July 5, 2026

Strategic positioning across global commodity markets has never required more sophisticated analysis than in 2026. While traditional investment frameworks focused on cyclical price movements and seasonal demand patterns, today's landscape presents an entirely different paradigm where technological transformation, geopolitical restructuring, and infrastructure modernisation converge to create unprecedented opportunities for long-term wealth creation.

Understanding this new commodity cycle requires abandoning conventional market timing approaches in favour of structural analysis that examines decades-long trends rather than quarterly fluctuations. Furthermore, the convergence of artificial intelligence deployment, renewable energy infrastructure buildout, and supply chain regionalisation represents a fundamental shift in how raw materials flow through the global economy.

Understanding Commodity Super-Cycles vs. Traditional Market Fluctuations

Modern commodity investing demands recognition that we are witnessing structural demand transformation rather than typical cyclical price appreciation. Historical analysis reveals that genuine super-cycles, spanning 15-20 years, emerge from permanent changes in global economic architecture rather than temporary supply-demand imbalances.

Historical Patterns of Multi-Decade Commodity Movements

The 1970s energy crisis established the template for understanding how geopolitical events can trigger sustained commodity appreciation lasting more than a decade. Unlike conventional market corrections that resolve within 2-5 years, super-cycles require fundamental shifts in global resource consumption patterns.

The 2000s China industrialisation boom demonstrated how emerging market development can sustain commodity demand for extended periods. China's GDP acceleration from 2000-2010, averaging approximately 10% annually according to World Bank data, created permanent infrastructure demand that supported steel, copper, and energy prices throughout the decade.

These historical precedents reveal critical characteristics distinguishing super-cycles from market volatility:

- Infrastructure investment patterns consistently exceed GDP growth rates during cycle initiation phases

- Technology adoption curves create permanent demand floors that prevent traditional cyclical corrections

- Industrial capacity expansion requires multi-year development timelines, preventing rapid supply responses

Key Indicators That Signal Cycle Transitions

Current market conditions exhibit several indicators historically associated with cycle transitions. Government infrastructure spending commitments across major economies now exceed traditional GDP correlations, suggesting structural rather than cyclical investment patterns.

Technology deployment timelines provide another critical indicator. Unlike previous commodity cycles driven by construction or manufacturing expansion, today's demand drivers involve systematic replacement of existing infrastructure with technologically advanced alternatives requiring different material compositions.

Geopolitical supply chain restructuring represents the third major indicator. Strategic stockpiling initiatives and domestic production incentives across multiple jurisdictions indicate permanent shifts in global trade patterns rather than temporary policy adjustments.

When big ASX news breaks, our subscribers know first

Which Structural Forces Are Driving the 2026 Commodity Shift?

Three convergent forces distinguish the current new commodity cycle from previous market episodes: energy transition infrastructure requirements, artificial intelligence computational infrastructure, and geopolitical supply chain regionalisation. Each force operates on multi-decade timelines with specific material requirements that cannot be substituted through conventional market mechanisms.

