June 7, 2026

The Architecture of Rare Earth Dependency: Why One Mine Defines a Nation's Industrial Future

For most of the past three decades, the United States systematically exited the rare earth business. Processing facilities closed. Mining operations were abandoned. Refining expertise migrated offshore. What remained was an almost complete dependence on Chinese supply chains for a category of materials sitting at the intersection of clean energy, consumer electronics, and national defence. The story of how America found itself in this position, and the role a single California mine is playing in reversing it, tells us something profound about the cost of industrial short-termism and the difficulty of rebuilding what was lost.

Understanding MP Materials rare earth sales requires more than reading a quarterly earnings report. It requires understanding a structural pivot that is reshaping how the United States thinks about supply chain sovereignty, critical mineral access, and the true cost of strategic dependency.

When big ASX news breaks, our subscribers know first

The Peculiar Economics of the Only Mine That Matters

Mountain Pass, California, holds a distinction that is simultaneously remarkable and concerning: it is the only active rare earth mine in North America. That a continent of this size, with this level of industrial complexity, depends on a single extraction point for an entire category of strategic materials reflects decades of market distortion rather than geological scarcity.

Rare earths are not rare in the geochemical sense. The group of 17 metals, which includes neodymium, praseodymium, dysprosium, and terbium among others, are found in reasonable concentrations across many parts of the world. What makes them strategically scarce is the infrastructure required to separate, refine, and process them into usable forms. Furthermore, that infrastructure has been concentrated in China through a combination of low-cost labour, state subsidy, and deliberate industrial policy spanning four decades.

The commercial reality is straightforward: rare earth magnets convert electrical energy into mechanical motion. Every electric vehicle motor, every wind turbine generator, every missile guidance system, and every hard disk drive depends on permanent magnets manufactured from these materials. Without a domestic supply chain, every one of these applications carries embedded geopolitical risk.

MP Materials' transition from a concentrate exporter into a vertically integrated mining-to-magnet producer represents perhaps the most consequential industrial supply chain pivot in recent U.S. history. The company's rare earth sales trajectory is therefore not merely a financial story. It is a live measurement of whether domestic critical mineral ambitions are translating into operational reality.

Reading the Q1 2026 Numbers With Appropriate Nuance

The headline figures from MP Materials' first quarter 2026 results were genuinely impressive. Revenue reached $90.6 million, representing a 49% year-over-year increase that significantly outpaced analyst consensus of $76.5 million by approximately $14.1 million, or roughly 18.4%. Adjusted earnings came in at $0.03 per share, beating expectations of breakeven. The net loss narrowed dramatically from $22.7 million in the year-ago quarter to $7.9 million, a 71% reduction in losses that signals genuine operational progress.

| Metric | Q1 2026 Actual | Analyst Estimate | Variance |

|---|---|---|---|

| Revenue | $90.6M | $76.5M | +$14.1M (+18.4%) |

| Adjusted EPS | $0.03 | $0.00 (breakeven) | Beat by $0.03 |

| Net Loss | -$7.9M (-$0.04/share) | N/A | Improved YoY |

| Prior Year Net Loss | -$22.7M (-$0.14/share) | N/A | -71% improvement |

However, two numbers embedded in these results require careful interpretation before investors draw conclusions about underlying profitability.

First, the company received $42.3 million in price protection income from the U.S. government during the quarter. This figure represents approximately 46.7% of total reported revenue. The mechanism functions as a price floor arrangement, ensuring that MP Materials remains economically viable when spot market prices fall below a predetermined threshold.

When prices exceed that floor, the company retains full market upside. This asymmetric structure is commercially rational and strategically designed to maintain domestic production capacity regardless of short-term commodity price cycles. However, it does mean that reported revenue quality carries a meaningful distinction between government-supported income and pure commercial demand. Consequently, investors should model these components separately when evaluating long-term business quality.

Second, operating costs surged 64% year-over-year to $157 million, producing a cost-to-revenue ratio that significantly exceeds 100%. This is not unusual for companies in the commissioning and ramp-up phase of major industrial facilities, and the primary driver was spending associated with starting up the magnetics division. Cost structures of this kind normalise as throughput increases and fixed overhead spreads across larger production volumes. Nevertheless, the trajectory of operating cost reduction will be the critical variable determining when the business achieves sustainable positive cash flow from operations.

