June 22, 2026

When Volume Meets a Price Ceiling: Understanding the Mongolia Coal Output Surge

Commodity markets have a long history of rewarding producers who scale efficiently, but the relationship between volume and value is rarely linear. When a nation doubles its output in under three years while simultaneously watching revenue per tonne compress, something structurally significant is underway. The Mongolia coal output surge is living this paradox in real time, and the implications extend well beyond the country's borders into the heart of Asia's industrial energy economy.

When big ASX news breaks, our subscribers know first

The Numbers Behind the Mongolia Coal Output Surge

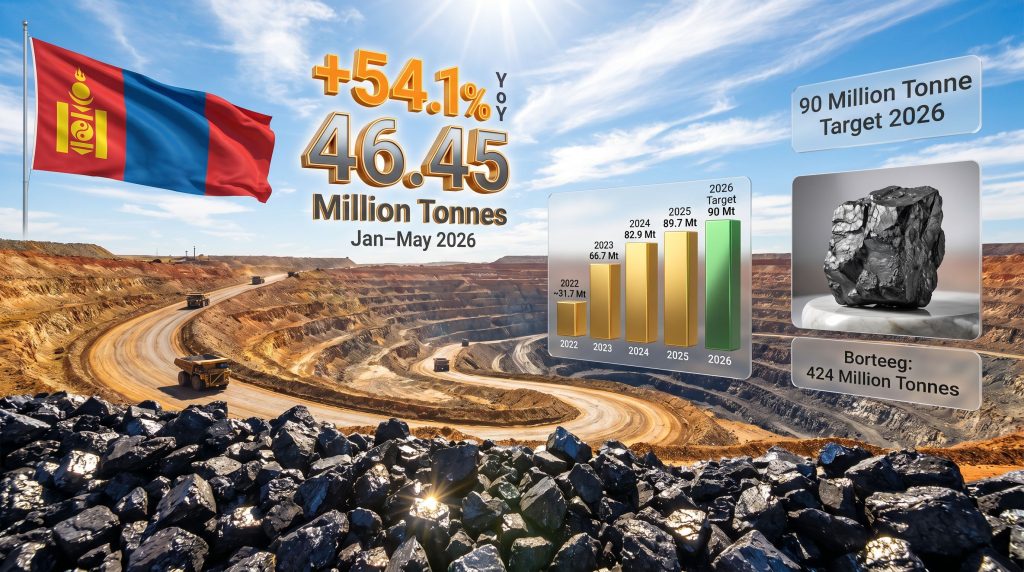

Mongolia's national statistics bureau confirmed that coal production across January through May 2026 reached 46.45 million tonnes, representing a year-on-year increase of 54.1%. That figure alone would be notable. What makes it analytically significant is that the acceleration has not tapered as the year progresses. May 2026 individually contributed 12.28 million tonnes, itself a 52.6% year-on-year gain, indicating that production momentum remains essentially unbroken.

The arithmetic of Mongolia's full-year ambition is equally striking. With a government-mandated production target of approximately 90 million tonnes for 2026, the country needs to average only around 6.2 million tonnes per month across the remaining months of the year to meet its goal. That figure represents roughly half of what Mongolia actually produced in May alone, providing substantial buffer against any operational disruptions.

To understand just how compressed this growth cycle has been, the trajectory since 2022 is instructive:

| Year | Coal Exports / Production (Mt) | Key Development |

|---|---|---|

| 2022 | ~31.7 | Pre-acceleration baseline |

| 2023 | 66.70 | Border reopening surge; +110.5% YoY |

| 2024 | 82.9 | Infrastructure and logistics consolidation |

| 2025 | 89.7 | Exceeded 85 Mt target; revenue fell 34% |

| 2026 Target | 90.0 (production) | On track to exceed with headroom |

Mongolia's coal output has more than doubled in three years. The volume story is compelling; the revenue story is considerably more cautious.

Borteeg: The Deposit That Changes Mongolia's Long-Term Supply Equation

While the January to May production data attracted significant market attention, a concurrent development deserves equal scrutiny. In early June 2026, the Mongolian government formally approved the commencement of mining operations at the Borteeg coal deposit, situated in the country's southern region in close proximity to Mongolia's primary export corridor toward China.

The scale of Borteeg's resource base is substantial by any measure:

- Total reserves: 424 million tonnes

- Coking coal proportion: approximately 95%

- Thermal coal proportion: approximately 5%

- Operator: Erdenes Tavan Tolgoi (state-owned enterprise)

The composition of Borteeg's reserves is what makes this deposit strategically differentiated. Coking coal, also known as metallurgical coal, is the variety used in steelmaking blast furnaces and commands a price premium over thermal coal used for electricity generation. The fact that 95% of Borteeg's reserves are classified as coking coal means that Mongolia's incoming supply additions are disproportionately weighted toward the higher-value end of the coal spectrum.

