July 15, 2026

When Benchmark Frequency Signals More Than Scheduling

In commodity markets, the cadence at which a price benchmark is published carries meaning far beyond administrative convenience. Publication frequency is a direct reflection of underlying market liquidity, data quality, and the confidence a price reporting agency (PRA) places in each assessment's representativeness. When a benchmark shifts from weekly to fortnightly, it is not a retreat — it is a recalibration that tells a more honest story about how a market is actually functioning.

That dynamic is now playing out in the nickel sulfate cif Japan and Korea pricing notice issued by Fastmarkets in May 2026, which proposes to reduce the publication frequency of two key battery-grade nickel sulfate assessments. The change offers a revealing window into the current state of Northeast Asia's battery materials markets, the structural forces reshaping how supply chains procure critical inputs, and what these shifts mean for everyone from procurement managers to commodity traders.

When big ASX news breaks, our subscribers know first

Understanding the Two Assessments at the Centre of This Change

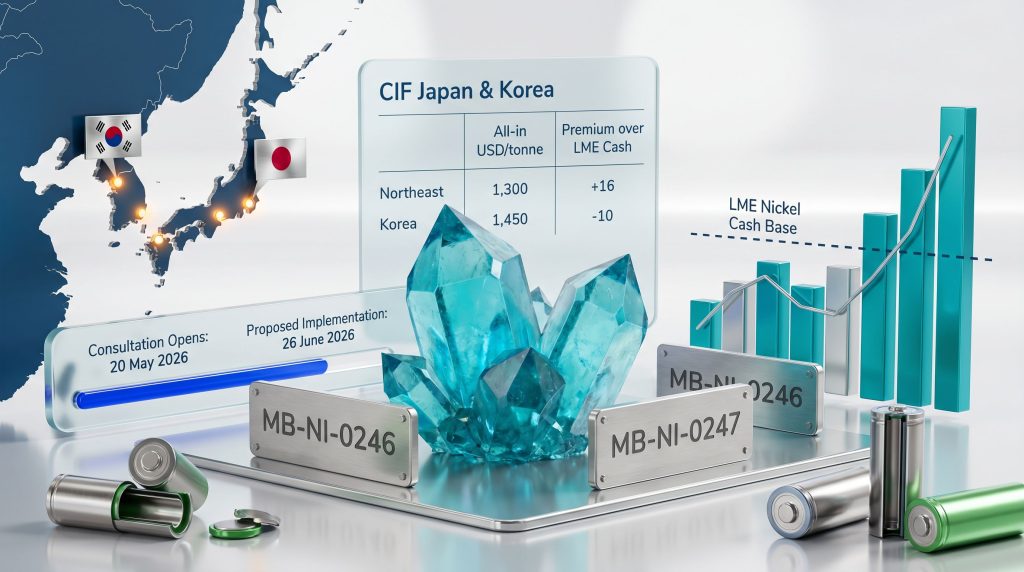

The Fastmarkets proposal specifically targets two price codes that together form the backbone of battery-grade nickel sulfate pricing for the Japan and Korea corridor:

- MB-NI-0246 captures the all-in delivered price for nickel sulfate, expressed in USD per tonne on a CIF basis to major ports in Japan and South Korea.

- MB-NI-0247 isolates the premium component above the weekly average LME nickel cash price, allowing supply chain participants to separate underlying metal exposure from the processing and logistics value-add.

Both assessments share the same quality specification framework. Battery-grade nickel sulfate must meet the following criteria to be eligible for inclusion:

| Parameter | Specification |

|---|---|

| Nickel content (base maximum) | 22.3% |

| Nickel content (minimum) | 22.0% |

| Cobalt impurity threshold | 50 ppm maximum |

| Minimum transaction quantity | 1 tonne |

| Delivery window | Within 60 days |

| Delivery location | CIF major ports, Japan and Korea |

| Publication window | 5-6 pm China Standard Time |

The CIF delivery term is worth examining closely. Under CIF (Cost, Insurance, and Freight) pricing, the seller is responsible for all costs associated with transporting goods to the named destination port, including freight and marine insurance. For battery material buyers in Japan and South Korea, this creates a true landed-cost reference point that eliminates the need to calculate origin-specific logistics separately. It makes the benchmark practical for real procurement decisions, not just theoretical market monitoring.

Furthermore, the battery raw materials market context surrounding these assessments is shifting rapidly, adding further urgency to understanding how these benchmarks are constructed and applied.

A critical but underappreciated detail: the cobalt impurity cap of 50 parts per million is not arbitrary. Elevated cobalt in nickel sulfate can disrupt the stoichiometric balance in precursor cathode active material (pCAM) synthesis, creating costly quality deviations further down the battery cell manufacturing chain. Specification discipline at the feedstock level has measurable consequences for end-product battery performance.

