July 16, 2026

When Supply Chains Become Battlegrounds: Myanmar's Rare Earth Crisis Explained

The global clean energy transition rests on a remarkably fragile mineral foundation. Decades of industrial policy have quietly concentrated the production of heavy rare earth elements (HREEs) into two geographic zones: southern China and a cluster of mining belts in northern Myanmar. When one of those zones becomes an active war theatre, the consequences ripple far beyond any regional conflict. That is precisely the situation unfolding across Kachin, Chin, and Karen states, where Myanmar military rare earth area offensives are reshaping both battlefield dynamics and global rare earth supply chains simultaneously.

When big ASX news breaks, our subscribers know first

Understanding Heavy Rare Earths and Why Northern Myanmar Is Irreplaceable

Not all rare earth elements carry the same strategic weight. The rare earth family is broadly divided into light rare earth elements (LREEs) and heavy rare earth elements (HREEs), and the distinction matters enormously for technology supply chains.

LREEs such as cerium and lanthanum are relatively abundant and used in applications like catalysts and glass polishing. HREEs, by contrast, are genuinely scarce and industrially critical. Key HREEs include:

- Dysprosium and terbium: used to stabilise neodymium-iron-boron (NdFeB) permanent magnets at high operating temperatures, a non-negotiable requirement for EV traction motors

- Holmium and erbium: applied in specialised magnets, fibre optic systems, and defence-grade components

- Gadolinium: used in medical imaging, nuclear reactor shielding, and high-performance alloys

Northern Myanmar's Kachin State hosts ionic clay deposits that are unusually rich in these heavy elements. Ionic adsorption clay deposits, the geological formation responsible for most HREE production globally, form when rare earth-bearing parent rock weathers over millions of years in humid subtropical conditions. The resulting clay matrix traps rare earth ions in exchangeable surface positions, allowing relatively low-cost in-situ leaching extraction methods to recover them.

This geological reality is poorly understood outside specialist circles: the specific climatic and lithological conditions required to form high-grade ionic clay HREE deposits are extraordinarily rare globally, which is why northern Myanmar cannot be substituted by simply opening a mine elsewhere.

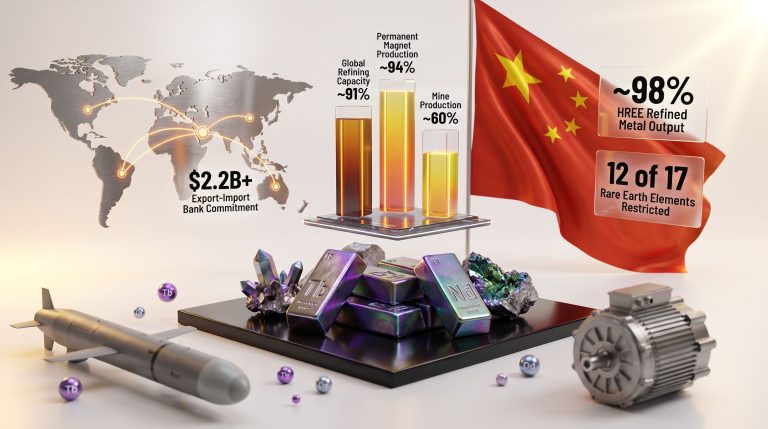

Northern Myanmar's mining belts account for approximately 50% of global heavy rare earth supply, a concentration that creates a structural single-point-of-failure risk for every industry dependent on high-performance permanent magnets.

How Does Downstream Industrial Exposure Vary Across Key Sectors?

| Sector | Primary HREE Dependency | Supply Disruption Exposure |

|---|---|---|

| Electric Vehicle Manufacturing | Dysprosium, terbium (NdFeB magnets) | Very High |

| Offshore Wind Energy | Neodymium-dysprosium magnet assemblies | Very High |

| Defence and Aerospace | Heavy rare earth alloys, guidance systems | High |

| Industrial Robotics | Permanent magnet motors | High |

| Consumer Electronics | Multiple HREE applications | Moderate |

The October 2024 Turning Point: KIA Seizure of the Mining Belts

The current crisis did not emerge overnight. Myanmar's February 2021 military coup, which removed the civilian government led by Aung San Suu Kyi, triggered a nationwide resistance movement that progressively eroded military territorial control across multiple regions between 2021 and 2024.

The inflection point for global supply chains arrived in October 2024, when the Kachin Independence Army (KIA) seized control of the primary rare earth mining belts in Kachin State, particularly around the Chipwi and Pangwa township areas. This transfer of control effectively suspended the integrated logistics chain connecting Myanmar's HREE extraction sites to Chinese processing facilities across the border.

What makes this disruption structurally significant rather than merely temporary is the processing dimension. Myanmar-origin HREEs are predominantly exported in semi-processed form to southern China, where separation and refining infrastructure has been built up over decades. Disrupting the extraction stage creates upstream pressure on Chinese rare earth processing capacity, which in turn affects the downstream availability of separated oxide products used by magnet manufacturers in China, Japan, and South Korea.

