June 29, 2026

The Race to Rewire the Global Critical Minerals Map

Imagine a scenario where a European electric vehicle manufacturer wakes up one morning to find that the primary supplier of dysprosium, a metal without which its motor magnets cannot function at high temperatures, has restricted export volumes overnight. This is not a hypothetical drawn from thin air. It reflects the structural vulnerability that Western industrial economies have been grappling with as they confront the reality of concentrated rare earth supply chains. The response from the EU, the United States, and Japan has been systematic: identify alternative jurisdictions, formalise supply partnerships, and begin locking in offtake agreements before the most advanced projects reach production.

Within this geopolitical scramble, one southern African country has emerged as a particularly compelling answer to the diversification question. Namibia's combination of geological breadth, political stability, established mining infrastructure, and a government actively courting long-term industrial partners has placed it at the centre of the global conversation around Namibia critical minerals and rare earths.

When big ASX news breaks, our subscribers know first

Why Namibia's Mineral Endowment Is Structurally Different From Any Other African Jurisdiction

Most resource-rich nations offer depth in one or two commodity categories. Namibia is unusual because its geological endowment spans virtually the entire spectrum of the energy transition. From uranium required for nuclear baseload generation, to lithium and graphite feeding battery supply chains, to heavy rare earth elements enabling the permanent magnets inside EV drivetrains and offshore wind turbines, the country's confirmed mineral portfolio is remarkably diverse.

Confirmed reserves and active exploration targets include:

- Uranium, lithium, graphite, and rare earth elements

- Copper, manganese, zinc, and cobalt

- Tantalum, niobium, strontium, tin, and rubidium

Mining already contributes over 10% of Namibia's GDP and represents more than 50% of total national export revenue, figures cited by Minister of Mines and Energy Modestus Amutse at the EU-Namibia Business Forum in Windhoek in May 2026. These are not marginal contributions. They reflect an economy where the extractive sector is foundational, and where the transition from raw material exporter to industrial value-add partner carries transformative economic implications.

The country also benefits from infrastructure advantages that most frontier mineral jurisdictions lack. Established uranium operations at Rössing and Husab represent decades of operational learning in large-scale hard rock extraction. Paladin Resources continues operating the Langer Heinrich uranium mine, cementing Namibia's position as one of Africa's most significant uranium producers. The Tsumeb copper smelter and Tschudi LME-grade cathode production facility demonstrate that downstream processing capability already exists within the country's borders. Port access for export-ready material is not a future aspiration but a present reality.

The Geological Case: What Makes Namibia's Rare Earth Profile Particularly Valuable?

Not all rare earth deposits are created equal. The global rare earth market divides broadly into two categories: light rare earth elements (LREEs), which include neodymium and praseodymium, and heavy rare earth elements (HREEs), which include dysprosium and terbium. The distinction matters enormously from both a commercial and strategic standpoint.

HREEs are significantly scarcer in nature and command substantially higher prices. More critically, they cannot easily be substituted in high-performance applications. Dysprosium is added to neodymium-iron-boron magnets to maintain magnetic performance at elevated operating temperatures, a property essential for EV motors that must perform reliably across a wide thermal range. Terbium serves a similar stabilising function in the most demanding magnet applications.

Without access to these two elements at scale, Western manufacturers of EVs, wind turbines, and advanced defence systems face a hard ceiling on production volumes. Furthermore, the surge in critical minerals demand from the energy transition is making this ceiling increasingly constraining for allied industrial economies.

