July 20, 2026

Understanding the Current Nickel Market Rally: Key Economic Indicators

Global commodities markets face unprecedented volatility as structural supply constraints intersect with evolving demand patterns across critical industrial sectors. The current surge in nickel prices hit 15-month high levels demonstrates how copper-uranium investment strategies must adapt to rapidly changing market fundamentals. Furthermore, the interplay between monetary policy, geopolitical tensions, and resource nationalism creates complex investment landscapes where traditional market fundamentals compete with speculative capital flows.

Price Performance Metrics and Trading Volume Analysis

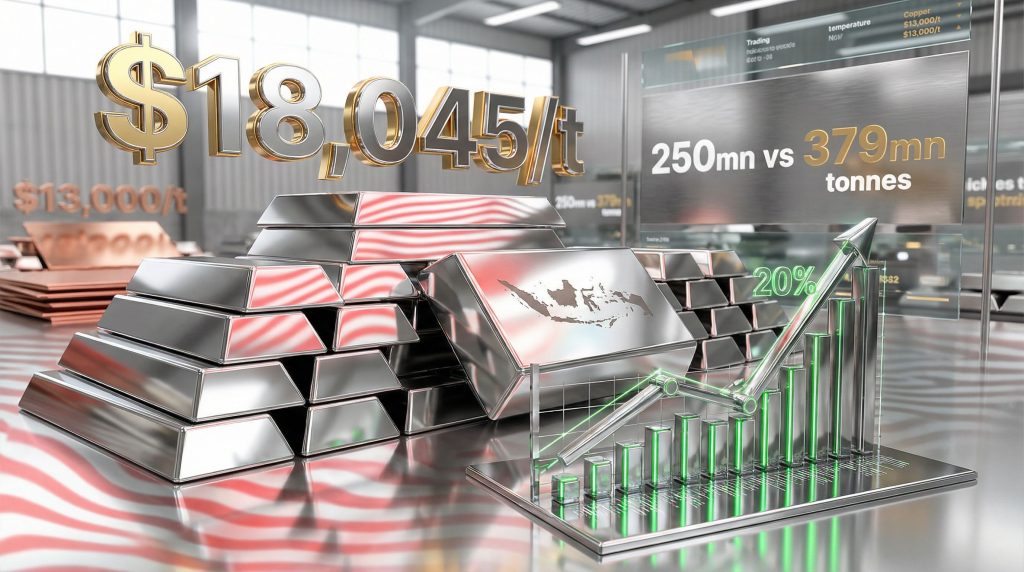

The London Metal Exchange witnessed a dramatic surge in nickel prices hitting $18,045 per tonne on January 6, 2026, marking the first time prices exceeded the $18,000 threshold in 15 months. This represented a substantial 7% single-day increase and culminated a remarkable 20% surge over just 12 trading sessions beginning December 17, 2025.

The Shanghai Futures Exchange responded with equal intensity, with nickel contracts hitting their 8% daily limit on January 6, demonstrating synchronised global price discovery mechanisms. This coordinated movement across major exchanges reflects deep structural shifts in market sentiment rather than isolated regional factors.

Historical analysis reveals the significance of this 15-month milestone. Previous cycles showing similar duration and magnitude typically coincided with major supply disruptions or fundamental shifts in industrial demand patterns driven by energy transition demand. The velocity of the current rally, achieving 20% gains in under three weeks, suggests underlying market imbalances that extend beyond typical seasonal variations.

Cross-Commodity Correlation Effects

The nickel rally coincided with copper's breakthrough above $13,000 per tonne, reaching new record highs and establishing a powerful cross-commodity momentum effect. Financial investors seeking alternatives to traditional precious metals have increasingly viewed base metals as viable safe-haven assets during periods of heightened geopolitical uncertainty.

"The synchronised movement between copper and nickel prices reflects a broader shift in investor psychology, where industrial metals are increasingly viewed as strategic assets rather than purely demand-driven commodities."

This correlation extends beyond simple price movements. Trading volumes across base metals sectors have increased substantially, with institutional investors allocating capital based on supply security concerns rather than immediate industrial consumption patterns. The arbitrage relationships between different metal exchanges have also compressed, indicating more efficient global price discovery mechanisms.

