July 10, 2026

When One Waterway Feeds the World: Rethinking Agricultural Supply Chain Fragility

Global commodity markets operate on the assumption that supply chains are elastic, that disruptions in one region can be offset by redirected flows from another. Phosphate fertiliser has quietly exposed the limits of that assumption. Unlike oil, where alternative routes, strategic reserves, and substitute energy sources provide meaningful buffers, the chemistry of food production is governed by rigid biological and industrial constraints. Crops require phosphorus. Phosphorus requires processing. Processing requires sulfuric acid. Sulfuric acid requires sulfur. And right now, a significant portion of that sulfur cannot move.

The escalation of the Iran conflict in 2026 has turned a theoretical chokepoint risk into a live agricultural crisis, with Mosaic cuts phosphate production decisions reverberating from fertiliser terminals in Tampa to grain farms across the U.S. Midwest. Understanding why this disruption is structurally different from previous commodity shocks, and what it means for food security timelines, requires working backward through the chemistry rather than forward through the geopolitics.

When big ASX news breaks, our subscribers know first

The Strait of Hormuz as Agricultural Infrastructure

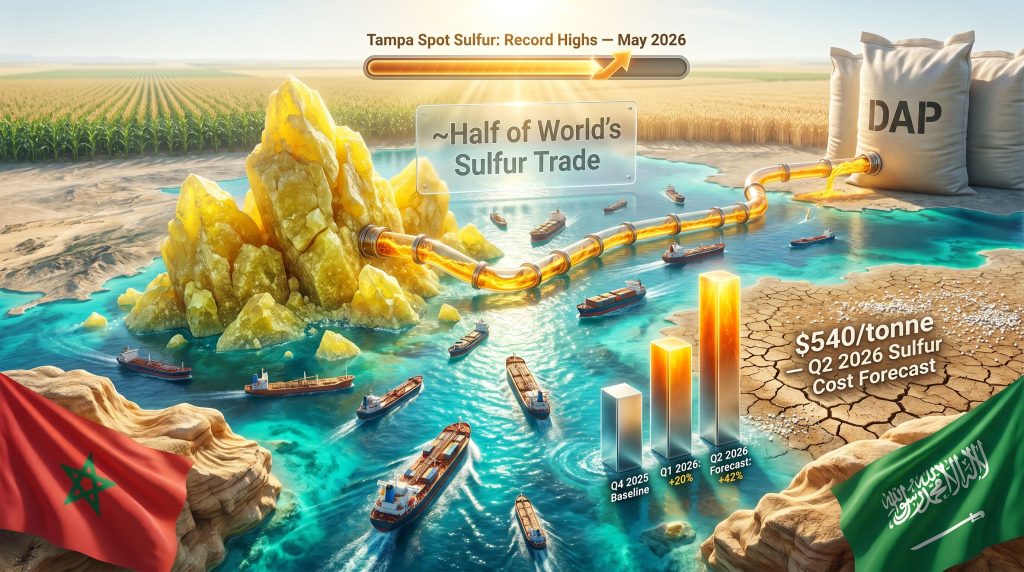

Most analysts frame the Strait of Hormuz through an energy lens, tracking oil tanker movements and crude price volatility. The fertiliser angle is far less discussed, yet arguably more consequential for long-term food security. Approximately one-fifth of globally traded phosphate fertiliser and nearly half of the world's sulfur trade depend on uninterrupted passage through this 33-kilometre-wide maritime corridor, according to data cited by Bloomberg Green Markets in May 2026.

This is not a new dependency — it has simply been invisible during periods of regional stability. Gulf producers, particularly Saudi Arabia, have long supplied sulfur to processing hubs in Morocco, China, and the United States. The logistics chain functioned smoothly enough that very few fertiliser market participants modelled it as a single point of failure. The Iran conflict has, however, changed that calculus entirely.

What makes this disruption distinct from the 2022 Russia-Ukraine shock is the level at which the supply chain is being struck. The 2022 crisis disrupted end-product supply: nitrogen fertilisers (via natural gas curtailments) and potash (via sanctions on Belarusian and Russian exports) were removed from global markets. Painful, but manageable through demand substitution and trade rerouting over time. The current crisis strikes further upstream, at the chemical processing input level. Sulfur is not a fertiliser. It is the reagent that makes fertiliser production physically possible.