Energy Transition Infrastructure Requirements

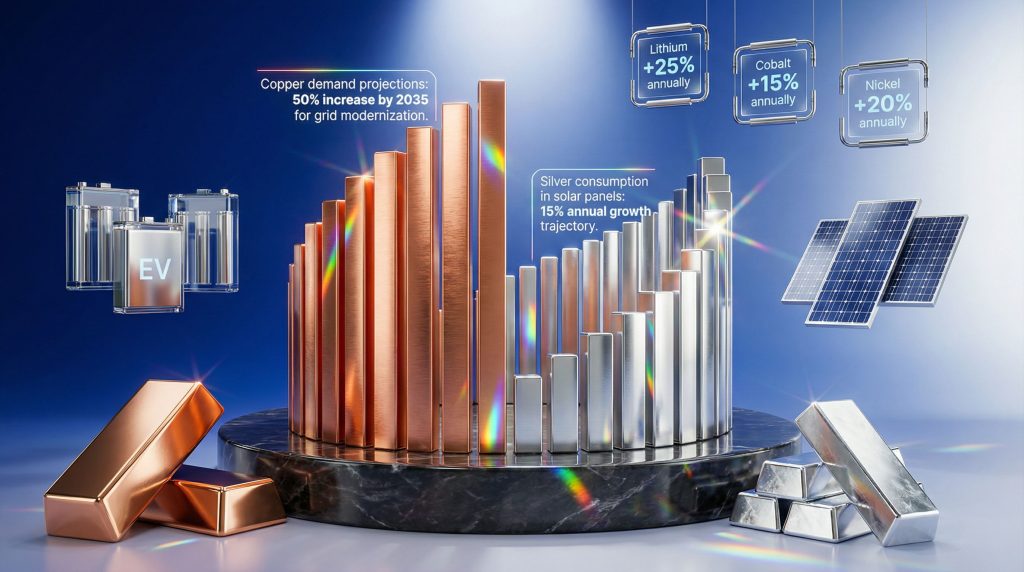

Grid modernisation represents perhaps the most significant copper demand driver in modern history. According to International Energy Agency assessments, electricity system transformation requires copper-intensive infrastructure replacement across transmission, distribution, and generation segments.

Smart grid deployment necessitates conductor material upgrades throughout existing electrical networks. High-voltage direct current (HVDC) transmission systems, essential for renewable energy distribution, require substantially more copper per mile than conventional AC systems.

Solar panel manufacturing continues expanding silver consumption at rates exceeding historical industrial applications. The Silver Institute's research indicates that photovoltaic cell production has become the largest industrial silver application, with technological improvements increasing rather than reducing silver content per panel.

Battery manufacturing supply chains present complex mineral interdependencies that extend far beyond lithium extraction. Cathode production requires specific cobalt and nickel compositions, while separator manufacturing involves specialised aluminium applications.

Artificial Intelligence and Data Centre Expansion

Hyperscale data centre construction introduces unprecedented infrastructure metal requirements. Cooling system specifications alone require substantial copper, aluminium, and specialised alloy applications not present in traditional commercial construction.

Semiconductor manufacturing expansion creates supply constraints in ultra-pure materials markets. Advanced chip production requires materials meeting specifications significantly more stringent than conventional industrial applications.

Power infrastructure upgrades supporting AI computational requirements extend beyond data centre facilities themselves. Grid capacity expansion, backup power systems, and transmission upgrades create cascading metal demand throughout electrical infrastructure networks.

Geopolitical Supply Chain Restructuring

Strategic mineral stockpiling initiatives across major economies indicate permanent shifts in government resource security priorities. Unlike previous strategic reserves focused primarily on energy, current initiatives encompass comprehensive critical minerals strategy portfolios.

Domestic production incentives reshape global trade patterns through policy mechanisms designed to reduce import dependencies. These initiatives operate on multi-decade timelines with substantial infrastructure investment commitments.

Resource diplomacy increasingly influences international relations, with mineral access agreements becoming components of broader strategic partnerships. This trend suggests supply chain regionalisation will persist regardless of short-term political changes.

Metals Markets: The New Investment Frontier

Industrial metals markets have evolved from traditional construction-driven demand patterns toward technology and infrastructure applications with fundamentally different consumption characteristics. This transformation creates investment opportunities distinct from historical commodity market dynamics.

Copper's Role as Economic Barometer 2.0

Copper's traditional correlation with economic growth increasingly reflects electrification trends rather than conventional construction activity. Renewable energy infrastructure requires substantially more copper per dollar of investment compared to fossil fuel alternatives.

Supply development challenges compound demand growth trends. Major copper deposits require 7-15 year development timelines from discovery through production, while permitting and environmental approval processes extend project delays further.

According to various industry forecasts, copper supply deficits could reach significant proportions by 2030, driven primarily by electrification infrastructure requirements rather than traditional economic growth patterns.

