June 5, 2026

The Architecture of Sovereign Control: Understanding Mozambique's 2026 Mining Law

Across the global energy transition, a quiet but consequential battle is unfolding beneath the Earth's surface. The minerals powering electric vehicles, wind turbines, and defence systems are not evenly distributed, and the nations that hold them are rapidly learning to leverage that asymmetry. Mozambique, long regarded primarily as a natural gas frontier, has emerged as a pivotal node in the critical minerals supply chain — and its government has just fundamentally rewritten the rules of engagement through new Mozambique mining law critical minerals legislation.

Signed into law on June 3, 2026, by President Daniel Chapo following parliamentary approval in May, Mozambique's new mining legislation represents the most structurally significant shift in the country's resource governance framework in over a decade. For investors, operators, and geopolitical strategists alike, understanding exactly what changed, why it changed now, and what it means in practice is no longer optional.

When big ASX news breaks, our subscribers know first

From Licence-Based Extraction to Sovereign Value Capture

How the Old Framework Functioned

Mozambique's previous regulatory architecture, anchored by Mining Law 20/2014, treated mineral resources as state property in principle while granting operational control to foreign operators through licences and contracts. State equity participation was not universally mandated under that framework, and domestic processing was encouraged only where considered economically viable — a threshold that operators could interpret broadly.

This structure attracted significant foreign capital but generated persistent criticism that the economic benefits of extraction were disproportionately captured abroad, particularly through raw mineral exports processed in third countries — primarily China — before re-entering global supply chains at much higher value.

What the 2026 Legislation Actually Requires

The new law introduces three core structural changes that collectively redefine the operating environment for every mining project in Mozambique:

-

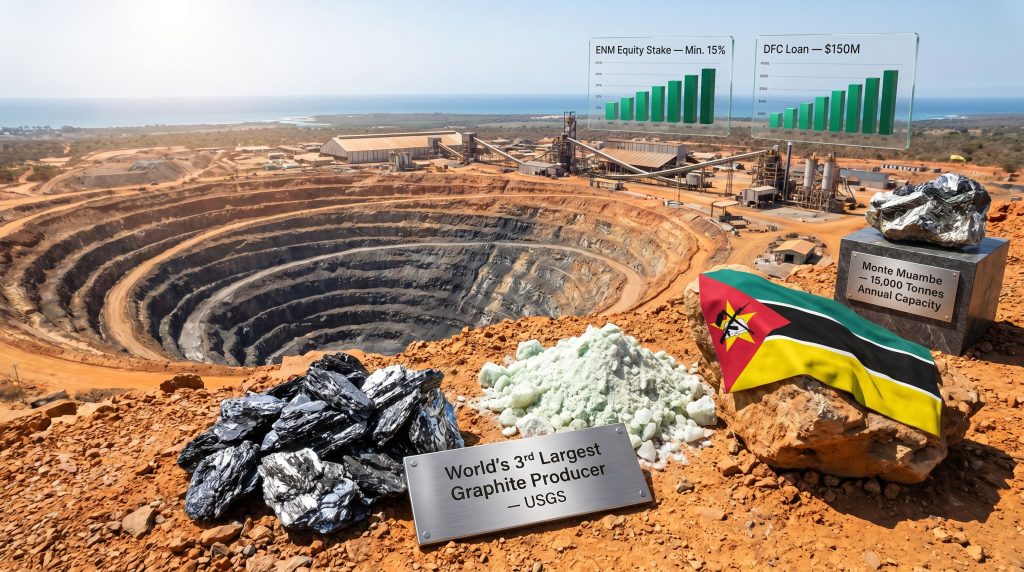

Mandatory free-carried state equity: The state-owned enterprise ENM (Empresa Nacional de Minas) receives a minimum 15% stake across all stages of the mining value chain in every project. Critically, this is a free-carried interest — ENM acquires this equity without contributing capital at the point of entry.

-

Export prohibition on unprocessed minerals: Raw or semi-processed mineral exports are banned as the default position. Operators seeking exemptions must obtain ministerial approval and demonstrate a credible domestic processing plan.

-

Strategic minerals contract model: For resources classified as strategically critical, a new mandatory contract structure replaces the more flexible licensing arrangements previously available, with state participation thresholds potentially exceeding 15% depending on the mineral's classification.

Furthermore, the legislation creates a two-tier regulatory architecture. Conventional minerals operate under a reformed standard framework, while strategically critical resources face a more controlled regime with elevated governance and equity requirements. This dual-track design is more sophisticated than the blunt resource-nationalist measures adopted by some peer jurisdictions.

