July 11, 2026

The Architecture of Energy Resilience: Why Bypass Routes Matter More Than Ever

Every major disruption to global oil markets in the past five decades has ultimately traced back to the same fundamental vulnerability: the concentration of crude transit through a handful of narrow maritime passages. When those corridors face genuine operational risk, the question stops being theoretical and becomes intensely practical. How much volume can actually move around the problem? The answer, in mid-2026, is not enough — and the UAE oil pipeline bypass Hormuz strategy is spending aggressively to change that.

The announcement confirmed by Abu Dhabi's media office in May 2026 that the UAE would accelerate construction of a new oil pipeline to double export capacity through Fujairah represents more than a single infrastructure decision. It signals a fundamental recalibration of how a major Gulf producer thinks about sovereign revenue protection when the waterway it depends on becomes a conflict zone rather than a trade corridor. (Reuters, Ahmed Elimam, Jana Choukeir, and Youssef Saba, May 15, 2026)

When big ASX news breaks, our subscribers know first

The Strait of Hormuz as a Systemic Concentration Risk

Understanding why the UAE oil pipeline bypass Hormuz strategy matters requires first appreciating the structural peculiarity of the strait itself. It is not simply a busy shipping lane. It is the single point through which an outsized share of the world's seaborne crude must pass, creating a concentration of crude oil trade geopolitics risk that has no parallel anywhere on the planet.

The waterway sits between the Persian Gulf and the Gulf of Oman. At its narrowest navigable point, the passage leaves very little room for alternative routing — tankers must queue through a constrained corridor before entering open ocean shipping lanes. Under normal operating conditions, the volume of petroleum liquids transiting the strait daily represents roughly one in every five barrels consumed globally.

Who Bears the Most Exposure?

The geographic reality of Hormuz dependency is not distributed evenly. Asian importing nations sit at the sharp end of this risk because their proximity to Gulf producing states has historically made Persian Gulf crude the most cost-efficient supply source available to them.

- Japan and South Korea have extremely limited alternative supply routing and depend heavily on uninterrupted Gulf crude flows to feed their refinery systems.

- China has developed partial overland pipeline alternatives through Central Asia, but these cannot come close to replacing seaborne Gulf imports at volume.

- India can theoretically reroute some supply via the Red Sea corridor, but this introduces different geopolitical exposure including Houthi maritime activity at the Bab el-Mandeb passage.

- European buyers have greater flexibility through Suez Canal routing or the Cape of Good Hope, but face significant added freight cost and delivery time.

- The UAE itself, as an exporter rather than an importer, faces a different category of risk: its ability to monetise its oil production becomes contingent on whether tankers can leave the Persian Gulf at all.

The core asymmetry of Hormuz risk is that disruption punishes exporters and importers simultaneously, but through entirely different mechanisms. Importers face supply shortfalls. Exporters face revenue lockout. The UAE's pipeline strategy is a direct response to the latter.

