July 7, 2026

The Hidden Tension in Credit Analysis: When a Better Balance Sheet Means a Weaker Business

Credit rating frameworks are built on a deceptively simple premise: stronger finances mean lower risk. However, the resources sector has long exposed the limitations of this logic. A company can simultaneously improve its liquidity position and weaken its fundamental earnings architecture, creating a paradox that ratings agencies must navigate carefully. Moody's reviews South32 for possible downgrade following the miner's agreement to sell its aluminium, alumina, and bauxite assets to Alcoa is a textbook illustration of this tension, and it carries implications that extend well beyond one company's balance sheet.

When big ASX news breaks, our subscribers know first

What a Moody's Credit Review Actually Means in Practice

Unpacking the Baa1/P-2 Ratings and the Review Trigger

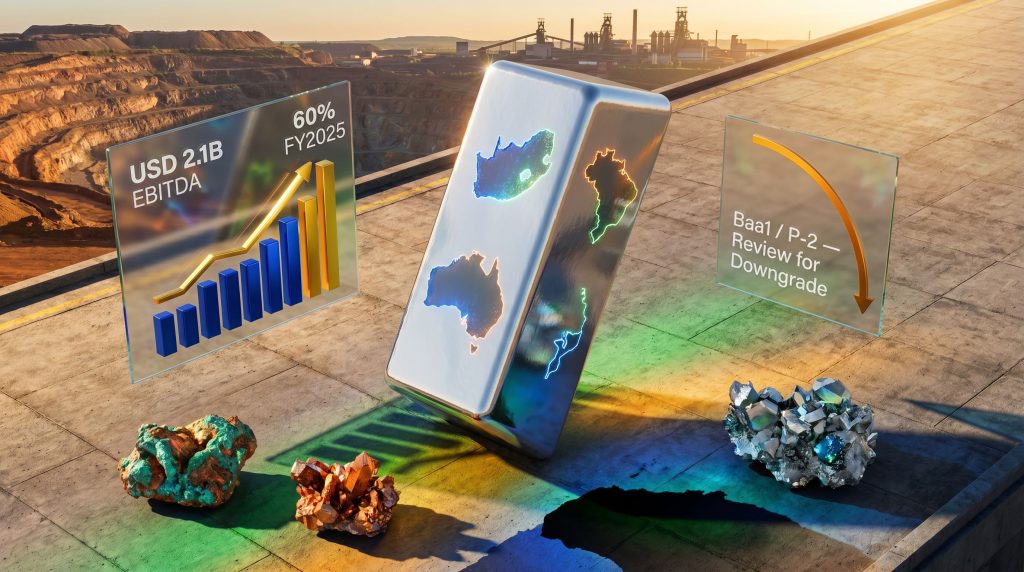

South32 currently holds a Baa1 long-term issuer rating and a P-2 short-term commercial paper rating from Moody's, both now placed on review for possible downgrade. For context, Baa1 sits at the upper end of the investment-grade spectrum, three notches above the threshold that separates investment-grade from speculative-grade debt. A downgrade of even one notch to Baa2 would remain investment grade but would carry meaningful consequences.

A review for downgrade is not a downgrade itself. It is a formal signal that Moody's has identified a material structural change to a company's risk profile that cannot be assessed using existing rating assumptions. The agency must now re-examine the credit from first principles. Furthermore, the Alcoa downgrade impact on the broader aluminium sector adds another layer of analytical complexity to this already nuanced review.

"A credit review places the issuer under an active analytical microscope. It signals that the current rating may no longer accurately reflect the company's risk architecture, and that a formal decision, in either direction, will follow within a defined timeframe."

How Ratings Affect Real-World Borrowing Conditions

For large mining companies operating at the scale of South32, credit ratings function as the invisible hand shaping financing costs. A downgrade affects:

- The yield spread demanded by bond investors above risk-free benchmarks

- Covenant structures in revolving credit facilities

- Counterparty confidence in long-term offtake and hedging agreements

- Eligibility for certain institutional investor mandates that require Baa1 or above

The practical cost of a one-notch downgrade in today's credit environment may appear modest in isolation, but compounded across billions in outstanding debt and new issuance, it becomes financially significant over multi-year horizons.