When big ASX news breaks, our subscribers know first

How Do Indonesian Supply Policies Shape Global Nickel Economics?

Indonesia's Market Dominance and Policy Tools

Indonesia's potential reduction of its nickel ore work plan and budget (RKAB) from 379 million tonnes in 2025 to 250 million tonnes in 2026 represents a 34% supply reduction that could fundamentally reshape global market dynamics. This policy shift occurs within the broader multipolar economic landscape where resource nationalism increasingly influences commodity markets.

Moreover, this occurs despite projections that Indonesian nickel ore consumption will increase to approximately 330 million wet metric tonnes in 2026, representing an 11% year-over-year increase.

| Policy Measure | 2025 Baseline | 2026 Target | Impact Scale | Market Response |

|---|---|---|---|---|

| RKAB Allocation | 379mn tonnes | 250mn tonnes | 34% reduction | Supply deficit creation |

| Domestic Consumption | 297mn wmt | 330mn wmt | 11% increase | Tighter export availability |

| Mining Licence Terms | 3-year duration | 1-year duration | Higher uncertainty | Operational volatility |

| Export Pricing Framework | Basic benchmarks | HPE/HR regulation | Cost escalation | Speculative positioning |

The Indonesian Trade Ministry's December 17 ministerial regulation on export benchmark pricing (HPE) and reference pricing (HR) for mining products has renewed market speculation about potential export tariffs. This regulatory framework provides the legal foundation for implementing cost-escalating measures that could significantly impact global nickel availability and pricing structures.

Supply-Demand Imbalance Projections

The mathematics of Indonesia's policy shift create compelling supply-side dynamics. With domestic consumption increasing by 11% while production allocations potentially decrease by 34%, the available export surplus faces dramatic compression. This structural imbalance extends beyond Indonesia's borders, as global consumers lack immediate alternative sources of equivalent scale and cost competitiveness.

Regional redistribution effects are already emerging, with processing facilities in China and other consuming markets beginning to evaluate supply diversification strategies. However, the lead times for developing alternative supply chains typically span multiple years, creating interim periods of market tightness that support elevated price levels.

Consequently, nickel prices hit 15-month high levels reflect not just speculative activity but genuine supply-side constraints that could persist throughout 2026.

What Are the Downstream Market Reactions to Nickel Price Volatility?

Stainless Steel Sector Price Transmission

The stainless steel industry has experienced rapid price transmission effects from the nickel rally. 304-grade cold-rolled coil prices increased from ¥12,800-12,900 per tonne ($1,829-1,843/t) on December 18, 2025, to ¥13,400-13,500 per tonne ($1,914-1,929/t) on January 7, 2026.

Chinese stainless steel mills have implemented multiple price adjustments to reflect rising input costs:

• ¥100 per tonne increase implemented on December 23, 2025

• ¥300 per tonne increase implemented on January 5, 2026

• Additional adjustments anticipated as nickel prices stabilise at elevated levels

These price adjustments demonstrate the steel industry's limited ability to absorb nickel cost increases through operational efficiency or inventory management. End-users have responded with accelerated purchasing decisions, concerned about further price escalation and seeking to secure material availability at current levels.

Battery Materials and EV Supply Chain Impacts

The electric vehicle supply chain faces particular challenges from nickel price volatility due to the metal's critical role in high-energy-density battery chemistries. Nickel sulfate pricing, essential for lithium-ion battery cathode production, maintains strong correlation with LME nickel movements, though with some lag effects due to processing and contracting mechanisms.

Battery manufacturers have implemented various risk management strategies:

• Strategic inventory accumulation during price dips

• Forward contracting to secure medium-term supply

• Alternative chemistry evaluation to reduce nickel intensity

• Vertical integration initiatives to control supply chain costs

These adaptations reflect the industry's recognition that nickel price volatility represents a structural challenge rather than temporary market disruption.

How Do Geopolitical Factors Amplify Commodity Price Movements?

