May 14, 2026

The Geopolitics of Dependency: How Supply Shocks Are Redrawing Asia's Energy Map

When global energy supply chains fracture, the countries most exposed are rarely those making the headlines. They are the vast import-dependent economies quietly absorbing the cascading effects of conflicts fought thousands of kilometres from their borders. For a nation consuming energy at the scale India does, the arithmetic of vulnerability is stark: third-largest energy importer in the world, with crude oil, liquefied natural gas, and cooking gas representing the three arteries through which industrial output, household welfare, and economic stability flow.

The disruption to Gulf supply corridors caused by the US-Israeli conflict with Iran has not merely created price volatility. It has exposed the fragility of procurement strategies built on spot market access and diversified sourcing rather than long-duration, government-anchored supply commitments. This is the structural context behind Prime Minister Narendra Modi's visit to the United Arab Emirates on May 15, 2026, the first leg of a five-nation tour running through May 20, encompassing the Netherlands, Sweden, Norway, and Italy.

The UAE stop is not incidental. It is the centrepiece. And the Modi UAE energy supply deals being sought during this visit represent a fundamental shift in how India intends to manage its energy future.

When big ASX news breaks, our subscribers know first

Why the UAE Has Become India's Most Indispensable Energy Partner

Not every bilateral relationship is built on equivalent foundations. The India-UAE energy partnership draws its durability from at least four distinct pillars that, taken together, create a depth of interdependence few other country pairs can match.

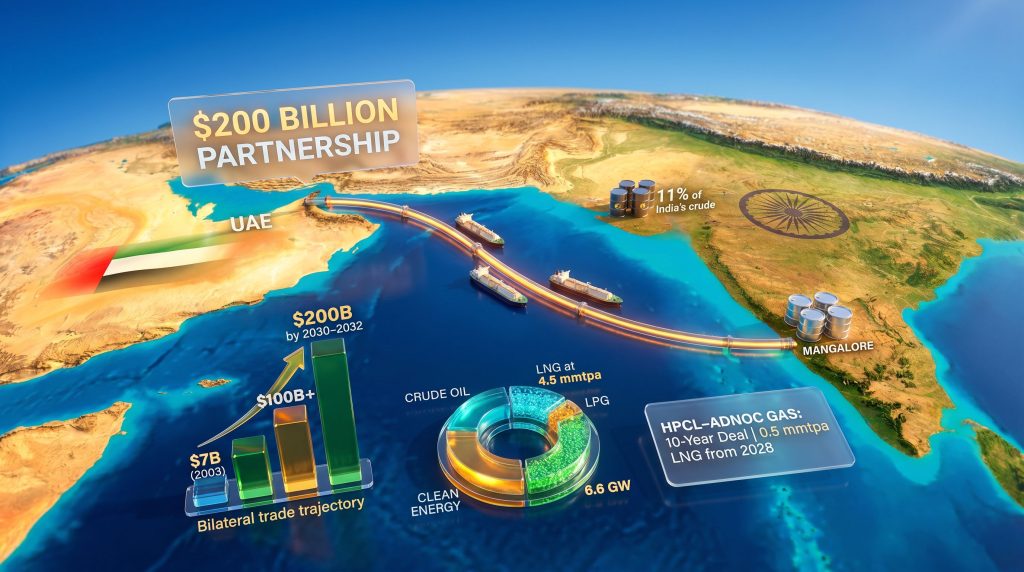

The UAE currently supplies approximately 11% of India's crude oil requirements, positioning it as India's fourth-largest crude supplier. On the natural gas side, the UAE holds the position of India's second-largest LNG provider. These are not marginal contributions to India's energy portfolio. At the scale of India's consumption, an 11% crude supply share represents volumes that cannot be substituted quickly or cheaply if disrupted.

Beyond commodity flows, the relationship carries demographic weight. Over 4.5 million Indian nationals reside in the UAE, forming one of the largest diaspora communities in any single country worldwide. This population functions as a living bridge between the two economies, generating remittance flows, cultural affinity, and a shared interest in bilateral stability that extends well beyond energy ministry negotiations.

The commercial trajectory reinforces the strategic logic. Bilateral trade between the two nations has grown from approximately $7 billion in 2003 to over $100 billion in recent years. A formal target of $200 billion within six years has been established, supported by the Comprehensive Economic Partnership Agreement (CEPA) and local currency settlement frameworks designed to reduce reliance on US dollar-denominated transactions.

