June 17, 2026

The Upstream Gap That Could Derail America's Nuclear Ambitions

The global uranium supply chain is often discussed from the reactor end outward. Policymakers celebrate new builds, technology companies announce power purchase agreements, and enrichment facilities attract capital. Yet the foundational question of where the raw uranium actually originates receives comparatively little attention. This asymmetry between downstream enthusiasm and upstream neglect is not merely an oversight — it represents one of the most consequential structural vulnerabilities in the American energy system today.

Understanding that vulnerability requires looking at a single state that holds more untapped nuclear fuel potential than almost anywhere else in the Western world: New Mexico. New Mexico uranium in situ recovery sits at the centre of this national conversation, and for good reason.

When big ASX news breaks, our subscribers know first

Why New Mexico Uranium In Situ Recovery Is a National Priority

The Numbers Behind the Supply Crisis

Nuclear energy currently accounts for approximately 20% of total U.S. electricity generation, making it the single largest source of carbon-free baseload power in the country. Yet the domestic uranium production infrastructure that once supported this fleet has largely ceased to function at meaningful scale.

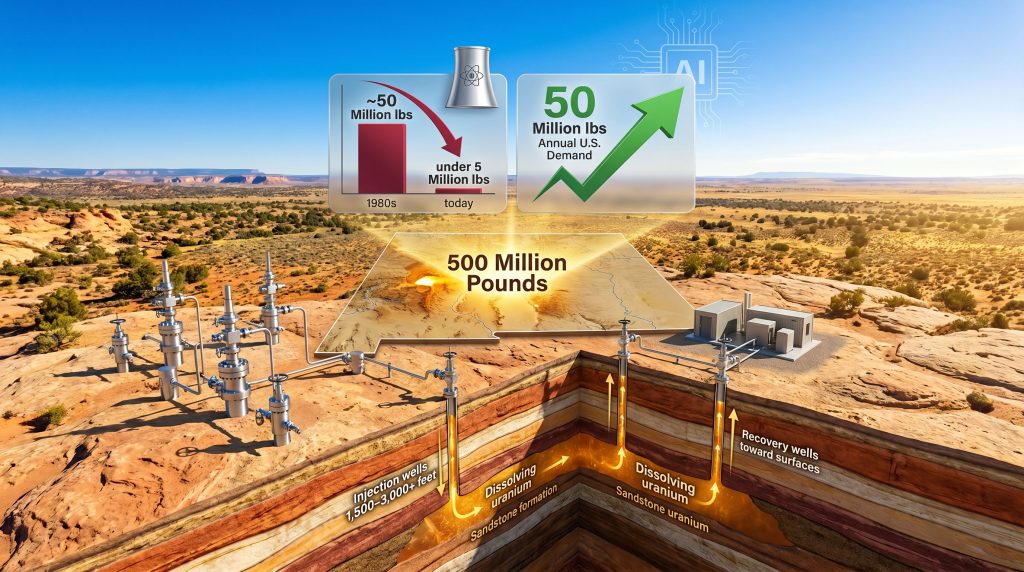

At its peak in the 1980s, the United States produced close to 50 million pounds of uranium per year from domestic operations. Today, that figure has collapsed to well under 5 million pounds annually, and for a period in recent years, total domestic output fell below even 1 million pounds. Against annual demand of approximately 50 million pounds, current domestic production covers somewhere between 5% and 10% of national requirements.

The structural consequence is stark: the country that pioneered civilian nuclear power and developed in situ recovery (ISR) technology is now more than 90% dependent on imported uranium to fuel its reactor fleet. Understanding the broader uranium market dynamics helps contextualise just how exposed the domestic supply chain has become.

The U.S. nuclear industry has effectively outsourced its entire upstream fuel supply chain over four decades, creating a dependency that no amount of reactor investment downstream can resolve without a parallel mining revival upstream.