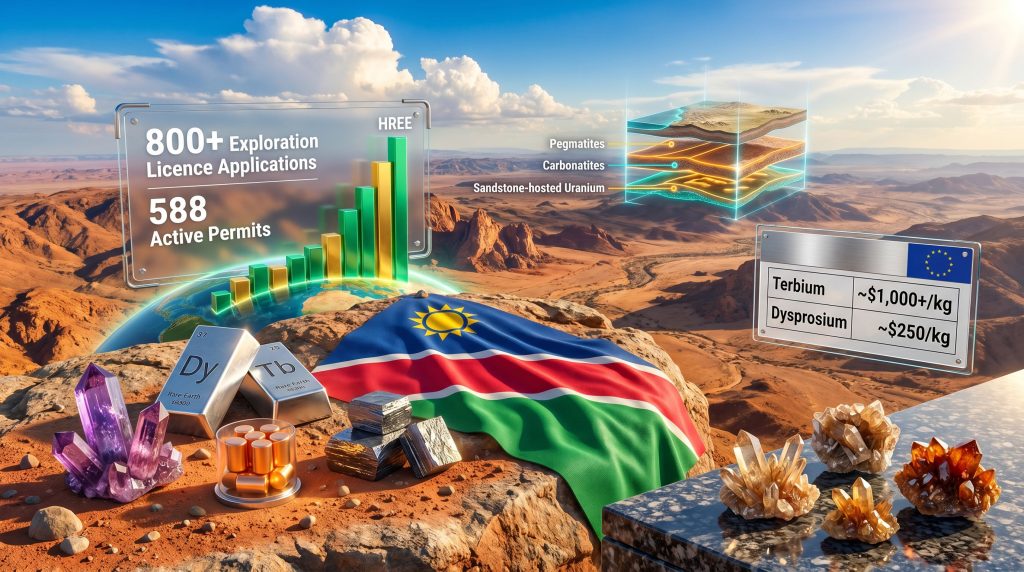

China controls the overwhelming majority of global HREE production and refining capacity. When Chinese export restrictions on dysprosium, terbium, and related elements began tightening, allied governments moved quickly to formally classify these materials as strategically critical. Namibia's response to this environment has been to accelerate the development of its own HREE resources, most notably at the Lofdal project, which is widely regarded as one of the most significant heavy rare earth deposits identified outside Chinese jurisdiction.

The Project Pipeline: From Near-Production Assets to Early-Stage Discovery

Lofdal: The Crown Jewel of Namibia's HREE Ambitions

The Lofdal heavy rare earth project occupies a unique position in the global critical minerals landscape. Its geological profile is distinguished by an unusually high ratio of dysprosium and terbium relative to lighter rare earth elements, a characteristic that is rare globally and that drives exceptional per-tonne revenue potential compared with more common LREE-dominated deposits.

Pre-Feasibility Study outcomes point to potential annual production of approximately 2,000 tonnes of TREO (Total Rare Earth Oxides), including an estimated 117 tonnes of dysprosium and between 17.5 and 30 tonnes of terbium per year. At current indicative pricing levels, where terbium trades above $1,000 per kilogram and dysprosium commands approximately $250 per kilogram, the revenue profile of even a modest HREE producer is materially different from a light REE operation of equivalent tonnage.

| Rare Earth Element | Approx. Price (USD/kg) | Primary Application |

|---|---|---|

| Terbium (Tb) | ~$1,000+ | High-temperature permanent magnets |

| Dysprosium (Dy) | ~$250 | EV motors, wind turbine generators |

| Neodymium-Praseodymium (NdPr) | ~$65 | Permanent magnets (general) |

Capital expenditure requirements are estimated at sub-$300 million, making Lofdal a relatively modest capital commitment by the standards of major mining developments. Production commencement has been targeted for 2026, with PFS completion planned for end-2025. Consequently, the Lofdal rare earth project represents one of the most time-sensitive opportunities in the global HREE space.

The project's strategic significance extends beyond its geological merits. Japan's state-backed mining investment agency, JOGMEC (Japan Oil, Gas and Metals National Corporation), has committed to earning a 40% equity interest via $17 million in staged funding, with a pathway to 50% ownership through a total commitment of $20 million plus additional funding options. The structure of this agreement signals that Lofdal is not merely an exploration play but an asset that has attracted sovereign-level interest as a supply security solution for Japan's rare earth-dependent manufacturing sector.

"The price differential between heavy and light rare earths reflects their relative scarcity and the technical difficulty of substituting them in high-performance applications. For investors and strategic buyers alike, HREE-rich deposits in politically stable jurisdictions represent a category of asset that is structurally undersupplied globally."

The Eureka Monazite Project: A Western-Standard Concentrate Pathway

While Lofdal captures headlines for its HREE profile, the Eureka monazite project represents a different but complementary angle on Namibia's rare earth opportunity. Operator ReeXploration, a Namibia-based exploration firm, has defined a maiden resource estimate of 310,000 tonnes at 4.8% TREO, with neodymium-praseodymium identified as the dominant revenue driver.

What distinguishes Eureka commercially is the metallurgical behaviour of its ore. Bench-scale processing tests have confirmed 60% extractability using established, proven methods, a metric that speaks directly to the project's technical and economic viability. In the context of Western supply chain ambitions, the ability to produce a clean, consistently graded concentrate that meets EU and US qualification standards is not a trivial achievement.

Regulatory sourcing requirements under frameworks like the EU Battery Regulation increasingly demand that critical mineral inputs can be traced, verified, and assessed for ESG compliance at the point of origin. However, as Namibia's mining sector continues to mature, the country's growing emphasis on value-add processing means that future production may increasingly meet these standards at a domestic level.

Uis Polymetallic Project: Phase 1 Results and the Pegmatite Frontier

In April 2026, Australian-listed Askari Metals reported Phase 1 trenching results at its 100%-owned Uis Project, delivering results that underscored Namibia's emerging status as a polymetallic mineral province. Trenching was completed on approximately 40-metre spacing, a systematic methodology designed to guide the placement of follow-up drill holes scheduled for the second half of 2026.