The Abu Dhabi Crude Oil Pipeline: Engineering a Way Around Hormuz

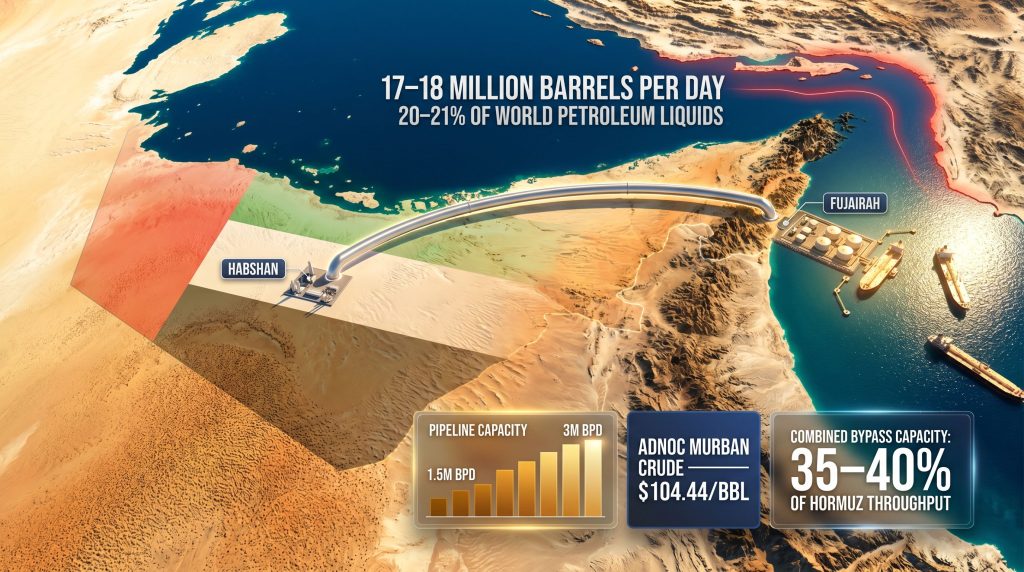

The UAE's existing infrastructure answer to Hormuz vulnerability is the Abu Dhabi Crude Oil Pipeline (ADCOP), an overland crude transit corridor operated by ADNOC that entirely circumvents the strait by connecting interior oil fields to a coastal export terminal on the Gulf of Oman. Furthermore, OPEC's global oil influence on production quotas adds another layer of complexity to how much volume these bypass routes can realistically handle.

The pipeline originates at the Habshan production complex in Abu Dhabi's interior and terminates at the Fujairah export terminal. By delivering crude to a port that sits east of the Strait of Hormuz, tankers loading at Fujairah can proceed directly into international shipping lanes without entering the Persian Gulf at all.

ADCOP Infrastructure at a Glance

| Specification | Detail |

|---|---|

| Operator | ADNOC (Abu Dhabi National Oil Company) |

| Origin Point | Habshan, Abu Dhabi interior |

| Terminus | Fujairah export terminal, Gulf of Oman |

| Pipeline Length | Approximately 370 kilometres |

| Design Capacity | Approximately 1.5 million barrels per day |

| Year Commissioned | 2012 |

| Construction Cost | Approximately $4.2 billion |

What makes Fujairah strategically significant beyond its bypass function is its dual identity as both a crude export terminal and one of the world's major bunkering hubs. The port provides maritime fuel services to vessels transiting the region, meaning it maintains a permanent operational ecosystem of tanker traffic, storage infrastructure, and logistics capacity. According to Al Jazeera's analysis of Gulf pipeline capacity, the Fujairah free zone has progressively been developed with this permanent strategic role in mind, not merely as a contingency facility.

Why the UAE Is Pushing Construction Forward Now

The decision to accelerate pipeline construction rather than continue on a standard development timeline reflects the changed threat environment surrounding the Strait of Hormuz in 2025 and 2026. With the strait described as largely shuttered due to the Iran conflict scenario, the calculus around bypass infrastructure has shifted from long-range planning to immediate operational necessity.

Several converging pressures explain the urgency:

- Active conflict dynamics have materially elevated the probability that Hormuz access restrictions could persist beyond the short-term disruption horizon.

- Existing ADCOP capacity constraints mean that the volume of crude the UAE can reroute during a Hormuz disruption is currently capped well below total production levels.

- Asian and European buyer demand for supply certainty has intensified, with long-term crude supply agreements increasingly incorporating delivery guarantee provisions that require demonstrable bypass capability.

- The IEA has warned that global oil supply could fall below demand in 2026 if the Iran conflict scenario persists and Hormuz access remains constrained, a projection that has added institutional weight to the urgency argument. (Zawya, referenced reporting, 2026)

- ADNOC's stated ambition to push UAE production capacity beyond 5 million barrels per day requires commensurate export infrastructure that can function regardless of Hormuz status. Zawya reporting confirms that ADNOC Drilling has indicated readiness to expand UAE oil capacity past the 5 million bpd target if called upon to do so.

The project as announced targets a doubling of Fujairah's total export throughput capacity. If the existing ADCOP pipeline operates at or near its approximately 1.5 million bpd design capacity, doubling that throughput at Fujairah would represent a substantial expansion in the UAE's Hormuz-independent crude export capability.

Important Disclaimer: Specific capacity projections for the new pipeline and associated price impact estimates involve forward-looking assumptions that carry material uncertainty. Investors and market participants should treat scenario-based figures as analytical frameworks rather than confirmed outcomes.