New Mexico's Half-Billion Pound Resource Base

New Mexico's Grants Mineral Belt in the northwestern part of the state ranks as the second-largest uranium reserve province in the United States and hosts one of the most significant concentrations of sandstone-hosted uranium deposits anywhere in the world. Known and historic resources within the state are estimated at approximately 500 million pounds, with state geological surveys indicating a comparable additional 500 million pounds of undiscovered potential.

Placed against current U.S. annual consumption of roughly 50 million pounds, this resource base carries the theoretical capacity to supply the entire domestic reactor fleet for approximately two decades. The critical additional fact is that the geology of New Mexico's uranium deposits is predominantly ISR-amenable, meaning the ore can be extracted through solution mining rather than conventional excavation, blasting, or open-pit methods.

What Is In Situ Recovery and How Does It Work?

A Technical Walkthrough of ISR Uranium Extraction

New Mexico uranium in situ recovery is a method of extracting uranium from underground rock formations without physically disturbing the surface or removing ore to the surface. The process is sequential and methodical:

- Injection wells are drilled into uranium-bearing sandstone aquifers, typically at depths ranging from 1,500 to over 3,000 feet

- Oxygenated groundwater amended with sodium bicarbonate is pumped into the formation, creating a lixiviant that chemically mobilises uranium from the host sandstone

- Recovery wells surrounding the injection point draw the uranium-laden solution back to the surface

- The solution passes through an ion-exchange resin system at the surface processing facility, which strips dissolved uranium from the water using a process functionally similar to a household water softener

- Approximately 99% of the processed water is returned to the aquifer after uranium extraction, maintaining hydrological balance and supporting groundwater restoration

ISR vs. Conventional Uranium Mining

| Feature | ISR (In Situ Recovery) | Conventional Mining |

|---|---|---|

| Surface disturbance | Minimal (wellheads only) | Significant (pits, waste dumps) |

| Mine tailings produced | None | Substantial |

| Processed water returned | ~99% | Minimal |

| Blasting or tunnelling required | No | Yes |

| Regulatory footprint | Lower | Higher |

| Share of global uranium output | ~60% | ~40% |

| Typical target depth | 500 to 3,500 feet | Surface to 2,000+ feet |

ISR technology was originally developed in the United States approximately 50 years ago, largely by oil and gas companies that encountered uranium in their drill logs while exploring for hydrocarbons. Those same companies generated much of the historic resource data that now underlies modern ISR project portfolios across New Mexico. Globally, ISR now accounts for the majority of all uranium produced worldwide, a statistic that often surprises those who associate uranium extraction primarily with large open-pit mines. For further context on the in situ leaching benefits that distinguish this approach, the environmental profile is particularly compelling.

Environmental and Safety Profile

The U.S. Nuclear Regulatory Commission (NRC) has confirmed there have been no drinking water contamination incidents attributable to ISR operations across its entire regulatory history. New Mexico projects targeting deep sandstone aquifers at depths of approximately 3,000 feet operate in zones that are physically isolated from shallower domestic water supply aquifers by steel-cemented well casings.

These deep zones are classified as non-potable under regulatory designations known as aquifer exemptions, which formally establish target formations as unsuitable for drinking water prior to any operations commencing. According to World Nuclear Association's guidance on ISR mining, this regulatory framework has been refined considerably over decades of operational experience.

One of the most persistent barriers to ISR advancement in New Mexico is not geological complexity or technical difficulty. It is a community knowledge gap around what modern ISR actually involves. Addressing that gap through education and direct site visits functions as a genuine permitting accelerant.

Federal Urgency: Why the Policy Environment Is Shifting

The Defense Production Act Nuclear Fuel Cycle Consortium

In late April 2026, the U.S. Department of Energy's Office of Nuclear Energy launched the Defense Production Act Nuclear Fuel Cycle Consortium, a formal initiative designed to coordinate federal and industry efforts to secure the domestic nuclear fuel supply chain. The initiative is explicitly designed to ensure adequate fuel supply for both the existing reactor fleet and next-generation advanced reactors.

