July 9, 2026

The Sulfur Shock Reshaping Global Phosphate Supply Chains

Few commodities illustrate the fragility of modern agricultural supply chains quite like phosphate. Unlike oil or gas, phosphate rock cannot be synthesised, substituted, or stockpiled indefinitely. It must be mined, chemically processed, and delivered in precise formulations to farms across the world. When the raw material inputs that underpin that processing chain are severed by geopolitical conflict, the consequences ripple outward in ways that most observers fail to anticipate until crop yields begin to suffer.

That is precisely the scenario now unfolding. The ongoing conflict in the Mideast Gulf has functionally closed one of the world's most critical maritime trade corridors, the Strait of Hormuz, to reliable commercial shipping. The immediate casualty is not crude oil, as many assume, but sulfur. And without sulfur, there is no sulphuric acid. Without sulphuric acid, phosphate fertilizer production halts. This chain of dependencies, stretching from Persian Gulf wellheads to Brazilian soybean fields, is now under severe stress — a direct consequence of escalating geopolitical supply risks that have been building for some time.

When big ASX news breaks, our subscribers know first

Why Mosaic Phosphate Production in Brazil Matters More Than Most Realise

Brazil occupies a structurally unique position in global phosphate markets. It is simultaneously one of the world's largest consumers of phosphate fertilizers and a significant domestic producer. That dual role amplifies any disruption: when domestic supply contracts, import demand does not merely increase, it surges, placing immediate pressure on globally traded volumes and price benchmarks.

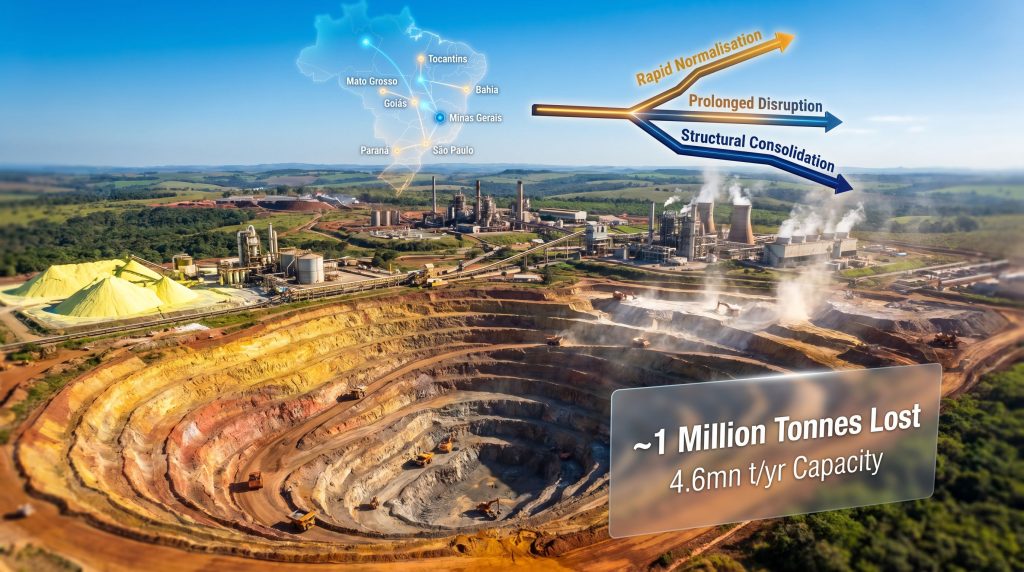

Before the current curtailment cycle, a single dominant operator accounted for approximately 74% of Brazil's total phosphate rock output, representing an annual production capacity of roughly 4.6 million tonnes. Brazil's phosphate chemical processing capacity, measured in P₂O₅ equivalent, reached approximately 1.1 million tonnes per year, with the dominant operator controlling close to 62% of that national capacity. This extreme concentration within a single operational base creates systemic vulnerability: decisions made at the facility level reverberate across continental supply chains.

The country's phosphate production spans a wide geographic corridor, from the central-western states of Goiás and Mato Grosso through the southeastern state of Minas Gerais to the southern state of Paraná. Finished products include monoammonium phosphate (MAP), diammonium phosphate (DAP), single superphosphate (SSP), and monocalcium phosphate for animal nutrition. Each product line carries different margin characteristics, different feedstock sensitivities, and therefore different survival probabilities during a raw material shock. Understanding these dynamics is essential for assessing Mosaic phosphate production in Brazil going forward.

