June 26, 2026

When Commodity Cycles Betray Structural Dependency: Reading Namibia's Economic Data in 2026

Namibia economy growth in Q1 2026 presents a compelling and sobering case study in how resource-rich nations navigate the tension between cyclical recovery and structural vulnerability. Resource-rich economies share a common paradox: the very assets that generate national wealth can simultaneously suppress the diversification needed to protect long-term stability. When commodity prices soften, production declines, or deposit grades deteriorate, the consequences ripple through government revenues, employment, household incomes, and ultimately GDP itself.

Understanding the Q1 2026 numbers requires more than reading a headline growth rate. It demands an examination of what is driving growth, what is suppressing it, and whether the forces at play are temporary or embedded.

When big ASX news breaks, our subscribers know first

Namibia Economy Growth in Q1 2026: The Headline and What Lies Beneath

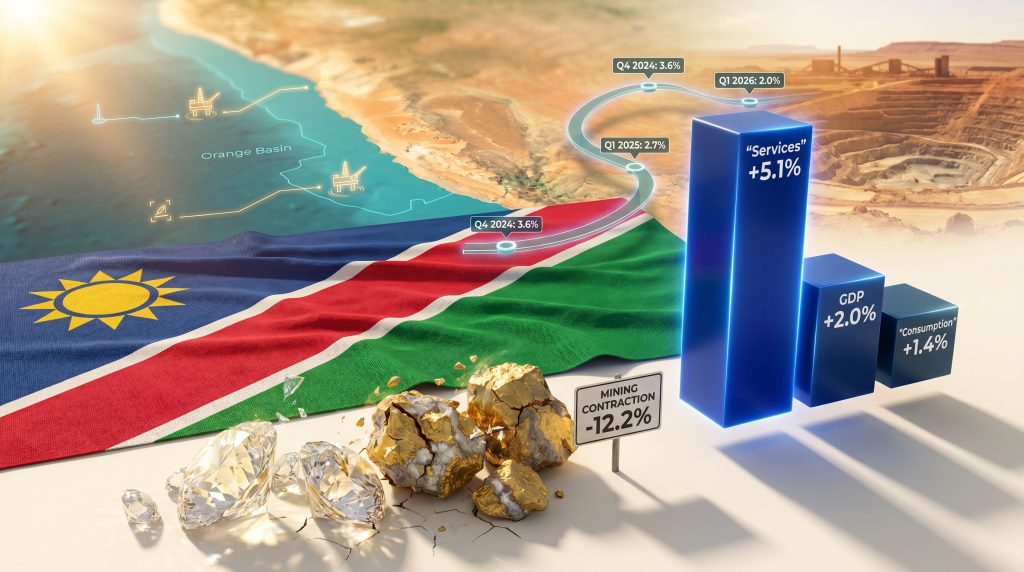

The Namibia Statistics Agency published its first-quarter 2026 national accounts on June 25, 2026, recording real GDP growth of 2.0%. On the surface, this represents a meaningful recovery from the near-stagnation of Q4 2025, when the economy expanded by just 0.1%. Framed differently, however, the result tells a more cautious story: Q1 2026 growth came in below the 2.7% to 2.8% recorded in the same quarter a year earlier, confirming a downward trend in year-on-year momentum.

The distinction between a quarterly rebound and a structural acceleration matters enormously for investors and policymakers alike. A jump from 0.1% to 2.0% signals that the economy did not fall further into stagnation, but it does not confirm a durable recovery. The engine driving that 2.0% is heavily concentrated in one sector, while the productive base that historically supported Namibia's export earnings is actively contracting.

| Period | Real GDP Growth | Key Characteristic |

|---|---|---|

| Q4 2024 | 3.6% (revised) | Broad-based expansion |

| Q1 2025 | 2.7% to 2.8% | Already slowing from 2024 peak |

| Q4 2025 | 0.1% | Near-stagnation |

| Q1 2026 | 2.0% | Partial rebound, below year-ago pace |

The Services Sector: Growth's Structural Anchor and Its Limitations

The tertiary sector delivered 5.1% real output growth in Q1 2026, providing the dominant upward contribution to the headline figure. Within this, several sub-sectors recorded positive performance:

- Wholesale and retail trade, supported by modest consumer activity

- Financial services, continuing a multi-quarter growth streak that has become one of the few consistent bright spots in Namibia's economy

- Health and education, underpinned by public expenditure commitments

- Public administration, reflecting sustained government activity levels

This services-led growth pattern is not new. In Q1 2025, health services expanded by 11.4%, wholesale and retail trade by 6.5%, and financial services by 6.0%, with those three sub-sectors collectively carrying the economy through an already-difficult period for mining. The repetition of this pattern in Q1 2026 confirms that the tertiary sector has become a structural floor for Namibian GDP.

"The concern is not that services are growing. The concern is that services alone are insufficient to replace the foreign exchange earnings, fiscal revenues, and employment multipliers generated by a healthy extractive sector."