What the Apple Prepayment Signals About Commercial Validation

Among the most strategically significant disclosures in Q1 2026 was the $32 million prepayment received from Apple as part of a magnet supply agreement signed the previous July. This single transaction carries implications beyond its dollar value.

A prepayment of this scale from one of the world's most sophisticated supply chain operators represents a deliberate commitment to securing non-Chinese rare earth magnet supply. Apple does not make procurement decisions lightly, and the willingness to prepay for future deliveries signals genuine confidence in MP Materials' manufacturing capability and long-term viability. In addition, it provides working capital to fund ongoing expansion during a period when operating costs substantially exceed revenue from commercial sales alone.

The prepayment also illustrates a broader strategic shift in how major technology companies are approaching critical mineral supply chain risk. Following years of documented concentration risk in Chinese rare earth processing, companies with the scale and sophistication to act are actively diversifying. MP Materials is the primary beneficiary of this reorientation in North America.

The Supply Chain Architecture: From California Earth to Texas Magnets

The physical structure of MP Materials' rare earth production involves three geographically distinct but operationally linked stages.

Stage 1 begins at Mountain Pass in California's Mojave Desert, where ore containing neodymium, praseodymium, and other critical elements is extracted and concentrated. This is the foundation of everything downstream, and its status as the continent's only active rare earth mining operation means any operational disruption carries systemic implications.

Stage 2 involves separation and processing in California, converting ore concentrate into separated rare earth oxides and metals. This is technically the most demanding stage of the supply chain and historically the one most dependent on Chinese infrastructure. MP Materials' ability to perform this process domestically represents a significant competitive and strategic capability.

Stage 3 is magnet manufacturing at the Fort Worth, Texas facility, which the company has branded the Independence plant. This is where separated rare earth materials are converted into finished neodymium-iron-boron (NdFeB) permanent magnets for sale to automotive manufacturers, defence contractors, technology companies, and industrial customers.

The Technical Significance of NdFeB Magnets

NdFeB permanent magnets occupy a specific and largely irreplaceable position in modern industrial technology. Their energy density, which measures how much magnetic force can be generated per unit of mass, is substantially higher than alternative magnet types. This makes them the only commercially viable option for applications where weight and size constraints are critical, including EV traction motors, where performance specifications demand maximum torque in minimum space.

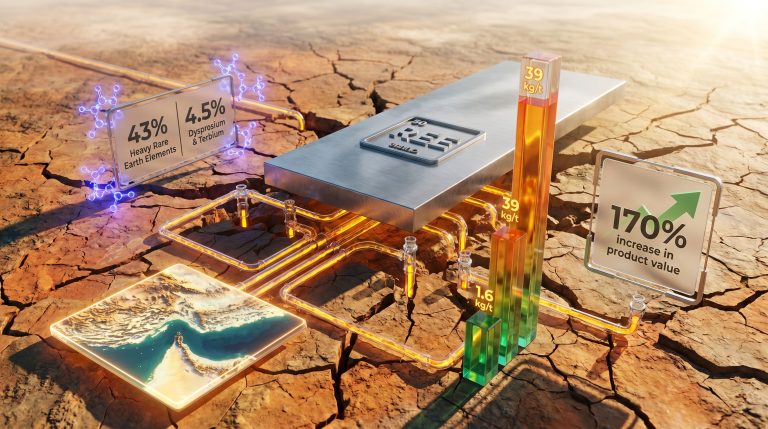

An important technical dimension often overlooked in mainstream coverage involves the distinction between light and heavy rare earth elements. Neodymium and praseodymium are light rare earths and form the primary input for basic NdFeB magnets. However, these magnets experience significant performance degradation at elevated temperatures, a problem encountered in high-performance EV motors, aerospace applications, and certain defence systems.

To address this, small quantities of heavy rare earths, specifically dysprosium and terbium, are added to stabilise magnet performance at high temperatures. This distinction matters commercially and geopolitically because China's dominance is even more pronounced in heavy rare earth processing than in light rare earth production. MP Materials is in the process of commissioning a heavy rare earth processing line, which, when operational, would further reduce the gap in domestic supply chain capability.

