May 15, 2026

The Geography of Nickel Power: Why Southeast Asia Now Sets the Global Price

Critical minerals rarely follow the same geographic logic as oil. Unlike petroleum, which is distributed across multiple continents and dozens of producing nations, nickel has spent the last decade consolidating its supply base into an increasingly narrow corridor of Southeast Asia. The consequences of this consolidation are now being felt across EV battery supply chains, stainless steel markets, and Western industrial policy in ways that are only beginning to register with mainstream investors.

Understanding what is unfolding between Indonesia and the Philippines requires more than tracking commodity prices. It requires appreciating how structural supply concentration, resource nationalism, and coordinated policy can combine to fundamentally reset the economics of an entire mineral sector. The Indonesia and the Philippines nickel supply coordination now underway is precisely this kind of structural inflection point.

When big ASX news breaks, our subscribers know first

Why Two Nations Now Hold the World's Nickel Supply in Their Hands

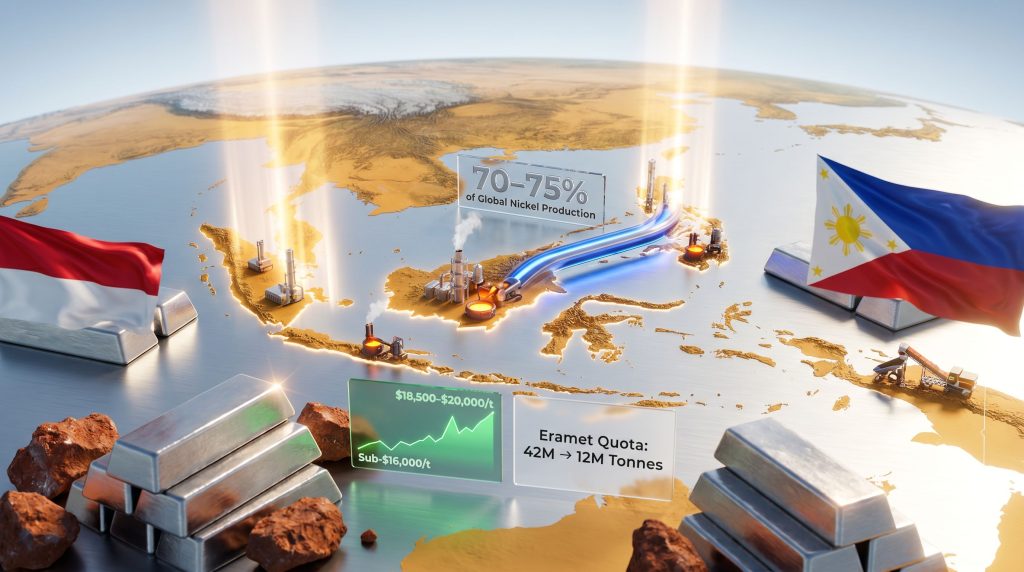

The numbers alone tell a compelling story. Indonesia and the Philippines together account for an estimated 70 to 75 percent of global nickel production as of 2025, a level of geographic concentration in a single critical mineral that is historically unusual. For context, OPEC's most influential period of pricing power came when member nations controlled a similar share of global oil output. What is different here is the absence of Western-aligned alternatives capable of stepping into that gap at comparable scale.

This concentration did not happen overnight. It developed across more than a decade of Indonesian investment in downstream nickel processing, including smelting, Nickel Pig Iron production, and High Pressure Acid Leach technology. While Western markets debated supply chain resilience in policy documents, Indonesia was building the physical infrastructure that now underpins a commanding share of global nickel supply.

The Philippines, by contrast, has remained primarily an ore exporter, possessing substantial laterite nickel reserves but lacking the downstream processing infrastructure that Indonesia has developed. This asymmetry is precisely what makes the bilateral coordination between the two nations so structurally significant. Furthermore, the Indonesian nickel industry has been a key driver of this growing imbalance in regional processing capacity.

What the IndoPhil Nickel Corridor Actually Is

A Framework Built on Complementarity

The IndoPhil Nickel Corridor is a formal bilateral cooperation structure built around five memoranda of understanding, covering distinct but interconnected areas of collaboration. It was signed by nickel industry associations from both countries and witnessed by senior government representatives, giving it an institutional weight that separates it from informal pricing signals or unilateral export policy adjustments.