Precious Metals in Portfolio Diversification

Silver's dual characteristics as both industrial commodity and monetary hedge create unique investment dynamics during inflationary periods. Solar panel manufacturing, electronics production, and medical applications provide industrial demand floors supporting price appreciation.

Gold's performance during commodity cycles reflects both monetary debasement concerns and portfolio diversification demands. Central bank purchases, particularly from emerging market institutions, provide sustained demand independent of investment flows.

Investment allocation toward physical precious metals reflects broader concerns about financial system stability and currency devaluation risks. This positioning particularly benefits from understanding gold‐secular cycles and their relationship to broader market trends.

Battery Metal Dynamics and Supply Security

Battery metal markets exhibit supply concentration risks that distinguish them from traditional commodity markets:

| Metal | 2026 Demand Growth | Primary Supply Risk | Price Outlook |

|---|---|---|---|

| Lithium | Highly volatile | Chile/Australia concentration | Supply-constrained |

| Cobalt | Moderate expansion | DRC political stability | Geopolitical premium |

| Nickel | Infrastructure-driven | Indonesian export policies | Structurally higher |

Lithium market dynamics reflect rapid electric vehicle adoption exceeding previous forecasts. However, supply response through brine extraction and hard rock mining faces environmental permitting challenges and water availability constraints.

Cobalt supply concentration in the Democratic Republic of Congo creates geopolitical risk premiums affecting long-term contract negotiations. Alternative supply development in Canada and Australia proceeds slowly due to capital intensity requirements.

Nickel markets face supply disruption potential from Indonesian export policy changes. Class I nickel suitable for battery applications commands premiums over stainless steel grades, creating market segmentation not present historically.

Energy Commodities: Navigating Oversupply Pressures

Traditional energy commodities confront structural headwinds as renewable energy cost competitiveness reaches critical thresholds across most global markets. However, transition timelines create complex supply-demand dynamics requiring careful analysis for investment positioning.

Oil Market Structural Headwinds

Global oil market fundamentals reflect accelerating demand destruction from transportation electrification and industrial fuel switching. Electric vehicle adoption rates in major markets continue exceeding previous projections, with implications extending beyond passenger vehicle segments.

Non-OPEC production capacity expansion, particularly from unconventional sources, continues outpacing demand growth despite OPEC+ production management efforts. Technological improvements in extraction efficiency reduce production costs while increasing recoverable reserves.

OPEC+ coalition effectiveness faces challenges from divergent member economic priorities and production capacity constraints. Market share preservation strategies compete with revenue maximisation objectives during periods of structural demand transition.

Natural Gas and LNG Market Imbalances

Global natural gas markets exhibit pronounced regional pricing disparities reflecting infrastructure bottlenecks and supply-demand mismatches. European market restructuring following recent energy security concerns creates persistent volatility patterns.

LNG trade flow optimisation faces constraints from terminal capacity limitations and shipping availability. Long-term contract renegotiations reflect changing fundamental assumptions about demand growth and supply availability.

Pipeline infrastructure development lags behind production capacity expansion, creating arbitrage opportunities constrained by transportation limitations rather than fundamental supply-demand balance.

Coal's Accelerated Decline Trajectory

Renewable energy cost competitiveness has reached decisive tipping points in most major markets. According to the National Renewable Energy Laboratory's levelised cost analysis, solar and wind generation costs have achieved parity with or undercut coal-fired generation across most global markets.

Carbon pricing mechanism expansion creates additional cost pressures on coal utilisation. The International Carbon Action Partnership documents accelerating implementation of carbon pricing systems across major economies.

Stranded asset risks in traditional coal mining regions reflect permanent demand destruction rather than cyclical corrections. Financial institutions increasingly restrict funding for new coal projects whilst existing operations face early retirement pressures.

Agricultural Commodities: Climate and Policy Intersections

Agricultural commodity markets face simultaneous pressures from climate pattern disruptions, regulatory compliance requirements, and technological transformation initiatives. These forces create complex supply-demand dynamics requiring specialised analysis approaches.