The Competitive Landscape and Emerging Challengers

MP Materials' near-monopoly position in North American rare earth mining will not remain unchallenged indefinitely. The same strategic imperative driving government support for MP's operations is also creating conditions for new entrants to emerge elsewhere.

The Shiloh exploration district in Georgia has attracted significant attention following claims of a potentially substantial heavy rare earth discovery. Rare Earths Americas, which listed on the NYSE in May 2026, is positioning this deposit as a potential contributor to U.S. heavy rare earth supply. Whether the deposit ultimately delivers at commercial scale remains to be demonstrated through detailed geological work and feasibility analysis.

Exploration-stage announcements and economic production at scale are separated by years of technical, environmental, and financial work. Nevertheless, the emergence of this narrative illustrates that capital is beginning to flow toward the rare earth sector in ways that were not commercially viable before the current policy and price environment.

Investors should approach early-stage rare earth exploration with appropriate caution. The history of the sector includes numerous projects that performed well at the resource definition stage but faced insurmountable technical or economic obstacles at the processing and refining stage, where rare earth extraction chemistry is particularly complex.

Understanding the Government-Commercial Funding Architecture

The financial structure underpinning MP Materials' operations involves a layered combination of government support mechanisms and commercial customer relationships that collectively reduce the risk profile of a capital-intensive, long-duration industrial build-out.

On the government side, the price protection income mechanism provides revenue floor protection, while a Pentagon commitment provides capital support for expanding domestic magnet supply capacity. On the commercial side, long-term supply agreements with major technology and automotive customers provide volume certainty that is essential for justifying the scale of investment in processing and manufacturing infrastructure.

This blended model, combining public risk mitigation with private commercial validation, reflects a mature understanding of what is required to build strategic industrial capacity in sectors where market forces alone have historically been insufficient to compete with state-supported foreign producers. It may also represent a template applicable to other critical mineral supply chains including lithium, cobalt, and graphite, where similar dependency structures exist and similar rebuilding challenges must be addressed.

| Customer/Source | Structure | Q1 2026 Impact |

|---|---|---|

| U.S. Government (price protection) | Price floor mechanism | $42.3M income |

| Apple | Magnet supply agreement + prepayment | $32.0M prepayment received |

| Pentagon | Capacity support commitment | Long-term structural support |

| General Motors | Ongoing magnet supply | Commercial volume validation |

The next major ASX story will hit our subscribers first

Risk Factors That Serious Investors Cannot Ignore

The MP Materials rare earth sales growth story carries genuine strategic weight. However, several risk dimensions warrant clear articulation.

Revenue quality concentration is the most immediate concern. With approximately 47% of Q1 2026 revenue derived from government price protection income, any policy discontinuity or renegotiation of support terms would materially affect reported financials. This dependency is structurally justified during the scale-up phase but creates earnings volatility risk tied to political and policy factors rather than purely operational performance.

Cost trajectory remains the key operational variable. Operating costs of $157 million against revenue of $90.6 million means the business is currently burning cash on operations. The investment thesis depends critically on cost normalisation as the magnetics division scales toward target throughput. If ramp-up extends longer than anticipated, or if technical commissioning challenges persist, the path to positive operating cash flow extends accordingly.

Single-asset concentration risk at the mining stage is inherent in a supply chain that depends on a single North American mine. Any significant operational disruption at Mountain Pass, whether from geological, regulatory, or environmental factors, would immediately affect the entire downstream production chain.

Heavy rare earth dependency remains partially unresolved until the company's heavy rare earth processing line reaches commercial production, expected in mid-2026. Until that point, high-performance magnets requiring dysprosium or terbium additions depend on externally sourced inputs, maintaining a residual supply chain vulnerability.

This article is intended for informational purposes only and does not constitute financial or investment advice. Projections, timelines, and forward-looking statements involve inherent uncertainty and should not be relied upon as predictive of future outcomes. Investors should conduct independent due diligence and consult qualified financial advisors before making investment decisions.

Want to Stay Ahead of the Next Major Mineral Discovery on the ASX?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries across more than 30 commodities, instantly translating complex geological data into actionable investment insights — begin your 14-day free trial today and explore the historic returns major discoveries have delivered to understand what early positioning can mean for your portfolio.