New Military Leadership and the Escalating Offensive Campaign

Myanmar's military underwent a command transition in March 2026, with Ye Win Oo assuming the role of military chief from his predecessor. Regional analysts have characterised this transition as a strategic recalibration rather than a continuity appointment. The new leadership's operational priorities appear oriented toward recovering border corridors and resource-rich zones that were lost during the post-coup resistance campaigns.

A 100-day peace dialogue proposal put forward by former junta leader Min Aung Hlaing, carrying a deadline of July 31, was rejected by virtually all major ethnic armed groups almost immediately upon announcement. The Karen National Union's response was particularly definitive: the group cited an unbroken history of military pledge violations and stated that no foundation for trust exists.

The KIA similarly rejected the overture and publicly confirmed its reinforced defensive preparations around the Chipwi and Pangwa mining zones. The simultaneous pursuit of peace talks and intensified military offensives reflects a pattern of strategic signalling rather than genuine negotiation, a dynamic that analysts covering Southeast Asian conflicts have observed across multiple prior cycles of engagement.

Three Active Fronts: Kachin, Chin, and Karen States

Kachin State: The Rare Earth Heartland

The military's Kachin campaign carries the greatest global economic consequence. Objectives include recapturing the Chipwi and Pangwa mining belts and restoring the Mandalay to Myitkyina arterial corridor, which functions as both a military supply line and a civilian trade route connecting central Myanmar to the Chinese border region. State media has reported early claims of progress along this corridor, though independent verification remains constrained by restricted media access.

The KIA has explicitly confirmed its defensive posture in Chipwi and Pangwa, signalling that any military recapture attempt will face organised resistance rather than a tactical withdrawal.

Chin State: The India Border Logistics Corridor

On Myanmar's western front, the military has deployed heavy aerial bombardment to recover Falam and Tonzang towns in Chin State, border-adjacent areas that function as logistics conduits supporting opposition supply lines connecting to India. Chin National Front fighters have conducted strategic retreats from both locations under sustained air pressure.

A particularly under-discussed dimension of the Chin State campaign involves the fuel supply chain sustaining military air operations. Previous investigative reporting established that illicit jet fuel deliveries from Iran were instrumental in enabling the military's aerial bombing campaign, which struck over 1,000 civilian locations across a fifteen-month period.

As of mid-2026, the military's air operations have not shown meaningful deceleration despite broader disruptions to Iranian energy exports, though civilian populations in Myanmar are experiencing significant fuel shortages as a knock-on effect.

Karen State: The Thailand Trade Corridor

In Karen State on the Thai border, the military is contesting control of the Myawaddy to Kawkareik highway, one of Myanmar's most economically significant bilateral trade arteries. The Karen National Union's 2024 push into Myawaddy was a strategically consequential move that the military has been attempting to reverse through ongoing operations. No clear territorial resolution has emerged from this front.

Supply Chain Risk Matrix: Assessing the Kachin State Situation

| Risk Factor | Current Status | Global Impact Level |

|---|---|---|

| Heavy rare earth extraction | Severely disrupted since October 2024 | Critical |

| China border trade access | Contested | High |

| Mining workforce displacement | Ongoing | Moderate to High |

| Export logistics continuity | Interrupted | Critical |

| Processing feed to Chinese refiners | Reduced | High |

The next major ASX story will hit our subscribers first

The China Dimension: Processing Dependency and Geopolitical Complexity

China's role in this equation extends beyond geographic proximity. The majority of Myanmar-origin HREEs are transported across the border in crude or partially processed form before entering China's rare earth separation infrastructure. This means that sustained disruption in Kachin State does not simply reduce Myanmar's export revenues: it reduces the feedstock available to Chinese separation plants that supply the global magnet manufacturing industry.

Furthermore, China's rare earth restrictions have already intensified pressure on downstream manufacturers, and the Myanmar supply disruption compounds these structural vulnerabilities considerably. How Beijing weighs these competing interests — stable feedstock supply versus supply chain leverage — represents one of the more consequential and least-discussed variables in the Myanmar conflict's international dimensions.

Why Alternative Supply Cannot Fill the Gap

A common misconception is that rising rare earth exploration activity in Australia, Canada, or Africa can serve as a near-term substitute for Myanmar-origin HREEs. The timeline reality is considerably less reassuring:

- Discovery to production for a greenfield ionic clay or hard rock HREE project typically spans 10 to 15 years under favourable permitting conditions

- Processing infrastructure for HREE separation does not exist at commercial scale outside of China and a small number of emerging facilities globally

- Grade thresholds matter: not all rare earth deposits carry sufficient HREE fractions to substitute for Myanmar-type material, which is specifically valued for its dysprosium and terbium content

- Capital intensity: HREE processing facilities require billions in specialised capital that has historically been difficult to attract given price volatility

The structural lesson for critical mineral supply chains is that geographic concentration in conflict-affected jurisdictions creates systemic risk that market mechanisms alone cannot resolve. Policy-level intervention, long-term offtake frameworks, and sustained capital commitment are prerequisites for meaningful supply diversification.