Weather Pattern Disruptions and Crop Volatility

La Niña and El Niño climate cycles continue influencing global grain production patterns, but extreme weather events increasingly override traditional seasonal patterns. NOAA Climate Prediction Centre data indicates increasing frequency of weather anomalies affecting major production regions.

Regional food security policies respond to supply volatility through strategic reserve accumulation and export restriction mechanisms. These policy responses create additional price volatility beyond fundamental supply-demand factors.

Insurance cost increases reflect actuarial assessment of increased weather-related crop damage risks. Premium increases affect producer economics whilst crop revenue protection mechanisms influence planting decisions.

Sustainable Agriculture Transition Costs

EU Deforestation Regulation compliance requirements, effective since December 2024, create additional cost structures for agricultural commodity importers. Traceability and certification requirements affect supply chain efficiency and pricing.

Organic farming conversion processes reduce production volumes during transition periods whilst increasing input costs. However, premium pricing for organic products provides economic incentives supporting continued conversion.

Precision agriculture technology adoption improves efficiency but requires substantial capital investments. GPS guidance systems, variable rate application equipment, and soil monitoring technologies increase productivity whilst reducing environmental impact.

Portfolio Construction for Commodity Cycle Exposure

Constructing investment portfolios positioned for the new commodity cycle requires understanding different exposure mechanisms and their respective risk-return characteristics. Direct commodity ownership, mining equity exposure, and infrastructure investments provide varying degrees of sensitivity to underlying commodity price movements.

Direct vs. Indirect Commodity Investment Approaches

Physical commodity ETFs provide direct price exposure but face storage costs and contango effects in futures-based products. Gold and silver ETFs such as SPDR Gold Shares (GLD) and iShares Silver Trust (SLV) offer direct metal exposure with professional storage and insurance.

Futures-based commodity funds face roll costs during contango markets but provide broad commodity exposure through single investment vehicles. Products like PowerShares DB Commodity Index Tracking Fund (DBC) provide diversified exposure across energy, metals, and agricultural commodities.

Mining equity investments provide operational leverage to commodity prices but introduce company-specific risks including management quality, operational efficiency, and capital allocation decisions. Furthermore, understanding the broader mining industry evolution helps inform investment selection.

Geographic Diversification Considerations

Resource-rich emerging markets offer direct exposure to commodity production but face political risk and currency volatility. Australian and Canadian mining companies provide developed market exposure to global commodity demand.

Currency hedging strategies become critical when investing across multiple jurisdictions. Commodity producers in countries with weakening currencies may outperform despite stable commodity prices due to cost structure advantages.

Political risk assessment requires monitoring regulatory changes affecting mining operations, environmental standards, and resource taxation policies. Jurisdictional stability rankings influence long-term investment attractiveness.

Timing and Allocation Framework

Critical Investment Principle: Commodity cycles typically reward early positioning but demand patience for structural trends to materialise in sustained price appreciation. Historical analysis suggests 18-24 month lead times before fundamental shifts generate consistent returns.

Dollar-cost averaging approaches help manage volatility inherent in commodity markets whilst maintaining exposure to long-term trends. Systematic investment programmes reduce timing risk whilst capturing average price appreciation over cycle duration.

Allocation percentages depend on overall portfolio risk tolerance and correlation with existing holdings. Commodity exposure typically ranges from 5-15% of diversified portfolios, with higher allocations appropriate during early cycle phases.

The next major ASX story will hit our subscribers first

Risk Management in Volatile Commodity Markets

Commodity market volatility requires sophisticated risk management approaches that account for both systematic and idiosyncratic risks. Traditional portfolio management techniques must adapt to unique characteristics of commodity investments.

Volatility Patterns During Cycle Transitions

Commodity prices exhibit increased volatility during structural adjustment periods as markets price in fundamental changes to supply-demand balance. Standard deviation measurements from historical periods may underestimate future volatility during transition phases.