The core pillars of the framework include:

- Joint coordination of nickel industry development across both nations

- Technology transfer in downstream processing and smelting operations

- Integration of Philippine laterite ore supply with Indonesian processing infrastructure

- Shared mechanisms targeting resilience in EV battery and stainless steel supply chains

- A working group structure for ongoing policy alignment between the two governments

The strategic logic underpinning this arrangement is straightforward: the Philippines has the ore, Indonesia has the processing infrastructure. By linking these two complementary capabilities rather than competing at the raw ore level, both nations can capture a greater share of the value generated across the nickel supply chain. According to reporting from Asian News Network, officials from both countries have framed this arrangement as a long-term strategic priority rather than a short-term market play.

The Nickel Corridor represents a deliberate move up the mineral processing value chain by two nations that previously exported much of their mineral wealth at commodity prices. The agreement is fundamentally about value retention, not just supply management.

What This Signals About Supply Intent

For investors and market analysts who questioned whether Indonesia's supply discipline would hold, the bilateral agreement provides meaningful clarification. It demonstrates that supply coordination is not a unilateral Indonesian experiment but a regionally shared policy orientation with institutional backing. Any reversal would now require not one government to change course, but two, along with the industry associations and hundreds of stakeholder companies that have already benefited from the new pricing environment.

Indonesia's Supply Management: The Policy Mechanics That Moved the Market

Quota Reductions and Their Market Impact

Before the bilateral corridor was formalised, Indonesia had already demonstrated its willingness to exercise supply discipline through quota-based output management. The most cited example involves a major reduction affecting Eramet's ore quota, which was cut from 42 million tonnes to 12 million tonnes. This single policy adjustment removed an estimated 300,000 tonnes of nickel from global supply, representing approximately 10 percent of global nickel output, a material shock by any commodity market standard.

The price response was measurable. Nickel, which had been trading well below $16,000 per tonne during the prolonged downturn, recovered into the $18,500 to $20,000 per tonne range, with the metal approaching $20,000 briefly before pulling back. Monitoring Indonesian nickel price trends over this period reveals the direct correlation between quota announcements and upward price movements. As of recent trading, nickel has been holding just under $19,000 per tonne, consolidating gains that many institutional investors initially dismissed as unsustainable.

| Policy Lever | Pre-Reform Position | Post-Reform Outcome |

|---|---|---|

| Eramet Ore Quota | 42 million tonnes | 12 million tonnes |

| Estimated Nickel Removed from Market | Baseline | |

| Indonesian Miner Revenue per Tonne | Baseline | Approximately 50% higher |

| Nickel Price Range | Below $16,000/t | $18,500 to $20,000/t |

The Minimum Price Formula: Building a Structural Floor

Alongside quota management, Indonesia introduced a minimum price formula for nickel ore, designed to establish a price floor that transfers economic value away from Chinese-controlled processing companies and toward domestic Indonesian mining operations. The formula was initially calibrated too aggressively, then adjusted to a more moderate level, but its existence represents a permanent change to the pricing environment rather than a temporary intervention.

The economic redistribution produced by these policies is significant:

- Hundreds of Indonesian mining companies are now receiving approximately 50 percent more revenue per tonne of ore compared to six months prior to the reforms

- The Indonesian government is collecting substantially higher tax and royalty revenues from the sector

- Vertically integrated operators, including Chinese companies with direct mine ownership such as Tsingshan and its associated entities, absorb higher input costs on the processing side but benefit from higher ore valuations on the mining side, partially insulating them from the policy shift

This last point is critical for understanding why the reversal thesis fails structurally. Vertically integrated operators with direct economic interests in both mining and processing have a more nuanced relationship with the new pricing regime than pure-play processors, reducing the lobbying pressure for policy reversal that sceptics anticipated.

The Reversal Thesis and Why the Evidence Does Not Support It

Why Smart Capital Initially Missed the Nickel Recovery

A meaningful portion of institutional investors missed a $4,000 per tonne price move in December, anchored to a thesis that Indonesia's supply discipline would not hold. The scepticism was not irrational at face value. Indonesia has a history of policy inconsistency in resource management, and the presence of powerful Chinese industrial interests in its nickel processing sector created a plausible narrative for reversal.

The reversal argument, however, requires accepting a specific sequence of events:

- The Indonesian government voluntarily surrenders substantially higher tax and royalty revenues it has already collected

- Hundreds of Indonesian mining companies accept a roughly 50 percent reduction in per-tonne revenues they have already been receiving for months

- Policy is reversed specifically to benefit Chinese-controlled processing companies at the direct expense of domestic Indonesian economic interests

Each step in this sequence runs contrary to observable political economy incentives. Governments do not routinely surrender realised revenue streams. Domestic mining constituencies that have benefited from higher prices are a politically active force. And the largest vertically integrated Chinese operators are, as noted, partially hedged against the cost increases by their mining-side gains.

