May 14, 2026

The Structural Scarcity Driving Capital Back Into Nickel Sulfide Development

In commodity markets, scarcity is not always visible until capital starts moving. For most of the past three years, nickel has been a sector investors preferred to avoid, weighed down by a structural oversupply narrative driven almost entirely by Indonesian nickel supply scaling at pace. But market dynamics rarely hold in one direction indefinitely, and the forces now reshaping nickel supply chains are creating a very different investment landscape heading into the second half of the 2020s.

Nickel price momentum has seen prices recover close to US$5,000 per tonne from their December 2025 lows, and institutional capital that disappeared from the sector years ago is returning with renewed intent. The problem facing that returning capital is a stark one: there are roughly 200 gold development stories, 150 silver stories, and 100 copper stories actively competing for attention in the market today, but only approximately six meaningfully advanced nickel projects exist globally, with perhaps another six requiring significant additional development work before they can be taken seriously.

When investor conviction concentrates into such a constrained opportunity set, the projects that are genuinely construction-ready carry outsized strategic value. The Canada Nickel Crawford project permit and financing story sits at the precise intersection of these forces, representing one of only approximately three nickel projects worldwide with a credible pathway to production before 2030.

When big ASX news breaks, our subscribers know first

Crawford by the Numbers: Scale, Location, and Why Ontario Matters

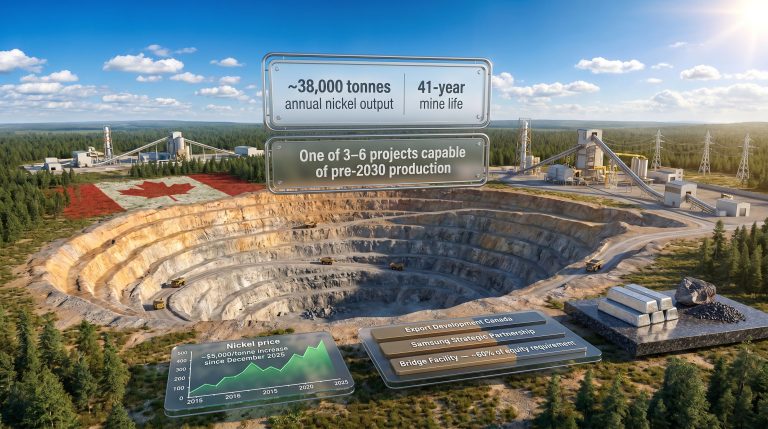

Located 42 kilometres north of Timmins, Ontario, Crawford is an open-pit nickel-cobalt sulfide deposit with technical characteristics that position it as a globally significant development asset. The project targets annual nickel production of approximately 38,000 to 42,000 tonnes, supported by a mill with a throughput capacity of 120,000 tonnes per day and a mine life estimated at 41 years.

These operational parameters alone would attract attention. However, what elevates Crawford beyond raw scale is the energy infrastructure surrounding it. Ontario operates one of the lowest-carbon electricity grids in North America, drawing predominantly from nuclear and hydroelectric generation. Crucially, the province is currently expanding its nuclear capacity by over 10,000 megawatts, a capital commitment that will further reduce the grid's embodied carbon intensity over the coming decades.

For a nickel project with a 41-year mine life, this trajectory matters enormously, as the carbon footprint of Crawford's output will improve continuously as the grid decarbonises.

| Metric | Detail |

|---|---|

| Location | 42 km north of Timmins, Ontario |

| Deposit Type | Open-pit nickel-cobalt sulfide |

| Target Annual Production | ~38,000 to 42,000 tonnes nickel |

| Mine Life | 41 years |

| Mill Throughput Capacity | 120,000 tonnes per day |

| Energy Grid | Ontario nuclear and hydroelectric |

| Ontario Nuclear Expansion | Over 10,000 megawatts planned |

| Primary End Markets | EV battery supply chains, specialty steel, European decarbonisation |

The nickel sulfide advantages over laterite deposits are worth understanding for investors less familiar with the sector. Sulfide deposits typically offer metallurgical benefits during processing, requiring less energy-intensive refining steps compared to laterite ore. This translates directly into lower processing emissions per tonne of finished nickel, a characteristic that carries increasing commercial value as downstream buyers face carbon accounting obligations and sustainability reporting requirements.