Correlation breakdowns between asset classes occur during periods of significant commodity price moves. Traditional portfolio diversification benefits diminish when commodity inflation affects multiple asset categories simultaneously.

Liquidity considerations become particularly important in physical commodity markets where transaction costs and bid-ask spreads widen during periods of high volatility.

Hedging Strategies for Commodity Exposure

Options strategies provide asymmetric risk-reward profiles suitable for commodity cycle positioning. Call options on commodity producers or commodity ETFs limit downside risk whilst maintaining upside participation.

Stop-loss mechanisms require careful calibration in volatile commodity markets. Technical analysis-based stop levels may prevent premature exit during normal volatility whilst protecting against significant adverse moves.

Portfolio rebalancing frequency must account for commodity price momentum characteristics. Too-frequent rebalancing may reduce returns during trending markets, whilst infrequent rebalancing increases concentration risk.

Duration Forecasting Based on Fundamental Drivers

Estimating commodity cycle duration requires analysis of the fundamental forces driving structural change. Unlike previous cycles driven primarily by economic growth or geopolitical events, the current new commodity cycle reflects technological transformation timelines spanning multiple decades.

Technology Adoption Curve Implications

S-curve adoption patterns in renewable energy deployment suggest sustained commodity demand over 15-20 year periods. Solar and wind capacity installation rates continue accelerating globally, with International Energy Agency projections indicating sustained growth through 2040.

Infrastructure replacement cycles inherently require extended time periods. Electrical grid modernisation, transportation system electrification, and industrial process conversion operate on timelines measured in decades rather than years.

Regulatory implementation schedules provide visibility into demand timelines. Carbon emission reduction targets, renewable energy mandates, and electric vehicle adoption requirements create policy certainty supporting long-term investment decisions.

Supply Response Mechanisms and Lead Times

Mining project development timelines from discovery through production typically require 7-15 years, preventing rapid supply responses to price increases. Permitting processes, environmental assessments, and infrastructure development extend these timelines further.

Capital allocation decisions in commodity companies reflect long-term price expectations rather than current market conditions. Investment committees approve mining projects based on fundamental analysis spanning project lifetimes of 20-50 years.

Technological improvements in extraction and processing efficiency provide gradual supply increases but cannot offset major supply-demand imbalances quickly enough to prevent sustained price appreciation.

Demand Sustainability Assessment

Emerging market industrialisation trajectories support sustained commodity demand growth independent of developed market consumption patterns. Infrastructure development in Asia, Africa, and Latin America requires substantial material inputs over multi-decade periods.

Developed market consumption evolution reflects quality improvements and efficiency gains rather than volume growth. However, material intensity of renewable energy infrastructure exceeds fossil fuel alternatives, supporting overall demand growth.

Substitution technology development proceeds slowly due to performance requirements and cost considerations. Alternative materials research continues but faces technical barriers preventing rapid displacement of established commodities.

Scenario Planning for Cycle Evolution

Multiple scenario outcomes remain possible for commodity cycle evolution, each with distinct implications for investment strategy and risk management. Probabilistic analysis across different scenarios provides framework for positioning decisions.

Bull Case: Extended Super-Cycle (2026-2040)

Accelerated energy transition mandates driven by climate policy urgency could extend commodity demand beyond current projections. Government spending commitments supporting renewable energy deployment, grid modernisation, and transportation electrification provide demand floors supporting sustained price appreciation.

Geopolitical fragmentation requiring redundant supply chains would multiply material requirements for strategic infrastructure. Domestic production initiatives and supply chain regionalisation increase total global capacity requirements whilst reducing efficiency gains from specialisation.

Emerging market GDP growth exceeding current expectations would compound infrastructure-driven demand. Continued urbanisation in Asia, Africa, and Latin America requires substantial commodity inputs for construction, transportation, and energy infrastructure development.