Services activity, while valuable, tends to be domestically oriented. It generates employment and supports household incomes, but it does not produce the hard currency export receipts that fund Namibia's import requirements or the royalty and tax revenues that finance public investment. For those, the economy remains dependent on minerals.

Mining's 12.2% Contraction: Understanding the Mechanics of Decline

The most consequential number in the Q1 2026 data is not the headline 2.0% GDP figure. It is the 12.2% contraction in real value added from the mining sector, which the Namibia Statistics Agency attributed specifically to reduced output in diamonds and gold.

Diamond Sector: Structural Forces Are Not Cyclical Noise

Namibia's diamond industry, historically one of the most productive in the world, is facing pressures that extend well beyond a single bad quarter. Several interconnected forces are reshaping global diamond markets:

- Lab-grown diamond proliferation: The cost of producing synthetic diamonds has fallen dramatically over the past decade. Lab-grown stones now trade at discounts of 80% or more relative to natural equivalents of comparable size and quality, fundamentally altering consumer purchasing decisions in key markets including the United States and China.

- Ageing deposit grades: Namibia's onshore alluvial diamond deposits, which have been mined intensively for decades, are yielding lower average stone sizes and reduced carats per hundred tonnes of material processed. This grade dilution increases unit production costs even when volumes are maintained.

- Demand softness in key markets: China's post-pandemic luxury consumption recovery has underperformed expectations, weighing on global rough diamond demand. Chinese buyers, who account for a significant share of global polished diamond consumption, have shifted preferences toward alternative luxury categories.

- Rough diamond pricing pressure: The Antwerp and Dubai rough diamond markets have experienced multi-year price softness, compressing the revenue realised per carat even when physical production is maintained.

These dynamics explain why the IMF has flagged prolonged diamond sector weakness as a structural constraint on Namibia's growth trajectory, not simply a short-term headwind. Recovery in this segment depends on forces largely outside Namibia's control.

Gold Output: Reversal After Partial Recovery

Gold production had shown gradual improvement through parts of 2025, offering a partial offset to diamond weakness. That recovery reversed in Q1 2026, with lower gold output contributing meaningfully to the broader mining sector contraction. Unlike diamonds, gold's challenge in Namibia is more cyclical in nature, linked to production scheduling, operational factors at specific mines, and the grade profile of ore being processed during any given quarter.

Uranium: The Underappreciated Stabiliser

While diamonds and gold dominated the negative narrative, uranium production remained a positive contributor to Namibia's mining output, consequently cushioning the severity of the overall sector contraction. This is a detail that receives insufficient attention in broad economic commentary.

Namibia hosts two of the largest uranium mines by output capacity: the Rössing mine, one of the longest-operating open-pit uranium mines globally, and the Husab mine, which reached full production capacity in recent years and ranks among the largest uranium producers in the world by volume. Together, these operations position Namibia as one of the top five uranium-producing nations globally.

The global uranium market has experienced a significant structural repricing since 2021, driven by the resurgence of nuclear energy as a low-carbon baseload power source. European energy security concerns following the Russia-Ukraine conflict accelerated interest in nuclear power across multiple markets. Furthermore, uranium market volatility has, in this instance, worked in Namibia's favour, with elevated spot prices and long-term contract activity providing producers with a more favourable commercial environment than at any point since the Fukushima-era collapse in demand.

"Uranium represents one of Namibia's most strategically valuable commodities at this particular point in the global energy transition, yet it rarely features prominently in mainstream economic narratives about the country."

In addition, Namibia nuclear energy ties with international partners are adding a geopolitical dimension to the country's uranium outlook, further reinforcing long-term demand signals for its mineral exports.

Household Consumption: A 7-Point Deceleration That Signals Real Pain

The demand-side data amplifies the concern embedded in the supply-side figures. Household consumption expenditure grew by just 1.4% in real terms during Q1 2026, compared with 8.4% in Q1 2025. That is a deceleration of more than seven percentage points in a single year, and it reflects genuine deterioration in the living standards of ordinary Namibians.

Several interconnected factors explain this sharp slowdown:

- Mining sector employment contraction: When mines scale back output, the workforce reductions and wage bill compression that follow reduce household income directly in mining communities and indirectly across supply chain businesses.

- Elevated fuel prices: Higher global oil price movements feed through into transport costs, electricity tariffs, and the price of virtually every consumer good that moves through Namibia's supply chains. For households with limited disposable income buffers, this represents an effective income reduction.

- Consumer confidence softening: When economic uncertainty rises, households delay discretionary expenditure, reduce debt acquisition, and increase precautionary saving. This behavioural response amplifies the mechanical income effect, creating a demand contraction that can persist beyond the initial shock.

The consumption deceleration is significant because domestic demand is one of the few levers available to sustain growth when external sector performance weakens. A simultaneously contracting mining sector and a decelerating consumption base creates limited room for policy manoeuvre.

The IMF's Assessment: Subdued 2026 With a Conditional Medium-Term Recovery

The IMF's latest projections confirm that Q1 2026's performance is not an anomaly but rather an expression of broader economic constraints. Full-year 2025 GDP growth came in at approximately 1.7%, below earlier projections, reflecting the cumulative impact of diamond weakness, slower oil exploration progress, and subdued domestic demand.