Beyond the policy dimension, there is a legally binding military requirement that creates a guaranteed floor of domestic demand. Under existing U.S. legislation, uranium used for military applications must be sourced exclusively from domestic producers. This covers nuclear submarine refurbishment programmes, naval propulsion systems, and warhead maintenance cycles. Unlike commercial utility demand, military uranium procurement is structurally insulated from foreign competition.

Nuclear submarines require periodic refuelling and refurbishment, warhead inventories erode over time and require replenishment, and the U.S. naval fleet is actively expanding its submarine programme. Each of these requirements feeds directly into a domestic uranium demand baseline that is independent of electricity market dynamics. The broader uranium supply challenges facing the nation make this military floor of demand all the more strategically significant.

Big Technology and the Power Purchase Agreement Wave

The technology sector has introduced a new and previously uncorrelated source of uranium demand. Major companies including Microsoft, Google, Meta, and Amazon have entered or are actively exploring power purchase agreements tied to nuclear generation capacity.

In June 2026, U.S. regulators granted a waiver to accelerate the restart of Three Mile Island Unit 1, with output contracted to serve Microsoft's data centre operations. The symbolic weight of that decision, given Three Mile Island's historic association with nuclear risk, is difficult to overstate.

AI infrastructure is generating electricity demand at a rate and consistency that intermittent renewable sources cannot reliably serve. Nuclear baseload capacity is consequently viewed as a structural necessity rather than a supplementary option.

A useful analogy helps frame where uranium extraction fits in this picture: the push for conversion, enrichment, and reactor capacity downstream is functionally equivalent to building refineries and neglecting the oil fields that supply them. The downstream infrastructure is visible and politically rewarding to champion, yet without the upstream fuel supply, the downstream investment cannot function.

SMRs and the Enrichment Bottleneck

Small modular reactors (SMRs) add a further dimension to the supply challenge that is not yet widely reflected in uranium equity valuations. SMRs require high-assay low-enriched uranium (HALEU) at enrichment levels up to 19.75%, compared with the approximately 5% enrichment used in conventional light-water reactors.

Existing U.S. enrichment infrastructure is not currently configured to supply HALEU at commercial scale, creating a dual bottleneck: insufficient uranium extraction capacity upstream and insufficient enrichment capability midstream. Both constraints must be resolved before SMR deployment can scale meaningfully.

The Permitting Landscape for New Mexico ISR Projects

Agreement States vs. Direct NRC Jurisdiction

A regulatory distinction that receives insufficient attention in mainstream coverage of uranium development is the difference between agreement states and states under direct NRC jurisdiction. In agreement states such as Texas and Wyoming, the NRC has devolved regulatory authority over uranium ISR to state agencies. This devolution produces more streamlined, predictable permitting timelines and has contributed to ISR activity concentrating in those jurisdictions.

New Mexico remains under direct NRC jurisdiction, meaning developers must simultaneously navigate both federal NRC licensing requirements and state-level permitting processes administered by the New Mexico Environment Department (NMED). This dual-track system has historically extended development timelines and increased regulatory uncertainty.

Achieving something comparable to agreement state status, or negotiating equivalent streamlining, may represent the single most impactful regulatory reform available for accelerating New Mexico's uranium development timeline. Furthermore, the US uranium production rebound already under way in other states demonstrates what streamlined regulation can unlock.

Key Permitting Milestones

- NRC Licence Application covering environmental impact assessment, safety analysis, and public comment periods

- Aquifer Exemption Petition filed with the EPA, formally classifying the target aquifer zone as non-potable prior to operations

- NMED Water Quality Bureau Permits covering discharge authorisation and groundwater monitoring requirements

- Tribal and Community Consultation mandated under NEPA and federal trust responsibilities

- State Land Office Approvals where state-administered mineral rights are involved

The aquifer exemption process is widely considered the single most time-sensitive milestone in the New Mexico ISR permitting sequence, often defining project timelines more decisively than any technical readiness factor.