The Mozambique mining law reforms have, however, left one critical issue unresolved: whether existing operations are subject to retroactive application remains legally ambiguous — a significant concern for active project holders.

| Reform Provision | Applies To | Core Requirement |

|---|---|---|

| 15% free-carried ENM equity | All mining projects | No capital contribution required from the state |

| Strategic minerals contract | Critical/strategic resources | Mandatory new contractual framework |

| Export ban on raw minerals | All mineral categories | Ministerial approval + domestic processing plan |

| Expanded public tendering | Areas with proven mineral potential | Competitive tender process mandated |

| Retroactive application | Existing operations | Legally unresolved — significant ambiguity |

Why Mozambique's Graphite Deposits Are Geopolitically Irreplaceable

Understanding Graphite's Role in the Battery Supply Chain

To appreciate the strategic weight of Mozambique's new mining law, it is necessary to understand what makes graphite fundamentally different from most industrial minerals. Graphite serves as the anode material in lithium-ion batteries, the dominant technology powering electric vehicles. Unlike cathode materials such as lithium or cobalt, where substitution research is relatively advanced, graphite's electrochemical properties make it difficult to replace in conventional battery architectures.

Battery-grade graphite undergoes a complex transformation from raw flake graphite through several processing stages — including purification to above 99.95% carbon content and spheroidisation — before it becomes suitable for anode production. This processing expertise is currently concentrated overwhelmingly in China, creating a critical bottleneck that Western battery manufacturers have struggled to replicate at scale. Indeed, the graphite supply shortage facing Western nations makes Mozambique's deposits all the more strategically significant.

Mozambique's Competitive Position in Global Graphite Supply

According to the U.S. Geological Survey (USGS), Mozambique ranks as the world's third-largest graphite producer, behind China and Madagascar. The Balama deposit in Cabo Delgado province, operated by Syrah Resources, is recognised as one of the largest flake graphite deposits globally by contained resource. Its scale provides Mozambique with a genuine claim to being a long-term anchor supplier for Western supply chain diversification.

What is less commonly understood is that flake graphite from different geological sources has variable characteristics that affect its suitability for battery processing. Large flake graphite, which Mozambique's deposits produce in significant proportions, commands premium pricing and is particularly suited for the spheroidisation process that produces battery-grade spherical graphite. This geological quality advantage is not replicated in all competing sources.

Mozambique's Critical Mineral Asset Landscape

| Mineral | Global Position | Key Project | Operator | Strategic End Use |

|---|---|---|---|---|

| Graphite | 3rd largest producer (USGS) | Balama | Syrah Resources (ASX: SYR) | EV battery anodes |

| Graphite | Development stage | Ancuabe | Triton Minerals (acquisition pending) | Battery supply chain |

| Graphite | Operational | Nipepe | DH Mining (Chinese-owned) | Processing and export |

| Rare Earths | Emerging producer | Monte Muambe | Altona Rare Earths (UK) | Defence, EVs, wind energy |

The US-China Contest Playing Out on Mozambican Soil

Washington's Financial Commitments in the Graphite Sector

The United States has constructed an integrated financial architecture around Mozambique's graphite sector, with Syrah Resources' Balama operation at its centre. The U.S. International Development Finance Corporation (DFC) provided a $150 million loan to Syrah's local subsidiary in November 2024, securing a direct financial stake in the world's largest graphite operation outside China.

This followed an earlier commitment in 2022, when the U.S. Department of Energy extended a $102 million loan to support Syrah's Vidalia anode processing facility in Louisiana. The Vidalia facility processes graphite shipped from Balama, creating a vertically integrated supply chain that the US government has deliberately constructed to reduce anode dependency on Chinese processors.

In March 2026, the DFC proposed converting a portion of its debt exposure at Syrah into equity. If finalised, this transaction would position the agency as Syrah's second-largest shareholder with a stake approaching 20%, effectively making the US government a direct equity participant in Mozambique's most strategically significant graphite mine. The proposal remains subject to audits and regulatory approvals.

The USTDA's Rare Earth Foothold

Washington's ambitions in Mozambique extend beyond graphite. In February 2026, the U.S. Trade and Development Agency (USTDA) awarded a grant to fund pre-feasibility study work on the Monte Muambe rare earth project, being advanced by British company Altona Rare Earths. The project carries a projected annual production capacity of 15,000 tonnes of mixed rare earth carbonate.

Rare earth elements — a group of 17 metals including neodymium, praseodymium, and dysprosium — are essential inputs for permanent magnets used in EV motors, wind turbine generators, and precision defence systems. The complexity of rare earth supply chains gives China structural leverage over Western industrial production that the US and allied nations have been urgently working to erode.

China's Industrial Investment and Acquisition Strategy

China's position in Mozambique's graphite sector is built on direct industrial investment rather than financial instruments. In January 2026, President Chapo inaugurated a graphite processing plant with 200,000 tonnes of annual capacity owned by Chinese company DH Mining, which invested $200 million in the Nipepe project. This facility represents a significant piece of in-country processing infrastructure and the most capitalised single investment in Mozambican graphite processing to date.