Comparing the Gulf's Two Major Bypass Corridors

The UAE is not the only Gulf producer with Hormuz bypass infrastructure. Saudi Arabia has operated its East-West Crude Oil Pipeline for decades, connecting Eastern Province production to the Yanbu export terminal on the Red Sea coast and providing a route that entirely avoids the Persian Gulf. However, the oil market disruption caused by ongoing geopolitical tensions means both corridors are being scrutinised more closely than ever.

ADCOP vs. Saudi East-West Pipeline

| Metric | UAE ADCOP | Saudi East-West Pipeline |

|---|---|---|

| Destination Port | Fujairah, Gulf of Oman | Yanbu, Red Sea |

| Bypasses Hormuz? | Yes, fully | Yes, fully |

| Approximate Design Capacity | ~1.5 million bpd | ~5 million bpd |

| Secondary Risk Exposure | Gulf of Oman shipping | Red Sea, Bab el-Mandeb, Houthi activity |

| Strategic Status | Expanding under acceleration | Periodically utilised |

The critical limitation of both bypass systems is that even their combined theoretical maximum throughput falls well short of the volume that normally transits Hormuz under ordinary conditions. This structural gap means that neither route, nor both together, can serve as a systemic replacement for the strait as a global oil transit mechanism.

Saudi Arabia's Red Sea alternative introduces its own geopolitical risk layer. Houthi forces operating in the Red Sea have demonstrated the capacity to target commercial shipping and energy infrastructure, meaning that routing crude to Yanbu does not eliminate conflict exposure — it merely exchanges one risk category for another.

What Disruption Means for Global Oil Pricing

The market implications of sustained Hormuz access restrictions operate through several simultaneous channels. ADNOC set its June 2026 Murban crude official selling price at $104.44 per barrel, a pricing level that reflects the supply constraint environment and the premium associated with guaranteed delivery through Fujairah. (Zawya, 2026)

Murban crude, the UAE's primary benchmark blend, is notable for its relatively light and sweet characteristics that make it attractive to Asian refiners seeking efficient processing yields. When Fujairah-routed barrels carry a logistics premium over Persian Gulf-loaded alternatives, it reflects genuine buyer willingness to pay for supply certainty. Geopolitical trade tensions continue to amplify this premium across the broader energy complex.

The broader market impact framework involves several interconnected dynamics:

- Brent and WTI benchmark prices face sustained upward pressure as the uncertainty premium embedded in forward curves expands during prolonged disruption scenarios.

- Strategic petroleum reserve drawdowns across IEA member states provide a buffer mechanism, but their capacity to absorb sustained multi-month disruptions is finite and their deployment carries its own market signalling implications.

- Asian refinery margins tighten as alternative routing adds both freight cost and delivery time to supply chains that were optimised for Persian Gulf crude at standard transit speeds.

- JPMorgan has flagged that traditional stock and bond allocations may no longer provide adequate portfolio protection amid the Middle East conflict environment, a perspective that speaks to the broader market repricing of geopolitical risk into asset class correlation assumptions. (Zawya, JPMorgan analysis, 2026)

The next major ASX story will hit our subscribers first

The Infrastructure Gap: Quantifying What Bypass Routes Cannot Do

Perhaps the most important analytical point about the UAE oil pipeline bypass Hormuz expansion is understanding what it cannot achieve, not merely what it can. Replacing the Strait of Hormuz as a global energy transit corridor would require an infrastructure investment programme spanning multiple producing nations, covering pipeline, terminal, and storage capacity across entirely different geographic corridors.

The capital requirement for such a programme would run well into the tens of billions of dollars and would represent a multi-decade construction undertaking that no single state has committed to pursuing. The existing bypass infrastructure across the Gulf, when considered in aggregate, covers a meaningful but structurally insufficient share of normal Hormuz throughput.

Security Vulnerabilities That Are Rarely Discussed

One dimension of bypass infrastructure that receives insufficient analytical attention is the vulnerability of the pipelines and terminals themselves. Overland pipelines covering hundreds of kilometres across Gulf terrain pass through territory that could face interference in an escalated conflict scenario. Furthermore, sanctions on oil trade imposed on regional actors have demonstrated how rapidly supply chains can be reshaped by political decisions, adding yet another layer of risk to bypass route planning.