The Sulfur-Phosphate Nexus: Understanding the Hidden Dependency

Why Sulfur Is the Invisible Keystone of Phosphate Fertilizer Manufacturing

Phosphate fertilizer production is fundamentally a wet chemical process. Phosphate rock, which contains calcium phosphate minerals, must be reacted with sulphuric acid to liberate plant-available phosphate compounds. This reaction is not optional and cannot be substituted. The ratio of sulphuric acid consumption to finished fertilizer output is substantial: producing one tonne of MAP, for example, requires roughly 0.4 to 0.6 tonnes of sulphuric acid, which itself requires elemental sulfur as its primary feedstock.

Historically, the Middle East has been a dominant source of elemental sulfur, with large volumes recovered as a byproduct of oil and gas processing in Kuwait, Saudi Arabia, Oman, and the UAE. These volumes have transited the Strait of Hormuz as a matter of routine, reaching markets across Asia, Africa, and Latin America. When that corridor becomes unreliable, the entire downstream phosphate industry faces feedstock starvation, with implications that extend well beyond global industrial demand for raw materials.

South Africa as a Canary in the Coal Mine

The scale of the sulfur supply disruption becomes visible through the South African experience. Sulphur imports into South Africa fell by approximately 68% in the first five months of 2026, with only around 56,300 tonnes entering the country compared to 174,183 tonnes across the same period in 2025, according to Argus Media reporting. In the January to May 2025 period, South Africa received 62,600 tonnes from Kuwait, 40,000 tonnes from Oman, 38,500 tonnes from Saudi Arabia, and 31,500 tonnes from the UAE. By contrast, only a single Middle Eastern cargo, approximately 55,000 tonnes delivered in February, arrived in the equivalent 2026 period, with Gulf imports absent entirely from late February onward.

"The South African data reveals something important that markets have been slow to price: the Strait of Hormuz disruption is not merely a headline risk for oil markets. It is a functional severing of the sulfur supply chain that underpins phosphate fertilizer production across multiple continents simultaneously."

South Africa's domestic sulphuric acid market experienced further strain when major producer Foskor was forced to shut operations in March due to sulfur shortages. Oil refiner Sasol, which also produces sulfur and sulphuric acid, suffered an unplanned shutdown at one of its facilities in the same month and remained offline through August. Trucking costs for sulfur transport between Richards Bay and the Democratic Republic of Congo peaked at approximately $1,000 per tonne for a round trip, illustrating the severity of the logistics premium that buyers are absorbing.

Mapping the Curtailment Cascade Across Brazilian Facilities

Facility-by-Facility Impact Assessment

| Facility | Location | Capacity | Current Status |

|---|---|---|---|

| Candeias blending unit | Bahia (northeast) | Part of 2.5mn t/yr combined | Temporarily suspended |

| Catalão blending unit | Goiás (central-west) | Part of 2.5mn t/yr combined | Blending suspended; rock production paused |

| Palmeirante unit | Tocantins (north) | 1mn t/yr | Output reduced |

| Sorriso unit | Mato Grosso (central-west) | 700,000 t/yr | Output reduced |

| Uberaba plant | Minas Gerais (southeast) | 1mn t/yr | Gradual mothballing from September 2026 |

| Tapira unit | Minas Gerais (southeast) | 2.2mn t/yr (rock) | Extended shutdown |

| Fospar unit | Paraná (south) | 500,000+ t/yr blending | Operating normally; acid stocks to September 2026 |

| Cajati unit | São Paulo (southeast) | 600,000 t/yr | Operational via sulfur imports; animal nutrition focus |

| Araxá Mining and Chemical Complex | Minas Gerais | Major integrated complex | Demobilisation underway |

| Patrocínio mine | Minas Gerais | 1.3mn t/yr | Mining activities idled |

| Araxá SSP site | Minas Gerais | 243,000 t/yr P₂O₅ | Closed and listed for sale |

Two Distinct Forces Driving Output Reductions

A critical analytical distinction separates the current curtailment picture from a simple market shock. Two overlapping but fundamentally different dynamics are at work simultaneously, and furthermore, conflating them leads to incorrect market forecasting:

-

Structural rationalisation: Decisions made independently of the sulfur crisis, including the closure and proposed sale of the Araxá SSP site with a capacity of 243,000 tonnes P₂O₅ per year, and the idling of the Patrocínio mine with 1.3 million tonnes per year of mining capacity. The financial charges associated with these closures, covering asset impairments, severance costs, and site decommissioning, are estimated at between $350 million and $400 million in pre-tax terms.