Peak assay results from the Phase 1 programme included:

- Tin: 8,340 ppm

- Lithium oxide: 0.57% (exceeding commonly used cut-off thresholds for spodumene pegmatites)

- Tantalum: 299 ppm

- Rubidium: 2,380 ppm

The significance of the lithium oxide grade exceeding spodumene pegmatite cut-off thresholds deserves particular attention. Spodumene is the primary hard rock mineral source for battery-grade lithium, and cut-off grades in established lithium jurisdictions typically sit in the range of 0.4% to 0.5% lithium oxide. Uis Phase 1 results are already sitting above this threshold in the strongest intersections, suggesting genuine economic potential before a single drill hole has been completed.

Rubidium, at 2,380 ppm, is also worth noting. It is a lesser-discussed element with growing applications in atomic clocks, GPS technology, and quantum computing, sectors where supply security is increasingly prioritised by Western technology firms.

Karabib Lithium: A Long-Life Battery Supply Chain Asset

The Karabib lithium project adds another dimension to Namibia's battery materials credentials. Project parameters include 773,000 tonnes of lithium concentrate production over a 14-year mine life, with concentrate processed at a UAE-based facility at 56,700 tonnes per annum. The processing pathway through a UAE facility reflects the current state of downstream infrastructure development, though the longer-term trajectory of Namibian policy is firmly oriented toward bringing beneficiation onshore.

The EU-Namibia Strategic Partnership: Structure, Scope, and What It Actually Means

Formal bilateral agreements between resource-rich developing nations and major consuming blocs have a mixed historical track record. What distinguishes the EU-Namibia strategic partnership is the specificity of its commitments and the breadth of its scope. In addition, the partnership sits within the broader context of Europe's critical minerals supply chain diversification agenda, which is accelerating rapidly following recent geopolitical disruptions.

The partnership formally covers two pillars: renewable hydrogen development and raw material value chains. Beyond the headline agreement, the EU has committed to providing technical assistance supporting Namibia's development of a comprehensive national critical raw materials strategy. This represents a meaningful difference from a simple offtake arrangement.

Technical assistance that helps Namibia build regulatory capacity, develop domestic processing know-how, and design a long-term minerals governance framework creates the institutional conditions for sustained, scalable production. Namibia's Minister Amutse framed the relationship's logic plainly at the May 2026 EU-Namibia Business Forum: Europe's priority is achieving secure, diversified, and sustained mineral supply, while Namibia's priority is converting its resource endowment into industrial capacity, employment, and long-term economic development.

The minister was explicit that integration into European and global supply chains linked to batteries, renewable energy technologies, advanced manufacturing, and nuclear fuel markets represents the country's strategic ambition. Since the inaugural EU-Namibia Business Forum in 2023, the relationship has evolved from dialogue to a structured partnership with defined deliverables. This trajectory is consistent with the EU's Critical Raw Materials Act (CRMA) diversification mandate, which explicitly targets reducing member state dependence on single-source suppliers for any strategic mineral to below a defined concentration threshold.

How Namibia Compares to Competing Critical Mineral Jurisdictions

| Dimension | Namibia | DRC | Australia | Canada |

|---|---|---|---|---|

| Political Stability | High | Low-Medium | Very High | Very High |

| HREE Endowment | High (emerging) | Low | Moderate | Moderate |

| Processing Infrastructure | Developing | Limited | Advanced | Advanced |

| EU Strategic Partnership | Formal (active) | Informal | Bilateral | Bilateral |

| Exploration Activity | Surging (800+ applications) | Active | Mature | Active |

| ESG Risk Profile | Low-Medium | High | Low | Low |

The Regulatory Pressure Point: 800 Applications, 600 Pending Petitions

Investor enthusiasm for Namibia's mineral potential is quantifiable. As of March 2026, Mining Commissioner Isabella Chirchir confirmed that the country had received over 800 fresh exploration licence applications, representing an extraordinary surge of competitive interest in a jurisdiction that previously derived its mining identity primarily from uranium and diamonds.

Against this backdrop, Namibia currently holds 588 active exploration permits. The gap between active permits and new applications signals a system under significant pressure. Compounding the challenge, more than 600 environmental petitions remain pending, creating a dual bottleneck in both the licensing and environmental approval processes.

"Investor momentum and institutional processing capacity are not yet in alignment. The 600+ pending environmental petitions represent the most concrete near-term constraint on translating exploration enthusiasm into actual production outcomes, with the potential to extend individual project timelines by 12 to 24 months in some cases."

The government's response has been to digitalise the licensing system, using technology to reduce administrative backlogs and accelerate approval timelines. This is a positive signal, but it is worth distinguishing between the intent of regulatory reform and its execution at scale. For investors with capital allocated to Namibian exploration assets, the pace of digitisation rollout will be a critical variable in project scheduling.