This creates what energy security analysts describe as a secondary target risk: as bypass infrastructure becomes more strategically significant, it also becomes more attractive as a pressure point for adversaries seeking to limit the UAE's ability to monetise production outside Hormuz-dependent channels. Infrastructure resilience, redundancy, and physical security investment must be factored into any comprehensive assessment of bypass capacity.

Experts warn that Gulf bypass plans remain far from complete, reinforcing that even accelerated construction timelines leave a significant window of vulnerability for producers reliant on Hormuz as their primary export corridor.

The Longer Strategic Logic Behind ADNOC's Expansion Push

The pipeline acceleration decision fits within a broader strategic framework that ADNOC has been building toward for years. The company's ambition to surpass 5 million barrels per day in production capacity requires that export infrastructure keep pace with upstream investment. Producing more crude than can be exported through reliable channels is not a production problem — it is a revenue problem.

By investing in permanent Fujairah export capacity rather than treating bypass infrastructure as a contingency measure, the UAE is signalling to long-term crude buyers that supply reliability is a core commercial proposition rather than a best-efforts commitment. This positioning matters particularly for Asian national oil companies and refining groups that sign multi-year supply agreements and need confidence that delivery terms can be met regardless of regional geopolitical conditions.

The Fujairah free zone's ongoing development as a permanent export hub, with deep storage capacity and direct access to major shipping lanes, reinforces this commercial signal. The terminal is increasingly positioned as a permanent feature of global crude trade infrastructure rather than a bypass option activated only during crises.

Frequently Asked Questions

What is the UAE's Hormuz bypass pipeline called?

The UAE's primary Hormuz bypass route is the Abu Dhabi Crude Oil Pipeline (ADCOP), which runs approximately 370 kilometres from the Habshan production complex in Abu Dhabi's interior to the Fujairah export terminal on the Gulf of Oman coast.

When did the ADCOP pipeline become operational?

The pipeline was commissioned in 2012 at a construction cost of approximately $4.2 billion and is operated by ADNOC.

Can the UAE fully replace Hormuz with its bypass infrastructure?

No. Even after the planned capacity expansion, UAE bypass infrastructure will represent only a fraction of the volume that transits the Strait of Hormuz under normal conditions. The pipeline provides meaningful protection for UAE crude revenue but cannot substitute for Hormuz as a global transit corridor.

Does Saudi Arabia also have a Hormuz bypass route?

Yes. Saudi Arabia's East-West Crude Oil Pipeline transports crude from the Eastern Province to the Yanbu export terminal on the Red Sea, entirely bypassing the Strait of Hormuz. Its design capacity significantly exceeds that of the current ADCOP system.

What is Murban crude and why does its pricing matter?

Murban is the UAE's primary crude benchmark, a relatively light and sweet blend produced by ADNOC that is particularly valued by Asian refiners for its processing efficiency. Its official selling price, set monthly by ADNOC, serves as a market signal for both UAE export competitiveness and the supply premium associated with Fujairah-routed delivery. ADNOC set the June 2026 Murban official selling price at $104.44 per barrel.

Why is Fujairah strategically important beyond just being a bypass terminal?

Fujairah's location on the Gulf of Oman east of the Hormuz passage allows tankers to load and depart directly into international shipping lanes without entering the Persian Gulf. The port is also one of the world's significant bunkering hubs, giving it a permanent operational role in global maritime commerce that extends well beyond its bypass function for UAE crude exports.

Disclaimer: This article contains forward-looking statements, scenario projections, and market analysis based on publicly available information as of May 2026. Readers should not treat any price projections, capacity estimates, or geopolitical scenario analyses as investment advice or confirmed outcomes. Energy market conditions, geopolitical developments, and infrastructure timelines are subject to material change.

Want To Stay Ahead of the Next Major Resource Discovery Driven by Shifting Energy Geopolitics?

As global oil infrastructure reshapes trade flows and commodity premiums, Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time, delivering instant, actionable alerts on significant mineral discoveries so investors can act before the broader market catches on — explore historic discovery returns or start your 14-day free trial at Discovery Alert today.