The UAE's recent departure from OPEC removes production ceiling constraints that previously limited its output flexibility, a development that benefits import-dependent nations precisely at a moment when supply reliability from other Gulf producers is under pressure.

Furthermore, OPEC's market influence on Gulf production dynamics means this structural shift carries significant implications for how India plans its long-term procurement strategies across the region.

A lesser-discussed dimension of the UAE's strategic value to India is the widening rift between Saudi Arabia and the UAE itself. India's primary regional rival, Pakistan, maintains a defence partnership with Saudi Arabia. As the Saudi-UAE divergence has deepened in recent years, it has created structural space for India to consolidate a preferential relationship with Abu Dhabi that carries both energy and strategic dimensions. This geopolitical asymmetry is rarely foregrounded in analysis of India-UAE energy ties, but it shapes the political bandwidth available for bilateral cooperation.

The Three Negotiation Pillars: LPG, Crude, and Strategic Reserves

According to three Indian government sources cited by Reuters, Modi's discussions in Abu Dhabi are structured around three interconnected priorities. Each serves a distinct function within India's broader energy security architecture.

1. Long-term cooking gas (LPG) supply agreements

LPG is not a commodity in the conventional sense for India. It is a household welfare instrument. Access to affordable cooking gas is directly linked to rural energy poverty, women's health outcomes, and the practical success of government welfare programs that have connected tens of millions of households to clean cooking fuel over the past decade. When global LPG prices spike, the downstream social and fiscal consequences are immediate. Long-duration bilateral supply agreements at negotiated terms function as a buffer against this volatility.

2. Crude oil procurement continuity

The shift from spot market procurement to long-duration government-to-government crude supply contracts represents a meaningful reduction in India's exposure to price spikes driven by supply disruptions. At India's scale of imports, even partial insulation from spot market volatility generates substantial macroeconomic benefits. Analysts estimate that every $10 per barrel reduction in India's average crude import cost translates to approximately $15 billion in annual foreign exchange savings, a figure that directly affects the current account deficit, the rupee's external stability, and the fiscal space available for productive public investment. Indeed, the recent oil price rally driven by geopolitical tensions has reinforced precisely why locking in long-term supply terms matters so much at this juncture.

3. Strategic petroleum reserve expansion

India currently operates three strategic reserve facilities with a combined capacity of 5.33 million metric tonnes (MMT). Two additional sites are planned that will add a further 6.5 MMT of storage capacity. The ADNOC connection to this infrastructure is already operational: India has leased approximately 1.5 MMT of existing reserve capacity to ADNOC, with over 5 million barrels of ADNOC crude stored at the Mangalore facility through the Indian Strategic Petroleum Reserves Ltd (ISPRL) arrangement.

This arrangement is architecturally elegant. India receives revenue from leasing underutilised capacity while simultaneously ensuring that a committed supplier maintains physical crude on Indian soil. For ADNOC, the arrangement provides a strategic foothold in Asia's fastest-growing energy market. The question now being negotiated is whether ADNOC will take anchor positions in the two planned new facilities, effectively deepening its embedded role in India's national energy buffer system.

The LNG Supply Architecture: What Has Already Been Committed

The January 2026 India-UAE energy summit, held during UAE President Sheikh Mohamed bin Zayed Al Nahyan's visit to New Delhi, established the diplomatic foundation for the current negotiation pipeline. That summit produced a $3 billion LNG purchase agreement, establishing a precedent for large-scale government-to-government energy commerce between the two nations.

India's existing LNG procurement from the UAE under long-term contracts stands at approximately 4.5 million metric tonnes per annum (mmtpa). A more recent addition, the HPCL-ADNOC Gas 10-year agreement for 0.5 mmtpa commencing in 2028, represents a new layer of supply certainty being constructed above this baseline. The broader LNG supply outlook for Asia suggests that locking in these agreements now, before the market tightens further, represents a strategically sound approach for New Delhi.

Each incremental LNG agreement serves a dual function that goes beyond the volume itself. It reduces India's structural exposure to the spot LNG market, where prices can move by multiples during supply crunches, and it deepens ADNOC's role as an anchor supplier across the Asian demand landscape at precisely the moment when Gulf producers are seeking to secure long-term demand commitments as a hedge against the energy transition.