-

Reactive curtailments: Temporary suspensions and output reductions directly triggered by feedstock unavailability and cost escalation resulting from the Strait of Hormuz disruption.

The structural closures represent permanent capacity removal. The reactive curtailments are theoretically reversible, but only if sulfur supply normalises within a timeframe that prevents further asset deterioration or commercial contract losses. These supply chain disruptions are compounding pre-existing pressures across the sector.

Which Facilities Survive and Why: The Product Mix Principle

The operational survivors in the current environment share a common characteristic: product mix optionality and feedstock flexibility. The Cajati facility in São Paulo state has continued operations by sourcing sulfur through alternative import channels, enabling production of monocalcium phosphate for the animal nutrition market. This higher-margin specialty product justifies elevated input costs in a way that commodity SSP production cannot.

The Fospar unit in Paraná continues blending under normal conditions but faces a hard operational deadline tied to sulphuric acid inventory levels, with fertilizer production projected to cease by the end of September 2026 if acid stocks are not replenished. This creates a near-term cliff edge that the market has not yet fully priced.

"When feedstock shocks strike, product mix and feedstock optionality determine survival. Facilities producing higher-margin specialty products for inelastic demand segments, such as animal nutrition, can justify paying a premium for constrained inputs. Commodity-grade SSP producers cannot absorb the same cost structure and are consequently the first casualties."

What the Combined US and Brazil Curtailments Mean for Global Supply Balances

Quantifying the Supply Withdrawal

The combined effect of structural closures and reactive curtailments across Brazil is estimated to remove approximately 1 million tonnes of annual phosphate production from the country's output base. Against a pre-curtailment capacity of roughly 4.6 million tonnes per year, this represents a meaningful percentage drawdown from a country that has historically supplied a significant share of its own agricultural demand.

The Brazilian curtailments do not exist in isolation. Parallel output reductions are underway at multiple North American facilities, including plants in Bartow, Florida; Faustina, Louisiana; Riverview, Florida; and Uncle Sam, Louisiana. The Faustina facility, which had already seen operating rates reduced earlier in 2026, is facing the prospect of a full operational halt according to multiple market participants, as reported by Argus Media. No specific scale of cuts has been publicly detailed for individual US plants.

The simultaneous contraction of output from both a major South American and a major North American producer creates a compounding supply withdrawal that global markets must absorb during a period when demand has not correspondingly declined. Mosaic phosphate production in Brazil thus sits at the centre of a genuinely global supply equation.

The OCP Countervailing Duty Pause: A Partial But Incomplete Offset

One significant counterbalancing development is the US government's decision to pause countervailing duties on Moroccan phosphate imports for an eight-month period. This reopens the US market to OCP volumes after a prolonged period of trade friction that traces back to 2011, when the dominant US producer alleged that Moroccan imports were causing material harm to the domestic industry.

Morocco controls the world's largest known phosphate reserves and maintains substantial export capacity. However, the extent to which Moroccan supply can substitute for reduced Brazilian or US production across other markets, particularly Latin America, is constrained by:

- Logistics and freight routing: Moroccan tonnes are better positioned for US and European markets than for competing in Latin American import markets where freight economics differ

- Product specification differences: OCP's product slate does not perfectly match the specific grade requirements across all end markets

- Existing trade relationships: Established supply relationships in Latin American markets are not easily redirected on short notice

Agricultural Market Implications: Brazil's Farms Caught in the Crossfire

The Downstream Exposure of Brazilian Agriculture

Brazil is the world's largest exporter of soybeans and a top-tier producer of corn and sugarcane, all of which are phosphate-intensive crops requiring regular fertilizer application to sustain yields. Domestic phosphate availability directly influences input costs for Brazilian farmers who are already navigating currency volatility, shifting global commodity prices, and climate uncertainty.