Critically, the market was already operating under strain before the first shot of the current conflict was fired. Mining industry demand for sulfuric acid, driven by copper, nickel, and lithium extraction requirements tied to critical minerals and energy transition needs, had already tightened the sulfur market structurally. The Strait closure did not disrupt a system with buffer capacity. It destabilised one that was already running lean.

The Irreplaceable Input: Why Sulfur Has No Substitute in Phosphate Chemistry

To understand why the current disruption cannot be engineered around quickly, it helps to trace the chemical pathway from raw rock to farm-ready fertiliser.

Phosphate rock, as mined, contains phosphorus in a form that plants cannot absorb. To become bioavailable, the rock must be reacted with sulfuric acid, producing diammonium phosphate (DAP) or monoammonium phosphate (MAP), the two commercially dominant phosphate fertiliser products. Sulfuric acid is manufactured from elemental sulfur through a high-temperature combustion and catalytic conversion process. There is no commercially viable industrial substitute for sulfuric acid in this reaction at scale. This is not a matter of economics — it is a constraint of phosphate chemistry.

The absence of a substitute input transforms every sulfur supply disruption into a direct phosphate production constraint, regardless of how much phosphate rock sits in the ground waiting to be processed.

The dual-use nature of sulfuric acid introduces an additional layer of market complexity. The same reagent used to manufacture phosphate fertiliser is also the primary processing chemical for copper ore leaching, nickel laterite processing, and certain lithium extraction pathways. As battery metal production has scaled globally, this demand has grown substantially and continuously. The fertiliser sector and the mining sector are, in effect, competing for the same input, and neither can simply walk away from it.

Furthermore, global commodity market disruptions of this nature rarely resolve in isolation — they tend to cascade across interconnected supply chains in ways that compound the initial shock.

Tampa spot sulfur prices reached record highs in May 2026, reflecting this simultaneous demand pressure. DAP prices climbed to their highest levels since October 2025, while forward cost curves for both sulfur and ammonia pointed toward further deterioration through the second quarter.

The Cost Escalation Timeline

| Period | Sulfur Cost (per long ton) | Sequential Change |

|---|---|---|

| Q4 2025 (baseline) | Below $315 (implied) | Baseline |

| Q1 2026 (actual) | $379 | +20% |

| Q2 2026 (forecast) | ~$540 | +42% further |

Ammonia, a separate but equally essential input for DAP and MAP production, carries a Q2 2026 cost forecast of approximately $610 per tonne, adding compounding pressure to an already compressed margin structure.

Mosaic Cuts Phosphate Production: Scale, Logic, and Reversibility

The United States' largest phosphate fertiliser producer, Mosaic Co., has responded to the sulfur supply crisis with a structured production curtailment strategy. According to a recent earnings call report, CEO Bruce Bodine confirmed that the company is reducing operating rates at its Bartow, Florida and Louisiana facilities to approximately 50% of nameplate capacity, with the primary rationale being margin preservation rather than physical inability to operate.

The operational logic is straightforward but counterintuitive: running at full production capacity while purchasing sulfur at record spot prices generates negative incremental margin. Every additional tonne of phosphate produced under current input cost conditions requires buying sulfur at prices that erode the revenue value of the output. Curtailment allows the company to limit exposure to peak-priced spot sulfur purchases while retaining the ability to rapidly restore output once conditions normalise.

The scale of the production reduction is significant:

- Nearly 2 million tonnes removed from U.S. phosphate output (Florida and Louisiana combined)

- Approximately 1 million additional tonnes previously taken offline from two Brazilian processing facilities

- Combined U.S. curtailments represent roughly one-tenth of total U.S. phosphate production capacity, according to U.S. Geological Survey data

- Full-year 2026 production guidance has been withdrawn entirely, reflecting the depth of uncertainty around raw material availability

Mosaic has also indicated that additional curtailment options exist if the Middle East conflict extends further into the growing season, suggesting the company has mapped a range of operational scenarios tied to geopolitical resolution timelines.

The reversibility claim warrants scrutiny. While idled facilities can theoretically be brought back online when sulfur prices normalise, industrial phosphate processing plants require procedural restart sequences that take time. A rapid resumption of full capacity following an extended partial shutdown is operationally feasible but not instantaneous, and market timing relative to planting seasons introduces additional complexity.

