June 19, 2026

The Economics of Sovereignty: Understanding Africa's Shift Toward State Equity in Mining

Across the African continent, a quiet but consequential restructuring of resource ownership is underway. Governments that once competed aggressively to attract foreign mining capital by offering generous fiscal terms are now recalibrating those arrangements. The shift is rooted in a pragmatic recognition that the global energy transition has fundamentally repriced the strategic value of certain minerals, and that host nations sitting atop these deposits have more negotiating leverage today than at any point in recent history. Understanding critical minerals demand provides essential context for why nations like Mozambique are repositioning their resource governance frameworks so decisively.

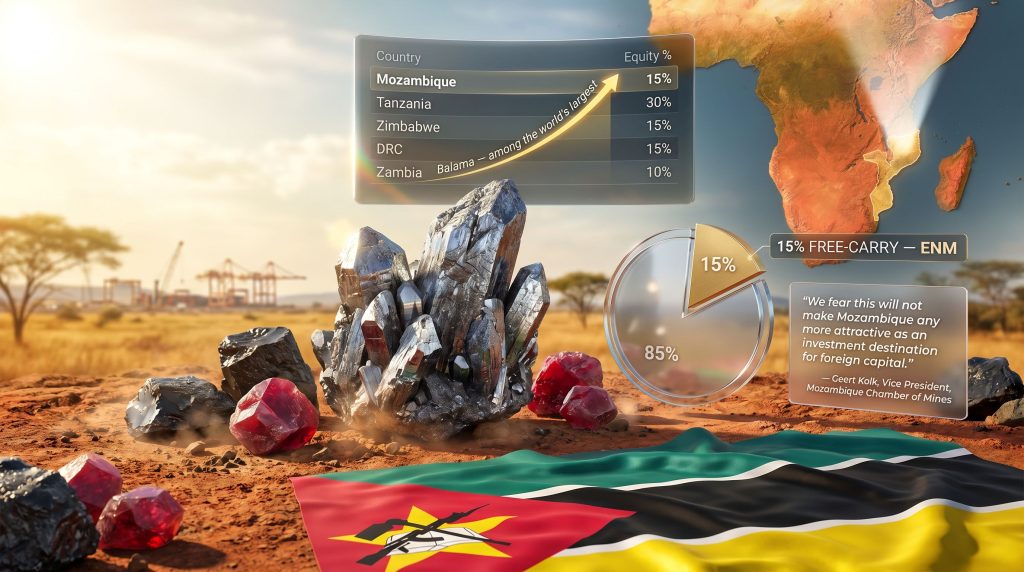

Mozambique's amended mining legislation sits squarely within this trajectory. The country's decision to mandate a minimum 15% free-carried, non-dilutable equity stake for the state in all mining ventures, administered through the National Mining Company (ENM), represents one of the most consequential regulatory shifts in southern African mining governance in years. For investors, operators, and supply chain planners with exposure to Mozambican assets, understanding the mechanics and implications of this law is no longer optional.

When big ASX news breaks, our subscribers know first

What the Mozambique 15% State Stake Mining Law Actually Requires

At its core, the Mozambique 15% state stake mining law establishes that ENM, the state mining vehicle, automatically receives an equity position in every mining venture operating under Mozambican law. Two features of this requirement distinguish it from softer forms of state participation seen elsewhere in the region.

First, the stake is free-carried, meaning the government does not contribute capital to earn its equity. Private investors must fund 100% of exploration, feasibility, construction, and development costs while the state participates in profits from the moment production commences.

Second, the stake is non-dilutable. This is legally significant because it means that future capital raises, whether through equity issuances to fund expansions, equipment upgrades, or working capital requirements, cannot reduce the state's 15% position. In a capital-intensive industry where development projects routinely require multiple financing rounds over years or even decades, this constraint adds material complexity to capital structuring.