As confidence builds that Indonesian supply discipline is durable, the pool of sceptical institutional capital that missed the initial move becomes a source of continued buying pressure. The psychological shift from scepticism to conviction is itself a market catalyst.

Consequently, nickel price momentum is increasingly being viewed by analysts as structurally supported rather than speculative, reinforcing the case for sustained investor interest in the sector.

The Discovery Deficit: Why New Supply Cannot Fill the Gap

A Resource Map That Has Not Changed Since the 1980s

One of the least appreciated dimensions of the nickel supply story is the near-total absence of major new laterite nickel discoveries over the past four decades. The last laterite nickel deposit discovered at meaningful scale was identified in the 1980s, meaning the global resource map for high-grade laterites has been essentially static for over 40 years.

The significance of this discovery deficit becomes clear when set against demand growth. The global nickel market is now approximately 10 times larger than it was in the mid-1980s. Deposits that appeared commercially significant when they were discovered may be marginal relative to current demand requirements, particularly as the market moves toward an estimated 5 million tonnes per annum requirement driven by EV battery and stainless steel demand growth.

Potential new supply sources exist in theory. Deposits in Ivory Coast and Guatemala have been identified, but even aggregating their combined potential contribution does not materially alter the fundamental supply picture. Indonesia remains, in practical terms, the Saudi Arabia of nickel, possessing a resource base with no credible peer elsewhere in the world.

The Aluminum Parallel: A Historical Template for What Happens Next

The aluminum sector provides a useful historical analogy for understanding how Chinese industrial strategy navigates supply constraints. The sequential pattern followed in aluminum involved:

- Exhausting domestic Chinese bauxite reserves

- Sourcing from Indonesian bauxite deposits, initially dismissed by Western producers as the wrong chemistry for conventional processing

- Moving to Guinea after Indonesian supply became constrained

The challenge in nickel is that this sequential fallback pattern has fewer available steps. Indonesia is not simply the current preferred source but the dominant global reserve base. There is no Guinea equivalent waiting in the wings for nickel. This structural reality strengthens the pricing power of the Indonesia-Philippines coordination over any comparable arrangement in aluminum.

Deep-Sea Nodule Mining: Context and Realistic Contribution

Deep-sea polymetallic nodule mining has advanced in permitting terms. The National Oceanic and Atmospheric Administration (NOAA) confirmed compliance on a key permit application, moving the relevant project to the next stage of the approval process. A partnership with deep-sea infrastructure specialist Allseas targets nodule extraction at 3 million tonnes per annum by 2027, which would yield an estimated 35,000 tonnes of nickel annually.

However, critical context is required here. Polymetallic nodules are primarily manganese-bearing, meaning their near-term market impact will be most significant in the manganese supply chain rather than nickel. At projected production volumes, the nickel contribution from deep-sea mining represents a small fraction of the supply removed by Indonesia's quota cuts alone. It is not a credible near-term substitute for conventional nickel supply, and market commentary suggesting otherwise overstates its relevance to the current nickel price environment.

The next major ASX story will hit our subscribers first

EV Battery Supply Chains and the Concentration Risk Premium

Nickel is a primary input in NMC (Nickel Manganese Cobalt) and NCA (Nickel Cobalt Aluminium) battery chemistries, which are preferred for high-energy-density EV applications where range is a priority. The role of nickel in the energy transition is therefore central to understanding why supply concentration carries such significant strategic implications. The concentration of roughly three-quarters of global nickel supply in two countries creates a single-region dependency risk that Western battery manufacturers and EV producers are only beginning to price into their procurement strategies.

The bilateral coordination between Indonesia and the Philippines amplifies this risk. Any coordinated supply restriction, quota adjustment, or geopolitical disruption now affects the majority of global nickel supply simultaneously, rather than creating a partial disruption that other sources could absorb.

Western governments have begun responding with capital deployment. Canada's announcement of $25 billion in new funding directed toward major critical mineral projects reflects the strategic intent to develop Western-aligned nickel supply chains capable of reducing dependency on Chinese-controlled processing infrastructure. Projects that are well-advanced in permitting, located in stable jurisdictions, and capable of contributing to supply chain diversification are the intended beneficiaries of this institutional capital.