Scenario Analysis: Three Possible Outcomes of the Abu Dhabi Dialogue

Forward-looking analysis of the Modi UAE energy supply deals requires scenario framing rather than point forecasts. Three distinct outcome pathways are plausible depending on the breadth of political will and the appetite for structural commitment on both sides.

| Scenario | LNG Volume Outcome | Reserve Expansion | Clean Energy Dimension | Probability Assessment |

|---|---|---|---|---|

| Incremental Expansion (Base Case) | +0.5 to 1.0 mmtpa on existing contracts | Modest ADNOC lease expansion | Limited formal commitments | Highest |

| Structural Deepening (Optimistic) | 1+ mmtpa for 15-year term | ADNOC anchor tenant in new sites | Framework agreements signed | Moderate |

| Transformational Partnership | Full-spectrum fossil and clean energy alliance | Equity stake model for ADNOC | $30B Alterra fund deploys into India | Lower near-term |

Disclaimer: These scenarios represent analytical projections based on publicly available information and confirmed sources. They do not constitute investment advice or confirmed government commitments. Actual outcomes will depend on government-to-government negotiations that remain confidential as of the date of this analysis.

The transformational scenario is the most structurally significant but also the most complex to operationalise. It would position the relationship not as a buyer-seller arrangement but as a co-investment architecture in which the UAE holds equity stakes in Indian energy infrastructure while India provides long-term demand certainty to Gulf producers navigating the global energy transition.

The Clean Energy Dimension: Beyond Hydrocarbons

One of the least-discussed aspects of the India-UAE energy relationship is its clean energy layer, which has been developing in parallel with the hydrocarbon supply architecture. The UAE has committed to achieving net-zero emissions by 2045, a target that is driving significant capital outflows into renewable energy markets globally, with India identified as a priority destination.

The UAE's Alterra clean energy fund, capitalised at $30 billion, carries a mandate to deploy capital across global clean energy markets. India's renewable sector, with its combination of strong solar resources, expanding wind capacity, and a regulatory framework that includes mechanisms like the Green Credit Initiative, represents a compatible investment environment for this capital. Moreover, renewable energy solutions are increasingly being viewed as complementary to, rather than competitive with, the hydrocarbon supply architecture that underpins India's near-term energy security.

Planned UAE-backed clean energy capacity in India encompasses 6.6 GW of total capacity, including 1.2 GW of wind and solar projects. If these commitments are formalised and operationalised, they would represent a meaningful contribution to India's renewable build-out while simultaneously giving ADNOC and associated UAE sovereign capital a long-term equity position in India's energy transition infrastructure. This aligns closely with the broader energy transition demand reshaping capital flows across the Indo-Pacific region.

Civil Nuclear Cooperation: The Emerging Third Pillar

Beyond fossil fuels and renewables, civil nuclear cooperation has emerged as a third dimension of the bilateral energy relationship. The UAE's operational experience with the Barakah Nuclear Power Plant, which reached a significant milestone with Unit 4 becoming operational, provides a reference model for knowledge transfer relevant to India's baseload energy strategy.

Nuclear cooperation in the context of India-UAE relations represents a longer-term ambition rather than an immediate deliverable. However, its inclusion in the bilateral agenda signals that both nations are thinking about energy cooperation on a multi-decade horizon that extends well beyond current hydrocarbon supply arrangements.

The next major ASX story will hit our subscribers first

What Modi's Eighth UAE Visit Signals to Energy Markets

Modi's upcoming visit will be his eighth trip to the UAE since 2015, when he became the first Indian prime minister to visit the country in 34 years. The frequency of these visits is itself a data point. High-level diplomatic engagement at this cadence indicates a bilateral relationship being actively managed and deepened, not maintained on autopilot.

The significance of this visit is amplified by reports that two specific pacts are expected to boost India's LPG supplies and strengthen its strategic reserve arrangements, representing tangible deliverables rather than aspirational framework agreements. Modi's willingness to visit the UAE in this environment signals India's risk assessment and its confidence in the bilateral relationship, as well as its determination to secure energy supply commitments regardless of regional conflict dynamics.

The five-nation tour structure is also instructive. Energy security leads the agenda with the UAE stop. The subsequent European legs covering the Netherlands, Sweden, Norway, and Italy are likely to carry different bilateral priorities. The sequencing communicates that hydrocarbon supply security, not European partnerships or multilateral cooperation, is the primary diplomatic imperative of the tour.

The Macroeconomic Stakes for India

The macroeconomic significance of the Modi UAE energy supply deals extends well beyond the energy sector itself. Long-term supply agreements at negotiated pricing serve as natural hedges against commodity price cycles. For an economy of India's scale, stable energy input costs have direct implications across multiple macroeconomic variables:

- Inflation management: Stable LPG and crude pricing reduces the pass-through of global commodity volatility into domestic consumer prices.