Venezuelan Crisis and Safe-Haven Asset Flows

The capture of Venezuelan President Nicolas Maduro by US forces created immediate ripple effects across commodity markets, with metals experiencing particularly pronounced safe-haven capital inflows. This geopolitical development coincided with existing market tensions, amplifying price movements beyond levels justified by immediate supply and demand fundamentals.

Financial investors have increasingly utilised industrial metals as portfolio diversification tools during periods of political uncertainty. Unlike traditional safe-haven assets such as gold or treasury securities, base metals offer potential upside from both financial demand and underlying industrial consumption growth, creating more attractive risk-adjusted return profiles.

The platinum group metals experienced similar volatility patterns, confirming that the phenomenon extends beyond copper and nickel to encompass broader categories of strategically important materials. This trend suggests fundamental shifts in how institutional investors approach commodity allocation during crisis periods.

Trade Policy Uncertainty and Market Speculation

Indonesia's export pricing regulations have created significant uncertainty about potential tariff implementation, leading to speculative positioning across global trading firms. Market participants are evaluating various scenarios for how export taxes might be structured and implemented, with implications for long-term supply chain strategies.

The speculation extends to other major producing regions, as market participants assess whether Indonesia's policy approach might be replicated by other resource-rich nations seeking to capture greater value from their mineral endowments. This uncertainty premium has become embedded in forward pricing curves and option volatility structures, contributing to ongoing US‑China trade tensions that affect global commodity flows.

What Does Technical Analysis Reveal About Nickel's Price Trajectory?

Support and Resistance Level Analysis

The breakthrough above $18,000 per tonne represents a significant psychological and technical milestone for nickel markets. Historical analysis shows that when nickel prices hit 15-month high levels during periods of fundamental strength, they tend to establish new trading ranges rather than quickly reversing.

Volume analysis during the recent rally indicates broad-based participation rather than concentrated speculative activity. Average daily trading volumes increased substantially during the December-January price surge, suggesting genuine market conviction rather than thin-market manipulation.

Technical momentum indicators remain in strongly positive territory, though approaching levels that historically precede consolidation periods. The sustainability of current price levels will likely depend on whether fundamental supply-demand dynamics continue supporting elevated valuations.

Forward Curve Structure and Market Expectations

The nickel forward curve has shifted from contango to backwardation over recent trading sessions, indicating immediate supply tightness relative to future availability expectations. This structure typically emerges when physical market participants compete aggressively for near-term material while maintaining confidence that supply constraints are temporary.

Options markets reflect elevated volatility expectations, with implied volatility levels approaching those seen during previous major supply disruption events. However, the term structure of volatility suggests market participants expect eventual stabilisation rather than prolonged extreme price swings.

Which Economic Scenarios Could Drive Future Price Action?

Bullish Case Scenario Modelling

The most optimistic scenario for nickel prices combines Indonesia's full implementation of the 34% RKAB reduction with accelerated global electric vehicle adoption and limited alternative supply development. Under these conditions, nickel prices could establish a new trading range above $18,000 per tonne through 2026 and potentially beyond.

Additional supportive factors include:

• Accelerated energy storage system deployment requiring LFP battery chemistry

• Grid modernisation projects increasing industrial nickel consumption

• Supply chain regionalisation creating premium markets for non-Chinese material

• Central bank monetary easing supporting commodity prices generally

The combination of these factors could create a structural supply deficit lasting multiple years, as new mining projects typically require 3-5 years from development decision to commercial production. Furthermore, mining innovation trends suggest that technological advances alone cannot rapidly offset supply constraints.

Bearish Risk Assessment

Downside scenarios primarily centre on demand destruction from elevated prices and potential policy reversals in Indonesia. If nickel prices remain above $18,000 per tonne for extended periods, substitution effects could accelerate across multiple end-use applications.

Key bearish factors include:

• Recycling capacity expansion reducing primary demand

• Battery chemistry shifts toward lower nickel-content alternatives

• Economic slowdown reducing stainless steel consumption

• Indonesian policy flexibility allowing increased production if needed

• Alternative supply activation from previously uneconomic projects

The resilience of industrial demand at elevated price levels remains untested, creating uncertainty about sustainable long-term pricing.

The next major ASX story will hit our subscribers first

How Should Industrial Participants Navigate This Price Environment?