The Export Restriction Clause

Alongside the equity requirement, the amended law introduces an export prohibition on raw and semi-processed mineral products. Operators seeking to export ore or concentrate that has not undergone a defined level of domestic processing must obtain explicit ministerial approval, and that approval is contingent on the company demonstrating a credible in-country processing plan.

This clause affects different mineral categories differently. For graphite, the distinction between flake graphite concentrate and battery-grade spherical purified graphite (SPG) is commercially enormous. Raw flake concentrate commands a fraction of the price of SPG, which requires purification to above 99.95% carbon content before it is suitable for lithium-ion battery anodes. The law's processing requirement effectively signals that Mozambique wants a share of the value-add chain, not merely royalties on raw material extraction. Furthermore, the global graphite shortage dynamics make this positioning increasingly significant for downstream battery manufacturers worldwide.

The Retroactivity Question

One of the most commercially sensitive unresolved issues is whether the law applies to existing operations holding long-term concession agreements negotiated under prior legislation. International mining law generally recognises stabilisation clauses in concession contracts, which are designed to shield investors from adverse regulatory changes enacted after a project is committed. Whether Mozambican courts or international arbitration panels would uphold such protections against the new law remains genuinely uncertain, and that uncertainty itself represents a material risk factor for active operators.

Mozambique's Mineral Endowment: Why the Stakes Are Exceptionally High

To understand why this law matters beyond Mozambique's borders, the country's resource profile is essential context.

| Mineral | Global Significance | Key Mozambique Asset |

|---|---|---|

| Graphite | Critical for EV battery anodes | Balama deposit, among the world's largest |

| Rubies | Premium gemstone export | Montepuez, the world's largest ruby mine |

| Coal | Thermal and metallurgical energy | Major reserves, previously held by Rio Tinto and Vale |

Syrah Resources' Balama operation in northern Mozambique is not merely large by African standards. It is one of the highest-grade, largest-tonnage natural flake graphite deposits identified globally, with total mineral resources measured in the hundreds of millions of tonnes. At peak operation, Balama has produced in excess of 350,000 tonnes per year of graphite concentrate, making Mozambique a genuinely pivotal swing supplier in the global graphite market.

Graphite occupies a structurally irreplaceable role in lithium-ion battery technology. The anode of a standard lithium-ion cell contains roughly 10 times more graphite by weight than lithium, a ratio that is frequently overlooked in mainstream critical minerals coverage. As battery metals investment scales globally, graphite demand is projected to grow substantially, with several industry forecasts pointing to a tripling or more of demand by 2035. Mozambique's position as a low-cost, high-volume natural graphite supplier gives the country genuine strategic leverage that its government is clearly aware of.

Gemfields' Montepuez ruby mine in northern Mozambique adds another dimension. Montepuez has fundamentally reshaped the global coloured gemstone market since its discovery, producing rubies of exceptional colour saturation from a deposit of a scale that was previously unknown in the ruby sector.

How Free-Carry Economics Affect Project Viability

The investment community's concern with the free-carry mechanism is grounded in straightforward project finance mathematics.

A free-carry equity arrangement requires the private investor to deploy 100% of development capital while receiving only 85% of the project's future cash flows. For marginal projects operating in high-cost or high-risk jurisdictions, this structural dilution of returns can move a borderline investment case from viable to unviable without any change in the underlying mineral economics.

When applied to project internal rate of return (IRR) modelling, the impact is direct. Assume a project with a pre-law IRR of 18% on 100% equity funding. If the state now captures 15% of cash flows from first production without contributing to the capital base, the effective IRR for the private investor on that same capital outlay declines, sometimes materially, depending on the project's production profile and capital intensity.

In scenarios where projects carry substantial upfront capital expenditure relative to operating cash flows, the compression can be significant enough to breach minimum return thresholds required by project lenders or equity sponsors.