The Investment Landscape: Scarcity, Psychology, and Asymmetric Opportunity

The Exploration Drought and Its Consequences

Four years of suppressed nickel prices have effectively eliminated a generation of exploration activity. Weekly drill result monitoring services report approximately 100 gold intervals and 25 silver intervals for every zero to five nickel intervals in a typical week. Rare earth intervals outnumber nickel intervals in most reporting periods. This exploration drought has created a structural scarcity of credible, advanced-stage nickel development projects at precisely the moment when institutional capital is beginning to rotate back into the sector.

For investors, the implication is straightforward. When capital returns to nickel at scale, it will chase a small number of surviving stories. Projects that maintained development momentum through the price downturn, advancing permitting, resource definition, and feasibility work while competitors exited the sector, now occupy a structurally advantaged position. In addition, the broader nickel market recovery narrative is beginning to attract renewed attention from fund managers who previously avoided the sector entirely.

Key Investment Thesis Components for Advanced Nickel Projects

- Permitting proximity as a de-risking catalyst that reduces capital requirement uncertainty

- Western jurisdiction premium as supply chain decoupling from Chinese-controlled processing accelerates

- Capital scarcity in nickel relative to gold and silver, creating re-rating potential as inflows concentrate in few available stories

- Institutional capital tailwinds from government-backed critical mineral programmes in Canada and other Western nations

- Drill interval scarcity creating a visibility premium for projects that continue to generate exploration results

In commodity sectors where new supply discovery has stalled and a prolonged price suppression period is followed by a structural demand catalyst, the projects that survived the downturn with development timelines intact typically capture a disproportionate share of the subsequent capital rotation.

Drilling Quality and Grade Thresholds

Not all nickel intervals are equal, and understanding grade thresholds matters for evaluating exploration results. Recent drilling in the Timmins district of Ontario produced a 35-metre interval grading 1 percent nickel, a result that attracted attention specifically because grades above 1 percent nickel are considered noteworthy in the current exploration environment.

As the wider sector has contracted, the bar for what constitutes a meaningful drill result has become more clearly defined, with sub-1-percent intervals in shallow targets drawing far less institutional interest than higher-grade intersections at depth. Copper-nickel projects in jurisdictions such as Botswana are drilling to depths of 1,500 to 2,000 metres to connect known deposits, raising the question of whether the economics of extracting mineralisation at those depths will prove viable at feasibility study stage. Depth is a material cost variable, and projects that carry high-grade mineralisation at accessible depths carry a meaningful structural advantage over deep targets requiring expensive infrastructure.

Monitoring the Signals: What to Watch

For investors and market participants seeking to track the durability of the Indonesia and the Philippines nickel supply coordination, three forward indicators are worth monitoring closely:

- Minimum price formula adjustments in Indonesia, which serve as a real-time signal of the government's commitment to its pricing architecture. Formula adjustments that move the floor higher indicate strengthening resolve; rollbacks would signal political pressure from processing interests

- Philippine ore export volumes and any quota announcements under the Nickel Corridor framework, which will indicate how seriously the Philippines is implementing supply discipline as a partner rather than a passive participant

- Institutional capital flows into Western nickel development projects, particularly those in permitting-adjacent stages, which will serve as a leading indicator of whether mainstream investment sentiment has shifted from scepticism to conviction on the durability of the supply coordination

The structural forces now converging in nickel are not cyclical. Supply concentration at historically unusual levels, a decades-long discovery deficit, accelerating EV-driven demand, and the formal institutionalisation of bilateral supply coordination between the world's two largest nickel producers represent a combination of factors that the market is only beginning to fully discount. Furthermore, as Mining.com has reported, the formal signing of cooperation agreements between the two nations' industry bodies marks a meaningful escalation beyond informal price signalling. The Indonesia and the Philippines nickel supply coordination is not a temporary intervention in a commodity cycle. It is a reconfiguration of who controls the world's nickel supply and on what terms they are willing to provide it.

This article is intended for informational purposes only and does not constitute financial or investment advice. Commodity price forecasts, supply projections, and policy outcomes discussed herein involve uncertainty and should not be relied upon as the basis for investment decisions. Readers should conduct their own due diligence and consult qualified financial advisers before making investment decisions related to any securities or commodity markets referenced in this article.

Want to Track the Next Major Nickel Discovery Before the Market Catches On?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries — cutting through complex data to surface actionable nickel and critical mineral opportunities the moment they hit the exchange, making it ideal for investors positioning ahead of the capital rotation now building in the sector. Explore how historic mineral discoveries have generated extraordinary returns, then start your 14-day free trial at Discovery Alert to ensure you're among the first to know when the next major find is announced.