Risk Management Strategies for Consumers

Industrial consumers face complex decisions about hedging strategies in the current price environment. Traditional approaches focusing on price protection may prove inadequate given the potential for sustained elevated levels driven by structural supply constraints.

Recommended risk management approaches include:

• Layered hedging strategies combining physical and financial instruments

• Supply diversification beyond Indonesian sources where possible

• Inventory optimisation balancing carrying costs against price risk

• Long-term contracting to secure predictable supply costs

• Operational flexibility to adjust production based on input cost volatility

The key insight is that traditional hedging approaches may provide incomplete protection during periods of structural market imbalance, requiring more sophisticated risk management frameworks.

Investment Implications Across the Value Chain

Current price levels create compelling economics for primary nickel production investment, though project development timelines limit near-term supply response capability. Secondary processing and recycling operations face particularly attractive returns given the spread between primary material costs and processed product pricing.

Investment considerations across the value chain:

• Primary production: Robust economics but long development cycles

• Processing facilities: Immediate margin expansion opportunities

• Recycling operations: Accelerated payback periods from price spreads

• Downstream manufacturing: Margin pressure requiring operational adjustments

• Technology development: Increased focus on substitution and efficiency

What Are the Long-Term Structural Changes in Nickel Markets?

Energy Transition Demand Fundamentals

The global energy transition creates long-term structural demand growth for nickel, particularly in battery applications and grid infrastructure. Electric vehicle battery chemistry evolution generally favours higher energy density formulations that require significant nickel content, offsetting potential market share losses to lithium iron phosphate alternatives.

Grid-scale energy storage systems represent an emerging demand category with substantial growth potential. These applications typically utilise lithium iron phosphate chemistry requiring approximately 30-50% more lithium per kilowatt-hour than nickel-rich alternatives, but grid modernisation also drives demand for nickel-containing electrical infrastructure components.

The competition between battery chemistries creates complex demand projections, as cost-performance tradeoffs vary significantly across different applications and market segments.

Supply Chain Regionalisation Trends

Western governments increasingly prioritise domestic or allied-nation supply chain development for critical materials, including nickel. These initiatives typically involve higher costs than Indonesian production but offer supply security benefits that justify premium pricing structures.

Key regionalisation trends include:

• North American supply chain integration linking Canadian resources with US processing

• European strategic autonomy initiatives reducing dependence on single-source suppliers

• Technology transfer programmes developing processing capabilities in consuming regions

• Strategic inventory systems providing buffer stocks during supply disruptions

These developments could create multi-tiered global markets with different pricing structures for strategically secure versus commodity-grade material.

Positioning for Nickel Market Evolution

Key Takeaways for Market Participants

The current nickel market environment reflects the intersection of short-term supply policies with long-term structural demand growth. Indonesia's potential 34% RKAB reduction combined with 11% domestic consumption growth creates immediate supply constraints, while energy transition applications provide sustained demand growth prospects.

Market participants should recognise that the recent surge where nickel prices hit 15-month high represents more than cyclical price recovery. The underlying dynamics suggest potential for establishing new price ranges that reflect structural scarcity premiums rather than temporary market imbalances.

Strategic positioning requires balancing immediate price risk management with longer-term supply security considerations. The organisations that successfully navigate this environment will likely combine sophisticated risk management with strategic supply chain investments, recognising that traditional market relationships may prove inadequate during periods of fundamental transformation.

Disclaimer: This analysis contains forward-looking assessments based on current market conditions and policy expectations. Actual outcomes may differ materially due to changes in government policies, economic conditions, or unforeseen market developments. Commodity investments carry substantial risk and may not be suitable for all investors.

Looking to Capitalise on the Next Major Nickel Discovery?

Discovery Alert's proprietary Discovery IQ model delivers instant notifications on significant ASX mineral discoveries, including critical metals like nickel that are driving the current market rally. With nickel prices hitting 15-month highs and structural supply constraints creating compelling investment opportunities, subscribers gain immediate insights into actionable trading prospects ahead of the broader market. Begin your 30-day free trial today and secure your competitive advantage in the rapidly evolving commodities sector.