Simultaneously, Chinese group Shandong Yulong Gold, through subsidiary NQM Gold 2, is pursuing a 70% acquisition stake in Triton Minerals' Ancuabe graphite project. The transaction was initiated in 2024 but has not yet received final government approval from Maputo — a fact that takes on considerably greater significance under the new regulatory framework.

"Mozambique's new mining law arrives at precisely the moment when both Washington and Beijing require decisions from Maputo. The DFC's proposed equity conversion and the Shandong Yulong acquisition both need government cooperation. This timing concentrates Mozambique's negotiating leverage at its peak."

Mozambique in Africa's Broader Resource Nationalism Wave

A Continent-Wide Policy Recalibration

Mozambique's 2026 overhaul does not exist in isolation. It is the latest expression of a continent-wide reassertion of sovereign control over mineral wealth that has been building since the early 2020s, accelerated by three converging pressures: the surge in critical minerals demand driven by energy transition targets, post-pandemic fiscal constraints that have forced governments to seek new domestic revenue streams, and growing political expectations that natural endowments should generate tangible improvements in living standards.

Comparative Policy Framework: Africa's Resource Nationalism Landscape

| Country | Target Mineral | Primary Policy Tool | Investor Outcome |

|---|---|---|---|

| Mozambique (2026) | Graphite, Rare Earths | 15% free equity + export ban | Investment uncertainty; peak leverage over US/China |

| Zimbabwe | Lithium | Export ban on unprocessed ore | Mixed — attracted some processing investment, deterred others |

| DRC | Copper, Cobalt | Domestic value-addition requirements | Persistent operator tensions; partial compliance |

| Mali | Gold | Increased mandatory state share | Significant investor-government disputes; arbitration threats |

| Guinea | Bauxite | Local processing requirements | Repeated disputes; prolonged resolution timelines |

What Makes Mozambique's Approach Structurally Different

Unlike Mali and Guinea, where resource nationalism reforms were primarily reactive to political transitions or fiscal emergencies, Mozambique's 2026 legislation is explicitly framed around critical minerals strategy and global supply chain positioning. The dual-track regulatory structure, separating strategic minerals from conventional resources, reflects a level of policy sophistication that distinguishes Maputo's approach from blunter instruments used elsewhere.

However, the retroactivity ambiguity is a structural weakness shared with earlier African mining reforms that generated the most prolonged legal disputes. The legislation does not clearly specify whether existing long-term agreements are grandfathered or subject to renegotiation. This unresolved question is, arguably, a more significant investor risk than the equity participation requirement itself.

Investment Risk Framework: Mapping Exposure Across Active Projects

Balama Graphite (Syrah Resources)

Syrah's Balama operation faces potential renegotiation pressure despite holding long-term agreements that may provide contractual protection. The DFC's proposed equity conversion adds a sovereign-to-sovereign dimension to the regulatory dynamic — any future negotiation between Maputo and Syrah would implicitly involve the US government as an equity stakeholder, fundamentally altering the political calculus on both sides.

The processing infrastructure gap creates an additional operational risk: if Mozambique enforces the export ban on raw graphite without adequate domestic spherical graphite processing capacity in place, Balama's ability to sustain production volumes would be constrained.

Ancuabe Graphite (Triton Minerals / Shandong Yulong Gold)

The pending Chinese acquisition of a 70% stake in Ancuabe is the transaction most directly exposed to the new framework. Shandong Yulong Gold still requires final government approval — approval that is now governed by legislation designed to maximise Mozambican sovereign value capture. The mandatory 15% ENM stake could alter the transaction's underlying economics, requiring renegotiation of deal terms before Maputo grants its consent.

Monte Muambe Rare Earths (Altona Rare Earths)

Monte Muambe's advanced exploration status means it has not yet transitioned to a mining licence under either the old or new regulatory framework. The new strategic minerals contract model will almost certainly apply to any future licensing, requiring compliance with the more demanding governance and equity participation provisions. The USTDA pre-feasibility grant positions the project within the US strategic supply chain — a factor that introduces a geopolitical dimension into what might otherwise be a straightforward licensing process.

Key Investor Risk Considerations

-

Retroactivity risk: Until the government formally clarifies whether new provisions apply to existing licences, all active projects face an unquantifiable period of contractual uncertainty.

-

Processing infrastructure gap: The export ban on raw minerals creates an obligation that Mozambique's current in-country beneficiation capacity cannot immediately absorb. The DH Mining facility at Nipepe has 200,000 tonnes of annual processing capacity, but it is Chinese-owned, raising questions about whether it serves broader sovereign value-capture objectives.