The Dual-Dimension Framework: Financial Profile vs. Business Profile

Moody's analytical approach separates two distinct dimensions of creditworthiness. The financial profile encompasses leverage ratios, liquidity, interest coverage, and cash generation. The business profile encompasses scale, commodity mix, geographic diversification, and competitive position. These two dimensions can, and in South32's case do, move in opposite directions simultaneously.

The USD 5.6 billion transaction with Alcoa will materially improve South32's financial profile by generating substantial cash proceeds and creating a net cash position. Yet the same transaction strips away assets that delivered an average of 37% of South32's underlying earnings over the five financial years ending June 2025, weakening the business profile in ways that cash on a balance sheet cannot immediately offset.

The USD 5.6 Billion Alcoa Transaction: What Is Changing Hands

Asset Portfolio Breakdown

The transaction encompasses a geographically diverse set of aluminium-chain assets spanning three continents. The table below summarises the key assets involved:

| Asset | Location | South32's Interest |

|---|---|---|

| Hillside Aluminium Smelter | South Africa | 100% |

| Worsley Alumina Refinery | Western Australia | 86% |

| MRN Bauxite Mine | Brazil | Partial interest |

| Brazil Alumina Refinery | Brazil | Partial interest |

| Brazil Aluminium Smelter | Brazil | Partial interest |

| Mozal Aluminium Smelter | Mozambique | Excluded (care and maintenance) |

Why Mozal Was Left Behind

The exclusion of the Mozal smelter in Mozambique is itself a telling data point. Mozal entered care and maintenance in March 2026 after the operation failed to secure affordable power supply at commercially viable rates. This reflects a broader challenge facing energy-intensive aluminium smelting operations in sub-Saharan Africa, where power infrastructure constraints and pricing volatility can render otherwise viable assets economically unsustainable.

The fact that Alcoa did not seek to include Mozal in the transaction suggests the asset's power situation made it unattractive even as part of a large portfolio acquisition. South32 now retains a mothballed smelter with no near-term earnings contribution and uncertain reinstatement prospects, a residual liability that does little to support the business profile Moody's is scrutinising.

How the Total Consideration Reaches USD 5.6 Billion

The headline figure of up to USD 5.6 billion incorporates a combination of upfront cash consideration and contingent components tied to commodity prices and project milestones. This structure is common in large mining asset transactions, where commodity price uncertainty at the time of signing makes fixed pricing commercially difficult. For South32, the contingent element means the final realised proceeds will depend partly on alumina and aluminium price trajectories over the settlement period.

The Earnings Architecture Being Dismantled

What 60% of FY2025 EBITDA Actually Represents

In the financial year ending June 2025, South32 reported USD 2.1 billion in underlying EBITDA. Within that figure, alumina alone contributed 51%, and aluminium added a further 9%, meaning the combined aluminium value chain represented approximately 60% of total group EBITDA in that single year. The five-year average contribution of 37% reflects years when other commodities, particularly metallurgical coal and manganese, delivered stronger relative performance.

This earnings concentration is the core of Moody's concern. When any single commodity or asset cluster generates more than half of a company's earnings in a given year, the removal of those assets fundamentally transforms the earnings base, regardless of the cash generated by the sale.

Concentration Risk: A Credit Framework Perspective

Investment-grade credit ratings for diversified miners are partly justified by the diversification premium, the analytical recognition that losses in one commodity segment tend to be offset by gains in another when prices move independently. Once South32 completes this transaction, it will no longer qualify as a diversified miner in the same structural sense.

Its remaining portfolio will be concentrated primarily in copper, zinc, manganese, and metallurgical coal assets, a tighter commodity mix that carries a higher correlation to specific industrial demand cycles. In addition, critical minerals demand forecasts will play a central role in determining whether this concentrated portfolio can generate sufficient earnings scale.

