June 24, 2026

The Hidden Cost of Free-Carry: How Resource Nationalism Is Reshaping Mining Investment Calculus in Africa

Across the African continent, a quiet but consequential rebalancing of power is underway between resource-rich governments and the foreign capital they have long relied upon to develop their mineral wealth. Driven partly by the global energy transition and partly by decades of frustration over perceived value leakage, more African nations are encoding resource nationalism directly into their legislative frameworks. The question investors now face is not whether this trend will continue, but how aggressively individual countries will pursue it, and at what cost to their own competitiveness.

Mozambique's 2026 mining law amendments represent one of the most structurally significant regulatory shifts in Southern African mining governance in recent years. Signed into law by President Daniel Chapo on June 3, 2026, following parliamentary approval in May 2026, the legislation rewrites the foundational rules governing foreign participation in the country's mining sector. For investors already deployed in Mozambique, and for those evaluating entry, understanding Mozambique mining law foreign investment dynamics is not optional. It is essential.

When big ASX news breaks, our subscribers know first

From Lei No. 20/2014 to the 2026 Amendment: A Legislative Evolution

Mozambique's mining governance architecture has evolved through several legislative cycles. The country's original modern mining law, Law No. 14/2002, permitted foreign entities to hold 100% equity stakes in locally incorporated mining companies, with state participation negotiated on a discretionary, case-by-case basis. The later Lei No. 20/2014 retained broadly permissive ownership structures while strengthening local content and licensing requirements.

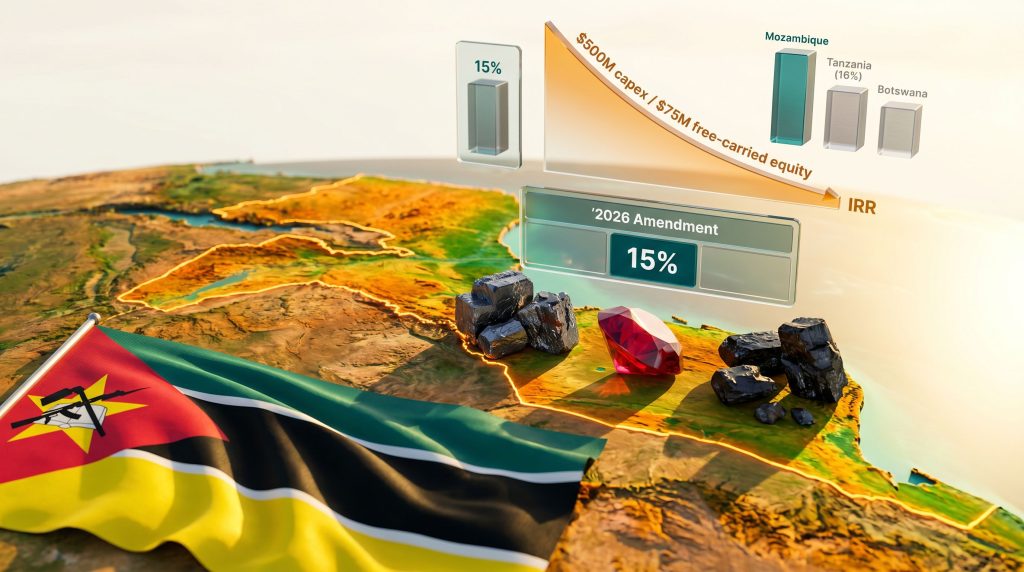

The 2026 amendment breaks sharply from this trajectory. Its central mechanism is the mandatory allocation of a minimum 15% equity stake in every mining operation to Empresa Nacional de Minas (ENM), a newly created state entity established specifically as the centralised vehicle for government equity participation across the sector. This stake is both free-carried and non-dilutable, which, as explored below, creates compounding financial risk for private investors that goes well beyond the headline percentage.