Geopolitical Competition and the Race to Lock In Namibia's Output

Namibia's minerals are not going uncontested. Japan's structured equity investment in Lofdal through JOGMEC provides a template for how allied nations are seeking direct project-level exposure rather than relying on secondary market procurement. China, meanwhile, has not been passive. The completion of a domestic lithium processing plant in Namibia by Chinese firm Xinfeng in July 2024 signals that Chinese industrial capital has already established processing infrastructure inside the country's borders, creating a first-mover advantage in lithium beneficiation that Western-aligned investors will need to compete with directly.

The broader context of critical minerals geopolitics is also shaping how Western governments assess Namibia's strategic value. Africa's broader positioning in the global energy transition is shifting, with the continent's proposal of a critical minerals-backed currency framework reflecting a growing continental awareness that geological endowment translates into economic and geopolitical leverage. Furthermore, Namibia's nuclear energy ties add another dimension to its strategic profile, underscoring how deeply the country is embedded in multiple competing geopolitical frameworks.

For Western manufacturers and governments assessing Namibia's strategic value, the timeline question is pressing. The most advanced projects, including Lofdal, are approaching production-readiness. Offtake agreements negotiated now carry pricing and supply security advantages that will not be available after first production is achieved and competing buyers have entered the market. Namibia's ambition to become a major force in the global critical minerals landscape is backed by both geological reality and growing sovereign-level investment interest.

The next major ASX story will hit our subscribers first

Key Dimensions of the Namibia Critical Minerals and Rare Earths Opportunity

Before drawing conclusions, it is useful to consolidate the key structural factors that define Namibia's position in the global critical minerals landscape:

- Geological diversity: Namibia's confirmed endowment spans the complete energy transition value chain, from uranium and graphite to lithium, cobalt, and multiple rare earth elements

- HREE premium value: The Lofdal deposit's dysprosium and terbium profile places it among the most strategically significant rare earth assets outside China

- Near-term production visibility: Lofdal is targeting 2026 production commencement, with Uis polymetallic drilling scheduled for the second half of 2026

- Sovereign-level interest: JOGMEC's structured equity partnership at Lofdal reflects Japan's direct integration of Namibian supply into its national rare earth security framework

- Regulatory constraint: Over 600 pending environmental petitions represent the primary near-term risk to project timelines

- Geopolitical competition: Chinese processing infrastructure is already operational in Namibia, meaning Western-aligned investors face a competitive timeline pressure

Frequently Asked Questions: Namibia Critical Minerals and Rare Earths

What rare earth elements are found in Namibia?

Namibia's confirmed rare earth endowment includes dysprosium, terbium, neodymium, praseodymium, yttrium, cerium, and lanthanum. Associated polymetallic systems also carry tantalum, niobium, strontium, and rubidium, elements that are increasingly classified as critical by multiple Western governments due to their roles in advanced electronics, quantum computing, and clean energy technologies.

Why are heavy rare earths from Namibia particularly significant?

Dysprosium and terbium are irreplaceable in the highest-performance permanent magnet applications, including the drivetrains of electric vehicles and the generators inside offshore wind turbines. There is currently no commercially viable substitute for these elements in these applications, and China controls the majority of global production. Namibia's Lofdal deposit is one of the few identified HREE resources outside Chinese jurisdiction that has reached advanced feasibility assessment stage. For further context on critical raw materials policy across Africa, SFA Oxford's analysis of Namibia's regulatory landscape provides useful background.

What is the current state of Namibia's exploration licensing system?

As of March 2026, Namibia holds 588 active exploration permits, has received over 800 new licence applications, and has more than 600 environmental petitions pending. The government is implementing digital tools to reduce processing backlogs, but the gap between application volumes and administrative capacity represents a near-term constraint on new project approvals.

Is Namibia a safe jurisdiction for mining investment?

Namibia consistently ranks among Africa's most politically stable democracies. Its established mining sector, SADC and SACU trade framework membership, and formal EU strategic partnership provide multiple risk mitigation layers. The primary investable risks are regulatory processing delays and the nascent state of domestic downstream processing infrastructure, rather than political or sovereign risk factors.

Disclaimer: This article is intended for informational and educational purposes only. It does not constitute financial advice, investment recommendations, or a solicitation to buy or sell any security or commodity. All forecasts, project timelines, pricing references, and production targets mentioned are subject to change. Readers should conduct their own independent due diligence and consult qualified financial and legal advisers before making any investment decisions. Rare earth and critical mineral prices are volatile and can change materially over short periods.

Want to Identify the Next Major Critical Minerals Discovery Before the Broader Market?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries — including critical minerals and rare earths — instantly transforming complex geological data into actionable investment insights for both short-term traders and long-term investors. Explore why historic discoveries have generated extraordinary returns on Discovery Alert's dedicated discoveries page, and begin your 14-day free trial today to position yourself ahead of the market.