Canada's 2019 Impact Assessment Act: What It Demands and Why Crawford's Progress Is Unprecedented

Understanding the Regulatory Architecture

The 2019 Impact Assessment Act replaced Canada's previous Canadian Environmental Assessment Act and introduced a materially broader assessment mandate. Where the previous legislation focused primarily on environmental compliance, the IAA now requires projects to demonstrate positive outcomes across environmental, health, social, economic, and Indigenous rights dimensions simultaneously.

Any project moving more than 5,000 tonnes of material per day is subject to federal review under this framework. Crawford, with its 120,000-tonne-per-day throughput, sits well above this threshold. Consequently, the critical context here is that Crawford is the first mining project in Canada to advance to final permitting under the 2019 IAA, according to Canada Nickel's project updates.

Every project that initiated development after 2019 falls under this legislation, yet none has progressed this far. That absence of precedent means Crawford's team has been navigating genuinely uncharted regulatory territory, with no comparable project's experience to benchmark against.

The Permitting Timeline: From Submission to Draft Report

| Date | Milestone | Significance |

|---|---|---|

| November 2024 | Impact Statement submitted to IAAC | Over 20,000 pages filed covering environmental, social, and Indigenous Knowledge dimensions |

| May 2025 | IAAC technical review comments issued | Public comment period completed |

| December 2025 | Canada Nickel formal response submitted | Response to IAAC technical review comments |

| March 3, 2026 | Impact Statement phase concluded; Impact Assessment phase commenced | IAAC confirmed all IAA subsection 19(1) requirements met |

| May 12, 2026 | Draft Impact Assessment Report published | Preliminary conclusions and proposed permit conditions released; 30-day public consultation opened |

| Target: Early to Mid Summer 2026 | Final permit issuance | Minister of Environment and Climate Change to sign following IAAC final report |

The volume of documentation filed alone illustrates the complexity of the process. The impact statement submission exceeded 20,000 pages, incorporating environmental studies, Indigenous engagement records, technical engineering data, and stakeholder consultation outcomes. Filing this under a legislative framework with no mining project precedent required the team to interpret and apply regulatory requirements without comparable guidance.

What Happens Between Draft Report and Final Permit?

The pathway from the May 12, 2026 draft report to final permit issuance follows a defined sequence:

- A 30-day public consultation window allows registered participants to respond to the proposed permit conditions published in the draft report.

- The Impact Assessment Agency of Canada consolidates feedback and prepares its final recommendations.

- The finalised report is submitted to the Minister of Environment and Climate Change, who issues the formal permit decision.

- Upon ministerial sign-off, the permit is formally issued.

Canada Nickel has indicated satisfaction with the conditions as published in the draft, an important signal that no material objections or unexpected requirements emerged from the assessment process. Furthermore, as noted by industry analysts, Crawford clearing this penultimate federal hurdle marks a significant milestone for the broader Canadian mining sector.

The 2019 Impact Assessment Act is considerably more demanding in scope than its predecessor, particularly in the areas of social engagement and First Nations consultation. Crawford's navigation of this framework in approximately four years, despite funding constraints that extended the timeline, demonstrates that regulatory rigour and processing efficiency are not fundamentally incompatible goals.

How the Regulatory Landscape Has Changed: Federal-Provincial Coordination

One of the less-discussed but strategically significant aspects of Crawford's permitting journey is what it reveals about the evolution of Canada's regulatory coordination architecture. When Crawford entered the process, the federal and Ontario provincial environmental assessment regimes operated as separate, parallel tracks. This created the possibility of duplicated requirements, conflicting timelines, and the inefficiencies that historically made Canadian mining permitting unpredictable.

Crawford navigated both tracks concurrently, a structural reality that added considerable complexity to an already demanding process. Since then, however, formal cooperation agreements have been established between the federal government and most individual provinces, enabling unified, co-authored permit processes for future applicants. A project submitting today would receive a single combined federal-Ontario assessment rather than two separate processes running in parallel.

The practical consequence of Crawford's permitting success is visible in this evolution. The absence of any material objections from Ontario reflected in the draft permit conditions confirms that federal-provincial alignment on Crawford's approval has effectively already occurred.