Financial Consequences: The Numbers Behind the Margin Compression

The earnings data from Q1 2026 quantifies the severity of the cost squeeze in concrete terms.

Mosaic reported a $373 million operating loss for the first quarter of 2026. Adjusted earnings per share came in at $0.05, falling well short of analyst consensus estimates of $0.23. The company's shares fell as much as 4.6% following the earnings announcement. These figures reflect the combined impact of elevated sulfur costs, rising ammonia prices, and weak farmer demand. The broader commodity market volatility environment has further complicated the company's ability to hedge its input cost exposure effectively.

CEO Bruce Bodine described the simultaneous pressure from elevated input costs and constrained farmer purchasing power as a situation that cannot be sustained at current levels, with margins effectively trapped between rising costs and demand-side affordability limits.

The nitrogen fertiliser sector tells a strikingly different story for the same quarter. CF Industries and Nutrien each reported approximately 20% year-over-year sales growth, benefiting from elevated nitrogen prices without exposure to the same sulfur-driven cost pressures. This divergence illustrates how the Iran conflict has created asymmetric impacts across fertiliser sub-sectors, with phosphate producers absorbing a disproportionate share of the supply chain shock while nitrogen producers capture higher prices with relatively stable input costs.

Q1 2026 Financial Snapshot

| Metric | Value | Context |

|---|---|---|

| Operating loss | $373 million | Q1 2026 |

| Adjusted EPS | $0.05 | vs. $0.23 consensus |

| Share price decline | -4.6% | Post-announcement |

| Sulfur cost (cost of goods sold) | $379/long ton | +20% vs. Q4 2025 |

| Q2 2026 sulfur cost forecast | ~$540/tonne | +42% sequential increase |

| Q2 2026 ammonia cost forecast | ~$610/tonne | Simultaneous pressure |

The Agricultural Downstream: Farmers, Food Security, and Difficult Choices

The financial stress inside phosphate production facilities translates directly into affordability constraints for the farmers who depend on those fertilisers. Elevated DAP and MAP prices are arriving precisely when spring planting decisions must be made, creating acute pressure on corn, soybean, and wheat growers across North America.

Farmers operating under what industry participants describe as stressed affordability conditions face three difficult choices when fertiliser costs surge:

- Absorb higher input costs and accept compressed margins on their crop output

- Reduce fertiliser application rates, accepting lower yield potential in exchange for lower input expenditure

- Shift to lower-input crop rotations, altering land use in ways that affect total grain supply volumes

None of these options is neutral. Reduced application rates do not manifest in harvest data immediately. Their impact on yields would not become measurable until Q3 and Q4 2026 at the earliest, introducing a delayed consequence that current price signals do not yet fully reflect.

The global food security dimension extends well beyond North American farm economics. Morocco's OCP Group controls approximately 70% of the world's known phosphate rock reserves, and any sustained disruption to its processing capacity carries long-duration implications for global fertiliser supply. Developing nations facing geopolitical risks in commodities markets have particularly limited capacity to absorb these price shocks. China's pre-existing DAP and MAP export restrictions, compounded by reduced sulfuric acid availability from Gulf sulfur shortfalls, have effectively removed one of the market's historical swing suppliers from the equation.

The next major ASX story will hit our subscribers first

Structural Vulnerabilities the Crisis Has Made Visible

Beyond the immediate supply shock, the Iran conflict has exposed systemic design flaws in how global fertiliser supply chains have been constructed and risk-managed.

The single-chokepoint problem has been structurally underweighted in fertiliser market risk models. The concentration of roughly half of global sulfur trade through a single 33-kilometre maritime corridor was treated as an acceptable operational dependency during an extended period of Gulf stability. The current crisis demonstrates that this dependency carries non-linear downside risk when geopolitical conditions deteriorate.

The mining-agriculture input competition represents an emerging structural tension that will intensify independent of the current conflict. As copper, nickel, and lithium processing operations scale to meet energy transition demand, their aggregate consumption of sulfuric acid will grow continuously. This competes directly with agricultural demand for the same reagent, placing structural upward pressure on sulfur prices even in the absence of geopolitical disruptions.