The table below summarises the key policy shifts between the old and new frameworks:

| Policy Dimension | Pre-2026 Framework | 2026 Amendment |

|---|---|---|

| Foreign Equity Ownership | Up to 100% permitted | Capped by mandatory 15% state stake |

| State Participation Model | Discretionary and negotiated | Automatic, non-dilutable via ENM |

| Capital Contribution by State | Negotiated case-by-case | None, free-carried by private investors |

| Mineral Export Rights | Broadly permitted | Requires ministerial approval |

| Construction Mineral Access | Open to foreign entities | Reserved for Mozambican nationals only |

| Local Content Obligations | Advisory and limited | Mandatory supplier preference enforced |

Deconstructing the Free-Carry Mechanism

The concept of a free-carry equity stake is not new to African mining. What distinguishes Mozambique's model is the combination of zero capital contribution, permanent non-dilutability, and parliamentary signals that the 15% floor may rise in future legislative cycles. Each of these elements carries distinct financial implications.

Under a standard free-carry arrangement, the state receives equity in a project without contributing to exploration, feasibility, construction, or operational costs. The private investor absorbs 100% of the upfront capital risk while the state retains a protected ownership share that insulates it from the stages of a project where loss is most probable. Furthermore, definitive feasibility studies conducted prior to development become critically important for investors to model these compounding costs accurately.

Hypothetical Illustration: A mid-tier graphite development project requiring $500 million in capital expenditure would, under the 2026 law, automatically deliver approximately $75 million in project equity value to ENM without any corresponding capital contribution. The private sponsor funds all development risk while the state captures a permanent, undilutable share of the upside.

The non-dilutability provision compounds this issue significantly. In conventional project finance, equity stakes are subject to dilution as new capital rounds are completed. A non-dilutable state stake means that every future fundraising event reduces only the private investor's proportional interest, never ENM's. For projects requiring multiple capital injections across long development timelines, typical of large-scale graphite or heavy mineral sands operations, this dynamic materially compresses the effective economics available to private capital.

Comparing Mozambique's structure against peer jurisdictions reveals where it sits on the regional risk spectrum:

| Country | State Equity Requirement | Free-Carry? | Capital Contribution | Dilutable? |

|---|---|---|---|---|

| Mozambique (2026) | 15% | Yes | None | No |

| Tanzania | 16% | Yes (partial) | None | Limited |

| Zimbabwe | Up to 51% (sector-specific) | Varies | Varies | Varies |

| Botswana | 15 to 25% (negotiated) | No | Yes | Yes |

| South Africa | 26 to 30% (BEE-linked) | No | Partially | Yes |

| DRC | 10% state plus 5% free | Partial | Partial | Yes |

The contrast with Botswana is particularly instructive. Botswana's model requires state capital contributions and allows for dilutability, meaning the government shares both the upside and the risk. Mozambique's 2026 framework offers the state upside with none of the downside, an arrangement that fundamentally distorts the risk-reward equation for foreign capital.

Export Restrictions and the Infrastructure Gap

The mandatory state equity provision is only one of two major structural risks embedded in the 2026 amendments. The second is the default prohibition on exporting unprocessed or semi-processed minerals without obtaining ministerial approval contingent on a credible domestic processing transition plan.

In principle, the push for in-country value addition is a well-established and broadly supported development objective across Southern and East Africa. Processing minerals domestically before export generates employment, develops industrial capacity, and captures a greater share of commodity value chains for the host country. The Mozambique Chamber of Mines, through its vice-president Geert Kolk, publicly stated at the Victoria Falls mining conference in June 2026 that the chamber supports greater in-country value addition as a legitimate regional trend.

The problem, however, is structural rather than philosophical. Industry representatives have consistently identified reliable electricity supply, access to adequate water resources, and functional port and rail logistics as the minimum enabling conditions for domestic mineral processing to be commercially viable at scale. Mozambique's current infrastructure position creates a meaningful gap between the policy's ambition and its operational feasibility.

Electricity access in Mozambique remains uneven, with significant capacity constraints outside major urban corridors. Energy-intensive processing operations, including the spherical graphite purification steps required to produce battery-grade material, demand consistent high-voltage power at competitive tariffs. Without this infrastructure foundation, an export approval conditional on demonstrable processing capability creates a catch-22 situation: investors cannot build processing plants without power, but cannot export raw ore without building processing plants.