Proposed legislation discussed in mid-2026 aims to compress future permitting timelines to as little as one year for qualifying projects, a reduction that would be transformative for the economics of mine development in Canada if implemented. Whether this ambition translates into enacted legislation remains to be seen, but the directional shift in regulatory philosophy is clear.

The Financing Architecture: Building a $2 Billion Capital Stack

How the Package Is Structured

Crawford's capital structure is deliberately engineered to minimise equity dilution by prioritising government-backed debt, refundable tax credits, and strategic equity partnerships over conventional equity raises. The total capital requirement for Phase 1 construction is estimated at approximately $1.9 to $2.5 billion CAD.

| Financing Component | Provider | Amount | Status |

|---|---|---|---|

| Long-term senior debt | Export Development Canada (EDC) | Up to US$500M | Letter of Intent signed August 2024; independent engineer review completed |

| Co-lender debt facility | Unnamed financial institution | Up to ~US$500M+ | Support letter issued September 2024 |

| Bridge facility (tax credit monetisation) | 3 to 4 competing groups | ~60% of equity requirement | Target announcement September to October 2026 |

| Strategic equity and offtake | Samsung | US$100M option for 10% equity and 30% offtake | Active and ongoing |

| Refundable tax credits | Canadian federal government | Over US$600 to 815M | First tranche targeted before end of June 2026 |

| Bridge financing | Auramet | Facility extended to August 9, 2026 | Active |

| Financial advisors | Deutsche Bank, Scotiabank, Cutfield Freeman | Full package assembly | Targeting completion summer 2026 |

The Tax Credit Bridge: The Most Underappreciated Component

Canada's refundable tax credit programmes for critical minerals production and carbon capture represent one of the largest sources of non-dilutive capital available to a project like Crawford. The combined estimated value of these credits exceeds US$600 to 815 million, and their refundable nature means they function as guaranteed government payments rather than contingent tax offsets.

The bridge facility against these credits is consequently a highly attractive proposition for institutional lenders. Three to four separate groups are currently competing to provide this bridge, a level of competition that reflects strong institutional confidence in both the credits' availability and Crawford's eligibility. This bridge is expected to cover approximately 60% of the total equity capital required for Phase 1 construction, substantially reducing the quantum of equity that needs to be sourced from capital markets.

Mark Selby, CEO of Canada Nickel, has framed the near-term equity requirement as minimal, describing anticipated equity raises of approximately $10 to $15 million at a time, which at current share prices represents roughly 2% dilution. The explicit strategic intent is to use government capital to protect shareholder value rather than resort to the large equity placements that can destroy value in project development companies.

The management team has been direct about the financing philosophy: some companies rush to build and execute equity raises representing 50% to 100% of their market capitalisation. The approach at Crawford prioritises waiting for government capital tranches to materialise, accepting short-term timeline delays in exchange for substantially lower long-term dilution.

Export Development Canada: What the Independent Engineer Review Unlocks

EDC's Letter of Intent, signed in August 2024, established a framework for up to US$500 million in long-term debt financing. A prerequisite for advancing to formal debt negotiations was the completion of an independent engineer review, which has now been successfully completed. With this review in hand, Canada Nickel has re-entered active negotiations with EDC on final debt terms.

Importantly, additional export credit agencies from other jurisdictions have expressed parallel interest in participating in the debt syndicate. This multi-agency interest creates competitive dynamics that may ultimately improve terms for the project.

Samsung's Strategic Logic: Supply Chain Sovereignty Over Price Optimisation

Samsung's US$100 million option for a 10% equity stake and 30% offtake represents a supply chain diversification strategy rather than a conventional financial investment. Crawford is one of only approximately three projects globally capable of delivering nickel into the market before 2030, and for a battery manufacturer heavily dependent on Indonesian supply, that scarcity has strategic value that transcends short-term commodity price movements.

Furthermore, in the context of battery metals investment, Samsung's continued engagement through a period of challenging nickel prices signals long-term conviction about Crawford's role in their supply chain, not opportunistic positioning driven by current market conditions.