Typical Project Timeline

| Phase | Estimated Duration |

|---|---|

| Resource definition and technical reporting | 6 to 18 months |

| Permitting and regulatory approvals | 5 to 10 years |

| Construction and wellfield installation | 12 to 24 months |

| Active production life | 20 to 30 years |

| Aquifer restoration and site reclamation | 3 to 5 years post-closure |

Even under favourable conditions, new ISR projects in New Mexico are unlikely to reach production before the early-to-mid 2030s under existing permitting frameworks. This timeline underlines the urgency of initiating the process now rather than waiting for further policy clarity.

The Grants Mineral Belt: Geology, Data, and Development Potential

Tabular Sandstone Deposits and ISR Compatibility

The Grants district in northwestern New Mexico hosts the largest concentration of known uranium resources in the United States outside of Wyoming's Powder River Basin. The deposits are predominantly tabular sandstone-hosted, which is the geological configuration most compatible with ISR extraction techniques.

The depositional geometry allows for efficient wellfield design, predictable solution flow patterns, and manageable aquifer restoration programmes. A less commonly appreciated aspect of New Mexico uranium development is the extraordinary volume of historical subsurface data generated during the exploration boom of the 1970s and 1980s.

Oil and gas companies drilling across the region logged uranium occurrences routinely and accumulated extensive proprietary datasets covering formation geometry, grade distribution, depth profiles, and hydrological characteristics. Much of this data remains privately held and has never entered the public domain, meaning companies with access to it hold a genuine informational advantage. The EPA's overview of uranium mine operations provides useful background on the regulatory context within which these historic datasets were generated.

Historic Resources and Modern Cutoff Grade Adjustments

A technically important but underappreciated detail relevant to New Mexico ISR resource estimation concerns cutoff grade assumptions. Many of the historic resource estimates in the Grants district were calculated using cutoff grades that are materially higher than those routinely used in modern ISR project evaluation.

As a result, resources estimated under historic parameters may understate the economically extractable uranium when reassessed against current industry standards. Updated NI 43-101 compliant technical reports that apply contemporary cutoff grades and incorporate peripheral drilling could produce resource estimates meaningfully higher than those in the historic record.

The Economic Case for Development

A full-scale ISR operation in the Grants district is projected to generate:

- Over 200 skilled local jobs during the operational phase

- Cumulative state and local tax revenue of $400 million or more across a 20 to 30-year operational life

- Carbon-free electricity generation aligned with both state climate commitments and federal clean energy policy objectives

Community Engagement: The Permitting Accelerant That Rarely Appears in Technical Reports

A landmark conference titled Nuclear in New Mexico: Fuelling the U.S. Nuclear Renaissance brought together stakeholders for the first time in approximately 40 years. Attendees included:

- Utility representatives

- International uranium trading houses from South Korea and Japan

- Federal national laboratories including Los Alamos and Sandia

- Tribal representatives and community members

- State educational institutions

- Everyday citizens from affected communities

The gathering surfaced a finding that has significant implications for project timelines: community unfamiliarity with modern ISR technology is widespread, and that unfamiliarity creates opposition that is not fundamentally anti-uranium, but rather anti-uncertainty. When stakeholders are taken to operating ISR sites and shown what the technology actually involves, resistance frequently converts to cautious acceptance.

Ongoing work at national laboratories on next-generation ISR approaches, sometimes described as ISR 2.0, reinforces the case that the technology continues to improve beyond its already strong environmental baseline. The conference produced a working consensus that uranium extraction in New Mexico is both necessary and achievable, provided legacy environmental concerns from earlier conventional mining eras are acknowledged transparently and modern ISR is clearly differentiated from those historical practices.

The next major ASX story will hit our subscribers first

Uranium Equity Markets: Understanding the Disconnect

Why Strong Fundamentals Are Not Translating to Share Price Performance

The URNM ETF, a widely used proxy for uranium sector equity performance, was trading approximately flat to marginally negative year-to-date as of mid-2026. Spot uranium prices, after an acceleration phase that drew significant investor attention, have largely consolidated in the $85 to $100 per pound range, reducing speculative momentum.