A sustained reduction in domestic phosphate supply forces the agricultural sector toward import dependence, exposing it to international price benchmarks and additional freight costs. Fertilizer affordability has been explicitly identified as a constraint on demand recovery in the current environment, suggesting that price-sensitive buyers are already moderating application decisions. Consequently, if supply tightens further while prices remain elevated, the risk of systematic under-fertilisation across key growing regions increases, carrying multi-season yield consequences.

The Animal Nutrition Segment: A Resilient Demand Pocket

Monocalcium phosphate, used in livestock and poultry feed formulations, behaves differently from commodity fertilizer grades in a supply shock environment. Demand for this product is relatively inelastic because livestock producers cannot simply reduce phosphate supplementation without direct animal health consequences. The deliberate decision to maintain Cajati facility operations specifically to serve this market reflects a calculated prioritisation of higher-margin, more defensible revenue during a period of acute feedstock cost pressure. This segment is likely to prove more resilient than bulk fertilizer markets throughout the disruption cycle, and broader phosphate project economics globally will increasingly reflect this shift in product mix dynamics.

The next major ASX story will hit our subscribers first

Three Scenarios for Brazilian Phosphate Recovery

| Scenario | Key Conditions | Expected Timeline | Supply Impact |

|---|---|---|---|

| Rapid Normalisation | Strait of Hormuz reopens; sulfur prices retreat; mothballed units restart | Q4 2026 to Q1 2027 | Near-full capacity recovery; limited long-term market impact |

| Prolonged Disruption | Geopolitical tensions persist; sulfur remains scarce; further curtailments required | 2027 and beyond | Sustained supply deficit; upward pressure on global phosphate prices |

| Structural Consolidation | Permanent closure of marginal assets; industry rationalisation; new entrants acquire idled capacity | Multi-year | Reduced Brazilian capacity ceiling; higher long-term price floor |

The geopolitical backdrop makes the rapid normalisation scenario increasingly uncertain. As of early July 2026, the US-Iran interim agreement signed in June appeared to be fracturing, with both sides threatening renewed escalation. Iran has indicated it would fully close Hormuz navigation in response to further US military action, a development that would remove any residual expectation of near-term sulfur supply restoration through the Gulf corridor.

The Araxá complex is also being evaluated for alternative uses, including potential niobium development, suggesting that some idled land and infrastructure may transition permanently to different commodity production rather than returning to phosphate output. In addition, the longer-term structural shift underway is accelerating interest in phosphate project development in alternative geographies as buyers seek to reduce their exposure to single-origin supply.

Key Variables to Monitor Going Forward

- Sulfur supply route diversification: Whether producers can secure sufficient volumes from alternative origins, including the US Gulf Coast, Vancouver, and the Black Sea, to sustain reactive curtailment reversals

- Fospar's sulphuric acid inventory: This facility's acid stockpile represents the most visible near-term operational deadline in Brazil's phosphate system, with fertilizer production projected to cease by late September 2026 absent replenishment

- The Araxá asset sale process: New investors or operators acquiring idled Brazilian capacity could reshape the sector's competitive structure over the medium term

- Brazilian agricultural import demand: Unmet domestic phosphate demand will translate into increased import requirements, influencing global trade flows and price benchmarks for the remainder of 2026 and into 2027

- The OCP duty pause timeline: The eight-month pause on countervailing duties creates a defined window during which Moroccan phosphate tonnes can re-enter the US market, partially reshaping competitive dynamics and potentially freeing up alternative supply for other regions

Furthermore, investors and procurement managers tracking Mosaic phosphate production in Brazil should monitor official announcements regarding curtailment extensions closely, as each facility-level decision carries direct implications for regional fertilizer availability throughout the remainder of 2026.

This article is intended for informational purposes only and does not constitute financial, investment, or trading advice. Forecasts and scenario projections involve inherent uncertainty and should not be relied upon as predictions of specific outcomes. Readers are encouraged to consult independent market intelligence and professional advisers before making investment or procurement decisions. Global commodity price assessments and fertilizer trade flow data are available through Argus Media at argusmedia.com.

Want to Stay Ahead of the Next Major Mineral Discovery Reshaping Commodity Markets?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries — instantly translating complex geological and commodity data into actionable investment insights across sectors experiencing exactly this kind of structural supply upheaval. Explore how historic mineral discoveries have generated extraordinary returns, and begin your 14-day free trial today to position yourself ahead of the market before the next major discovery is announced.