May 20, 2026

When Mines Wake Up: The Strategic Logic Behind Hard Rock Lithium Restarts

Commodity markets punish patience and reward timing in equal measure. For hard rock lithium producers, the window between a prolonged price trough and the onset of a genuine demand recovery is one of the most consequential decision points in the mining cycle. Restart too early and capital bleeds into an unforgiving market. Wait too long and competitors capture the premium end of a price recovery that took years to rebuild. The announcement that MinRes to restart Bald Hill lithium mine in Western Australia in mid-2026 reflects precisely this kind of calculated market re-entry, and it carries implications that extend well beyond a single ASX filing.

When big ASX news breaks, our subscribers know first

The Lithium Price Cycle: From Euphoria to Correction to Recovery

Understanding why the Bald Hill restart matters requires revisiting where the lithium market has been. Between 2021 and late 2022, spodumene concentrate prices surged to levels that seemed to validate almost every lithium development thesis on the market. Battery demand from electric vehicles was accelerating, supply was structurally constrained, and the capital markets responded with a flood of investment into lithium projects at every stage of development.

What followed was a textbook commodity correction. Chinese lithium carbonate prices collapsed from historic highs, spodumene concentrate markets softened sharply, and producers across the hard rock and brine segments began cutting output or placing assets on care and maintenance. The lithium market downturn was driven by a combination of demand growth that came in below aggressive forecasts, inventory buildups across the Chinese conversion and battery supply chains, and a wave of new supply that had been unlocked during the boom years.

By late 2024 and into 2025, prices had stabilised at levels that made marginal production deeply uneconomic. For assets like Bald Hill, the rational response was capital preservation, not continued extraction at a loss.

What Spodumene Grade Classifications Actually Mean for Market Pricing

One piece of technical context that is often overlooked in mainstream coverage is the distinction between spodumene concentrate grades and how they translate into market value. Understanding spodumene extraction processes helps clarify why the two most commonly referenced benchmarks matter so significantly:

- SC6: Spodumene concentrate grading 6% lithium oxide (Li2O), the standard benchmark grade used for most pricing references in the industry.

- SC5.1: A lower-grade concentrate grading approximately 5.1% Li2O, which requires an adjustment factor when compared to SC6 pricing.

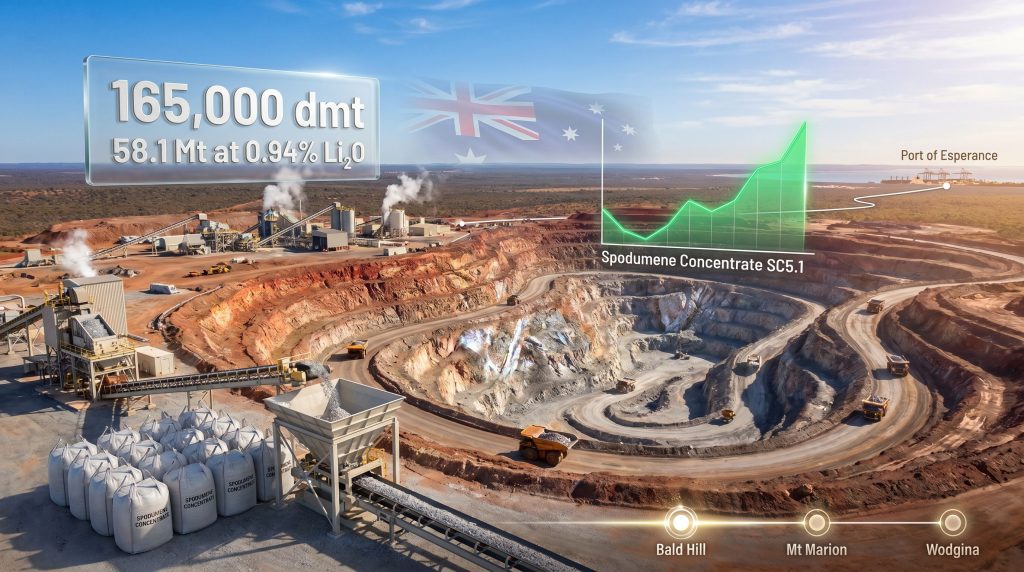

Bald Hill produces a 5.1% spodumene concentrate. This is not a deficiency in the asset but rather a function of the ore's mineralogical characteristics. The plant produces roughly 165,000 dry metric tonnes (dmt) per year of SC5.1 product, which converts to approximately 140,000 dmt SC6-equivalent annually. For downstream converters, the SC6-equivalent figure is what drives purchasing decisions, as conversion plants are calibrated to lithium oxide input grades rather than raw concentrate tonnages.