The sector-by-sector risk exposure under the export restriction framework breaks down as follows:

| Mineral Sector | Current Export Profile | Processing Feasibility | Risk Rating |

|---|---|---|---|

| Graphite | Primary export commodity | High capital intensity; limited domestic demand | High |

| Rubies and Gemstones | Cut and polished internationally | Partially feasible with targeted investment | Medium |

| Coal | Historically bulk exported | Low value-add incentive for processing | High |

| Heavy Mineral Sands | Typically exported raw | Smelting infrastructure required | Very High |

Mozambique's Strategic Mineral Endowment: What Is Actually at Stake

The regulatory debate surrounding Mozambique mining law foreign investment carries disproportionate global significance because of the country's remarkable mineral endowment relative to its size. In addition, the critical minerals demand driven by the global energy transition makes these assets increasingly strategic for consuming nations worldwide.

Mozambique is recognised as one of the world's leading graphite-producing nations. The Balama graphite operation, owned by Syrah Resources, is among the largest graphite mines on the planet by reserve base and has positioned Mozambique as a critical node in the lithium-ion battery supply chain. Graphite serves as the anode material in every lithium-ion battery currently in commercial production, and natural graphite from operations like Balama is a foundational input for the electric vehicle transition.

Beyond graphite, Mozambique hosts the Montepuez ruby mine, operated by Gemfields as a joint venture and widely considered one of the world's largest known ruby deposits by resource scale. The country also carries the legacy of significant coal sector investment, with both Rio Tinto and Brazil's Vale having held major Mozambican coal positions before making strategic exits following project difficulties.

Emerging sectors including heavy mineral sands and liquefied natural gas add further dimensions to the country's resource profile. It is precisely this endowment quality that makes the 2026 legislative framework so consequential. The assets are genuinely world-class. The question is whether the new ownership and export architecture will attract the capital needed to develop them or redirect that capital to competing jurisdictions.

The Compounding Risk of Policy Trajectory Uncertainty

One of the least-discussed but most materially significant risks embedded in the 2026 amendments is not what the law currently requires, but what parliamentary commentary suggests it may require in the future. Statements made during the legislative debate indicated that the 15% free-carry floor is not necessarily a fixed ceiling and could be subject to upward revision in subsequent legislative cycles.

For investors conducting long-horizon capital allocation decisions, this trajectory uncertainty functions as a risk multiplier. A project modelled under a 15% free-carry assumption delivers meaningfully different IRR and NPV outcomes than one modelled under 20% or 25%. When the legislative framework contains language or political signals suggesting escalation is possible, sophisticated investors will apply a probability-weighted adjustment to their base-case return calculations. This effectively raises the required return threshold for new Mozambican project commitments.

Investor Framework Note: Investors evaluating Mozambique exposures should stress-test project economics not only against the current 15% free-carry structure but also against upside scenarios of 20% to 25% state equity. Where project returns become marginal at these higher thresholds, capital reallocation to jurisdictions with more predictable policy frameworks becomes the rational outcome.

The next major ASX story will hit our subscribers first

What the Stakeholder Debate Reveals About the Underlying Tension

The Mozambique Chamber of Mines' position, articulated by Geert Kolk at the Victoria Falls conference, draws a careful distinction between supporting in-country value addition as a policy objective and endorsing the specific structural mechanism chosen to implement it. The chamber's concern is that mandatory, non-contributory state equity will not make Mozambique more attractive as a destination for foreign mining capital, and that this outcome runs counter to the country's own development interests.

The Mozambican government, for its part, frames the ENM structure and mandatory state participation as tools for strengthening sovereign management of strategic national resources. This rationale reflects a broader and increasingly mainstream view across resource-rich developing nations that the historical terms of foreign mining investment failed to deliver adequate domestic benefit capture. Consequently, the mining geopolitical landscape across the continent is shifting in ways that demand investor attention.