Three Scenarios for the Conflict's Trajectory

Scenario 1: Protracted Stalemate (Most Probable Near-Term)

Neither party achieves decisive control. Rare earth supply from Kachin State remains partially disrupted for an extended period, sustaining upward pricing pressure on dysprosium and terbium oxides. Consequently, terbium demand pressures are likely to intensify further, creating ongoing procurement uncertainty for magnet manufacturers dependent on Myanmar-origin material.

Scenario 2: Military Recapture of Mining Zones (Moderate Probability)

The Myanmar military successfully retakes Chipwi and Pangwa. Mining operations resume under military-aligned administration, restoring supply flows but under conditions of continued conflict risk, international scrutiny, and potential sanctions pressure affecting downstream buyers.

Scenario 3: Negotiated Territorial Arrangement (Low Near-Term Probability)

A ceasefire framework emerges through regional mediation, potentially involving China given its border proximity and commercial interests. Mining zones operate under transitional governance. Supply chain uncertainty reduces materially, though long-term stability would remain contingent on the durability of any political arrangement.

The Clean Energy Transition Paradox

There is a deep structural irony embedded in this situation. The same decade that demands the most aggressive scaling of EV manufacturing, offshore wind deployment, and defence modernisation is the decade in which the primary supply zone for the minerals enabling those technologies has become a contested war zone.

Dysprosium and terbium have no commercially viable substitutes in high-performance NdFeB permanent magnets at present operating temperatures. Magnet designs that reduce or eliminate these elements exist in research contexts but have not achieved production-scale viability for high-temperature EV motor applications. Moreover, critical minerals demand continues to accelerate precisely as Myanmar military rare earth area offensives remove a substantial portion of HREE supply from global markets.

This means that every month of sustained disruption translates directly into tighter supply conditions for components that sit at the core of the energy transition hardware stack. Governments and manufacturers pursuing net-zero commitments face an uncomfortable supply chain reality that energy transition mineral security frameworks have so far been inadequate to address at the policy level.

For a detailed analysis of how conflict is reshaping the rare earth market, the strategic dimensions extend well beyond the immediate battlefield dynamics.

Frequently Asked Questions

What Makes Kachin State's Rare Earth Deposits Geologically Distinctive?

Kachin State hosts ionic adsorption clay deposits, a formation type that concentrates heavy rare earth elements far above average crustal abundance levels. These deposits form only under specific long-term weathering conditions and are globally rare, making them disproportionately significant relative to their physical size.

Why Are Dysprosium and Terbium Specifically So Critical?

Both elements are added to NdFeB magnets to prevent demagnetisation at elevated operating temperatures. Without them, permanent magnets in EV motors and wind turbine generators would lose performance integrity under normal operating conditions. No cost-effective alternative additive currently performs this function at commercial scale.

How Significant Is Myanmar's Share of Global HREE Supply?

Northern Myanmar's mining belts contribute approximately 50% of global heavy rare earth supply, a figure that reflects the geographic rarity of ionic clay HREE deposits and the decades of relatively low-cost artisanal and semi-industrial extraction that developed in the region. However, as recent reporting on militia-assisted mining ventures confirms, the governance structures underpinning this supply have always been fragile.

What Is the Current Status of Peace Negotiations?

As of mid-2026, all major ethnic armed groups including the KIA and KNU have rejected the military's 100-day dialogue proposal. Defensive preparations are being reinforced, and active offensives are ongoing across at least three state-level fronts simultaneously.

How Does This Situation Affect Rare Earth Pricing?

Sustained disruption to Kachin State extraction reduces global HREE supply, creating upward pricing pressure particularly for dysprosium and terbium oxides. Given the absence of near-term substitute supply sources, pricing volatility is likely to persist for as long as Myanmar military rare earth area offensives remain unresolved.

Disclaimer: This article is intended for informational purposes only and does not constitute financial, investment, or commodity trading advice. Forecasts and scenario projections involve inherent uncertainty and should not be relied upon as predictions of future outcomes. Readers should conduct independent research and consult qualified advisers before making investment or procurement decisions.

Want to Track ASX Opportunities Emerging From the Rare Earth Supply Crisis?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts the moment significant rare earth and critical mineral discoveries are announced on the ASX, transforming complex geological data into clear, actionable investment insights. Explore historic discovery returns on Discovery Alert's dedicated discoveries page and begin a 14-day free trial to position ahead of the market as HREE supply disruptions continue to reshape the global minerals landscape.