- Current account stability: India's current account deficit is structurally linked to energy import costs. Long-term supply agreements at competitive terms reduce the deficit's sensitivity to global oil price movements.

- Rupee stability: Reduced foreign exchange outflows for energy imports, particularly through rupee-dirham settlement mechanisms, lower the structural demand for US dollars in India's balance of payments.

- Fiscal space: Lower energy import costs reduce the pressure on fuel subsidy expenditure, freeing fiscal resources for productive public investment.

The CEPA framework and local currency settlement mechanisms already in place between India and the UAE provide the infrastructure through which these macroeconomic benefits can be captured at scale. The energy supply agreements being negotiated in Abu Dhabi will flow through this existing commercial architecture.

FAQs: Modi UAE Energy Supply Deals

What is Modi seeking from the UAE during his May 2026 visit?

According to three Indian government sources cited by Reuters, Prime Minister Modi is seeking long-term supply agreements for cooking gas and crude oil, as well as expanded participation by ADNOC in India's strategic petroleum reserve infrastructure. The UAE is the first of five nations on a tour running May 15 to 20, 2026.

How important is the UAE as an energy supplier to India?

The UAE supplies approximately 11% of India's crude oil requirements, making it India's fourth-largest crude supplier, and holds the position of India's second-largest LNG provider. ADNOC also stores over 5 million barrels of crude at India's Mangalore strategic reserve facility under an existing lease arrangement.

What LNG agreements already exist between India and the UAE?

India signed a $3 billion LNG purchase agreement with the UAE in January 2026, building on approximately 4.5 mmtpa of existing long-term LNG supply contracts. A 10-year HPCL-ADNOC Gas agreement for 0.5 mmtpa commencing in 2028 represents a more recent addition to this supply architecture.

What is India's current strategic petroleum reserve capacity?

India operates three strategic reserve facilities with a combined capacity of 5.33 MMT. Two additional facilities are planned with a further 6.5 MMT of combined capacity. India has leased approximately 1.5 MMT of existing capacity to ADNOC.

How does the UAE's OPEC exit affect India's supply outlook?

The UAE's departure from OPEC removes production ceiling constraints, potentially enabling higher output volumes from ADNOC. For India, this means greater supply availability from a trusted bilateral partner at a time when other Gulf supply routes face significant geopolitical disruption from the US-Israeli conflict with Iran.

What clean energy investment is the UAE directing toward India?

The UAE's Alterra clean energy fund, capitalised at $30 billion, has identified India as a priority market. Current plans encompass support for approximately 6.6 GW of clean energy capacity in India, including 1.2 GW of wind and solar projects.

What is the bilateral trade target between India and the UAE?

The two nations have established a target of $200 billion in bilateral trade within six years, supported by the CEPA framework and local currency settlement mechanisms that reduce US dollar dependency in bilateral commerce.

The Strategic Architecture Taking Shape

What is emerging from the accumulated weight of India-UAE energy agreements, reserve infrastructure arrangements, clean energy commitments, and diplomatic engagement is something qualitatively different from a conventional commodity supply relationship.

The relationship is evolving toward a model in which energy supply security, infrastructure co-investment, clean energy transition financing, and geopolitical alignment function as mutually reinforcing elements of a single bilateral architecture. This is a template that neither nation has built with any other partner to the same degree.

For India, this architecture provides structural insulation against the supply disruptions that have exposed the vulnerabilities of spot-market dependent procurement strategies. For the UAE, it secures long-term demand commitments from Asia's fastest-growing energy market at a moment when Gulf producers are navigating the existential uncertainty of the global energy transition.

The India-UAE relationship is no longer primarily defined by what India buys and what the UAE sells. It is increasingly defined by what both nations are building together, and by the depth of mutual interest in ensuring that the architecture they have constructed remains stable regardless of what the broader global energy landscape throws at it.

The Modi UAE energy supply deals being sought in Abu Dhabi in May 2026 are not a single transaction. They are the latest stratum in a multi-decade structure of bilateral energy interdependence that both nations have strong incentives to deepen, and equally strong incentives to protect.

Want to Stay Ahead of the Next Major Resource Discovery Driving These Energy Shifts?

As geopolitical forces reshape global energy supply chains and drive demand for critical minerals, Discovery Alert's proprietary Discovery IQ model delivers real-time ASX mineral discovery alerts — turning complex data across 30+ commodities into actionable investment insights the moment announcements hit the market. Explore the historic returns major discoveries have generated and begin your 14-day free trial today to position yourself ahead of the broader market.