Bear Case: Shorter Cycle Duration (2026-2030)

Rapid technological substitution could reduce material intensity faster than anticipated. Breakthroughs in alternative materials, recycling efficiency, or production processes might limit commodity demand growth despite continued economic expansion.

Economic recession dampening industrial demand represents another scenario limiting cycle duration. Global financial instability, trade disruptions, or policy mistakes could reduce industrial activity and infrastructure investment supporting commodity demand.

Supply response faster than historical precedent might occur through technological improvements, regulatory streamlining, or capital allocation efficiency gains. Accelerated mining project development could alleviate supply constraints sooner than expected.

Base Case: Selective Commodity Performance

Differentiated outcomes across commodity categories reflect varying demand drivers and supply constraints. Energy transition metals might outperform fossil fuels whilst agricultural commodities face distinct climate and policy pressures.

Regional variations in cycle timing and magnitude would create geographic arbitrage opportunities. North American, European, and Asian markets might experience different cycle phases based on local policy implementation and economic conditions.

Policy intervention effects could moderate extreme price movements through strategic reserve releases, trade policy adjustments, or regulatory modifications affecting supply-demand balance.

Key Takeaways for Investors and Market Participants

Successfully navigating the new commodity cycle requires strategic thinking that transcends traditional market analysis approaches. Understanding structural demand drivers, technological transformation timelines, and geopolitical supply chain evolution provides essential framework for long-term positioning decisions.

Strategic Principles for Commodity Cycle Navigation

Focus on structural demand drivers rather than cyclical factors when evaluating long-term commodity investments. Energy transition infrastructure, artificial intelligence deployment, and supply chain regionalisation operate on multi-decade timelines unaffected by traditional business cycle fluctuations.

Diversification across commodity categories and geographic regions helps manage concentration risks whilst maintaining exposure to broad transformation trends. Different commodities exhibit varying sensitivity to specific demand drivers and supply constraints.

Patience for long-term themes to materialise in pricing remains essential for commodity cycle investing. Structural changes require time to translate into sustained price appreciation, with historical precedent suggesting 18-24 month lead times for trend confirmation.

Monitoring Framework for Cycle Progression

Leading indicators include infrastructure spending announcements, policy implementation schedules, and technology deployment rates. Government budget allocations, regulatory timelines, and corporate capital expenditure plans provide forward-looking insight into demand trajectory.

Coincident indicators encompass inventory levels, price momentum, and production utilisation rates. Current supply-demand balance metrics reflect immediate market conditions whilst indicating potential supply constraints or surplus situations.

Lagging indicators involve supply capacity additions, demand destruction evidence, and substitution technology adoption. These metrics confirm cycle progression but provide limited predictive value for positioning decisions.

Additionally, understanding gold as inflation hedge becomes particularly relevant during commodity cycles when inflation concerns intensify.

For investors considering exposure to this transformation, recognising the importance of critical minerals and energy security provides crucial context for long-term positioning strategies.

As highlighted in recent analysis of commodity cycle characteristics, structural transformation indicators suggest extended duration potential for current trends.

Disclaimer: This analysis presents forward-looking assessments based on current market conditions and historical precedent. Commodity markets involve substantial risk including complete loss of investment principal. Readers should conduct independent research and consider consulting qualified financial professionals before making investment decisions. Market conditions, government policies, and technological developments may differ from projections presented.

Understanding the new commodity cycle requires recognising that traditional analytical frameworks may prove inadequate for comprehending the structural transformation currently underway. Technological advancement, geopolitical reconfiguration, and climate policy implementation create investment landscapes fundamentally different from historical precedent, demanding sophisticated analysis and strategic patience for successful navigation.

Ready to capitalise on the next commodity discovery?

Discovery Alert instantly identifies significant ASX mineral discoveries using its proprietary Discovery IQ model, providing actionable insights during market transitions when strategic commodity positioning becomes most critical. Historical major discoveries demonstrate the potential for exceptional returns, which you can explore through Discovery Alert's dedicated discoveries page showcasing previous breakthrough announcements and their market impact.