For investors and commodity analysts, this distinction matters considerably. A tonne of coking coal and a tonne of thermal coal are not economically equivalent, even when quoted on the same tonnage basis. Mongolia's reserve base is skewed toward the product that steel mills around the world specifically require, and that China's domestic supply of is now under pressure. Furthermore, the global crude steel outlook for 2025 and beyond underscores just how critical reliable coking coal supply has become for industrial producers globally.

The decision to place Erdenes Tavan Tolgoi as the lead operator reflects a consistent Mongolian government preference for retaining sovereign control over its most strategically significant assets. Rather than opening the project exclusively to private or foreign-led development, the state-enterprise model ensures that production revenues flow through a government-aligned structure.

China's Safety Crackdown and Its Counterintuitive Effect on Import Demand

A gas explosion at a coking coal mine in China's Shanxi province, one of the country's most concentrated and historically productive mining regions, triggered a tightening of mine safety compliance standards across the sector. The regulatory consequences of this incident extend beyond individual operations.

When Chinese regulators apply heightened safety enforcement across a large production region, the near-term effect is a reduction in domestic coal output as mines undergo inspections, implement procedural modifications, and in some cases suspend operations pending compliance certification. This supply-side constraint within China creates a structural gap that imported coal is well positioned to fill.

Market participants have broadly anticipated that Chinese coal import demand will remain elevated through the second half of 2026 as a direct consequence. Mongolia, sharing a land border with China and operating the most logistically direct supply corridor available to any foreign supplier, is the natural beneficiary of this dynamic. According to Reuters, Mongolia's coal shipments to China surged 61% in April, overtaking Indonesia as a leading supplier.

It is worth understanding why land-based supply matters so much in this context:

- No maritime freight costs, which can add $15 to $30 per tonne to the delivered cost of seaborne coal depending on vessel type and route.

- No port handling delays, which affect seaborne suppliers including Australian and Indonesian exporters.

- Weather-independent logistics, eliminating seasonal disruption risks common in ocean freight.

- Shorter transit times, enabling tighter inventory management for Chinese buyers.

These structural cost advantages position Mongolia not merely as an alternative supplier during domestic Chinese shortfalls, but as a preferred low-cost provider within China's coal procurement hierarchy under normal operating conditions as well.

Mongolia vs. Indonesia: The Shifting Geography of China's Coal Imports

The competitive dynamics between Mongolia and Indonesia as coal suppliers to China represent one of the more consequential shifts occurring in Asian commodity markets. The two countries compete in partially overlapping but structurally distinct segments:

| Metric | Mongolia | Indonesia |

|---|---|---|

| Primary coal type | Coking (dominant) | Thermal (dominant) |

| Logistics model | Land border | Seaborne |

| Jan-Apr 2026 export trend | Strongly accelerating | Down 6.9% YoY |

| April 2025 China imports | Surpassed Indonesia that month | 11.07 Mt (thermal, April 2025) |

| September 2025 China imports | 9.29 Mt (+33% YoY) | Declining trend |

| Freight exposure | Minimal | High |

In April 2025, Mongolia temporarily surpassed Indonesia as China's largest coal supplier by monthly volume, a milestone that would have seemed implausible five years earlier given Indonesia's historically dominant position in Asian seaborne coal markets.

Indonesia's export challenges are compounded by several intersecting pressures. Its domestic market obligation (DMO) requirements, which mandate that at least 30% of annual coal output be allocated to domestic supply, constrain exportable volumes. Delays in mining quota approvals (RKAB) have further limited export availability. The rollout of Indonesia's export centralisation initiative through Danantara Sumber Daya Indonesia introduces additional operational complexity for seaborne suppliers.

Meanwhile, elevated freight rates linked to geopolitical disruptions have raised the delivered cost of Indonesian coal into Chinese ports, eroding the competitive position that lower fob prices once provided. Indonesia's total coal exports reached 37.33 million tonnes in April 2026, down 3.5% year-on-year, with cumulative January to April shipments of 151.1 million tonnes representing a 6.9% annual decline. In addition, the China steel market dynamics further amplify Mongolia's competitive advantage as Chinese steelmakers seek cost-efficient coking coal alternatives.

