June 19, 2026

Resource Nationalism Is Reshaping Africa's Mining Investment Map

A quiet but consequential transformation is underway across Sub-Saharan Africa. Over the past decade, governments from Lusaka to Harare have progressively reasserted control over their mineral endowments, moving away from the liberalised ownership frameworks that attracted foreign capital throughout the 1990s and 2000s. Mozambique mine ownership rules and foreign investment considerations are being fundamentally reshaped by the 2026 mining law overhaul, which introduces mandatory state equity participation and sweeping export restrictions. These changes, furthermore, alter the economics of foreign mining investment at a structural level.

Understanding what these changes actually mean, how they compare to regional peers, and what they imply for the global critical minerals and energy security supply chain requires more than a surface reading of the legislation. The real story lies in the intersection of sovereign resource strategy, EV-battery supply dynamics, and the infrastructure realities that ultimately determine whether policy intent translates into commercial outcomes.

When big ASX news breaks, our subscribers know first

The Architecture of Mozambique's 2026 Mining Law Reform

What the New Rules Actually Require

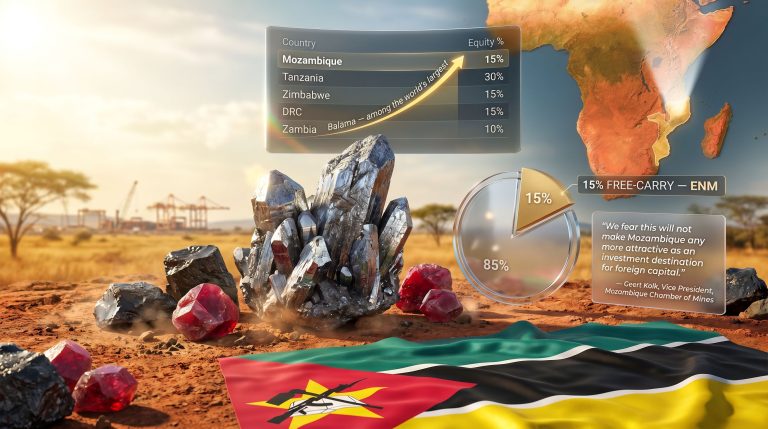

Mozambique's amended mining legislation operates across two distinct but connected regulatory layers. The first governs general ownership and participation eligibility, while the second introduces mandatory state equity participation through the national mining company, Empresa Nacional de Minas (ENM). According to Mozambique's mining law framework, these layers together represent a significant departure from prior regulatory norms.

Foreign investors are not excluded from the sector, but they must satisfy a gateway condition: local incorporation within Mozambique is required before a mining licence can be obtained. Beyond this threshold, the most consequential new obligation is the mandatory 15% free-carried, non-dilutable state equity stake that ENM holds in every new mining venture.

| Regulatory Layer | Pre-2026 Position | 2026 Reform Position |

|---|---|---|

| General Foreign Ownership | Permitted with local incorporation | Still permitted with local incorporation |

| State Equity Participation | Not mandated | Minimum 15% free-carry stake for ENM |

| Export of Unprocessed Minerals | Generally permitted | Banned unless ministerial approval granted |

| Local Content Obligations | Limited requirements | Mandatory; preference for Mozambican-partnered suppliers |

| Artisanal and Small-Scale Mining | Reserved for nationals | Unchanged; nationals only |

The Free-Carry Mechanism and Its Financial Implications

The term free-carry refers to an equity arrangement in which the state receives an ownership stake in a mining project without contributing capital to its development, construction, or ongoing operational costs. In practical terms, this means a foreign investor financing a project from feasibility through to production is simultaneously funding a 15% ownership interest held by ENM, without receiving proportionate capital recovery from that partner.

The financial impact is not trivial. For return-on-investment modelling, a non-dilutable 15% free-carry stake effectively compresses the investable equity base available to private capital. Internal rate of return (IRR) and net present value (NPV) calculations must be restructured accordingly, with no offsetting capital contribution from the state counterparty.

In capital-intensive projects with long payback periods, this dynamic can meaningfully shift a project from economically marginal to economically unattractive, particularly when layered with other country-risk premiums already embedded in discount rates for Mozambique. Consequently, the broader battery metals investment landscape is adjusting its expectations for Mozambican project returns.