The reason this matters from an investor perspective is that SC5.1 pricing typically attracts a discount to the SC6 benchmark. The size of that discount fluctuates with market tightness. When supply is scarce, converters accept wider grade ranges with smaller price penalties. When supply is abundant, lower-grade concentrates face steeper discounts. A sustained recovery in lithium prices therefore benefits SC5.1 producers more than the headline SC6 price movement alone might suggest, because the discount narrows as converters compete for available tonnes.

Bald Hill Asset Profile: What MinRes Is Bringing Back Online

Location, Geology, and Infrastructure

Bald Hill sits approximately 50 kilometres south-east of Kambalda in Western Australia's Goldfields region, one of the most infrastructure-rich mining jurisdictions on the planet. The region has benefited from decades of gold and nickel mining investment, meaning road networks, power infrastructure, and skilled labour pools are far more accessible than at genuinely remote greenfield sites.

The asset's mineral resource stands at 58.1 million metric tonnes grading 0.94% Li2O, a substantial orebody by global hard rock lithium standards. The geological setting is within the broader Archaean granite-greenstone terrane that hosts many of Western Australia's major lithium deposits, where pegmatite-hosted spodumene mineralisation has proven both consistent and mineable at scale.

Export logistics flow through the Port of Esperance, which provides direct access to Asian converter markets without the need for costly transhipment arrangements. For producers selling into Chinese or South Korean conversion facilities, port proximity and reliable shipping schedules are meaningful cost variables.

Full Production Specifications at a Glance

| Metric | Specification |

|---|---|

| Annual Production Capacity | ~165,000 dmt of SC5.1 |

| SC6-Equivalent Output | ~140,000 dmt per year |

| Mineral Resource | 58.1 Mt at 0.94% Li2O |

| Care and Maintenance Period | November 2024 to May 2026 |

| Export Facility | Port of Esperance, Western Australia |

| Distance from Kambalda | 50 km south-east |

Why Care and Maintenance Is Strategically Different from Closure

A distinction that is frequently misunderstood outside the mining industry is the difference between placing an asset on care and maintenance versus permanently closing it. Care and maintenance involves:

- Retaining site infrastructure and processing equipment in a serviceable condition.

- Maintaining minimum staffing for safety, environmental compliance, and asset preservation.

- Preserving permits and approvals so that restart does not require full regulatory re-engagement.

- Keeping the mineral resource intact for reactivation when economics improve.

The financial cost of care and maintenance is real, but it is dramatically lower than the cost of full closure followed by eventual re-permitting and greenfield-style restart. MinRes placed Bald Hill into this holding pattern in November 2024 specifically to retain optionality over the orebody, and that decision has now paid off approximately 18 months later.

When a well-maintained asset can be restarted months rather than years after suspension, the effective cost of the care-and-maintenance period is often justified by the time-to-market advantage over competing development projects.

The Restart Sequence: Operational Milestones Explained

Phased Timeline from Ramp-Up to Full Capacity

The MinRes restart plan follows a sequenced approach that minimises operational risk during the transition from suspended to fully productive status. The key milestones are:

- Late May 2026: Site ramp-up activities commence; workforce mobilisation begins.

- June 2026: Mining and crushing operations initiated.

- July 2026: First spodumene concentrate production targeted.

- Q1 FY27: Initial spodumene concentrate shipment from the Port of Esperance.

- Q2 FY27: Full production capacity expected to be achieved.

The approximately two-month gap between the commencement of mining and the first shipment reflects the time required for processing plant commissioning, inventory accumulation to a shiploading threshold, and logistics coordination. For concentrate producers, the practical minimum shipment size is typically tied to vessel capacity, which for Handysize or Supramax bulk carriers commonly ranges from 25,000 to 55,000 tonnes. Building sufficient stockpile before the first shipment is therefore an operational constraint, not a planning failure.

The Vertical Integration Advantage

One of the less-discussed structural advantages MinRes carries into this restart is the role of its in-house Mining Services division. Rather than engaging external contractors for mining, crushing, haulage, and processing, MinRes deploys its own divisional capabilities across all operational phases. This model provides several concrete benefits:

- Cost control: Internal transfer pricing replaces external contractor margins, compressing the operating cost per tonne.

- Scheduling flexibility: Ramp-up timelines can be adjusted based on equipment redeployment from other MinRes operations without relying on third-party availability.

- Institutional knowledge: Crews who have previously worked on the asset or across MinRes sites arrive with existing familiarity with the equipment and geology.

- Risk reduction: A single integrated organisational structure reduces the coordination friction that commonly slows multi-contractor restart projects.