End Markets: Why Europe Is as Important as North America

Two Product Streams, Two Market Pathways

Crawford's process plant produces two distinct output streams with separate commercial pathways:

- Nickel concentrate, refined into battery-grade or specialty steel nickel products for EV supply chains and industrial applications.

- Magnetite concentrate containing nickel and chromium, converted into semi-finished specialty steel products for European and North American downstream processors.

This dual-stream structure gives Crawford commercial flexibility that single-product projects lack, allowing it to direct output toward whichever market offers the most favourable economics at any given time.

The European Carbon Border Adjustment Mechanism Opportunity

The EU's Carbon Border Adjustment Mechanism creates a structural cost disadvantage for European steel producers still operating blast furnaces dependent on fossil fuel or coal-powered electricity grids. For specialty steel producers using nickel and chromium, this regulatory cost will escalate systematically over the next decade as CBAM coverage expands.

Crawford's ultra-low-carbon production profile, powered by Ontario's nuclear and hydroelectric grid, positions it as a natural supplier to European producers seeking to reduce the embodied carbon in their feedstock materials. Furthermore, the role of nickel and energy transition objectives means management estimates that approximately half to two-thirds of Crawford's steel-related output could ultimately be directed into European downstream processing operations.

This is a more nuanced commercial story than the simple battery metals narrative that typically drives nickel coverage. Crawford is, in practical terms, functioning as a decarbonisation supply chain asset for European specialty steel producers facing escalating regulatory carbon costs.

The North American Incremental Capacity Argument

In the US steel market, Crawford fills a different but equally structural need. Existing furnace operators requiring incremental throughput capacity face a capital constraint: new blast furnace construction is not economically divisible. You cannot build one-third of a furnace to satisfy one-third of an incremental capacity requirement.

Crawford's output can consequently serve as top-up feedstock for existing US operators who need additional throughput without committing to full greenfield capital expenditure, positioning the project's steel-related stream as a flexible, demand-responsive supply source for North American industrial buyers.

The next major ASX story will hit our subscribers first

Technical Readiness: What Remains Before Construction Begins

Engineering Completion and Long-Lead Procurement

Crawford's technical development is, by management's assessment, complete. The Ausenco feasibility study published in November 2023 represents the project's engineering baseline, and the team characterises the project as being in a ready-to-order-long-lead-items state, pending only capital deployment.

The two immediate long-lead procurement priorities are:

- Hydroelectric power connection, already announced and classified as a long-lead item requiring advance ordering.

- Electrical equipment, specifically transformers and high-voltage switchgear, which carry chronically extended delivery timelines across the mining and energy sectors globally.

The second category warrants particular attention. Transformer procurement lead times have been structurally extended for several years, and the current wave of AI data centre construction is competing directly for the same electrical equipment supply chains. Management has indicated that initial government funding tranches will be directed immediately toward securing order positions for this equipment.

The Sequential Construction Decision Pathway

- Federal permit issued (target: early to mid summer 2026)

- First government funding tranche received (target: before end of June 2026)

- Tax credit bridge facility announced (target: September to October 2026)

- EDC debt terms finalised (target: summer to fall 2026)

- Full financing package assembled (target: summer 2026)

- Long-lead equipment orders placed (immediately post-funding)

- Formal construction decision (target: early to mid 2027)

- First production (potentially achievable 2028 to 2029)

The Broader District Strategy: Crawford as a Starting Point, Not an Endpoint

A Pipeline of Assets Beyond the First Project

A detail that frequently gets overlooked in coverage of the Canada Nickel Crawford project permit and financing progress is that management explicitly frames Crawford as the first development in a multi-asset district strategy, not the company's ultimate ceiling. The broader portfolio spans several stages of advancement:

- Nesbitt deposit: Smaller in scale than Crawford but described as still commercially meaningful in absolute terms.

- Reed project: Under active evaluation for a Preliminary Economic Assessment, characterised by lower strip ratios, reduced overburden, and more consistent serpentinisation, which improves metallurgical recovery rates.

- Additional properties: Several assets at various resource definition stages, with resource updates anticipated in the near term.

Serpentinisation is a geological process worth explaining for less technical readers. When ultramafic rocks undergo serpentinisation, the mineralogy changes in ways that can improve how efficiently nickel is liberated and recovered during processing. More consistent serpentinisation across an ore body reduces metallurgical variability, which simplifies process plant design and improves recovery rate predictability.