The Export Ban: Policy Rationale Versus Practical Execution

The prohibition on exporting unprocessed or semi-processed minerals unless ministerial approval is secured represents the second major structural shift. The stated logic reflects a broader African industrial policy objective: retaining more of the value-add chain within the country rather than exporting raw commodities at lower unit values.

The Mozambique Chamber of Mines has publicly supported the in-country processing ambition in principle, recognising it as consistent with a regional trend toward greater domestic value capture. However, industry voices have stressed that the processing mandate's commercial viability depends entirely on whether enabling infrastructure is actually in place.

"The commercial viability of in-country mineral processing is fundamentally contingent on reliable access to industrial-grade electricity, water infrastructure, and export logistics. Without meaningful state investment in these enablers, processing mandates risk functioning as structural barriers rather than value-creation mechanisms."

The five conditions investors assess before committing to in-country processing are:

- Grid reliability — mineral processing is energy-intensive; even intermittent power disruptions can render beneficiation plants economically unviable

- Water access — processes such as graphite flotation beneficiation require consistent, high-volume water supply that is not universally available across Mozambique's mining corridors

- Logistics connectivity — proximity to functioning rail networks and deep-water ports determines whether processed output can reach international markets at competitive freight costs

- Skilled labour depth — downstream processing requires a substantially different and more technically complex workforce than primary extraction operations

- Fiscal offset mechanisms — capital-intensive processing infrastructure typically requires accelerated depreciation schedules or other tax incentive structures to generate acceptable investor returns

Why Mozambique's Mineral Endowment Still Commands Global Attention

The Critical Mineral Profile Driving Strategic Interest

Despite the regulatory friction introduced by the 2026 reforms, Mozambique's underlying resource base continues to attract attention from investors and supply chain strategists. The country's critical mineral credentials span several strategically significant commodities:

- Graphite: Mozambique ranks among the world's largest producers of natural flake graphite. The Balama deposit in Cabo Delgado province, operated by Syrah Resources, is one of the largest known graphite reserves globally by contained resource. Natural graphite is a primary input material for battery anodes in lithium-ion cells used in electric vehicles and grid-scale energy storage systems.

- Rubies: The Montepuez deposit in northern Mozambique, operated by Gemfields, is widely recognised as the world's largest ruby mine by production volume. Its output has reshaped global coloured gemstone supply since commercial production began.

- Coal: The Tete Basin holds significant thermal and metallurgical coal resources. Both Rio Tinto and Vale held major positions in this region before divesting, reflecting the complex interplay between commodity cycles, infrastructure challenges, and country risk.

- Emerging battery minerals: The geological characteristics of northern Mozambique are increasingly being assessed for broader battery supply chain relevance beyond graphite, though early-stage exploration activity has been complicated by the security situation in Cabo Delgado.

The EV Supply Chain Dimension

The intersection of Mozambique mine ownership rules and foreign investment takes on a different character when viewed through the lens of the global energy transition. Battery-grade graphite is currently subject to significant supply concentration risk, with China dominating both synthetic graphite production and natural graphite processing capacity.

The global graphite shortage has prompted Western governments and automotive supply chains to actively diversify graphite sourcing away from single-country dependency. In this context, Mozambique's Balama deposit represents one of a small number of non-Chinese natural graphite sources of scale capable of supplying international battery manufacturers.

"As EV adoption targets in the EU, United States, and Asia drive accelerating demand for battery-grade graphite, Mozambique's investment environment directly influences the pace at which its reserves can be integrated into international supply chains. Regulatory friction that slows development timelines compounds supply-side constraints already building in the market."

How Mozambique Compares to Regional Peers on State Participation

The African Resource Nationalism Spectrum

Mozambique's approach to state participation sits within a regional continuum that spans from negotiated case-by-case arrangements to mandatory fixed-percentage requirements. Contextualising the 2026 reform against peer jurisdictions helps investors calibrate relative attractiveness, particularly within today's complex geopolitical mining landscape.

| Country | State Participation Model | Export Restrictions | Local Content Regime |

|---|---|---|---|

| Mozambique (2026) | 15% free-carry, non-dilutable | Yes, ministerial approval required | Mandatory Mozambican partner/supplier preference |

| Tanzania | 16% free-carry + 5% local equity option | Partial restrictions in place | Yes, formalised requirements |

| Zimbabwe | Up to 51% indigenisation in select sectors | Export levies apply to key commodities | Yes, structured requirements |

| Zambia | Negotiated equity, case-by-case | Limited restrictions | Yes, sector-specific |

| Botswana | Negotiated participation, no fixed free-carry | No broad export ban | Moderate, largely voluntary |

| DRC | Variable; state royalty and equity structures | Concentrate export restrictions apply | Yes, increasingly enforced |

Mozambique's 15% free-carry threshold is numerically lower than Tanzania's combined participation structure and considerably lower than Zimbabwe's indigenisation requirements in targeted sectors. However, the non-dilutable characteristic introduces a feature that limits investor flexibility in ways that simple percentage comparisons do not fully capture.