The Mozambique Chamber of Mines, through its vice president Geert Kolk at the Victoria Falls Mining Conference in 2026, made the industry's position unambiguous. Kolk stated that the organisation viewed the mandatory free-carry stake as likely to reduce Mozambique's attractiveness as a destination for foreign mining capital. This is not a peripheral concern from a small lobby group. The Chamber represents the operators of Mozambique's most significant producing assets, and formal industry opposition of this nature sends a clear signal to investors assessing new project commitments.

Regional Comparison: Where Mozambique Sits on the Spectrum

| Country | State Equity Requirement | Free-Carry Provision | Export Restrictions |

|---|---|---|---|

| Mozambique | 15% minimum | Yes, non-dilutable | Yes, ministerial approval required |

| Tanzania | Up to 16% | Partial | Yes |

| Zimbabwe | 51% (indigenisation, select sectors) | No | Selective |

| DRC | 10% (state and local combined) | No | Partial |

| Zambia | Negotiated case-by-case | No | No formal ban |

The non-dilutable feature places Mozambique's framework closer to the more restrictive end of the regional spectrum. Tanzania's broadly comparable equity thresholds have already demonstrated the capacity to delay project development timelines and reshape deal structures. Zimbabwe's higher indigenisation requirements in certain sectors have historically redirected capital toward competing jurisdictions, though Chinese state-backed financing has partially filled that gap.

The Local Processing Debate: Sound Economics or Premature Mandate?

The export restriction clause reflects a value-add argument that has genuine economic merit. The gap between the export revenue generated by raw graphite concentrate versus battery-grade spherical purified graphite is substantial. Purification and shaping processes transform a relatively low-value industrial commodity into a premium battery material commanding significantly higher per-tonne pricing. If Mozambique could capture even a portion of that value domestically, the multiplier effects on employment, tax revenue, and foreign exchange earnings would be material.

However, the Chamber of Mines has identified the gap between policy aspiration and commercial reality with precision. Kolk acknowledged the legitimacy of the processing ambition while noting that its commercial viability depends on the government delivering reliable infrastructure. Specifically:

-

Power supply: Northern Mozambique's electricity grid is not currently configured to support energy-intensive mineral processing at industrial scale. Graphite purification, for example, involves high-temperature thermal treatment requiring consistent, cost-competitive power.

-

Water access: Processing operations in the Cabo Delgado and Tete provinces face genuine water availability and reliability constraints that add capital and operational cost to any in-country processing facility.

-

Logistics connectivity: The export pathway through Mozambican ports, particularly for landlocked processing scenarios, requires rail and road infrastructure that is still developing. Nacala Logistics Corridor investments have improved the picture, but capacity constraints remain.

The Chamber's position is not opposition to processing in principle. It is a call for sequencing: government infrastructure commitments must be credible and deliverable before processing mandates become commercially viable for investors.

China's Shadow Over Mozambique's Investment Calculus

One underappreciated dimension of Mozambique's policy shift is how it interacts with the changing landscape of mining finance in Africa. Western private capital and publicly listed mining companies operate under strict return threshold requirements, driven by shareholder expectations and project finance covenant structures. A 15% non-dilutable free-carry stake compresses those returns in ways that can disqualify projects from institutional capital allocation.

Chinese state-backed financing entities operate under a fundamentally different return calculus. Access to strategic mineral supply, rather than project-level IRR optimisation, often drives Chinese investment decisions in African mining. This asymmetry means that policies which deter Western private capital may not deter Chinese state-linked investors to the same degree, and could inadvertently tilt the ownership landscape of Mozambican mining assets toward structures more aligned with Chinese strategic interests than with Western supply chain diversification goals.

This is a speculative but analytically important point. It is not inevitable, and Mozambique retains the policy flexibility to structure terms differently for different investors. However, the directional risk is real and worth factoring into any geopolitical assessment of where Mozambican graphite ultimately flows in a supply-constrained global market. Consequently, the broader dynamics around metals mining geopolitics are increasingly shaping how Western governments view African resource governance reform.