"Commodity diversification is not merely a strategic preference for mining companies, it is a credit rating input. Agencies explicitly apply lower credit risk assessments to issuers whose earnings streams span multiple uncorrelated commodities, geographies, and customer bases."

South32's Strategic Pivot: The Critical Minerals Thesis

Copper and Zinc as Replacement Growth Engines

Incoming CEO Matt Daley has articulated a clear strategic direction for the post-divestment entity, centred on growing the company's copper and zinc exposure. This positioning is anchored in structural demand forecasts tied to the global energy transition. The table below contrasts the demand fundamentals of the divested aluminium assets against the target commodities:

| Commodity | Primary Demand Driver | Long-Term Outlook |

|---|---|---|

| Copper | EV motors, grid infrastructure, data centres | Structural deficit projected beyond 2030 |

| Zinc | Galvanised steel, battery technology | Moderate growth, supply constraints emerging |

| Aluminium (divested) | Packaging, transport, construction | Mature demand profile, energy-intensive production |

The logic here is compelling from a growth investor perspective, but it introduces a timing mismatch that credit analysts will scrutinise. Furthermore, the well-documented copper supply crunch makes acquiring high-quality deposits at reasonable valuations exceptionally competitive. The capital required to rebuild EBITDA scale in copper to match what is being surrendered in aluminium is substantial and not guaranteed to arrive within Moody's review timeframe.

The Energy Intensity Problem in Aluminium

One underappreciated driver of this strategic exit is the structural energy cost disadvantage of aluminium smelting. Primary aluminium production is among the most electricity-intensive manufacturing processes in existence, requiring approximately 13 to 15 megawatt-hours per tonne of aluminium produced. In an era of rising power costs, carbon pricing mechanisms, and decarbonisation obligations, energy-intensive smelting assets become strategic liabilities for companies with sustainability commitments and ESG-linked financing structures.

For South32, the Mozal situation illustrated this vulnerability vividly. Power affordability issues forced the smelter into care and maintenance, eliminating its earnings contribution entirely. The Hillside smelter in South Africa operates in a power environment that has historically been challenging due to the constraints of Eskom, South Africa's national utility. Offloading these exposures to Alcoa, which is building a vertically integrated aluminium business, allows South32 to exit a structurally difficult energy cost environment.

Three Scenarios for the Moody's Review Outcome

How the Review Could Conclude

Ratings reviews for mining companies following large-scale transactions typically resolve within three to six months of announcement. For South32, three plausible pathways exist:

Scenario 1: Transaction completes with no major portfolio enhancement

- Moody's proceeds with at least a one-notch downgrade

- South32 moves from Baa1 to Baa2, remaining investment grade

- Borrowing costs rise modestly but institutional investor eligibility is largely preserved

- Management faces pressure to accelerate copper or zinc acquisitions

Scenario 2: South32 announces a material acquisition before the review concludes

- A significant copper or zinc asset purchase could demonstrate credible EBITDA replacement

- Moody's could affirm the Baa1 rating or limit any downgrade to a narrower adjustment

- The acquisition would need to demonstrably offset the scale loss from divested aluminium assets

Scenario 3: The Alcoa transaction conditions change materially or the deal falls through

- The ratings review would likely be withdrawn

- Business profile concerns revert to pre-announcement status

- Strategic uncertainty increases but near-term credit stability is restored

"The USD 5.6 billion transaction gives South32 significant capital deployment optionality. Whether management moves quickly and decisively enough to satisfy ratings agency timelines remains the central unanswered question for credit investors."

The next major ASX story will hit our subscribers first

What This Means for the Global Aluminium Supply Chain

Alcoa's Consolidation Play and What It Tells Us About Industry Structure

Alcoa's acquisition of South32's aluminium assets represents one of the most significant reshufflings of the aluminium value chain in recent years. By absorbing Hillside, Worsley, the MRN bauxite mine, and the Brazilian operations, Alcoa materially extends its vertically integrated footprint across bauxite extraction, alumina refining, and primary smelting. Consequently, aluminium industry leaders are watching this consolidation closely as it reshapes competitive positioning across the sector.