This vertical integration model is relatively uncommon in the mid-tier mining space, where most operators of comparable size rely heavily on external service providers for at least part of their operational chain.

The 370-Job Workforce Strategy: Redeployment as a Cost Lever

The restart is expected to generate approximately 370 positions across the Bald Hill operation. What makes this figure strategically interesting is the composition of that workforce. MinRes has indicated it will draw on a combination of new hires and redeployed personnel from elsewhere within its operational portfolio.

Internal redeployment serves a dual function. It reduces the recruitment costs and onboarding timelines associated with bringing in entirely external labour, and it preserves institutional knowledge within the broader MinRes workforce. For a company managing multiple simultaneous hard rock operations, the ability to flex labour across sites without losing experienced workers to the broader market is a meaningful operational advantage.

The regional employment impact in Western Australia's Goldfields is also notable. The area has faced varying levels of labour market pressure tied to commodity cycles, and a 370-person workforce addition from a single operation represents a material contribution to regional economic activity.

MinRes' Globally Rare Three-Mine Portfolio

What Operating Three Hard Rock Lithium Mines Simultaneously Actually Means

When Bald Hill returns to production, MinRes will be operating three separate hard rock lithium mines, each with its own dedicated spodumene concentrate processing infrastructure. This is, by any reasonable measure, an exceptional competitive position in the global lithium market.

| Asset | Status | Key Characteristic |

|---|---|---|

| Bald Hill | Restarting (2026) | 165,000 dmt/yr SC5.1 capacity |

| Mt Marion | Active | One of Australia's largest hard rock lithium mines |

| Wodgina | Active (Joint Venture) | Among the world's largest hard rock lithium deposits by resource size |

The significance of this portfolio extends beyond the raw production numbers. Operating three assets simultaneously means MinRes can offer customers blended supply arrangements, maintain commercial leverage in offtake negotiations, and absorb operational disruptions at one site without compromising overall delivery commitments. For a lithium converter assessing supply security, counterparty reliability across multiple operations is a more compelling proposition than a single-asset producer offering equivalent volume.

The combination of three independently processing hard rock operations under a single corporate structure is, to date, a globally unique position in the spodumene concentrate market. It creates a scale of supply optionality that most peers simply cannot replicate.

The next major ASX story will hit our subscribers first

Supply Chain Implications: What the Restart Signals for Global Spodumene Markets

How Mine Restarts Differ from New Project Supply

A restart of a production-ready, permitted asset like Bald Hill contributes supply to the market on a fundamentally different timeline than a greenfield development project. A new hard rock lithium mine typically requires:

- Three to seven years from resource definition to first production, depending on permitting complexity.

- Capital expenditure in the hundreds of millions to over one billion dollars for mine construction and processing plant installation.

- Multiple rounds of environmental assessment and community consultation before operations can commence.

By contrast, Bald Hill moves from care-and-maintenance suspension to first production in under two months, with initial shipments following roughly three to four months after the restart announcement. This speed advantage is why reactivated assets are consistently the first to respond to price recovery signals, and why they represent the most immediate supply-side risk to continued price appreciation during a recovery phase. Furthermore, Australia's lithium mining evolution continues to demonstrate how the sector adapts rapidly to shifting market conditions.

The Simultaneous Restart Risk: A Speculative Scenario

One scenario that deserves consideration, though it remains speculative at this stage, is the possibility that multiple suspended Australian lithium operations restart within the same 12-month window. The Australian hard rock sector saw a wave of curtailments in 2024, and if the price recovery that has prompted the MinRes to restart Bald Hill lithium mine decision is sustained, it may trigger parallel restart decisions at other mothballed operations.

If three or more suspended projects return to production simultaneously, the cumulative supply addition could be sufficient to dampen the price recovery that justified the restarts in the first place. This is not a novel dynamic in commodity markets, but it is worth monitoring closely. The structural demand signals from EV adoption and battery storage deployment provide a meaningful buffer, however timing mismatches between supply responses and demand growth have historically been a source of renewed price volatility in cyclical mineral markets.

Downstream: The Conversion Chain and Geographic Concentration Risk

Spodumene concentrate from Bald Hill feeds into a downstream processing chain that is heavily concentrated in China. Chinese lithium chemical converters dominate global lithium hydroxide and lithium carbonate production capacity, and the economics of that conversion step critically determine the net-back value that flows back to Australian spodumene producers.