Investor attention has rotated toward high-profile technology sector opportunities, including anticipated major IPOs. Against that backdrop, uranium exploration and development companies have become relatively underfollowed. However, the uranium supply-demand volatility underlying these markets remains structurally unresolved.

The underlying demand fundamentals have not weakened. Annual domestic demand of approximately 50 million pounds is covered only 5 to 10% by domestic production. AI data centre expansion and SMR deployment pipelines represent demand additions that are not yet reflected in uranium equity valuations.

The supply response from new ISR projects requires 5 to 10 years of lead time, meaning production from projects entering permitting today cannot reach market before the early-to-mid 2030s. That lag is a structural feature, not a temporary obstacle.

Potential Re-Rating Catalysts

| Potential Catalyst | Likely Timeline | Impact Level |

|---|---|---|

| Uranium spot price sustained above $100/lb | 1 to 3 years | High |

| Defense Production Act federal procurement contracts | 1 to 2 years | High |

| New Mexico permitting reform or agreement state progress | 3 to 7 years | Very High |

| SMR commercial deployment announcements | 3 to 5 years | Medium-High |

| Major utility long-term contracting cycle | 2 to 4 years | High |

| Additional technology sector nuclear PPAs | 1 to 2 years | Medium |

Three Scenarios for New Mexico Uranium Development Through 2035

Scenario 1: Accelerated Federal Coordination (Bull Case)

New Mexico achieves agreement state status or equivalent regulatory streamlining within five years. Defense Production Act contracts direct capital toward ISR-ready projects in the Grants district. Community education programmes reduce social licence friction materially. First new ISR production from New Mexico reaches market by 2031 to 2033.

Scenario 2: Gradual Progress (Base Case)

Permitting timelines remain at seven to ten years under the existing dual-track NRC and state framework. Community engagement and ISR education programmes gradually reduce opposition. Aquifer exemption applications filed in the near term create a regulatory pipeline. First new production from the Grants district reaches market by 2033 to 2036.

Scenario 3: Regulatory Stagnation (Bear Case)

Federal-state coordination fails to materialise at a meaningful pace. New Mexico remains under direct NRC jurisdiction without streamlining. Permitting timelines extend beyond ten years. New Mexico uranium in situ recovery production remains negligible through the 2030s, consequently deepening import dependency and widening the domestic supply gap.

Key Indicators to Monitor

Investors and policymakers tracking New Mexico uranium in situ recovery development should focus on:

- Progress of aquifer exemption applications in the Grants district, which represent the most time-sensitive permitting milestone

- Completion of NI 43-101 compliant technical reports updating historic resource estimates using modern cutoff grade assumptions

- New Mexico state government positioning on uranium regulatory devolution and any movement toward agreement state status

- Defense Production Act contract awards to domestic ISR producers and the scale of committed procurement volumes

- Uranium spot price trajectory relative to the $100 per pound threshold that has historically preceded equity sector re-rating

- Announcements related to SMR HALEU fuel supply agreements, which would signal that the enrichment bottleneck is being addressed and pull forward upstream demand timelines

Disclaimer: This article is intended for informational and educational purposes only. Nothing contained herein constitutes financial or investment advice. Forecasts, scenario projections, and market analysis reflect current assessments based on publicly available information and are subject to change. Readers should conduct their own independent research and consult qualified financial advisers before making investment decisions. Past performance of commodities or equities is not indicative of future results.

Want to Know When the Next Major Uranium Discovery Hits the ASX?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries — including uranium — instantly cutting through complex data to surface actionable opportunities before the broader market reacts. Explore historic examples of major mineral discoveries and their returns on Discovery Alert's dedicated discoveries page, and start your 14-day free trial today to position yourself ahead of the next significant find.