Why Fortnightly? Reading the Signal Behind the Scheduling Change

The proposed amendment moves both MB-NI-0246 and MB-NI-0247 from once-weekly to once-fortnightly publication. The consultation timeline is as follows:

- Consultation opens: Wednesday, 20 May 2026

- Consultation closes: Thursday, 18 June 2026

- Proposed implementation date (subject to feedback): Friday, 26 June 2026

Fastmarkets has cited inactive spot liquidity and low price volatility in the Japan and Korea nickel sulfate corridor as the primary drivers. This reasoning has significant methodological weight. Under the IOSCO Principles for Financial Benchmarks, to which major PRAs are expected to adhere, a benchmark must be anchored to observable, verifiable transaction data. When spot volumes are insufficient to generate meaningful price signals on a weekly basis, continuing weekly publication risks creating what practitioners sometimes call false precision — a specific number that implies granular price discovery where none actually exists.

This is not a hypothetical concern. In thinly traded specialty chemical markets, a single transaction or even a single indicative quote can distort a weekly assessment far beyond what the underlying market would support. Fortnightly aggregation smooths this risk by widening the data collection window, improving the statistical robustness of each published number.

Structural Reasons Behind Softening Spot Activity

The reduction in observable spot transactions is not random. However, several structural forces are systematically pulling nickel sulfate procurement away from open-market spot buying:

- Long-term offtake agreements now dominate procurement strategy among major Japanese and Korean cathode manufacturers, reducing the frequency of spot transactions that would otherwise feed benchmark data pools.

- Vertical integration by large battery cell producers has shortened the visible portion of the supply chain. When a battery manufacturer sources nickel sulfate from a captive HPAL facility, no open-market transaction occurs, and price reporting databases capture nothing.

- Demand-side chemistry shifts within the region are also relevant. While high-nickel NCM (nickel-cobalt-manganese) chemistries remain prevalent in South Korean battery manufacturing, the broader regional market is navigating a competitive tension with lithium iron phosphate (LFP) chemistries, which require no nickel sulfate at all. This constrains the growth trajectory of nickel sulfate spot demand.

Battery chemistries are not static. The ongoing commercial contest between high-nickel NCM and LFP is one of the most consequential long-term variables for nickel sulfate demand. Any scenario in which LFP adoption accelerates beyond current projections in the Japanese or Korean markets would structurally depress spot nickel sulfate volumes for years.

The Northeast Asia Demand Hub: Japan and Korea in Context

Japan and South Korea occupy a unique position in the global battery materials ecosystem. These two countries are home to some of the world's most technically sophisticated cathode active material (CAM) and precursor PCAM manufacturers, including operations supplying cells destined for electric vehicles produced across North America, Europe, and Asia.

Supply into this corridor is increasingly dominated by Indonesian-origin nickel sulfate produced via High-Pressure Acid Leach (HPAL) processing. HPAL technology extracts nickel and cobalt from low-grade laterite ores using high-temperature, high-pressure sulphuric acid digestion — a capital-intensive but scalable process that Indonesia has deployed at significant scale. The Indonesian nickel industry has expanded rapidly through this technology, and the CIF Japan and Korea pricing structure naturally incorporates Indonesian freight economics, making Busan and other Korean ports key normalisation anchors in the assessment methodology.

The geographic concentration of HPAL capacity in Indonesia introduces a supply-chain concentration risk that procurement teams in Japan and Korea are increasingly aware of. In addition, Indonesian nickel price trends have played a meaningful role in shaping the delivered cost dynamics that feed directly into CIF assessments. Origin diversification is consequently a growing strategic priority, but alternatives remain limited in scale.

How the CIF Japan and Korea Assessments Fit Into the Global Pricing Landscape

The Fastmarkets assessments do not exist in isolation. The battery-grade nickel sulfate pricing ecosystem now features competing benchmarks from multiple PRAs, each with distinct methodological approaches:

| Assessment | Publisher | Region | Frequency | Structure |

|---|---|---|---|---|

| MB-NI-0246 (proposed) | Fastmarkets | CIF Japan & Korea | Fortnightly | All-in USD/tonne |

| MB-NI-0247 (proposed) | Fastmarkets | CIF Japan & Korea | Fortnightly | Premium over LME cash |

| NiSO₄ Premium CIF NE Asia | S&P Global (Platts) | Northeast Asia | Daily | Premium over LME nickel cash |

| European Nickel Sulfate Premium | Various | Europe | Periodic | Premium structure |

The contrast between Fastmarkets' fortnightly cadence and Platts' daily NiSO₄ assessment reflects different market coverage philosophies and data availability assumptions. Daily assessments carry high utility for traders using the benchmark as a basis for financial derivatives or short-cycle spot contracts, but they require a continuous flow of verifiable market data to remain credible. In the CIF Japan and Korea corridor specifically, that data density does not currently exist at daily frequency — making Fastmarkets' fortnightly proposal arguably a more methodologically honest representation of actual market conditions.