What Non-Dilutability Actually Means for Capital Structure

In most mining financing structures, equity interests are subject to dilution as additional capital rounds occur. A 15% stake held by a passive state entity would, under standard equity mechanics, be diluted progressively as new capital is raised. The non-dilutable provision in Mozambique's framework removes this pathway entirely, ensuring ENM's 15% economic interest remains fixed regardless of how much additional private capital is deployed.

This has meaningful implications for late-stage capital raising, project expansion financing, and any transaction involving secondary equity sale or joint venture restructuring. Furthermore, as Pinsent Masons notes, this mandatory ownership structure marks a significant shift in how the state engages with foreign mining capital.

Navigating Compliance: A Practical Framework for Foreign Investors

What Active and Prospective Investors Need to Assess

For mining companies with existing operations or active exploration programmes in Mozambique, the 2026 reforms generate a structured set of compliance and strategic planning obligations. In addition, investors should work through the following assessment framework before making capital allocation decisions:

- Confirm whether existing licences are grandfathered under prior terms or subject to the new state participation mandate

- Recalculate project IRR and NPV with a 15% non-dilutable free-carry stake factored into the equity model

- Assess the export strategy against the unprocessed mineral ban, and determine whether the ministerial approval pathway is clearly defined and practically accessible

- Map local content obligations, identifying Mozambican-incorporated suppliers and potential joint venture partners who satisfy preference requirements

- Define ENM's expected operational involvement and governance rights under the mandatory participation framework

- Confirm whether artisanal or small-scale mining classifications apply, given the nationals-only restriction in this sub-sector

- Conduct infrastructure dependency assessment covering power grid reliability, water access, and logistics connectivity for any processing obligations

The next major ASX story will hit our subscribers first

The Bigger Picture: Sovereign Ambition Meets Investment Reality

Why This Reform Pattern Will Continue Across Africa

The structural forces driving Mozambique's 2026 reform are not unique to Mozambique. Across the continent, governments are responding to a combination of rising commodity prices, growing public awareness of resource extraction economics, and a global rebalancing of supply chain leverage. These dynamics have elevated the strategic value of African mineral endowments considerably.

The African Continental Free Trade Area (AfCFTA) framework, while primarily focused on trade liberalisation, indirectly reinforces the in-country processing argument by expanding the potential domestic market for semi-processed and processed mineral products. Whether AfCFTA's structural incentives are sufficient to offset the infrastructure deficits that constrain processing viability remains an open question.

What is clear is that the era of relatively unconstrained foreign private ownership of African mineral assets is narrowing. Consequently, a coherent critical minerals strategy has become essential for any investor seeking to navigate these evolving frameworks successfully. The strategic question for international mining capital is not whether resource nationalism will continue, but how to structure commercially viable participation within frameworks that progressively incorporate mandatory state partnership.

"Mozambique's 2026 mining reforms do not eliminate the foreign investment opportunity, but they fundamentally reprice the terms of entry. Investors who model these changes accurately, build genuine local partnerships, and engage constructively with ENM's role are better positioned to extract long-term value from one of Sub-Saharan Africa's most strategically significant critical mineral jurisdictions."

This article is for informational purposes only and does not constitute financial, legal, or investment advice. Mining investment involves material risks including sovereign risk, commodity price volatility, operational uncertainty, and regulatory change. Readers should conduct independent due diligence and seek professional advice before making any investment decisions.

Want to Stay Ahead of Significant ASX Mineral Discoveries in Real Time?

As resource nationalism reshapes investment economics across Africa and critical mineral supply chains face mounting structural pressure, identifying high-potential opportunities early has never been more valuable. Discovery Alert's proprietary Discovery IQ model delivers instant ASX mineral discovery alerts, converting complex geological and commodity data into actionable insights — and you can explore why historic discoveries have generated extraordinary returns before beginning your 14-day free trial to secure a genuine market-leading edge.