This geographic concentration creates a structural dependency that the broader industry is beginning to address, though slowly. Interest in onshore Australian lithium processing has grown as both producers and governments explore supply chain diversification strategies. However, the capital intensity of conversion plant construction and the established competitive advantages of existing Chinese facilities mean that meaningful diversification of the conversion chain is a medium-to-long-term prospect rather than an imminent shift. In addition, the contrast between hard rock vs brine lithium processing pathways further underscores how geography shapes downstream economics.

Risk Factors: What Could Undermine the Restart Thesis

No investment thesis around a mine restart is complete without a clear-eyed assessment of the risks. The Bald Hill re-entry faces several identifiable headwinds:

- Price reversal risk: Lithium markets have surprised to the downside before. If SC6-equivalent prices retreat during the ramp-up phase, the economics of sustaining full production become more challenging.

- Processing yield uncertainty: The transition from care-and-maintenance to full production involves commissioning risks, particularly around plant throughput and metallurgical recovery rates in the early months.

- Labour availability: While MinRes has an internal workforce to draw upon, the competition for experienced mining personnel in Western Australia remains intense across the sector.

- Offtake market conditions: The geographic concentration of converting capacity in China means that bilateral trade tensions or Chinese domestic policy shifts can create demand disruptions for Australian spodumene producers.

- Simultaneous competitor restarts: As discussed above, a coordinated industry-wide restart could soften the price environment that is currently supporting the Bald Hill decision.

Disclaimer: This article contains forward-looking analysis and scenario modelling that involves assumptions about future market conditions, commodity prices, and operational outcomes. Such analysis is inherently uncertain and should not be construed as financial advice. Readers should conduct their own due diligence before making investment decisions.

Frequently Asked Questions: MinRes Bald Hill Lithium Mine Restart

When will Bald Hill lithium mine restart production?

Site ramp-up activities begin in late May 2026, mining and crushing commence in June 2026, and the first spodumene concentrate production is targeted for July 2026. Full capacity is expected to be achieved in Q2 FY27.

How long was Bald Hill on care and maintenance?

Bald Hill was placed on care and maintenance in November 2024 and remained suspended for approximately 18 months before the restart was announced in May 2026.

What is the production capacity of Bald Hill?

The operation has an annual production capacity of approximately 165,000 dry metric tonnes of 5.1% spodumene concentrate, equivalent to roughly 140,000 dmt SC6 per year.

How many jobs will the restart create?

Approximately 370 positions will be created, combining new hires with redeployment of existing MinRes personnel from other operations within the group.

Where does Bald Hill export its concentrate?

Spodumene concentrate is exported through the Port of Esperance in Western Australia, with the first shipment expected in Q1 FY27.

What is the mineral resource at Bald Hill?

The mineral resource is estimated at 58.1 million metric tonnes grading 0.94% Li2O.

Why is MinRes restarting Bald Hill now?

According to MinRes' official announcement, a sustained recovery in spodumene concentrate prices, underpinned by strengthening structural demand from the EV battery supply chain, has created the economic conditions necessary to justify reactivating the production-ready asset. The decision to see MinRes to restart Bald Hill lithium mine follows a disciplined care-and-maintenance strategy that preserved optionality throughout the downturn.

Key Takeaways: What the Bald Hill Restart Tells Us About Lithium in 2026

- The lithium market has shifted from a supply-surplus correction phase into a recovery cycle that is prompting production-ready assets to re-enter the market.

- Hard rock restart assets like Bald Hill respond to price signals far faster than any greenfield project can, making them the leading edge of supply-side recovery.

- MinRes' vertically integrated Mining Services model provides a structural cost buffer that makes the operation more resilient across price cycles than standalone producers.

- Operating three simultaneous hard rock lithium mines with dedicated processing infrastructure is a globally rare competitive position that provides commercial leverage in offtake negotiations.

- The pace and geographic distribution of lithium mine restarts across Australia in 2026 will be a critical variable in determining whether the current price recovery is sustained or softened by a new wave of supply additions.

- The SC5.1 versus SC6 pricing dynamic at Bald Hill means that the operation benefits disproportionately when market tightness compresses the grade discount, adding a secondary leverage mechanism to any SC6 benchmark price recovery.

The MinRes to restart Bald Hill lithium mine decision is most accurately understood not as a single operational event, but as a market signal from one of the sector's most operationally sophisticated producers that the structural case for hard rock lithium supply has re-established itself sufficiently to justify meaningful capital re-deployment.

Want to Track the Next Major ASX Lithium Discovery Before the Market Does?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries — instantly converting complex geological data into actionable investment insights for both short-term traders and long-term investors. Explore why well-timed discoveries have historically generated extraordinary returns on Discovery Alert's dedicated discoveries page, and start your 14-day free trial today to position yourself ahead of the next major market move.