Trade policy friction has compounded the supply shock. Countervailing duty proceedings involving Moroccan phosphate imports into the United States introduced pricing uncertainty for importers even before the current crisis. A detailed industry report on Mosaic's curtailment decisions notes that a December 2025 ruling reduced applicable duties to 2.11%, with a subsequent appeal dismissed in March 2026. A separate class-action lawsuit alleging coordinated pricing behaviour across nitrogen, phosphorus, and potash markets since 2021, alongside Department of Justice antitrust inquiries, adds regulatory overhang to an industry already operating under extraordinary cost pressure.

Global Phosphate Producer Vulnerability Comparison

| Producer Region | Gulf Sulfur Dependency | Primary Disruption Mechanism |

|---|---|---|

| Morocco (OCP Group) | High; specific volumes not publicly confirmed | Input shortage constrains large-scale processing capacity |

| China | High; specific volumes not publicly confirmed | Reduced sulfuric acid output; DAP/MAP export restrictions compound the effect |

| Saudi Arabia | Net exporter, currently blocked | Physical blockade prevents outbound sulfur and fertiliser shipments |

| United States (Mosaic) | Primarily domestic; spot Gulf exposure for incremental supply | Record Tampa spot prices elevate cost of goods sold; 50% capacity reduction implemented |

Resolution Pathways and What the Market Is Pricing

The trajectory of the phosphate supply crisis is almost entirely contingent on geopolitical developments, which are by definition difficult to model. However, several resolution and adaptation pathways can be identified across different time horizons.

In the near term, a ceasefire or the establishment of a humanitarian shipping corridor through the Strait of Hormuz would rapidly restore sulfur flows and allow spot prices to retreat from record levels. North American refinery-derived sulfur supply could partially offset Gulf shortfalls if domestic refinery utilisation rates increase, though this provides only partial relief given the scale of the disruption. Strategic inventory drawdowns at major processing facilities could extend operational capacity for a limited period without requiring new spot sulfur purchases at peak prices.

Over the medium term, the crisis has created strong economic incentives for investment in alternative sulfur sourcing infrastructure. Expanded recovery from domestic industrial byproduct streams represents the most technically straightforward pathway. Diversifying phosphate processing geography away from Gulf-sulfur-dependent facilities could reduce chokepoint exposure over a three-to-five year horizon, though this requires capital commitments that will not materialise without extended price signals.

The broader commodity context provides an interesting counterpoint. Copper prices have demonstrated relative resilience to Middle East uncertainty in May 2026, with market commentary suggesting the copper market has developed a distinct price trend largely independent of the conflict. Gold and silver have rallied sharply, reflecting a safe-haven market response to inflation concerns partially driven by food cost pressures. The divergence between copper's resilience and phosphate's distress highlights how commodity markets are increasingly pricing geopolitical risk at the product-specific level rather than applying uniform risk premiums across resource categories.

The selective pricing of geopolitical risk across commodity markets in 2026 reflects a maturing in how institutional participants model supply chain vulnerabilities, distinguishing between commodities with substitutable supply routes and those, like sulfur-dependent phosphate, where the disruption pathway is chemically non-negotiable.

The fertiliser sector's financial stress, if prolonged beyond the current planting season, carries the potential to accelerate consolidation activity within the phosphate industry and may intensify government attention to agricultural input supply chain resilience across multiple jurisdictions. For investors, the asymmetric performance between phosphate and nitrogen producers in Q1 2026 provides a case study in how geopolitical shocks with chemistry-specific mechanisms can create sustained divergence within what is superficially treated as a single sector.

Disclaimer: This article is intended for informational and educational purposes only and does not constitute financial or investment advice. Fertiliser market conditions, geopolitical developments, and commodity prices referenced in this article are subject to rapid change. Past financial performance and cost projections cited from earnings calls represent company guidance and analyst estimates, which may not reflect future outcomes. Readers should conduct independent research and consult qualified financial professionals before making investment decisions.

Want To Stay Ahead of Supply Chain Shocks Affecting ASX-Listed Resource Companies?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries — including those exposed to critical input commodities like sulfur, phosphate, and copper — instantly transforming complex market data into actionable investment insights. Explore historic examples of major mineral discoveries and their market returns, then begin your 14-day free trial to ensure you're positioned ahead of the broader market when the next significant discovery is announced.