The next major ASX story will hit our subscribers first

Three Scenarios for Mozambique's Mining Investment Climate

Scenario 1: Orderly Adaptation

Established operators renegotiate project economics to absorb the free-carry cost. The government demonstrates credible infrastructure commitments. New entrants adjust feasibility models accordingly and continue advancing projects. Mozambique retains its position as a preferred graphite and gemstone investment destination within a recalibrated fiscal framework.

Scenario 2: Investment Retreat

Capital allocation decisions shift toward competing graphite jurisdictions, including Tanzania, Madagascar, and Canada, where project economics are not subject to free-carry equity requirements. Exploration activity in Mozambique declines. Existing operators curtail expansion plans. The country's share of global graphite supply growth underperforms its geological potential.

Scenario 3: Legal Contest and Structural Bifurcation

Existing concession holders invoke stabilisation clauses and pursue international arbitration to contest retroactive application of the law. A two-tier system emerges between legacy projects operating under prior terms and new entrants subject to the full 15% requirement. Prolonged legal uncertainty suppresses new project commitments while existing operations continue under contested frameworks.

The most probable near-term outcome is a combination of elements from all three scenarios, varying by project stage, operator nationality, and asset quality.

Frequently Asked Questions: Mozambique Mining Law and the 15% State Stake Rule

What is the Mozambique 15% state stake mining law?

Mozambique's amended mining legislation requires the state, through ENM, to hold a minimum 15% free-carried and non-dilutable equity interest in all mining ventures operating within the country. Reuters reporting on the new legislation provides a useful overview of how the law was enacted and its immediate regulatory implications.

Does the 15% rule apply to existing mining operations?

The application to existing mines operating under long-term concession agreements negotiated before the amendment remains legally uncertain. This ambiguity is a primary concern for active operators and investors with legacy positions.

What minerals are most affected?

Graphite is the most strategically significant commodity affected given Mozambique's global position as a top producer. Rubies and coal are also subject to the new framework. Graphite's critical role in EV battery supply chains makes this law particularly relevant to clean energy investors worldwide.

What does free-carry mean in this context?

The government receives its equity share without contributing development capital. Private investors bear 100% of project construction and development costs while the state participates in production profits from day one.

Can companies still export unprocessed minerals?

Exports of raw or semi-processed mineral products are prohibited unless the relevant minister grants specific approval, contingent on a credible in-country processing plan being demonstrated by the applicant. In addition, critical minerals supply chains across Europe and other Western markets are watching these export restriction clauses closely, given their potential to disrupt downstream battery manufacturing inputs.

Key Variables Investors Should Track

-

Legislative implementation timeline: The specific dates and transitional provisions governing when the law takes effect for new versus existing projects remain critical to monitor.

-

ENM's institutional capacity: Whether the National Mining Company has the governance structures, technical expertise, and financial resources to function as an effective and constructive equity partner will significantly influence project dynamics.

-

Infrastructure delivery: Government commitments on power, water, and logistics in northern Mozambique will serve as the clearest indicator of whether processing mandates are intended as development tools or de facto barriers.

-

Arbitration developments: Any legal challenges from existing concession holders that proceed to international arbitration will create precedent with implications well beyond individual projects.

-

Regional capital flows: Investment allocation trends across competing graphite and critical mineral jurisdictions will reveal how the market is pricing Mozambique's regulatory shift relative to alternatives. The Assay's analysis of the proposed reforms offers additional technical detail on how the legislation was structured before enactment.

This article contains forward-looking analysis and scenario projections that involve assumptions and uncertainties. Nothing in this article constitutes investment advice.

Want to Track the Next Major Critical Minerals Discovery Before the Market Catches On?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries — including graphite, battery metals, and other critical commodities reshaping the global energy transition — instantly translating complex announcement data into actionable investment insights. Explore Discovery Alert's dedicated discoveries page to understand how historic mineral discoveries have generated substantial returns, and begin your 14-day free trial today to position yourself ahead of the broader market.