Regional divergence in nickel sulfate pricing is also accelerating at a structural level. The United States' Inflation Reduction Act (IRA) has introduced origin-based eligibility criteria that are generating measurable price differentials between materials sourced from IRA-compliant and non-compliant jurisdictions. While this primarily affects materials destined for the North American market, it is reshaping global supply routing decisions in ways that eventually feed back into CIF pricing dynamics across all regions. Furthermore, nickel price momentum in 2025 has established important baseline conditions against which these regional divergences are being measured.

Practical Implications for Market Participants

For Procurement and Contracting Teams

A shift to fortnightly publication changes the reference architecture for contract indexation. If a supply agreement currently specifies weekly price resets tied to MB-NI-0246 or MB-NI-0247, the new publication cadence will require renegotiation of indexation clauses. Procurement managers should audit existing contracts now, well ahead of the 26 June 2026 implementation date, to identify where adjustments are needed.

For Traders and Hedging Operations

The premium assessment (MB-NI-0247) is particularly relevant for traders managing basis risk between physical nickel sulfate positions and LME nickel cash hedges. A widened publication interval means basis will only be formally reset every two weeks rather than weekly. In low-volatility environments this is manageable, but any unexpected supply disruption or currency move during a fortnightly window could create meaningful unhedged exposure. Traders should consequently factor this into their risk limits and margin buffers.

For Data Submitters

The consultation process represents a direct opportunity to influence benchmark specifications that govern significant contract value across the Northeast Asian battery materials supply chain. Participants with relevant market intelligence are encouraged to engage. Feedback can be submitted to pricing@fastmarkets.com and basemetals@fastmarkets.com, using the subject line Re: Nickel sulfate cif Japan and Korea prices. The deadline is 18 June 2026. Respondents should indicate whether comments are confidential.

Under IOSCO-aligned consultation protocols, price reporting agencies are required to consider all substantive feedback before finalising benchmark amendments. Market participant engagement in these processes is not merely symbolic — documented commercial objections or alternative data submissions have historically influenced whether proposed changes proceed as drafted, are modified, or are withdrawn entirely.

The next major ASX story will hit our subscribers first

Frequently Asked Questions

What does the CIF Japan and Korea delivery term mean in practice?

CIF means the seller covers all costs to deliver the nickel sulfate to the named port in Japan or South Korea, including sea freight and marine insurance. The buyer assumes risk from the point of loading, but the price they receive already reflects full delivery cost to their region. This makes CIF assessments directly usable as procurement benchmarks without additional freight adjustments.

Why does the premium assessment (MB-NI-0247) matter separately from the all-in price?

The premium isolates the value attributed to nickel sulfate production, processing quality, and logistics above and beyond the raw metal value tracked by LME nickel cash pricing. This separation allows cathode manufacturers to use LME-based instruments to hedge their underlying nickel exposure while separately tracking — and negotiating — the supply-chain premium component. In a falling LME environment, a stable premium signals that market participants still attribute meaningful value to the conversion and logistics function, which is commercially significant information in its own right.

What does fortnightly publication mean for price transparency?

In genuinely liquid markets, reducing publication frequency would reduce price transparency. In thin spot markets like the current Japan and Korea nickel sulfate corridor, however, the opposite logic applies. A fortnightly benchmark grounded in a fuller sample of observable transactions is more transparent than a weekly number constructed from sparse or estimated data. The change improves the integrity of the benchmark rather than diminishing it.

What This Benchmark Change Reveals About Battery Market Maturity

The nickel sulfate cif Japan and Korea pricing notice from Fastmarkets is, on its surface, a routine administrative proposal. At a deeper level, it reflects a battery materials market that is growing up. Spot market activity is giving way to long-term contracts and vertically integrated supply chains. Price discovery is becoming less frequent but more structurally meaningful.

The accelerating transition to electric vehicles, driven in part by battery storage expansion across global markets, is fundamentally reshaping the demand environment these benchmarks must serve. Regional benchmarks are consequently diverging to reflect genuinely distinct supply, demand, and policy environments.

For companies operating in the cathode materials value chain — whether as nickel sulfate producers, precursor manufacturers, battery cell makers, or commodity traders — understanding the mechanics and evolution of these benchmarks is not optional. The numbers published in these assessments flow directly into procurement contracts, hedging strategies, and investment valuations. The proposal to move to fortnightly publication is ultimately a message from the market itself: the nature of price discovery in battery-grade nickel sulfate is changing, and the benchmarks that serve it must change with it.

This article contains forward-looking references and analysis of proposed benchmark amendments that remain subject to market consultation outcomes. Nothing in this article constitutes financial, investment, or legal advice. Readers should conduct independent due diligence appropriate to their specific commercial circumstances.

Want To Stay Ahead Of The Next Major Mineral Discovery On The ASX?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, instantly translating complex commodity data across more than 30 sectors into clear, actionable insights for traders and investors alike — explore the historic returns major discoveries have generated and begin your 14-day free trial at Discovery Alert to secure your market-leading edge.