-

Capital dilution modelling: New project financing must now price in ENM's free-carried equity, which reduces the effective return on capital for the remaining shareholders without reducing their capital expenditure obligations.

-

Ministerial discretion risk: The requirement for ministerial approval of export exemptions introduces a regulatory bottleneck that could delay production ramp-ups at projects lacking established domestic processing infrastructure.

The 15% free equity requirement is comparable to provisions in other African jurisdictions and is therefore priceable. The unresolved retroactivity question is not — and until it is resolved, it represents the single largest source of near-term legal uncertainty for the Mozambican mining sector as a whole.

The next major ASX story will hit our subscribers first

Frequently Asked Questions: Mozambique Mining Law and Critical Minerals

What is the central change introduced by Mozambique's 2026 mining law?

The legislation mandates a minimum 15% free-carried equity stake for state enterprise ENM in every mining project across all value chain stages, and prohibits the export of raw or semi-processed minerals without ministerial approval accompanied by a domestic processing plan. These Mozambique mining law critical minerals provisions represent the most substantial governance overhaul in more than a decade.

Does the new law apply to mines already in operation?

The legislation does not explicitly resolve whether its provisions apply retroactively to operations governed by pre-existing long-term agreements. This ambiguity is the most material legal uncertainty facing current operators and has not yet been formally clarified by the government. Consequently, proposed mining law reforms continue to attract close scrutiny from international legal and investment communities.

Why is Mozambique's graphite sector considered strategically critical?

Mozambique is the world's third-largest graphite producer according to the USGS. Graphite is an essential anode material for EV batteries, and with China controlling the majority of battery-grade processing capacity, Mozambique's large-flake deposits represent one of the few credible sources for Western supply chain diversification. The geological quality of Mozambican graphite, particularly its large-flake characteristics, enhances its suitability for battery-grade processing.

How does the US government hold exposure to Mozambique's mining sector?

The DFC provided a $150 million loan to Syrah Resources' Mozambican subsidiary in November 2024, and in March 2026 proposed converting part of that debt into equity that would give the agency a shareholding approaching 20% in Syrah. The U.S. Department of Energy also provided a $102 million loan to Syrah's Vidalia anode facility in Louisiana, which processes Balama graphite.

What is ENM and what role does it play under the new framework?

ENM (Empresa Nacional de Minas) is Mozambique's state-owned mining enterprise and the vehicle through which the government acquires its mandatory stakes. Under the 2026 law, ENM receives a minimum 15% free-carried interest in all new mining projects without contributing capital at entry.

What Comes Next: Mozambique's Window of Maximum Leverage

The 2026 legislation represents Mozambique's attempt to institutionalise its negotiating leverage at the precise moment when that leverage is at its structural peak. Both the United States and China require decisions from Maputo on active transactions. The global energy transition continues to intensify demand for graphite and rare earth elements. And no comparable alternative to Mozambican supply has yet been developed at sufficient scale to replace it.

However, this leverage is inherently time-limited. As alternative graphite sources in Canada, Tanzania, and elsewhere progress through development, and as synthetic graphite capacity expands in the United States and Europe, Mozambique's indispensability will diminish. The government's handling of the retroactivity question, the pace of domestic processing infrastructure development, and the terms on which it resolves the Shandong Yulong acquisition will collectively signal whether Maputo intends to manage this leverage strategically or risk turning it into prolonged investor-state conflict.

The broader critical minerals trade dynamics shaping global markets add further pressure on Mozambique to resolve these ambiguities quickly. Furthermore, the mining geopolitical landscape is shifting rapidly, and Mozambique's window to extract maximum value from its sovereign position may be shorter than policymakers currently anticipate.

The precedents from Mali and Guinea are instructive — both countries achieved short-term revenue gains from aggressive resource nationalism while generating disputes that deterred subsequent capital inflows. Mozambique's dual-track design suggests a more calibrated approach, but the retroactivity ambiguity remains an unresolved fault line. That fault line could yet determine whether this round of Mozambique mining law critical minerals reform is remembered as a sovereign success or a cautionary tale.

The legal framework under review continues to evolve, and stakeholders across the investment community will be watching closely as Maputo moves to clarify the outstanding provisions that remain at the centre of international concern.

This article is intended for informational purposes only and does not constitute financial or investment advice. Readers should conduct independent due diligence before making any investment decisions. Forward-looking statements and projections involve inherent uncertainty. For ongoing coverage of African mining and economic policy, visit Ecofin Agency.

Want to Track the Next Major Mineral Discovery Before the Market Does?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries — including graphite, rare earths, and other critical minerals driving the global energy transition — instantly turning complex geological data into actionable investment insights. Explore Discovery Alert's discoveries page to see how historic mineral discoveries have generated substantial market returns, and begin your 14-day free trial today to position yourself ahead of the broader market.