This consolidation reflects a broader industry dynamic: scale and vertical integration are becoming increasingly important competitive advantages in aluminium, as smaller standalone operations struggle to absorb energy cost volatility, capital expenditure requirements for decarbonisation, and the margin compression that comes from commodity price cycles. Alcoa's willingness to pay up to USD 5.6 billion signals strong conviction in the long-term aluminium demand story, even as South32 is exiting it. According to Moody's formal statement on the review, the agency's concern centres precisely on this earnings scale reduction.

Bauxite and Alumina Supply Chain Implications

The transfer of the Worsley Alumina refinery in Western Australia and the MRN bauxite mine in Brazil to Alcoa restructures supply relationships across the Pacific and Atlantic basins. Worsley is one of Australia's largest alumina refineries, processing bauxite from the Boddington mine system into metallurgical-grade alumina for export. Its change of ownership will not immediately alter trade flows but will shift the strategic decisions around expansion, contracting, and decarbonisation investment to Alcoa's management framework.

The Brazilian assets are particularly noteworthy given the broader context of global bauxite supply. Brazil holds some of the world's largest and highest-grade bauxite deposits, particularly in the Pará state region. The MRN (Mineração Rio do Norte) mine operates within the Trombetas River system, a geologically rich bauxite province where ore grades typically exceed 50% aluminium oxide (Al₂O₃), well above the global average for commercially mined bauxite. Alcoa's deepened exposure to this resource base strengthens its long-term raw material security.

Market Reaction: Reading Between the Price Movements

The 11% Rally and Its Meaning

When South32 first announced the Alcoa transaction, the market's response was unambiguous: shares surged more than 11%, reflecting strong investor approval of the strategic direction. This reaction signals that equity investors viewed the aluminium asset portfolio as a drag on South32's valuation multiple, likely because aluminium smelting's energy intensity, carbon exposure, and earnings volatility were weighing on the company's price-to-earnings and EV/EBITDA multiples relative to peers with cleaner, more growth-oriented commodity exposures.

The subsequent share price softness following the Moody's announcement reflects a more nuanced second-order consideration: credit costs, institutional selling triggers, and the recognition that EBITDA will shrink materially before copper and zinc growth replaces it. This divergence between strategic approval and tactical caution is typical of how institutional investors process large transformative transactions. As reported by Mining.com, the review underscores how credit and equity markets can respond very differently to the same strategic announcement.

Key Takeaways for Investors and Industry Observers

Moody's reviews South32 for possible downgrade is more than a credit agency administrative action. It encapsulates several converging forces reshaping the global mining landscape:

- Scale matters in credit analysis, and removing 37% to 60% of earnings cannot be offset purely by cash proceeds, regardless of how strategically sound the rationale is

- Aluminium's energy intensity is accelerating portfolio exits by diversified miners who face carbon cost and power availability pressures that vertically integrated, scale-focused producers can better absorb

- The critical minerals pivot carries execution risk, particularly the timeline mismatch between divesting mature cash-generating assets and building replacement earnings in copper and zinc

- Alcoa's consolidation of these assets reflects genuine conviction in aluminium's long-term structural demand story, even as South32 exits the sector

- Leadership transitions add analytical uncertainty for both credit agencies and equity investors, since a new CEO's strategic execution track record with acquisitions is by definition unproven at South32

- The Mozal situation serves as a cautionary case study in how power infrastructure vulnerability can rapidly transform a viable smelting operation into a stranded cost centre

This article contains forward-looking statements, analytical scenarios, and financial projections for informational purposes only. It does not constitute financial advice. Readers should conduct independent research and consult qualified financial advisers before making investment decisions. Credit rating outcomes are subject to change based on information not available at the time of writing.

Want to Spot the Next Major ASX Mineral Discovery Before the Market Does?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries — cutting through complex data across more than 30 commodities to surface actionable opportunities the moment they are announced. Explore how historic discoveries have generated substantial returns on Discovery Alert's dedicated discoveries page, and begin your 14-day free trial today to position yourself ahead of the broader market.