Neither position is without merit. The tension is real, and it is not unique to Mozambique. The fundamental challenge for any resource-rich developing economy is that foreign capital, technology, and technical expertise remain essential to converting geological endowment into economic output, while the domestic political imperative increasingly demands that a larger share of that output stays within national borders.

The design quality of the legislative mechanism chosen to navigate this tension determines whether both objectives can be partially achieved or whether one is sacrificed entirely. Industry analysts at mining.com have noted that the new ownership rules could actively deter foreign investment, a concern echoed across multiple industry bodies evaluating the framework's long-term consequences.

Key Variables Investors Must Monitor

For investors with existing or prospective Mozambican mining exposures, the following variables represent the most critical monitoring points as the 2026 framework moves from legislation to implementation:

- The governance structure and operational transparency of ENM as it establishes itself as the state equity vehicle

- Ministerial approval processing timelines and criteria for export exemptions under the processing conditionality framework

- Whether infrastructure investment commitments accompany processing mandates in practice or remain aspirational

- The applicability and robustness of bilateral investment treaty protections for both existing project holders and new entrants

- Legislative and parliamentary signals regarding whether the 15% free-carry floor will be revised upward in future reviews

- The extent to which state-backed investors or development finance institutions, rather than commercial capital, move to fill any investment gap created by the new framework

Risk Summary for Capital Allocation Decisions

| Risk Category | Severity | Mitigation Pathway |

|---|---|---|

| State equity reducing investor returns | High | BIT review and IRR stress-testing at 15% to 25% state stake scenarios |

| Export restriction compliance uncertainty | High | Early ministerial engagement and processing feasibility studies |

| Policy trajectory risk (15% may rise) | Medium-High | Contractual stabilisation clauses in mining agreements |

| Local content compliance complexity | Medium | Early local partnership structuring before licensing |

| Infrastructure gap for processing mandates | High | Government infrastructure commitment as investment precondition |

| Construction mineral sector exclusion | High (sector-specific) | Capital reallocation to other eligible mineral categories |

The Broader Continental Context

Mozambique's legislative direction is not occurring in isolation. Across Africa, the acceleration of the global energy transition has emboldened resource-rich nations to reassess the terms under which foreign capital accesses their mineral wealth. As graphite, lithium, cobalt, and rare earths move from industrial inputs to strategic geopolitical assets, governments that hold these resources are increasingly unwilling to accept the historical royalty-and-tax model as the primary mechanism of value capture.

The dynamics shaping critical minerals trade globally are also influencing how African governments position their regulatory frameworks relative to major consuming nations, including those in Asia and Europe. The rise of Chinese state-sponsored investment models in Africa has also reshaped government expectations. Chinese-backed projects have often incorporated infrastructure-for-resources frameworks, technology transfer commitments, and employment targets that purely commercial Western capital has been reluctant to match.

African governments observing these comparisons have recalibrated their expectations of what foreign mining investment should deliver domestically. Furthermore, resource export challenges faced by other commodity-exporting nations offer instructive lessons about the long-term trade-offs between restrictive export policies and sustained investment attraction.

The long-term trajectory for Mozambique mining law foreign investment will depend heavily on whether the ENM framework, export restrictions, and local content mandates attract a new investor profile, potentially including development finance institutions, sovereign wealth funds, or state-backed entities from resource-consuming nations. Assessments by UNCTAD's investment policy monitor confirm that the revised regime reduces incentives while increasing government monitoring, a combination that will test investor appetite in the years ahead. The answer will not emerge from the legislation itself. It will emerge from the investment decisions made, or not made, in the years ahead.

Disclaimer: This article is intended for informational purposes only and does not constitute financial advice. All forward-looking statements, modelled scenarios, and projections involve inherent uncertainty and should not be relied upon as the basis for investment decisions. Readers should conduct independent due diligence before making any capital allocation decisions related to Mozambican mining assets or the broader African mining sector.

Ready to Identify the Next Major Mineral Discovery Before the Market Does?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, cutting through complex data to surface actionable investment opportunities the moment they are announced — explore Discovery Alert's discoveries page to understand why major finds can generate extraordinary returns, and begin your 14-day free trial today to position yourself ahead of the broader market.