The Volume-Revenue Paradox: Why More Coal Does Not Always Mean More Wealth

Perhaps the most instructive and underappreciated dimension of Mongolia's coal story is the divergence between export volumes and export revenues. In 2025, Mongolia shipped 89.7 million tonnes of coal, exceeding its 85 million tonne target and recording year-on-year volume growth of approximately 7%. Yet export revenue over the same period fell by approximately 34% to around $5.8 billion.

This is not a market share problem. Mongolia has not lost buyers — it has gained them. The issue is one of benchmark pricing: global coking coal prices weakened considerably through 2024 and into 2025, compressing the per-tonne revenue realised on each shipment regardless of how efficiently the coal was mined or transported. Consequently, metallurgical coal prices remain a critical variable in determining whether Mongolia's volumetric gains translate into meaningful fiscal outcomes.

The implications for revenue scenario planning under the 90 million tonne target are meaningful:

| Scenario | Volume (Mt) | Assumed Price ($/t) | Estimated Revenue |

|---|---|---|---|

| Base case (current pricing) | 90 | ~$65 | ~$5.85 billion |

| Coking coal price recovery | 90 | ~$85 | ~$7.65 billion |

| Full target plus Borteeg ramp | 95-100 | ~$80 | ~$7.6-8.0 billion |

Note: Price assumptions are illustrative and based on prevailing market conditions as of mid-2026. These figures do not constitute financial forecasts and should not be relied upon as investment guidance.

It is worth noting that metallurgical coal futures experienced a 30% price increase from July 2025, partially driven by growing recognition of Mongolia's supply reliability and China's domestic safety-driven output constraints. If that pricing momentum extends into the second half of 2026, the revenue gap between the base case and recovery scenarios could narrow materially.

The next major ASX story will hit our subscribers first

Central Asia's Broader Coal Ambitions: Kazakhstan as a Parallel Case Study

Mongolia's production acceleration does not exist in regional isolation. Neighbouring Kazakhstan has announced a comprehensive national coal development programme spanning 2026 to 2031, encompassing coal-to-chemicals projects, synthetic fuel production, metallurgical coke manufacturing, and the modernisation of thermal power infrastructure.

Kazakhstan's energy ministry has confirmed it is developing plans for six coal-to-chemicals projects within this timeframe, with objectives to produce metallurgical coke and synthetic fuels derived from coal feedstocks. The country also intends to produce gas, ammonia, urea, and other chemical products from coal within the same framework.

The scale of coal's role in Kazakhstan's domestic energy system underscores why any rapid decarbonisation pathway faces significant structural resistance. Coal generated approximately 62.1% of Kazakhstan's electricity in 2026, with natural gas contributing 23.4%, hydroelectric power 7.5%, and renewables accounting for the remaining 7%.

Both Mongolia and Kazakhstan are pursuing coal expansion strategies that run counter to global decarbonisation trajectories. This reflects the economic realities facing landlocked, resource-rich nations with limited near-term renewable energy infrastructure and significant existing coal-dependent industrial bases.

Long-Term Demand Risks: What the IEA Plateau Scenario Means for Mongolia

The International Energy Agency projects Mongolia's coal output to moderate toward approximately 97 million tonnes, with exports plateauing near 84 million tonnes by 2027, as growth in Chinese demand slows. This trajectory is not a collapse scenario, but it does suggest that the current expansion phase may be approaching its natural ceiling.

Several risk variables warrant specific attention:

- China's domestic safety policy reversal: If regulators ease enforcement pressure following the Shanxi incident, domestic Chinese coal output could recover, reducing the import premium that currently benefits Mongolian suppliers.

- China's clean energy trajectory: Beijing's stated long-term commitments to expanding solar, wind, and nuclear capacity introduce structural demand uncertainty for all coal exporters beyond the 2027 planning horizon.

- Coking coal benchmark pricing: Mongolia's revenue is highly sensitive to metallurgical coal prices given the composition of its reserves. A sustained period of benchmark weakness, as experienced in 2025, can render volumetric production gains financially hollow.

- Infrastructure bottlenecks: Rail and border crossing capacity at Mongolia's key export points, particularly Gashuun Sukhait, has historically been a limiting factor. Any saturation of current infrastructure could constrain the production volumes the government is targeting.

Furthermore, trade impacts on iron ore and broader commodity markets illustrate how geopolitical and regulatory headwinds can reshape supply chains rapidly, adding another layer of uncertainty for Mongolian export planners.

The strategic question for Mongolia is not whether it can produce 90 million tonnes of coal, but whether that volume can be sustained profitably if coking coal prices remain range-bound and Chinese demand growth plateaus as projected.