Management has stated directly that three to four projects in the pipeline are expected to ultimately be larger and of higher quality than Crawford itself. However, the challenge is sequencing: with permitting timelines measured in years, Crawford must be fully de-risked before capital and management bandwidth can rotate to the next asset.

The Global Nickel Supply Narrative and Crawford's Competitive Position

How Few Investable Projects Actually Exist

The competitive landscape for advanced nickel development projects is genuinely narrow. Globally, fewer than a dozen projects have achieved meaningful development advancement, and of those, only approximately three can realistically reach production before 2030. This contrasts sharply with the hundreds of stories competing for attention in gold, silver, and copper.

When institutional capital rotates back into nickel with conviction, it must concentrate into a very small number of assets. The projects that are genuinely advanced, permitted, and financed when that rotation occurs will absorb disproportionate attention and capital flows.

Indonesian Supply Management and Its Structural Implications

Indonesia's ongoing management of its nickel export and processing policies has created persistent uncertainty for downstream buyers dependent on Indonesian supply. Any tightening of export policy would directly benefit projects offering Western-jurisdiction, non-Indonesian supply with stable regulatory environments.

Crawford is not competing with Indonesian nickel purely on production cost. Instead, it is competing on supply chain security, carbon credentials, and jurisdictional predictability — characteristics that carry increasing commercial value for both industrial buyers managing supply chain risk and ESG-mandated institutional investors with carbon accounting obligations.

Frequently Asked Questions: Crawford Permit and Financing

What Is the Current Status of Crawford's Federal Environmental Permit?

The draft Impact Assessment Report was published on May 12, 2026. A 30-day public consultation period is underway, after which the IAAC will finalise its report and submit it to the Minister of Environment and Climate Change for the formal permit decision, expected in early to mid summer 2026.

How Much Will It Cost to Build the Crawford Nickel Project?

The total capital requirement for Phase 1 is estimated at approximately $1.9 to $2.5 billion CAD, comprising roughly $1.5 billion in debt and $1 billion in equity, partially offset by more than US$600 to 815 million in refundable federal tax credits.

Who Is Financing the Crawford Project?

The financing syndicate includes Export Development Canada at up to US$500 million, a second unnamed financial institution at up to approximately US$500 million, Samsung through strategic equity and offtake, competing bridge facility providers for tax credit monetisation, and financial advisors Deutsche Bank, Scotiabank, and Cutfield Freeman managing the broader capital raise.

When Could Crawford Begin Construction?

Subject to permit receipt in summer 2026 and full financing package completion, a formal construction decision is targeted for early to mid 2027, with first production potentially achievable in 2028 to 2029.

Why Is Crawford Significant Beyond Canada?

Crawford is one of the largest undeveloped nickel sulfide deposits in the world, one of only three projects globally capable of producing before 2030, and a critical supply chain alternative to Indonesian laterite nickel for European and North American battery and steel industries.

What Makes Crawford's Carbon Footprint Comparatively Low?

Crawford operates within Ontario's electricity grid, powered predominantly by nuclear and hydroelectric generation, among the lowest-carbon grids in North America. Ontario is also expanding nuclear capacity by over 10,000 megawatts, further improving Crawford's long-term carbon profile across its 41-year mine life.

What Is the Reed Project and Why Does It Matter?

Reed is a separate deposit within Canada Nickel's broader district portfolio, characterised by lower strip ratios, reduced overburden, and more consistent serpentinisation compared to Crawford. These geological characteristics suggest potentially superior recovery economics. A Preliminary Economic Assessment is under consideration to demonstrate the pipeline's value to the market before Crawford construction begins.

This article contains forward-looking statements and market analysis based on publicly available information and management commentary. It does not constitute financial advice. Commodity prices, regulatory timelines, and financing outcomes are subject to change. Investors should conduct their own due diligence before making investment decisions.

Want To Be First When The Next Major Nickel Discovery Hits The ASX?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries — including battery metals like nickel — instantly translating complex data into actionable opportunities for both short-term traders and long-term investors. Explore historic discoveries and their returns, then start your 14-day free trial to position yourself ahead of the market before the next major find is announced.