removes one category of downside scenario from investment models, which typically translates into a modest but real reduction in required hurdle rates.

Persistent Risks Investors Should Not Discount

The policy package has genuine strengths, but several structural tensions remain unresolved:

- The AI pilot program's effectiveness depends on data quality, system integration, and institutional willingness to act on algorithmic outputs. None of these are guaranteed within the 12-20 week delivery timeline

- Community and legal challenge pathways remain structurally unchanged. Even administratively accelerated approvals can be delayed by third-party legal action, particularly for projects with significant environmental footprints

- The hybrid tax reform proposal remains unlegislated but not abandoned. Operators planning beyond a five-year horizon carry residual uncertainty about whether structural reform re-enters the legislative agenda in a future budget cycle

- Downstream processing ambitions embedded in the budget's industrial capability measures require capital incentives that approvals reform alone cannot deliver

Furthermore, the Trump executive order mining permits framework in the United States is intensifying global competition for critical minerals investment, meaning Australia's policy settings must remain competitive on a comparative basis, not merely in isolation.

Frequently Asked Questions: Mining Taxes and Approvals in Australia

Are there new mining taxes in the 2026-27 Budget?

No new mining taxes were introduced in the 2026-27 Federal Budget. The government retained existing company tax rates, state royalty frameworks, and the fuel tax credit scheme while directing budget measures toward approvals acceleration and strategic resource security.

How much does the Australian mining sector pay in taxes and royalties?

In 2023-24, the sector paid a combined $65 billion, comprising $38.1 billion in company taxes and $26.9 billion in state royalties, exceeding every other industry sector's fiscal contribution for the third consecutive year. The Minerals Council of Australia has highlighted this contribution as evidence that the sector underpins national economic resilience.

What is causing delays in Australian mining project approvals?

EPBC Act assessment timeframes increased by 60% to reach an average of 3.8 years per major project decision by 2025. The structural mismatch between assessment capacity and a rapidly expanding critical minerals project pipeline is the primary driver.

What is the AI program for mining approvals?

A $13 million, three-year program proposed at Minerals Week 2026 to integrate artificial intelligence into EPBC environmental decision-making, targeting reductions in manual review bottlenecks, RFI volumes, and overall assessment duration, with projected long-term system savings of $1 billion.

What is Australia's G7 minerals alliance membership?

Through agreements signed with Canada in March 2026, Australia formalised membership in the G7 minerals alliance, positioning its critical minerals stockpiling and supply security initiatives within a multilateral framework alongside the United States, Canada, Japan, and European G7 members.

Is Australia's Mining Policy Architecture Fit for the Energy Transition?

Assessed holistically, the 2026-27 Budget's mining policy package represents deliberate consolidation rather than transformative reform. The fiscal settings that have made Australia one of the world's largest mining tax contributors are preserved. The operational bottleneck that has most directly constrained new investment is being targeted through both technology and administrative redesign.

The strengths are real and material:

- Fiscal predictability removes a key sovereign risk variable from long-duration investment modelling

- Multi-jurisdictional reform momentum at both federal and state levels is creating genuine pipeline acceleration across the critical minerals segment

- Strategic alignment between Australian policy, allied nation frameworks, and domestic industrial capability goals provides a coherent narrative for international capital allocation

- AI-driven efficiency gains offer scalable improvement potential without requiring primary legislation

The gaps are equally real:

- Environmental assessment rigour and community challenge rights remain structurally intact, meaning acceleration at the administrative level does not guarantee acceleration at the project delivery level

- The unresolved hybrid tax reform proposal creates residual medium-term uncertainty that disciplined investors will continue to model

- Downstream processing ambitions require capital incentive structures that go beyond approvals reform, and the budget's industrial capability measures may be insufficient to shift the calculus for marginal processing investment decisions

Consequently, for project developers and capital allocators assessing Australian critical minerals exposure, the 2026-27 framework offers a meaningfully improved operating environment. With mining taxes unchanged faster approvals Australia emerging as the country's primary competitive tools in the global race to attract energy transition investment, the long-term effectiveness of that positioning will depend on whether the AI pilot delivers, whether state-level reforms hold their shape under community scrutiny, and whether the downstream processing ambition eventually attracts the capital incentives it requires to move from policy aspiration to industrial reality.

This article contains forward-looking analysis and projections regarding policy timelines, GDP impacts, and investment scenarios. These represent estimates and analytical assessments, not guaranteed outcomes. Readers should conduct independent due diligence before making investment decisions based on any information contained in this article.

Want to Capitalise on Australia's Next Major Mineral Discovery Before the Broader Market?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts the moment significant ASX mineral discoveries are announced, transforming complex geological and commodity data into clear, actionable investment insights for both short-term traders and long-horizon investors. With Australia's approvals pipeline accelerating and critical minerals demand intensifying, explore Discovery Alert's discoveries page to understand the historic returns major mineral discoveries have generated, and begin your 14-day free trial today to position yourself ahead of the market.