Mongolia Coal Output Surge: Key Data at a Glance

| Metric | Value |

|---|---|

| Jan-May 2026 coal output | 46.45 million tonnes |

| Year-on-year growth (Jan-May 2026) | +54.1% |

| May 2026 monthly output | 12.28 million tonnes |

| May 2026 YoY growth | +52.6% |

| 2026 full-year production target | 90 million tonnes |

| Monthly output needed (Jun-Dec) to meet target | ~6.2 million tonnes |

| Borteeg deposit total reserves | 424 million tonnes |

| Borteeg coking coal proportion | ~95% |

| 2025 export volume | 89.7 million tonnes |

| 2025 export revenue | ~$5.8 billion (-34% YoY) |

| September 2025 China imports from Mongolia | 9.29 million tonnes (+33% YoY) |

Frequently Asked Questions: Mongolia Coal Output Surge

How much coal did Mongolia produce in the first five months of 2026?

Mongolia's national statistics bureau confirmed production of 46.45 million tonnes between January and May 2026, equating to a 54.1% year-on-year increase over the same period in 2025.

What is Mongolia's coal production target for 2026?

The Mongolian government has set a full-year production objective of approximately 90 million tonnes, primarily to support increased volumes flowing to Chinese buyers across both coking and thermal coal categories.

Why is Chinese demand for Mongolian coal increasing in 2026?

Two concurrent factors are amplifying Chinese import demand. First, Mongolia's land border logistics provide inherent cost and delivery advantages over seaborne suppliers. Second, the Shanxi province mining safety crackdown, triggered by a gas explosion at a coking coal operation, has tightened domestic Chinese supply and reinforced import dependency in the near term.

What is the Borteeg coal deposit and why does it matter?

Borteeg is a newly approved mining project in southern Mongolia with 424 million tonnes of total reserves, of which approximately 95% is classified as coking coal. Its proximity to the main export corridor to China and its state-enterprise operational structure make it a material medium-term addition to Mongolia's supply capacity.

Is Mongolia's export revenue growing in line with its production volumes?

No. Despite achieving 89.7 million tonnes of exports in 2025 and exceeding its annual volume target, Mongolia's export revenue fell by approximately 34% to around $5.8 billion, reflecting broad-based weakness in global coking coal benchmark pricing rather than any deterioration in market access or demand.

How does Mongolia compare to Indonesia as a coal supplier to China?

The two countries serve partially different segments of China's coal market. Mongolia supplies primarily coking coal via land-based logistics, while Indonesia exports predominantly thermal coal via seaborne routes. In April 2025, Mongolia surpassed Indonesia as China's largest coal supplier by volume for that month, reflecting Mongolia's accelerating growth alongside Indonesia's cumulative export decline of 6.9% across January to April 2026. Bigmint data on coking coal exports further corroborates this trend, showing Mongolia's coking coal exports surging by 14% in calendar year 2024 alone.

Structural Significance or Cyclical Peak? A Framework for Investors

For commodity traders and market analysts, the near-term signal from the Mongolia coal output surge is reasonably bullish. Mongolian coking coal supply is growing, Chinese import demand is elevated, and the Borteeg deposit adds a credible medium-term supply pipeline dominated by the higher-value metallurgical variety.

For longer-horizon investors, however, the picture warrants more careful framing. The IEA's plateau projections, China's stated clean energy ambitions, and the cautionary tale of 2025's revenue compression collectively argue that Mongolia's current production window may be narrower than the headline production numbers imply. In addition, Indian steel prices and demand trajectories represent an emerging secondary market that could, over time, provide Mongolian exporters with meaningful diversification away from sole reliance on Chinese buyers.

The Borteeg deposit approval and Erdenes Tavan Tolgoi's expanded operational mandate signal genuine government commitment to maximising coal export revenues within the current demand window. However, commodity markets, particularly those anchored to a single downstream buyer, carry concentration risk that volume statistics alone do not capture. Mongolia's challenge in the years ahead will be converting its geological endowment and geographic advantage into durable fiscal revenue, rather than simply mounting tonnage.

This article contains forward-looking projections and scenario-based analysis drawn from publicly available market data and third-party research. All revenue estimates and price assumptions are illustrative only and do not constitute investment advice. Commodity markets are subject to significant price volatility and structural change.

Want to Capitalise on Major Commodity Discoveries Before the Broader Market?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries — including coking coal and metallurgical commodities — instantly transforming complex market data into actionable insights for both short-term traders and long-horizon investors. Explore historic examples of exceptional discovery returns or start your 14-day free trial today to position yourself ahead of the next major market move.