For 2026, the Fund expects growth to remain constrained, with the Q1 2026 result of 2.0% broadly consistent with the cautious annual outlook. The medium-term picture improves gradually, with the IMF projecting a recovery toward approximately 3% over the coming years, contingent on several conditions being met.

| Forecast Period | IMF Growth Estimate | Critical Assumption |

|---|---|---|

| 2025 (actual) | ~1.7% | Diamond weakness, partial gold recovery |

| 2026 (projected) | ~2.0% to 2.5% | Continued diamond softness, high fuel costs |

| Medium term | ~3.0% | Oil development, export diversification |

The recovery pathway the IMF envisions depends on progress in offshore oil development, stabilisation of commodity prices, and continued services sector expansion. Each of these conditions carries meaningful execution risk.

The next major ASX story will hit our subscribers first

Offshore Oil: Namibia's Most Transformative but Uncertain Variable

No discussion of Namibia's economic trajectory is complete without addressing the offshore oil sector, which has attracted substantial international attention following significant discoveries in the Orange Basin in recent years.

The Orange Basin, situated off Namibia's southern Atlantic coastline, has emerged as one of the most prospective deepwater exploration frontiers in sub-Saharan Africa. Major international operators have reported material discoveries, and the basin's geological characteristics suggest the potential for world-class recoverable resources.

Investor interest remains active at the licensing level. The Namibian government recently approved a 25% stake transfer in the PEL96 offshore license from Tower Resources to Pakistan's Prime Global Energies, signalling ongoing international appetite for Namibian upstream exposure. Such transactions are a normal feature of the exploration financing landscape, where smaller companies bring in partners to share technical risk and capital requirements.

However, translating exploration success into production-level revenues involves a timeline measured in years to decades, not quarters. The IMF's citation of slower-than-expected oil exploration as a 2025 growth constraint reflects this reality. Even optimistic production scenarios suggest that meaningful oil export revenues remain several years away.

"If Namibia successfully develops its Orange Basin resources at scale, the economic transformation could be among the most significant in Southern Africa since Botswana's diamond development era. The timeline, however, remains deeply uncertain."

Structural Diversification: Incremental Progress Against a Persistent Challenge

The Q1 2026 data reinforces a challenge that Namibian economic planners have acknowledged for many years: the economy's export earnings and fiscal revenues remain disproportionately concentrated in a small number of mineral commodities, each subject to forces beyond domestic control.

Diversification efforts have included investment in agro-processing, expansion of financial services, development of tourism infrastructure, and efforts to build manufacturing capacity. Progress has been real but modest relative to the scale of the structural challenge. The services sector's consistent growth is partly a product of these efforts; however, services expansion alone cannot replace the foreign currency generation or fiscal contribution of a well-functioning mining sector.

For investors monitoring Namibia's macroeconomic trajectory, the key variables to track include:

- The global rough diamond price index and lab-grown diamond market penetration rates

- Uranium spot and long-term contract pricing relative to Rössing and Husab production costs

- Orange Basin exploration drilling results and development timeline announcements

- Household consumption growth as a leading indicator of domestic economic health

- Government fiscal balance as mining revenues fluctuate

What Q1 2026 Tells Investors About Namibia's Risk-Reward Profile

Namibia economy growth in Q1 2026 is one of a nation with genuine long-term potential navigating a difficult near-term period. The 2.0% growth rate represents neither collapse nor acceleration. It represents an economy holding itself together through services sector resilience while its traditional growth engine undergoes structural reconfiguration.

The risks are real: diamond sector recovery depends on global demand forces that Namibia cannot influence, oil production revenues remain years away, and household consumption lacks the momentum to serve as a durable growth substitute. The opportunities are also real: uranium investment dynamics are among the strongest in decades, offshore oil exploration continues to attract reputable international partners, and the services sector has demonstrated consistent growth capacity across multiple challenging quarters.

Investors and analysts assessing Namibia's near-term economic outlook should treat the Q1 2026 data as evidence of an economy in cyclical trough rather than structural deterioration. Whether the recovery toward the IMF's projected 3% medium-term growth rate materialises on schedule will depend less on domestic policy choices and more on the trajectory of global commodity markets and the pace of offshore energy development.

Disclaimer: This article is intended for informational purposes only and does not constitute financial or investment advice. All growth projections and forecasts referenced are derived from publicly available sources including the Namibia Statistics Agency and the International Monetary Fund. Economic conditions and forecasts are subject to change. Readers should conduct independent research before making any investment decisions.

Want to Capitalise on the Next Major Mineral Discovery Before the Broader Market Reacts?

As Namibia's uranium sector demonstrates, structural shifts in commodity markets can create significant investment opportunities for those positioned early — Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, instantly translating complex mineral data into actionable insights for investors at every experience level. Explore how historic discoveries have generated substantial returns on Discovery Alert's dedicated discoveries page, and begin your 14-day free trial today to secure a market-leading advantage.